IRS Letters

IRS Letter 531 Notice of Deficiency: Your 90-Day Tax Court Deadline (2026)

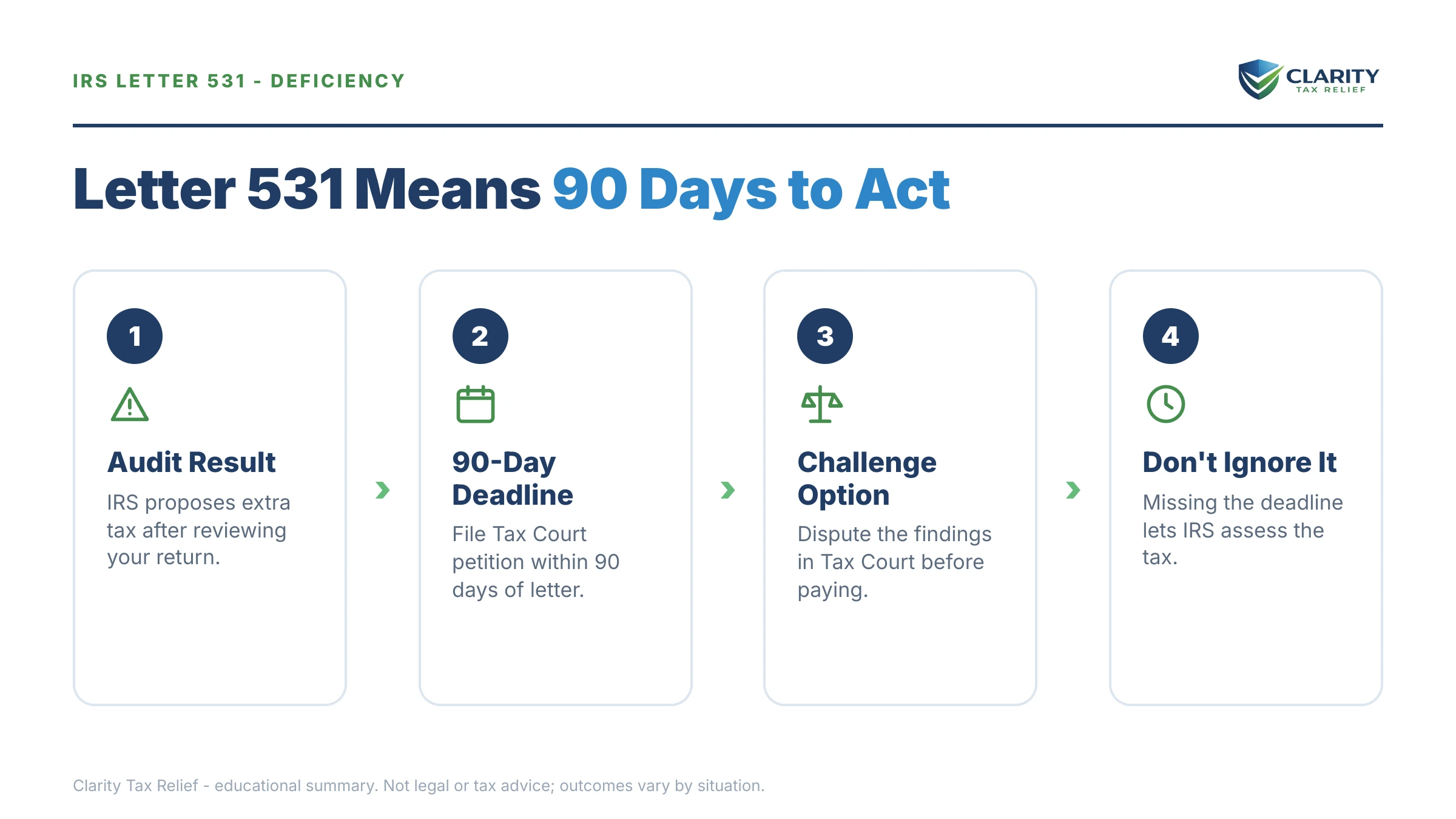

The short answer: IRS Letter 531 is a statutory notice of deficiency — the formal letter closing an audit and stating the extra tax the IRS intends to assess. You have 90 days from the date on the letter (150 if it was addressed to you abroad) to petition the U.S. Tax Court without paying first. That deadline cannot be extended.

A Letter 531 notice of deficiency means your examination is over — the auditor's numbers are now the IRS's official position, and the letter arrived by certified mail because it starts a legal clock. You sat through the audit, sent what you could, and this envelope is the government saying: this is our final figure, and here is your one chance to fight it before it becomes a bill.

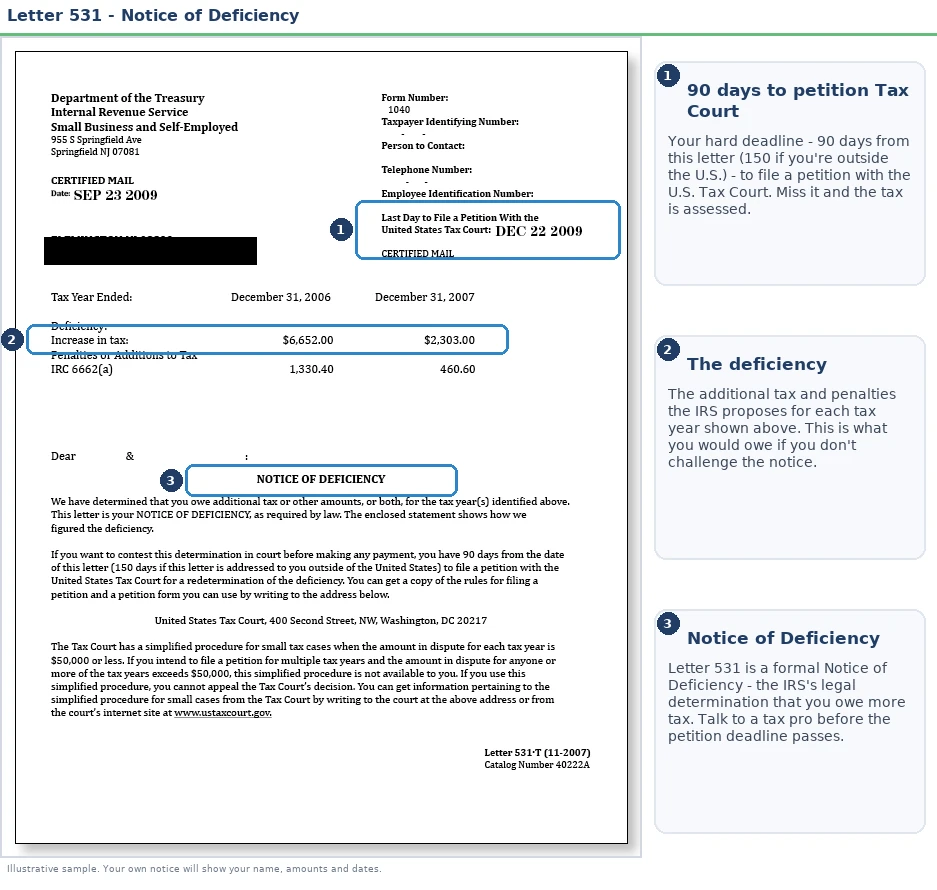

That sounds heavier than it is. Letter 531 is also the moment you hold the most leverage you will ever have in this case — a court door that stands open for exactly 90 days. The image below shows what a Letter 531 looks like and where the one date that controls everything appears, so you can find it on your own copy in seconds.

⏱ Your deadline: you have 90 days from the date on Letter 531 to file a petition with the U.S. Tax Court — 150 days if the letter was addressed to you outside the United States. The exact last day to file is printed on the letter itself. Neither the IRS nor the Tax Court can extend it, for any reason.

Why you got a Letter 531 notice of deficiency

Letter 531 is issued when an audit ends without your signed agreement. Somewhere before this letter, an examiner reviewed your return and proposed changes — usually on a Letter 525 irs audit report with Form 4549 attached, giving you roughly 30 days to agree or protest. You either disagreed, ran out of time, or never saw the earlier mail. The IRS then closes the exam by issuing the statutory notice.

The letter states the tax year (or years), the deficiency — the gap between the tax on your return and the tax the examiner says you owe — plus any penalties, such as the 20% accuracy related penalty irs examiners routinely add. Attached is Form 5564, a waiver you sign only if you agree with everything. For general background on why the IRS sends what it sends, see why did I get a letter from the IRS — this page stays focused on what makes a 531 different from every other envelope.

Letter 531 vs. CP3219A vs. CP3219N

All three are statutory notices of deficiency with identical legal force, but they come from different IRS pipelines. Letter 531 comes from a real examination — a human auditor built a file on your return. A cp3219a notice of deficiency comes from the automated underreporter computer after a CP2000 mismatch went unresolved. A CP3219N goes to people who never filed at all.

The distinction matters for strategy: because a 531 sits on a developed exam file, the IRS's position is usually more specific — and the points where the examiner over-reached are usually more findable. Your rights and deadline are the same on all three.

What your 90 days actually protects

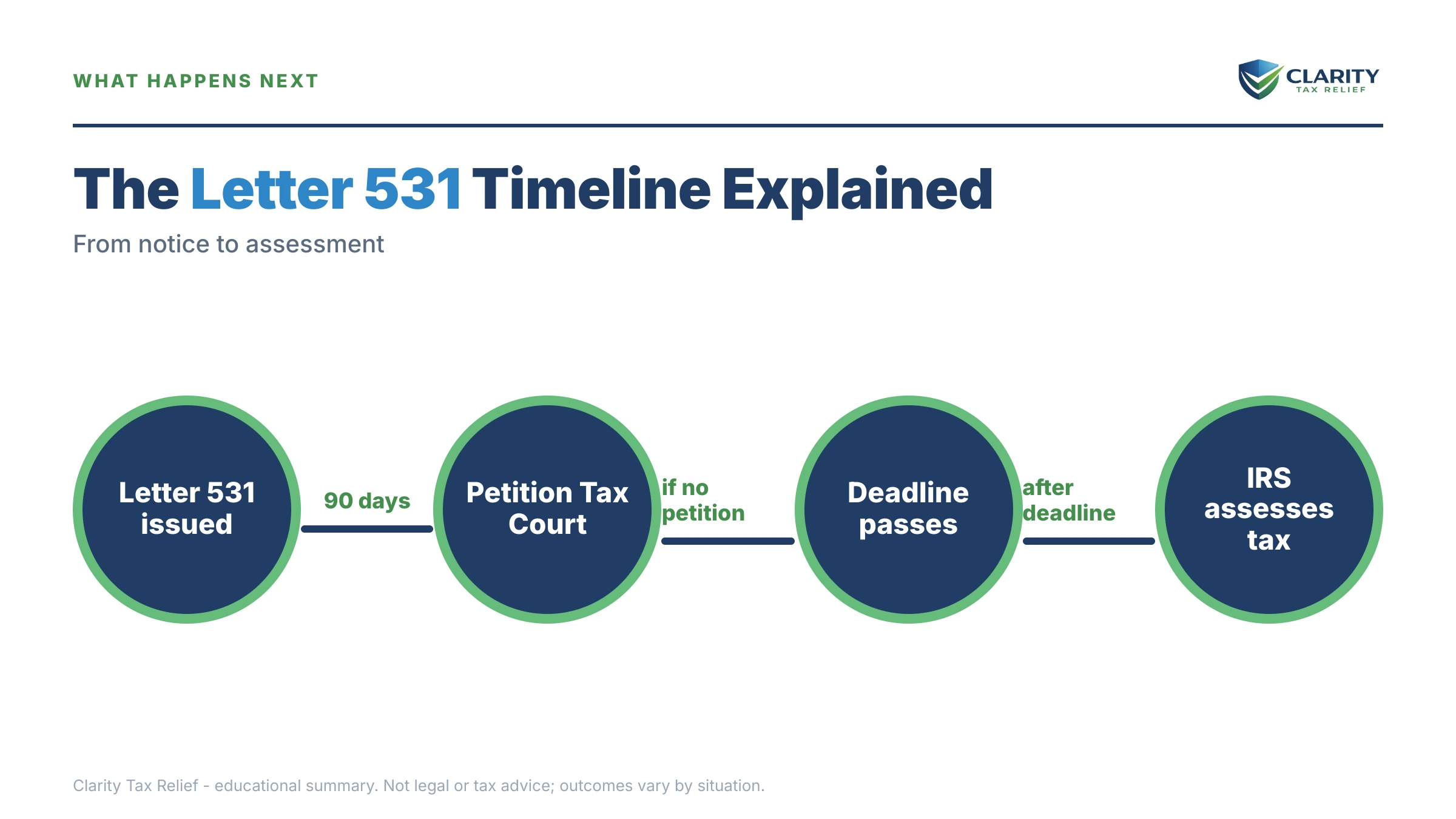

A timely Tax Court petition lets you dispute the tax before paying a dime — and legally blocks the IRS from assessing or collecting while your case is pending. That is why practitioners call Letter 531 the 90 day letter tax court petition trigger: the U.S. Tax Court is the only court with prepayment review of a tax dispute.

Miss the deadline and the entire posture flips. The IRS assesses the deficiency, collection begins, and your remaining court route is generally to pay the whole balance first and then sue for a refund. For most households, especially retirees on fixed incomes, "pay first" is not a real option — which makes the 90-day window the whole ballgame.

Two more things the letter's fine print won't emphasize. First, the clock runs from the IRS's mailing date, not the day you opened the envelope. Second, the notice is legally valid if it was mailed to your last known address — even if you moved and never received it.

Here is where a Letter 531 sits in the full audit-to-collection sequence:

| Stage | What arrives | Your window |

|---|---|---|

| Audit opens | Letter 566 or 2205-A exam contact | Respond by the date the examiner sets |

| Exam report | Letter 525 with Form 4549 (the "30-day letter") | Typically 30 days to agree or protest to Appeals |

| Deficiency — you are here | Letter 531, statutory notice of deficiency | 90 days to petition Tax Court (150 abroad) |

| Assessment | Balance-due bill for tax, penalties, and interest | Typically about 21 days to pay before reminders escalate |

| Enforced collection | CP504, then Letter 1058 / LT11 final notice | 30 days to request a Collection Due Process hearing before levy |

| Levy and lien | Bank or benefit levy; Letter 3172 lien filing | 21-day hold on bank levies; the lien becomes public record |

What happens if you ignore Letter 531

Ignoring a Letter 531 converts a disputable proposal into an enforceable debt. The sequence is automatic — no examiner has to touch your file again:

- Day 91 — your right to prepayment Tax Court review expires permanently. No late petitions, no exceptions.

- Assessment — the full deficiency, penalties, and interest post to your account. Interest has been running since that year's original due date and compounds daily.

- Billing — a balance-due notice arrives, then escalating reminders, each adding a failure-to-pay penalty of 0.5% per month.

- Intent to levy — a CP504, then a letter 1058 irs final notice. Thirty days after that, the IRS can levy bank accounts and take 15 percent of Social Security through the Federal Payment Levy Program — continuously, every month.

- Lien and passport — a letter 3172 notice of federal tax lien can make the debt public record, and once a balance is certified seriously delinquent at $66,000 or more (the 2026 threshold), the State Department can deny or revoke your passport.

In 2026, IRS staffing is down sharply — but every stage above is generated by automated systems that never got smaller. The machine escalates on schedule whether or not a human ever re-reads your audit file.

Holding a Letter 531 right now?

Your 90-day Tax Court window is already running, and the last day to file is printed on your letter. Send us a photo of it — an experienced tax professional will map your options against that exact date, free and confidential.

Your options when you receive Letter 531

Every Letter 531 response falls into one of seven paths, and the right one depends on two questions: are the numbers right, and has your deadline passed?

| Option | Deadline | Cost | Best when |

|---|---|---|---|

| Sign Form 5564 (agree) | Any time within the 90 days | The tax, penalties, and accrued interest | The numbers check out and you want to arrange payment |

| Tax Court petition — regular case | 90 days (150 abroad) | $60 filing fee | You dispute more than $50,000 for any single year |

| Tax Court petition — small (S) case | 90 days (150 abroad) | $60 filing fee | $50,000 or less in dispute per tax year; simplified rules |

| Keep working with the examiner or Appeals | Does not pause the 90 days | Free | You have new documents — but file the petition as backup |

| Audit reconsideration | After assessment (missed the window) | Free | You have information the examiner never saw |

| OIC — doubt as to liability (Form 656-L) | After assessment | No application fee | You dispute the amount itself but lost the court window |

| Pay in full, then claim a refund | After assessment | Full payment up front | Last-resort court route once the 90 days pass |

Two of these deserve emphasis. First, signing Form 5564 is one-way: it authorizes immediate assessment and ends your Tax Court rights for this deficiency, so sign only after verifying every adjustment. Second, if you miss the window, irs audit reconsideration and the offer in compromise doubt as to liability route can still correct a genuinely wrong number — they just do it from the weaker side of an assessed debt, with collection pressure running in the background.

A worked example: an $83,100 deficiency on a fixed income

Say you're retired, living mainly on Social Security and IRA withdrawals, and the IRS audited the year you sold a long-held rental property. The examiner disallowed part of your claimed basis and a capital-loss carryover you couldn't fully document. Your Letter 531 shows:

- Additional tax (the deficiency): $69,250

- Accuracy-related penalty at 20%: $69,250 × 0.20 = $13,850

- Total proposed: $83,100, plus interest compounding daily from the return's original due date

Here's what that number changes. Because $83,100 relates to a single tax year and exceeds $50,000, the simplified small tax case procedure is off the table — a petition proceeds under regular Tax Court rules, where representation usually pays for itself. If the same total had been spread across two audited years at roughly $41,550 each, you could elect S-case treatment for both.

Suppose you can reconstruct records proving $40,000 of the disallowed basis. Filing a timely petition preserves that argument: most docketed cases settle with Appeals, and every dollar of deficiency conceded also cuts the 20% penalty riding on it. Do nothing, and the full $83,100 is assessed — a balance that sits above the $66,000 passport-certification threshold, exposes a $2,400 monthly Social Security check to a continuous 15% levy ($360 every month), and grows daily. You can estimate how fast an assessed balance compounds with our IRS Penalty & Interest Calculator. This scenario is hypothetical, but the arithmetic is exactly how the IRS runs it — and it's why retired owe irs back taxes cases turn so heavily on acting inside the 90 days.

Situations that change your next move

Joint return. A deficiency on a jointly filed return makes both spouses fully liable, and a petition can be filed by either or both. If the adjustments trace to your spouse's income or deductions — a business you had no part in, income you never knew about — raise innocent spouse relief how to qualify early; it can be asserted in the Tax Court case itself.

Living abroad. If the letter was addressed to you outside the United States, your window is 150 days, not 90. The controlling date is still printed on the letter — trust that date, not your own count.

Multiple years on one letter. The $50,000 small-case ceiling applies per tax year, not to the letter's total. A $70,000 letter covering two years at $35,000 each can still be an S case; a $70,000 letter for one year cannot.

You partly agree. You don't have to fight everything. You can concede the adjustments that are right and petition only the ones that aren't — which shrinks both the dispute and the penalty attached to it.

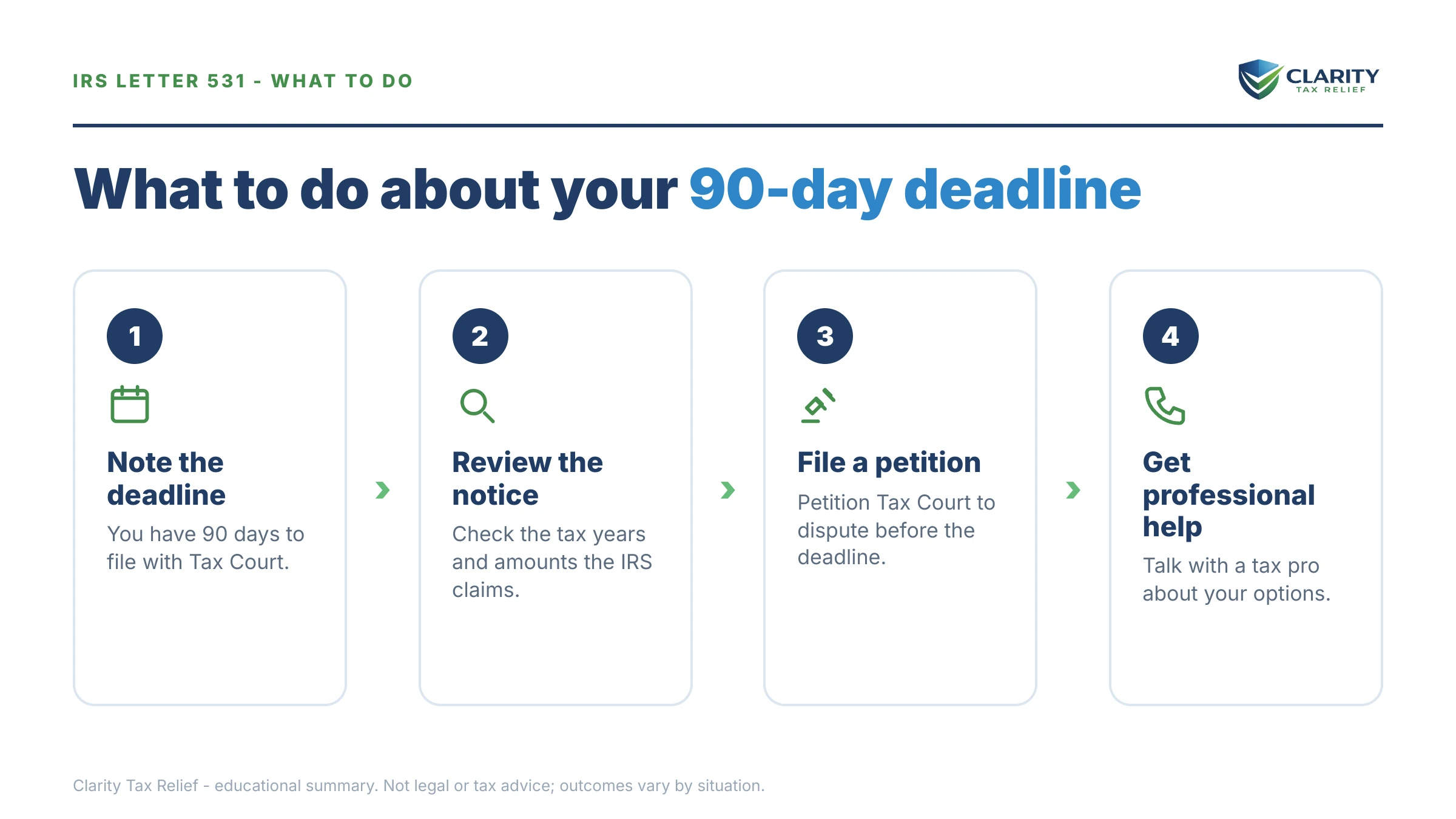

How to respond to Letter 531, step by step

- Find your petition deadline. Locate the last-day-to-file-a-petition date printed on page one of Letter 531 and put it on your calendar. Everything else works backward from that date.

- Compare the audit report to your records. Review Form 4549 line by line against your return and documents to decide whether you agree, partly agree, or dispute the adjustments.

- Sign Form 5564 only if you fully agree. Return the signed waiver and arrange payment or a payment plan. Signing ends your Tax Court rights for this deficiency, so verify the numbers first.

- File a Tax Court petition if you disagree. File before the deadline — the fee is $60, and you can elect the small tax case procedure if $50,000 or less per year is in dispute. Filing stops assessment and collection while the case is pending.

- Keep negotiating after you file. Most docketed cases settle with the IRS Independent Office of Appeals before trial, so continue providing documentation while your petition protects your rights.

When you can handle Letter 531 yourself

You genuinely don't need professional help when the adjustments are correct and manageable — say the examiner caught a 1099 you really did omit, the total is something you can pay or finance, and you simply sign Form 5564 and set up payment at IRS.gov/payments. The small tax case procedure was also built for self-represented taxpayers: if your dispute is under $50,000 per year and rests on clean documentation, plenty of people petition and settle on their own.

Experienced help changes outcomes in specific situations: a single-year deficiency over $50,000 (regular Tax Court rules and evidence standards apply), a deadline inside the next two or three weeks, multiple audited years, a joint return with an innocent-spouse angle, or a retiree budget that needs collection alternatives lined up in case any balance survives. If money is tight, the Taxpayer Advocate Service maintains a directory of free Low Income Taxpayer Clinics at taxpayeradvocate.irs.gov — a legitimate no-cost route for qualifying households.

Terms on your Letter 531, decoded

- Deficiency — the difference between the tax on your filed return and the tax the IRS says you actually owe; it is proposed, not yet owed.

- Statutory notice of deficiency — the legal name for Letter 531 (and its siblings); the only letter that opens the Tax Court's doors.

- Form 5564 — the waiver enclosed with the letter; signing it consents to immediate assessment and waives Tax Court review.

- Assessment — the moment a proposed tax is formally recorded as a debt the IRS can collect; nothing can be levied before it.

- Docketed case — your dispute once a petition is filed; most docketed cases settle with IRS Appeals before any trial date.

- Small tax case (S case) — a simplified, less formal Tax Court track for disputes of $50,000 or less per tax year; the trade-off is that the decision cannot be appealed.

Letter 531 questions, answered

Can the IRS extend the 90-day deadline on a Letter 531?

No — the 90-day window (150 days if the letter was addressed to you outside the United States) is fixed by statute, and neither the IRS nor the Tax Court can extend it. The last day to file is printed on the front of the letter. The clock runs from the mailing date, not the day you opened the envelope — and the notice is legally valid if it was mailed to your last known address, even if you never actually received it.

What is the difference between Letter 531 and CP3219A?

Both are statutory notices of deficiency carrying the same 90-day Tax Court deadline. Letter 531 comes out of an examination — a human auditor reviewed your return and you did not agree with or respond to the audit report. A CP3219A comes from the automated underreporter program after a CP2000 income mismatch. Your response options are identical, but a Letter 531 usually means a larger, more developed case file sits behind the numbers.

Do I have to pay the amount on Letter 531 before going to Tax Court?

No. The U.S. Tax Court is the only court where you can dispute the tax before paying it, and a timely petition blocks the IRS from assessing or collecting while your case is pending. If you miss the 90-day deadline, that changes: the IRS assesses the tax, and your remaining court option is generally to pay the balance in full first and then sue for a refund.

Should I sign Form 5564, the waiver that comes with Letter 531?

Only if you have verified the numbers are right and you do not intend to dispute them. Signing Form 5564 lets the IRS assess the tax immediately and permanently gives up your Tax Court rights for that deficiency. If any part of the adjustment looks wrong — a disallowed deduction you can document, income that is not yours — do not sign; petition instead. You can also agree to part of the deficiency and contest the rest.

What happens if I miss the 90-day deadline on Letter 531?

The IRS assesses the full deficiency, penalties, and interest, and the balance moves into collection — bills, then possible lien filing and levy notices. You lose prepayment Tax Court review, but you are not out of options: audit reconsideration can reopen the exam if you have documentation the examiner never saw, a doubt-as-to-liability Offer in Compromise disputes the amount itself, and payment plans or hardship status can manage what was assessed.

How much does it cost to file a Tax Court petition?

The filing fee is $60, and the court can waive it if you cannot afford it. If the disputed amount is $50,000 or less per tax year, you can elect the simplified small tax case procedure, which is designed for taxpayers representing themselves. Many petitioners never see a courtroom — most docketed cases settle with the IRS Independent Office of Appeals before trial.

Can the IRS take my Social Security over a Letter 531 balance?

Not while your 90-day window is open or a timely Tax Court case is pending — collection cannot start until the tax is assessed. After assessment and a final notice of intent to levy, though, the IRS can take up to 15% of your Social Security benefit through the Federal Payment Levy Program, continuously, until the debt is resolved. Retirees on fixed incomes often qualify for hardship protections that stop this — but only if they raise them.

Does sending more documents to the IRS stop the Letter 531 clock?

No. You can — and often should — keep working with the examiner or Appeals during the 90 days, because cases do get resolved that way. But nothing except a filed Tax Court petition preserves the deadline. The safe play when talks are still open near the deadline is to file the petition anyway; you can continue negotiating with Appeals afterward, and most docketed cases settle without ever going to trial.

Your next 24 hours

- Find the controlling date. On page one of your Letter 531, locate the last day to file a petition with the United States Tax Court. Write it down and count how many days you have left — that number decides everything else. The court's own filing information is at ustaxcourt.gov.

- Gather three documents. The Letter 531 itself (every page, including Form 5564), the audit report with Form 4549, and the tax return for the year in question, plus records for the adjusted items.

- Get the letter reviewed free — inside your window. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will tell you whether the numbers hold up, whether a petition makes sense, and what to do before your printed deadline arrives.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.