IRS Notices

CP3219A Notice of Deficiency: What It Means, Your 90-Day Deadline, and Every Option (2026)

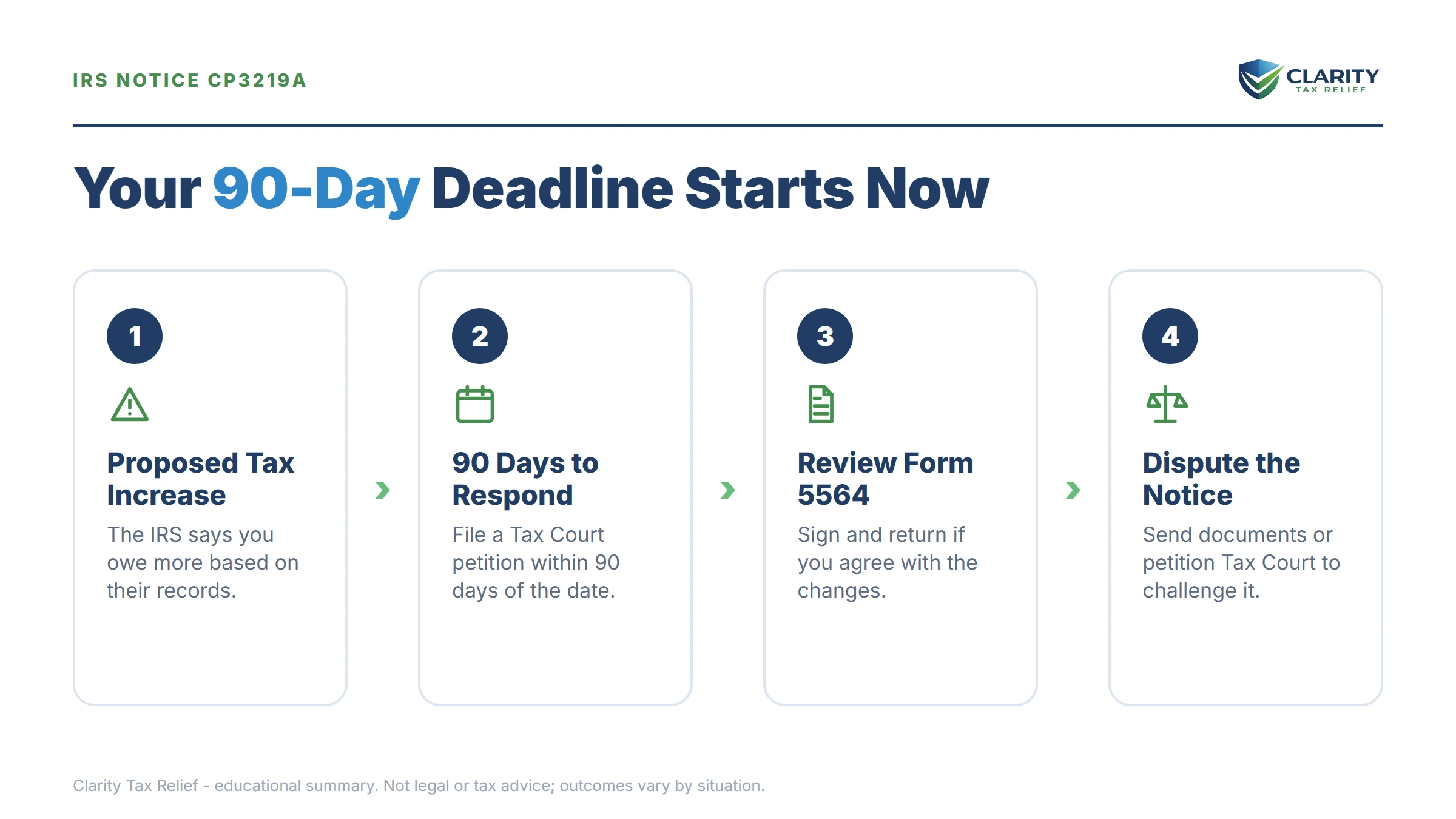

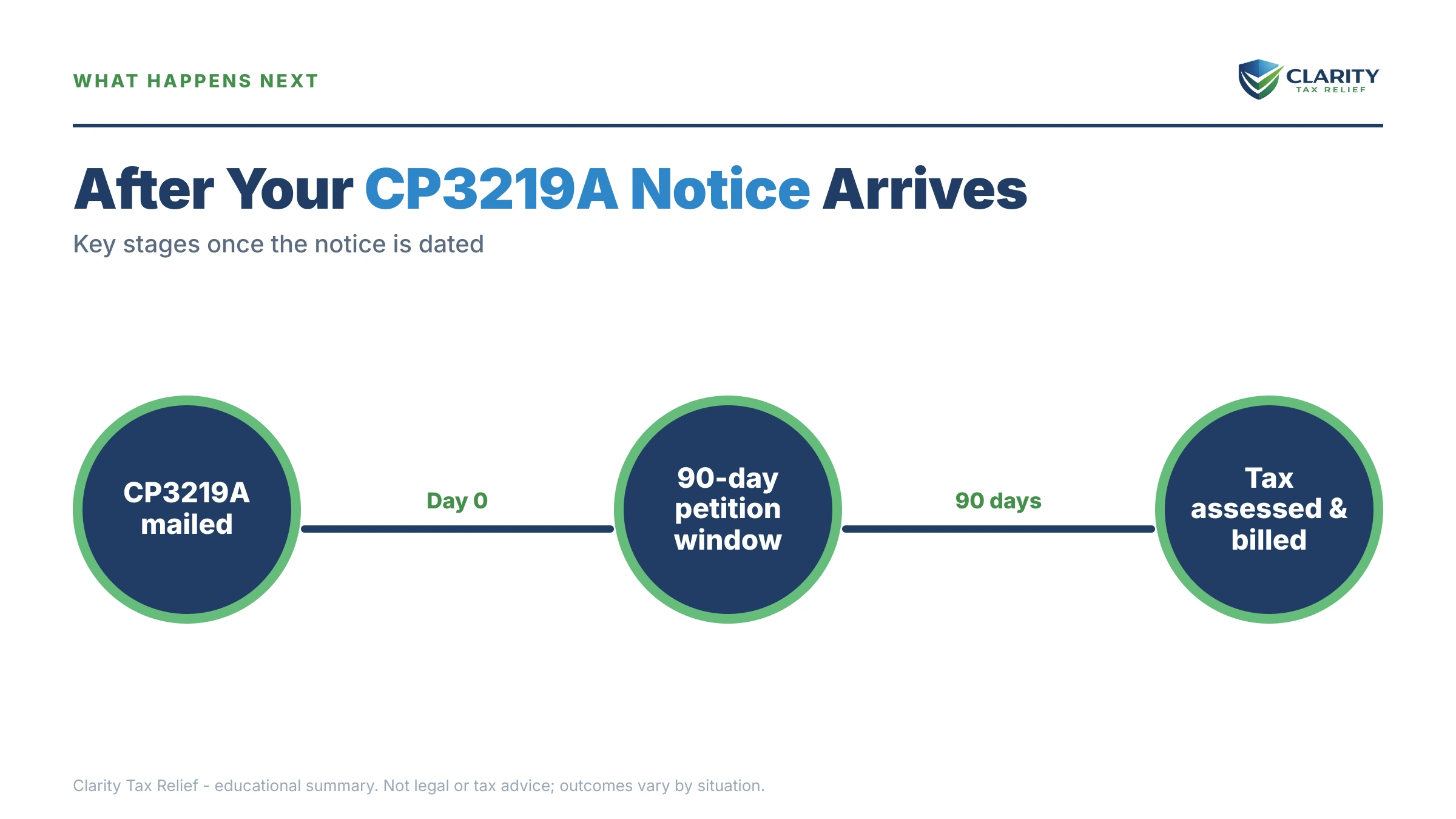

The short answer: a CP3219A notice of deficiency is the IRS's formal legal determination that you owe additional tax — usually after an unanswered or unresolved CP2000. You have 90 days from the date on the notice to either agree (Form 5564) or petition the U.S. Tax Court. That deadline is set by law and cannot be extended.

The envelope came certified, the header says "Notice of Deficiency," and the total could swallow two payroll runs. If you own a business, odds are a CP2000 proposal arrived months ago and got buried under deposits, invoices, and a busy quarter — and the IRS just converted that proposal into a formal legal determination.

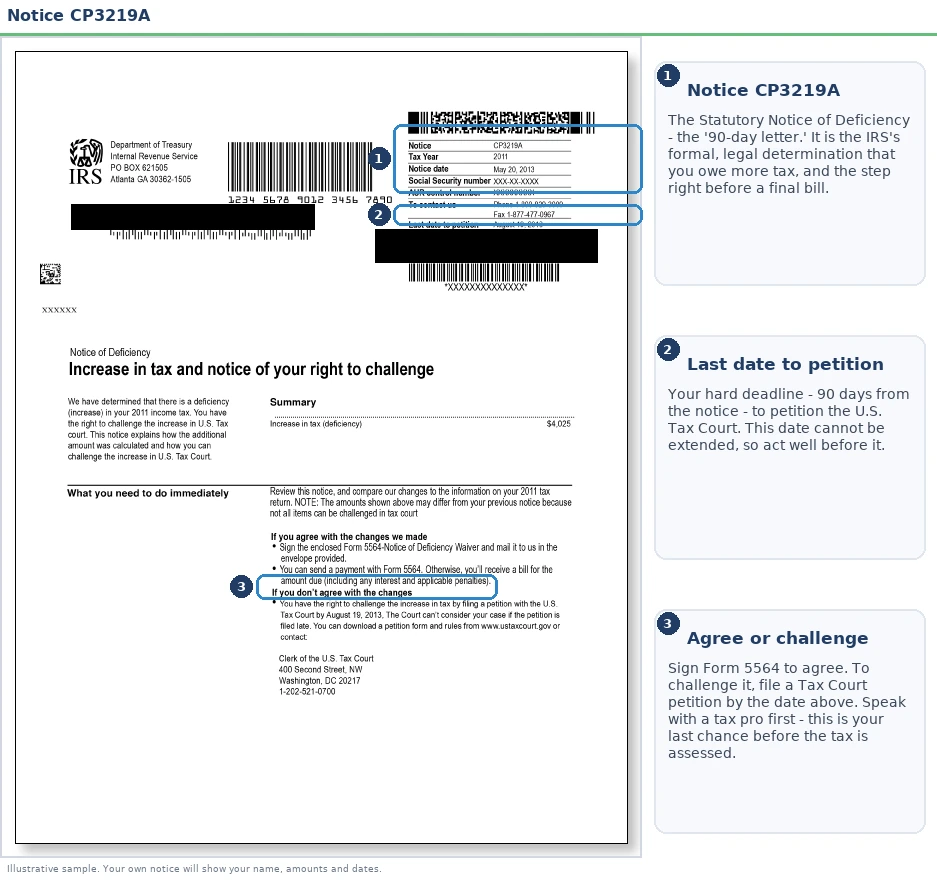

Here's the part that matters: this is the one IRS notice that hands you a courtroom-grade right, and a fixed window to use it. The image below shows exactly what a CP3219A looks like and where the single date that controls your case is printed — everything in this guide keys off that date.

⏱ Your deadline: you have 90 days from the date on your CP3219A — 150 days if the notice was addressed to you outside the United States — to file a petition with the U.S. Tax Court. The exact last day is printed on page one of the notice. Neither the IRS nor the Tax Court can extend it, and sending documents or calling the IRS does not pause it.

Why you got a CP3219A notice of deficiency

The IRS issues a CP3219A when it has formally decided your return understated your tax — most often because third-party income reports didn't match your return and the earlier proposal stage didn't resolve it. In practice, one of these happened:

- A CP2000 notice went unanswered. The IRS's underreporter program matched W-2s, 1099-NECs, 1099-Ks, and brokerage forms against your return, proposed changes, and heard nothing back within the response window.

- You responded, but the IRS wasn't persuaded. If your CP2000 disagreement lacked documentation — or crossed in the mail with the next stage — the system escalates anyway.

- An earlier CP2501 notice or CP2000 went to an old address. Here's the harsh rule: the IRS only has to mail the notice to your last known address. A CP3219A you never physically received still starts the 90-day clock.

For business owners, the most common trigger in 2026 is 1099-K and 1099-NEC income that never landed on a Schedule C or flowed through to the 1040 — often because a bookkeeper change, a payment-processor switch, or a busy payroll season broke the paper trail. The IRS computes tax on the gross amount reported to it, with none of your expenses, which is why the number on the notice usually looks inflated. That's not a scare tactic; it's how the matching program works, and it's exactly why disputing is often worth it.

If you're not sure this notice fits your situation at all, start with our decoder on why you got a letter from the IRS — but if the words "Notice of Deficiency" appear on page one, this is your page.

Where the 90-day letter sits in the IRS sequence

A CP3219A is the final stop in the underreporter process — the last notice before the IRS legally records the debt. Everything before it was a proposal; everything after it is collection. For the deeper mechanics of the deficiency procedure itself, see our CP3219A statutory notice of deficiency explainer; here's the sequence at a glance:

| Stage | Your response window | What it means |

|---|---|---|

| CP2501 — initial income mismatch inquiry | Typically 30 days | The IRS flags a discrepancy and asks you to explain — no tax proposed yet |

| CP2000 — proposed changes | Typically 30 days | The IRS proposes additional tax, penalty, and interest and invites agreement or dispute |

| CP3219A — statutory notice of deficiency | 90 days, fixed by law | Formal determination; your only window to dispute in Tax Court before paying |

| Assessment → CP14 bill | ~21 days to pay the CP14 | The deficiency posts to your account and becomes legally collectible |

| CP501/CP503 → CP504 → LT11 | Escalating; LT11 gives a final 30 days | The collection sequence that ends in liens, levies, and garnishment |

Don't confuse the CP3219A with its neighbors. The CP3219N is the deficiency notice for people who never filed at all — the IRS built a return for them. Letter 531 is the deficiency notice issued after a full audit rather than document matching. And a CP11 notice is a math-error correction the IRS can assess immediately, with no 90-day court window — a completely different procedure. The CP3219A's defining feature is that the IRS legally cannot assess the tax during your 90 days, or while a timely Tax Court case is pending.

What happens if you ignore a CP3219A

Ignoring a CP3219A converts a disputable proposal into a legally enforceable debt on day 91. The sequence from there is automated and runs in stages:

- Day 91 — assessment. The restriction on assessment lifts. The IRS records the full deficiency — tax, the accuracy-related penalty, and interest back to the return's original due date — on your account. The 10-year collection statute starts running, and your right to a prepayment court challenge is gone for good.

- The CP14 bill arrives. A CP14 notice demands payment, typically within about 21 days. Interest and the monthly failure-to-pay penalty now compound on the assessed balance.

- Reminder notices, then intent to levy. CP501 and CP503 reminders give way to the CP504, which lets the IRS take your state tax refund and signals that a federal tax lien is on the table — a serious problem if your business needs credit or bonding.

- Final notice, then enforcement. The LT11 or Letter 1058 starts a 30-day clock, after which the IRS can levy bank accounts — including business accounts — and garnish wages. Levied bank funds sit on a 21-day hold before they leave; a wage levy runs continuously until released.

Two 2026 realities sharpen this. First, the IRS workforce shrank roughly 27% in 2025, so fixing an assessment after the fact — reaching a human, getting reconsideration worked — is slower than ever, while the automated escalation never paused. Second, once your total assessed federal debt crosses $66,000, the IRS can certify it to the State Department, which can deny or revoke your passport. The cheapest, fastest version of this fight happens inside the 90 days.

Holding a CP3219A right now?

Your petition window is already counting down. Send us the notice and an experienced tax professional will tell you — free — whether the IRS's numbers hold up, whether the 20% penalty is contestable, and which track protects you before the last day printed on page one.

Your options during the 90 days

A CP3219A gives you exactly four moves, and the right one depends on whether the IRS's numbers are right — not on whether you can pay. Paying ability comes later; the 90 days is about locking in the correct amount.

| Response | Deadline | What happens next |

|---|---|---|

| Agree — sign and return Form 5564 | Anytime, but sooner is cheaper | The IRS assesses the amount; you then arrange payment before the CP14 escalates |

| Send corrections and proof to the IRS | Within the 90 days — but this does not pause the clock | The IRS can revise or withdraw the deficiency; if it hasn't resolved in writing, you still must petition |

| Petition the U.S. Tax Court | By the last day printed on the notice — no extensions | Assessment stays frozen; the case usually routes to IRS Appeals and settles without trial |

| Do nothing | — | Day 91: full assessment, then the collection sequence; the prepayment forum is lost permanently |

If the notice is right: sign Form 5564 (the waiver enclosed with the notice) and return it. This doesn't obligate you to pay on the spot — it just lets the IRS assess without waiting out the window, which stops additional stages from stacking up while you arrange payment. Balances of $50,000 or less generally qualify for a 72-month online installment agreement; under $25,000, a streamlined agreement requires no financial disclosure at all. Our guide to setting up an IRS payment plan online walks through it.

If the notice is partly right: you can agree to some items and contest others — including contesting only the penalty. The accuracy-related penalty is 20% of the underpayment and is removable for reasonable cause even when the tax itself stands.

If the notice is wrong: send documentation to the address or fax number on the notice immediately — expense records, a corrected 1099, proof the income was reported elsewhere on the return. The IRS genuinely does reverse CP3219As when the proof is clear. But treat this as a parallel track: with 2026 processing backlogs, written confirmation may not arrive before your deadline, and only a filed petition preserves your rights if it doesn't.

One trap to avoid: filing a Form 1040-X amended return during the 90 days does not stop the clock or replace a petition. The IRS may process it, or may not process it in time — and if the window closes first, the deficiency gets assessed regardless.

How the Tax Court petition actually works

Filing a Tax Court petition costs $60 and does not commit you to a trial. You file electronically through the court's DAWSON system or by mail, using the simple petition form on the court's website; a fee waiver is available if you can't afford the $60. If your disputed amount is $50,000 or less per tax year, you can elect the small tax case ("S case") procedure — relaxed rules, no formal legal briefs, built for self-represented taxpayers.

What filing really buys you: the IRS remains barred from assessing or collecting while the case is pending, and your file gets routed to the IRS Independent Office of Appeals, where the large majority of docketed cases settle. In effect, the petition forces the substantive review your CP2000 response should have gotten. For the mechanics — what goes in the petition, how the calendar works, what settlement looks like — see our full guide to the 90-day letter and Tax Court petition.

One caution: the deadline is brutal in a way most IRS deadlines aren't. A petition postmarked or e-filed on the last printed day counts; one day late and the court almost certainly cannot hear your case, no matter how good your facts are.

Worked example: the IRS says you owe $27,500

This is a hypothetical to show the math — not a client story. Say you run a small contracting business with three employees on payroll. A general contractor client reported $65,000 in 1099-NEC payments to the IRS for 2024 that never made it onto your Schedule C — a bookkeeping handoff dropped them. Your CP3219A shows:

- Additional tax on $65,000 of unreported gross income: $22,500

- Accuracy-related penalty (20% × $22,500): $4,500

- Interest to date: $500

- Total deficiency: $27,500

But that $65,000 was gross. Your records show $38,000 of subcontractor labor and materials tied to those jobs. Netted correctly, the unreported profit is $27,000 — and the recomputed additional tax comes to roughly $9,500, not $22,500. The penalty recalculates too: 20% × $9,500 = $1,900. With interest, you'd be resolving something near $11,700 instead of $27,500 — a difference of roughly $15,800, all of it riding on whether you document expenses inside the 90-day window instead of after assessment. You can rough out how the penalty and interest side of your own notice grows over time with our Penalty & Interest Calculator — it estimates, it doesn't promise.

That's the pattern in most business-owner CP3219As: the IRS's tax figure is computed on gross reported income, and the taxpayer's job is proving the deductions the matching program can't see.

What if the 90 days already passed

Missing the CP3219A deadline closes the Tax Court door, but it does not make a wrong assessment permanent. Three routes remain — all slower and all at the IRS's discretion, which is why the 90 days matters so much:

| Option | Best for | Trade-off |

|---|---|---|

| Audit reconsideration | You have documentation the IRS never considered (expense records, corrected 1099s) | Discretionary and slow in 2026; collection can continue while it's pending unless you get a hold |

| Offer in Compromise — doubt as to liability | You dispute that you legally owe the assessed amount at all | Filed on Form 656-L with a full written case; the IRS decides, and approval is far from automatic |

| Pay, then claim a refund | Strong facts plus the ability to pay first and litigate in district court if denied | Requires paying the disputed amount up front — usually impractical for business owners |

| Payment plan, hardship (CNC) status, or a collectibility-based OIC | The amount is correct but you can't pay it | Resolves the debt, not the dispute; interest continues on plans, and eligibility is means-tested |

If you're in this after-the-deadline position, sequence matters: get any wrong numbers challenged through reconsideration or a liability offer before negotiating payment on them, or you'll be paying on an inflated balance.

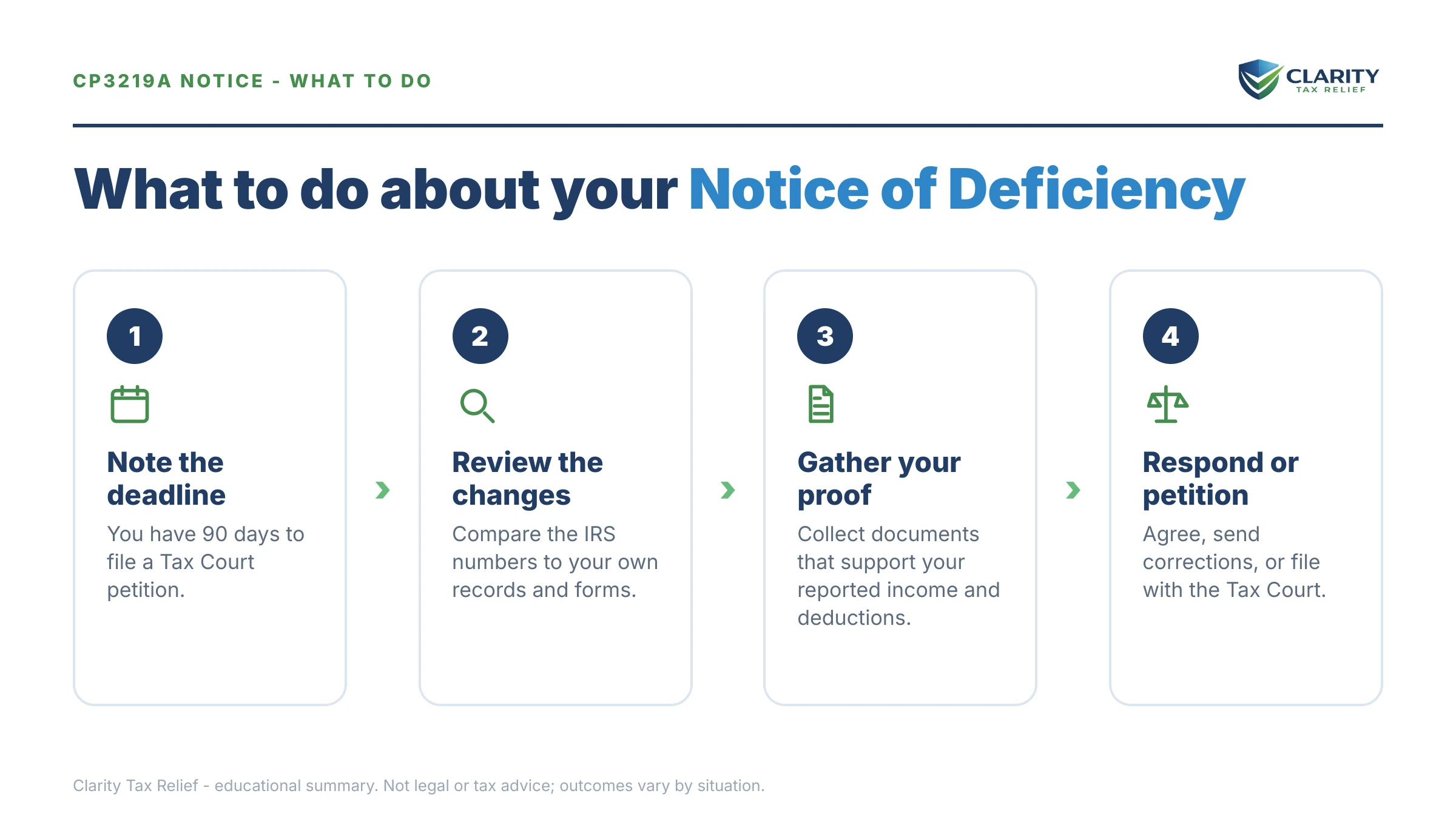

How to respond to a CP3219A, step by step

- Circle your deadline. Find the "Last day to file a petition with the United States Tax Court" date on page one — that printed date, not a rough 90-day count, controls everything.

- Verify the IRS's numbers. Pull your return for the year on the notice and match every income item the IRS added against your 1099s, W-2s, bank deposits, and business books.

- Pick your track. Agree in full (sign and return Form 5564), agree in part, or dispute — partial agreement is allowed, and the penalty can be contested separately from the tax.

- Send documentation immediately if the notice is wrong. Mail or fax proof to the contact on the notice — but treat it as a parallel effort, because it does not pause the 90-day clock.

- File the Tax Court petition before the printed date if anything is still disputed. File electronically through the court's DAWSON system or by mail; the fee is $60, a waiver is available, and filing preserves every right you have.

- Set up payment for whatever you truly owe. A payment plan arranged now prevents the assessment from rolling straight into the collection-notice sequence.

When you can handle this yourself

Plenty of CP3219A situations don't need professional help. You can confidently handle it alone if:

- The notice is simply right — you recognize the income, the math checks out, and the balance is one you can pay in full or on a straightforward plan. Sign Form 5564, set up the plan, done.

- The fix is one clean document — a 1099 that duplicated income you already reported, or a payer's corrected form. Send it with a short cover letter and calendar the petition deadline as your backstop.

- The dispute is small and simple — an S-case petition over one clearly documented item is genuinely manageable without a representative.

Experienced help changes outcomes in a different set of cases: business income where the real fight is reconstructing deductions (like the $27,500 example above), multiple tax years or a CP3219A layered on top of unfiled returns, payroll-adjacent debt where personal liability questions lurk, deficiencies large enough to threaten the $66,000 passport threshold, or a deadline that's days away. In those cases, the value isn't hand-holding — it's knowing which numbers the IRS will actually accept, and in what order to fight the tax, the penalty, and the payment terms.

If your notice involves business income and the deadline is inside 30 days, get your CP3219A reviewed free before you choose a track — the wrong first move here is expensive to unwind.

Terms on your notice, decoded

- Deficiency: the gap between the tax the IRS says you owe and the tax shown on your return — not yet a debt, until it's assessed.

- Statutory notice of deficiency (the "90-day letter"): the formal letter the law requires before the IRS can assess that gap, which opens your one prepayment window to go to Tax Court.

- Form 5564: the waiver enclosed with the notice; signing it means you agree and let the IRS assess without waiting out the 90 days.

- Assessment: the moment the debt is officially recorded on your IRS account — after which collection tools (bills, liens, levies) become available.

- Petition: the short filing that opens a Tax Court case; filing it on time freezes assessment until the case resolves.

- Accuracy-related penalty: the 20% addition most CP3219As include for a substantial or negligent understatement — contestable separately from the tax.

CP3219A questions, answered

Can the 90-day deadline on a CP3219A be extended?

No. The 90-day window (150 days if the notice was addressed to you outside the United States) is set by statute, and neither the IRS nor the Tax Court can extend it. Talking with the IRS, sending documents, or filing an amended return does not pause the clock. If you disagree and the deadline is approaching, file the petition — you can keep negotiating with the IRS afterward.

What happens if I ignore a CP3219A notice of deficiency?

On day 91, the IRS assesses the full amount shown — tax, penalty, and interest — and the balance becomes legally collectible. A CP14 bill follows, then the collection sequence that ends in liens and levies. You permanently lose the right to dispute the debt in Tax Court before paying; the remaining challenge routes, like audit reconsideration, are slower and entirely at the IRS's discretion.

What is the difference between a CP2000 and a CP3219A?

A CP2000 is a proposal — the IRS suggesting changes and inviting a response, typically within 30 days. A CP3219A is a formal legal determination that a deficiency exists, and it starts a fixed 90-day Tax Court clock. Most CP3219A notices are issued because a CP2000 went unanswered or the response didn't resolve the mismatch. The CP3219A is your last stop before assessment.

Do I need a lawyer to file a Tax Court petition?

No. You can represent yourself, and if your disputed amount is $50,000 or less per tax year, you can elect the simplified small tax case ("S case") procedure, which is designed for people without attorneys. The filing fee is $60, and a fee waiver is available if you can't afford it. That said, most petitioned cases settle with IRS Appeals before trial, and experienced representation often changes the settlement math on business-income cases.

What if I agree with the CP3219A but can't pay?

Sign and return Form 5564 to stop the case from dragging on, then set up a resolution before the bill escalates. Balances of $50,000 or less generally qualify for an online installment agreement of up to 72 months; short-term plans give you up to 180 days at no setup fee. Agreeing to the assessment and arranging payment are two separate steps — doing the first without the second just starts collection.

Can I still send information to the IRS after getting a CP3219A?

Yes — the notice tells you where to send documentation, and the IRS can revise or reverse the deficiency if your proof holds up. But submitting information does not stop the 90-day clock. If the IRS hasn't fully resolved the notice in writing as your deadline approaches, file the Tax Court petition anyway to preserve your rights; you can continue working the paperwork side afterward.

What if I missed the 90-day deadline on my CP3219A?

You can no longer go to Tax Court on that notice, but the debt is still challengeable. Audit reconsideration lets the IRS re-examine the assessment if you submit new documentation it hasn't considered. An Offer in Compromise based on doubt as to liability (Form 656-L) disputes whether you owe the amount at all. And if the number is right but unpayable, payment plans and hardship status still apply.

Does filing a Tax Court petition mean I'll go to trial?

Almost never. After you petition, the case is typically routed to the IRS Independent Office of Appeals, which settles the large majority of docketed cases without a trial. Filing the petition is best understood as preserving your right to dispute the debt before paying it — it freezes assessment while the case is pending and forces a real human review of your numbers.

Why does my CP3219A include a 20% penalty?

Most CP3219A notices add the accuracy-related penalty — 20% of the underpaid tax — on the theory that the understatement was substantial or negligent. That penalty is contestable separately from the tax itself: reasonable cause, reliance on a preparer, or documentation showing the income was actually reported can remove it even when some tax is owed. Interest is charged on top and keeps accruing until paid.

Your next 24 hours

- Find your date. Locate "Last day to file a petition with the United States Tax Court" on page one of the CP3219A and count the days you have left — that number decides how aggressive today needs to be.

- Gather your proof. Pull the tax return for the year on the notice, every 1099 and W-2 you received, and — if you're a business owner — the expense records and bank statements tied to the income the IRS added.

- Get the numbers checked before you choose a track. A free case review at the 2-minute form or (888) 825-7779 tells you whether to sign, correct, or petition — while all three doors are still open inside your 90 days.

Primary sources: the IRS's official page, Understanding your CP3219A notice; the United States Tax Court, where petitions are filed and the petition form and fee-waiver application live; and the Taxpayer Advocate Service, which can help when IRS processing delays threaten your rights.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.