IRS Letters

Letter 525 IRS: What the 30-Day Audit Report Letter Means and How to Respond (2026)

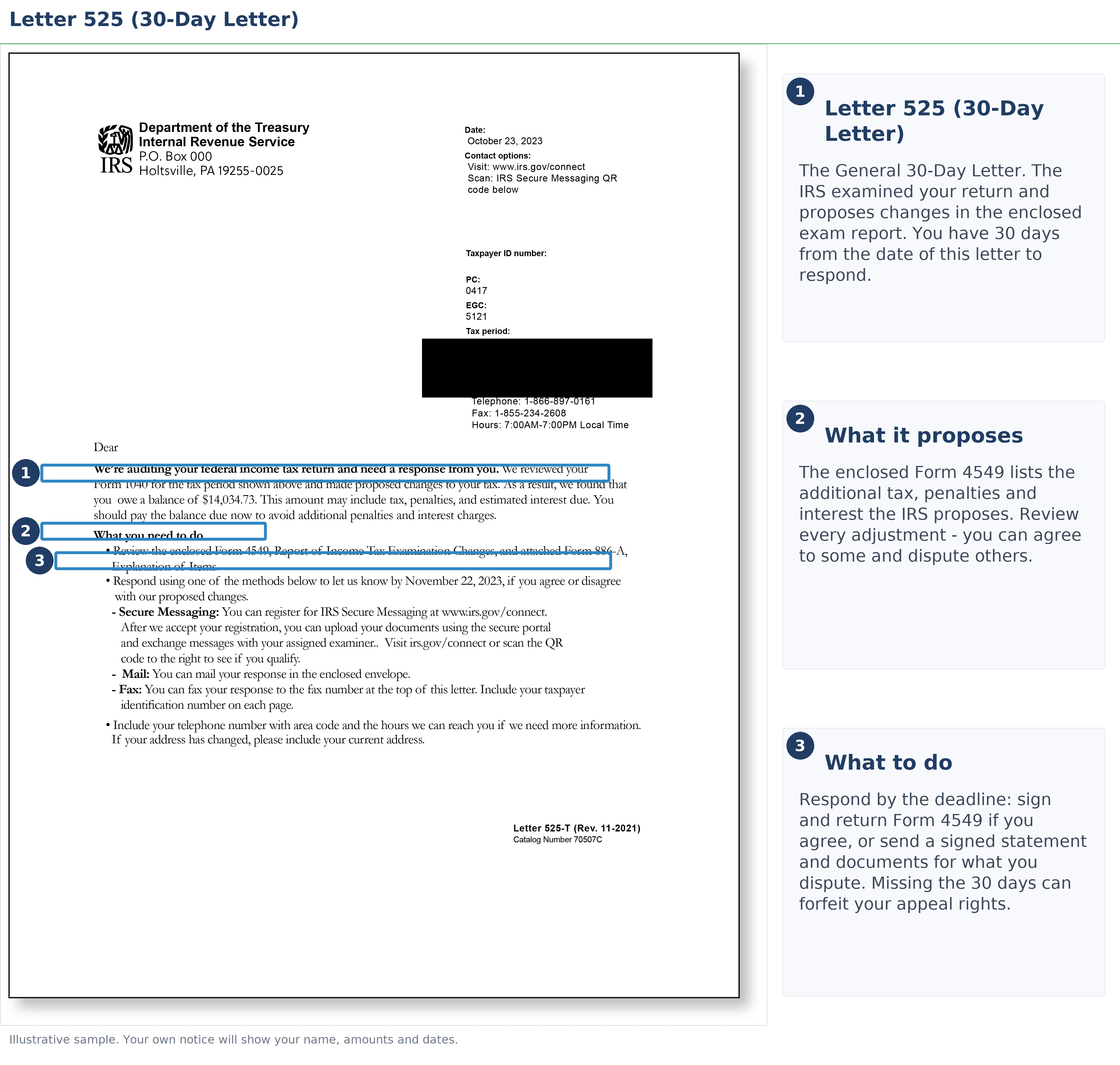

The short answer: Letter 525 is the IRS's "30-day letter" — the cover letter for your audit report (Form 4549) listing the changes an examiner wants to make to your return. Nothing is assessed yet. You typically have 30 days from the letter's date to agree, or to request an appeal before the changes become final.

The examination of your return is over, and Letter 525 IRS mail is the examiner's answer: a short cover letter with Form 4549 behind it, totaling a number you never budgeted for. If you're a business owner making payroll every two weeks, the real question isn't only whether the IRS is right — it's how to contest the parts that are wrong without starving the company of cash. This guide covers both.

Letter 525 packs three things into one envelope — the letter itself, the examination report, and an agreement form for your signature. The image below shows you exactly what each piece looks like and where to find the two numbers that control everything: your response date and the total proposed change.

⏱ Your deadline: the response date printed on your letter — typically 30 days from the date on Letter 525 — to agree with the audit report or request an appeal. Interest keeps accruing on the proposed balance while you decide, so the letter's clock and the interest clock run at the same time.

Why you got Letter 525 from the IRS

Letter 525 means an IRS examiner has finished reviewing your return and is proposing specific changes — listed on the enclosed Form 4549 — that increase what you owe. It's the standard closing move of an examination, whether your audit ran by mail, at an IRS office, or at your place of business, and whether it opened with a Letter 566 or a phone call from an examiner.

Form 4549 — officially "Income Tax Examination Changes," informally the Revenue Agent's Report or RAR — is the document that matters. It shows each adjustment, the additional tax it creates, any penalties, and interest computed to a stated date. Letter 525 is a proposal, not a bill — no balance exists on your account yet, and nothing can be collected at this stage.

For small-business owners, the most common adjustments are disallowed deductions the examiner decided weren't substantiated — vehicle expenses without a mileage log, contract labor without matching 1099s, meals and supplies paid in cash — plus unreported income found by comparing 1099-Ks and bank deposits against the return. If any adjustment reclassifies your contractors as employees, be alert: that opinion can spill into a separate payroll tax exposure covered in our guide to 941 back taxes.

If you're not sure this letter fits your situation at all — or you received several IRS letters at once — start with our overview of why did I get a letter from the IRS, then come back here for the 525-specific playbook.

What happens if you ignore IRS Letter 525

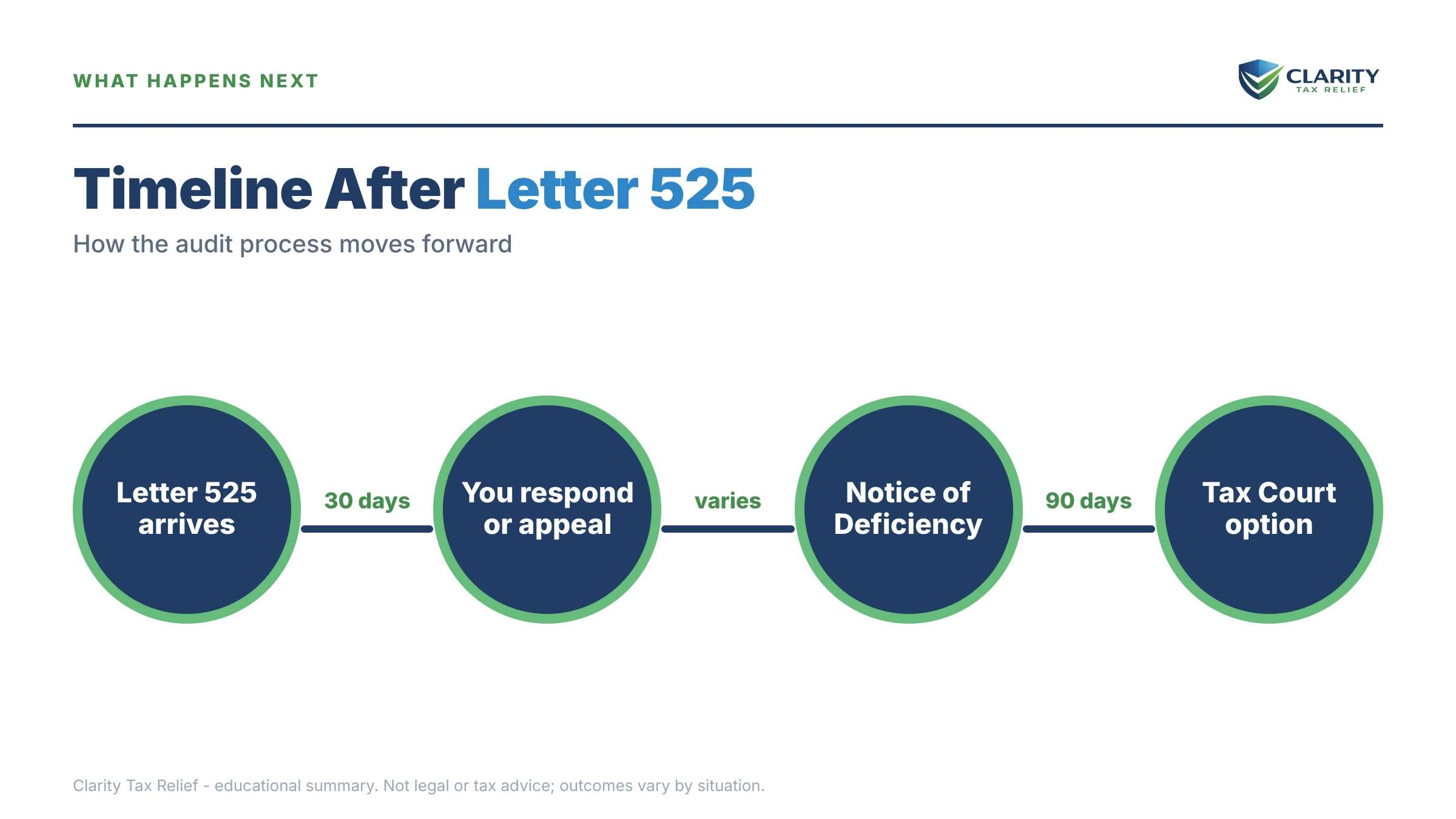

If you don't respond to Letter 525 within the response window, the IRS issues a Notice of Deficiency and starts a 90-day statutory clock toward final assessment. The sequence after that is automated and doesn't require a human to approve each step:

- Letter 525 + Form 4549 — you are here. The changes are proposed, your appeal rights are fully intact, and nothing is on your account yet.

- No response → Letter 531, the Notice of Deficiency (some cases receive a CP3219A instead). This is the IRS's formal legal determination. It starts the 90-day letter Tax Court petition window — your last chance to contest the amount before it's assessed.

- No petition → assessment. The proposed $27,500 (or whatever your report shows) becomes a legal debt. A CP14 bill follows, typically giving about 21 days to pay.

- Nonpayment → collection notices. Reminders escalate to a CP504, which lets the IRS take your state tax refund, and a federal tax lien becomes a live possibility.

- Final stage → Letter 1058 or LT11. This final notice of intent to levy starts a 30-day Collection Due Process window (Form 12153); after it closes, the IRS can levy bank accounts, wages, and business receivables.

For a business with employees, there's one more escalation path: audit-generated balances that go unaddressed are exactly the kind of case that gets assigned to a revenue officer, which usually announces itself with a Letter 725-B revenue officer visit. In 2026, IRS staffing is down sharply — but the notice stream, deficiency letters, and levies run on automated systems that never took a day off.

| Stage | What it is | Your window / what changes |

|---|---|---|

| Letter 525 + Form 4549 | Proposed audit changes — nothing assessed yet | Typically 30 days from the letter date to agree or appeal |

| Letter 531 / CP3219A | Notice of Deficiency — the IRS's formal determination | 90 days to petition the U.S. Tax Court |

| Assessment + CP14 | The proposed amount becomes a legal debt; first bill arrives | About 21 days to pay before reminders begin |

| CP501 → CP504 | Escalating collection notices; CP504 reaches your state refund | Automated; lien filing becomes a real risk |

| LT11 / Letter 1058 | Final notice of intent to levy wages, accounts, receivables | 30 days to request a CDP hearing via Form 12153 |

Holding a Letter 525 with numbers you don't agree with?

Send us a photo of the letter and the Form 4549 behind it. An experienced tax professional will tell you which adjustments are worth fighting and how to file before your 30-day response window closes — free, confidential, no pressure.

Your options on Letter 525

You have six realistic ways to respond to Letter 525, and only one of them — doing nothing — costs you leverage. Which one fits depends on whether you agree, how much is in dispute, and how strong your documentation is.

Agree completely. Sign the agreement portion of Form 4549 and return it. The IRS assesses the balance, interest stops growing the day you pay in full, and the case closes. Know what you're trading: signing waives your right to take those items to Tax Court later.

Agree partially. You don't have to accept or reject the whole report. Tell the examiner in writing which adjustments you accept and which you dispute — the disputed items can go to Appeals while the agreed ones close out.

Ask for more time. Examiners commonly grant an extension if you call before the deadline and explain you're gathering records. Confirm any extension in writing.

Appeal — small case. If the total you dispute is $25,000 or less per tax period, you can use the simple one-page Form 12203 appeal request to get an independent review by the IRS Independent Office of Appeals. No court, no filing fee.

Appeal — formal written protest. Above $25,000 per period, the same Appeals review requires a formal written protest: a letter stating each disputed adjustment, the facts, and the law or authority supporting your position, signed under penalties of perjury. It costs nothing to file, but it has to be built carefully — the protest frames your entire Appeals case. If the examiner sends additional findings after your first response, that follow-up often arrives as a Letter 692, which keeps the same appeal doors open.

Do nothing — deliberately. Some taxpayers skip Appeals and wait for the Notice of Deficiency so they can petition Tax Court (there's a modest filing fee, and most petitioned cases still settle with Appeals before trial). That's a legitimate strategy in some disputes, but it burns months of interest accrual and should be a choice, not a default. And if you miss every window, IRS audit reconsideration can sometimes reopen the exam after assessment — with new documentation and no guarantee.

| Option | Cost & timeline | What you keep or lose |

|---|---|---|

| Sign Form 4549 (full agreement) | Free; assessed within weeks; interest stops when paid | Fastest close; waives Tax Court rights on those items |

| Partial agreement | Free; disputed items move to Appeals | Closes what you accept; preserves appeal rights on the rest |

| Small case request (Form 12203) | Free to file; Appeals review often takes months | Only if the disputed total is $25,000 or less per tax period |

| Formal written protest | Free to file; longer Appeals timeline | Required above $25,000 per period; full appeal rights preserved |

| Wait for the Notice of Deficiency | $0 now; interest accrues throughout; modest Tax Court filing fee later | Keeps the court option; gives up the cheapest, fastest forum |

| Audit reconsideration (after assessment) | No fee; requires new documentation | Possible reopening, never guaranteed; collection may continue meanwhile |

A worked example: $27,500 in proposed changes

Say you run a six-employee landscaping company and the IRS examined your 2023 return. The Form 4549 behind your Letter 525 proposes $27,500 in total, built like this:

- $21,600 in additional tax — the examiner disallowed your vehicle deductions (no mileage log) and part of your contract-labor expense (no matching 1099s);

- $4,320 in accuracy-related penalty — 20% of the $21,600 in extra tax;

- roughly $1,580 in interest computed to the report date, accruing from the return's original due date and growing daily.

First strategic fact: because you dispute more than $25,000 for one tax period, the simple Form 12203 route is off the table — you need a formal written protest to reach Appeals. Second: the penalty is a multiplier on the outcome. If Appeals accepts a reconstructed mileage log and vendor payment records and allows, say, $6,700 of tax back, the 20% penalty recomputes on the lower tax and interest recalculates too — one successful appeal can swing the total by $8,000 or more. You can estimate how penalties and interest compound on your own numbers with our penalty & interest calculator.

Third: if you agree and can't pay, the math still works. A $27,500 assessed balance divided over a 72-month installment agreement is roughly $382 a month before accruing interest and the 0.5%-per-month late-payment penalty, so your actual payment would be set somewhat higher — manageable next to a payroll run, and it stops every enforcement step in the table above.

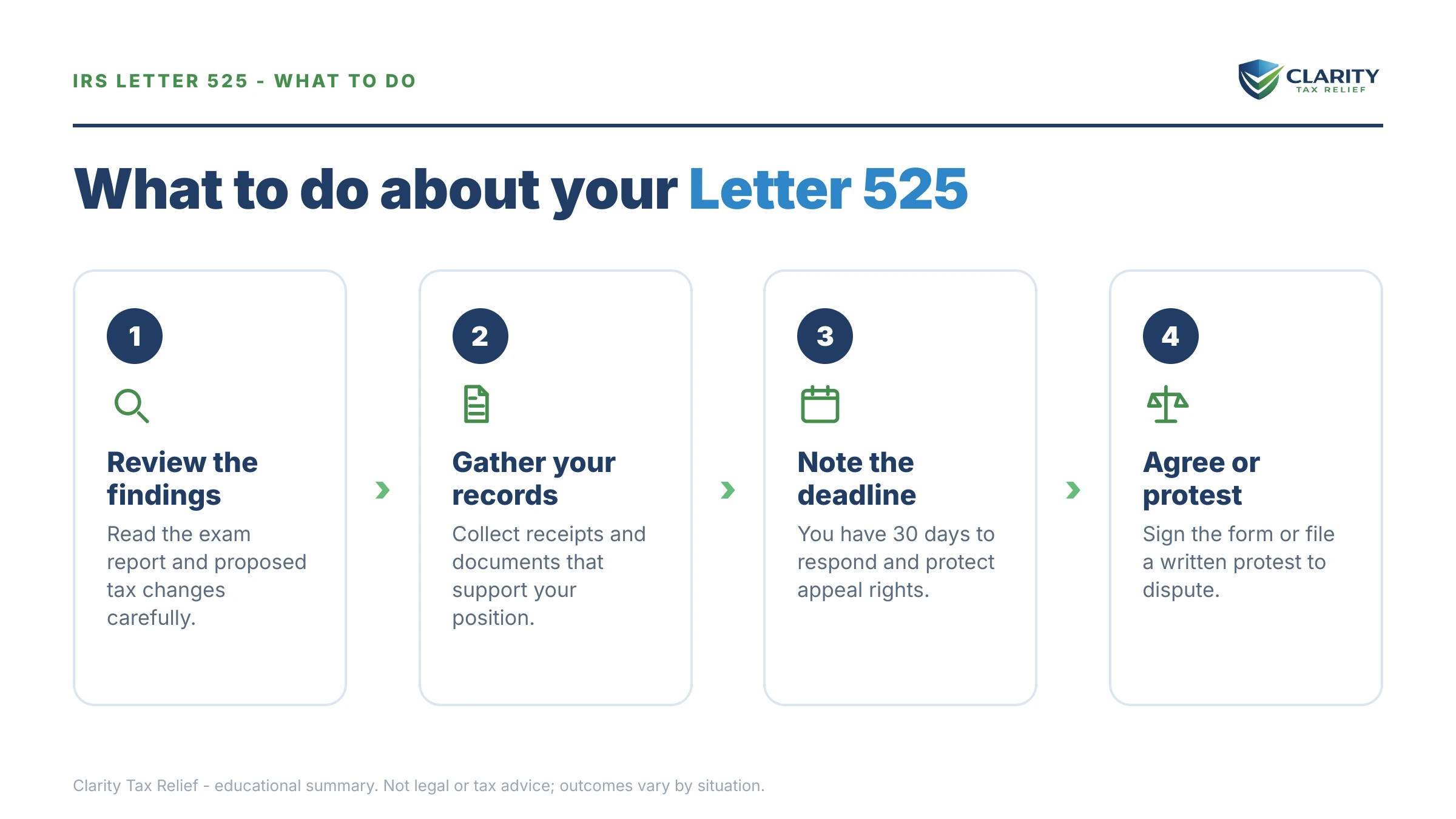

How to respond to Letter 525, step by step

- Read Form 4549 line by line. Match each adjustment on the exam report to the line of your return it changes, and note the separate tax, penalty, and interest amounts attached to each one.

- Confirm your deadline. Find the response date printed on Letter 525 and put it on your calendar. Extensions must be requested from the examiner before that date, not after.

- Sort the adjustments into agree and dispute. Decide item by item. You can accept some changes and contest others — partial agreement is normal and often the smartest move.

- Gather proof for every disputed item. Pull receipts, bank statements, mileage logs, invoices, and contracts that support the deductions or income figures the examiner changed.

- Send your response before the deadline. Sign Form 4549 for what you accept. For what you dispute, file Form 12203 if the disputed total is $25,000 or less per tax period, or a formal written protest if it's more.

- Arrange payment for anything you agreed to. Pay online or set up a payment plan so the agreed amounts don't ride into the collection notice stream and grow with penalties.

If you agree with the report and just need time to pay, our walkthrough on how to set up an IRS payment plan online covers the process once the balance posts to your account. Payments themselves go through IRS.gov/payments — never to anyone who calls asking for gift cards or wire transfers.

When you can handle Letter 525 yourself

You can handle Letter 525 without professional help when you agree with the changes and the balance is one you can pay or finance. Signing Form 4549, paying online, or setting up a streamlined installment agreement is genuinely a do-it-yourself task. The same is true if the disputed amount is small, your records are clean, and a one-page Form 12203 tells the whole story.

Experienced help changes outcomes in specific situations: the disputed total is over $25,000 per period and a formal protest has to be drafted under penalties of perjury; the exam disallowed deductions you can only prove by reconstruction (missing logs, cash payments, lost receipts); the report covers multiple years; or an adjustment hints at worker reclassification that could open a payroll tax front. Appeals officers weigh the "hazards of litigation" — how the case would look in court — and a protest written to that standard is a different document than a letter saying you disagree. The IRS explains the appeals process itself at IRS.gov/appeals.

One honest note: a professional can't manufacture documentation that doesn't exist. What they can do is know which reconstruction methods examiners and Appeals actually accept, and which adjustments are worth conceding to strengthen the rest. If your core problem is missing records, start with our guide to surviving an IRS audit with no receipts.

Terms on your Letter 525, decoded

- Form 4549 — the examination report ("Income Tax Examination Changes") listing every proposed adjustment, penalty, and interest figure; also called the Revenue Agent's Report or RAR.

- 30-day letter — the informal name for Letter 525, because it typically gives 30 days to agree or request an Appeals review.

- Notice of Deficiency — the formal legal determination (Letter 531 or CP3219A) that follows if you don't respond; it opens a 90-day window to petition the U.S. Tax Court.

- Formal written protest — the signed statement of facts and law required to reach Appeals when you dispute more than $25,000 per tax period.

- Accuracy-related penalty — a 20% penalty on the portion of underpaid tax attributed to negligence or a substantial understatement; it appears on most exam reports and recalculates if the tax changes.

- Independent Office of Appeals — the IRS division, separate from the examiner, that reviews disputed audit findings and can settle based on how the case would fare in court.

The IRS's own summary of this letter is at Understanding your Letter 525. If you feel the process itself has gone off the rails — deadlines the IRS missed, responses ignored — the Taxpayer Advocate Service is an independent avenue.

Letter 525 questions, answered

What is IRS Letter 525?

Letter 525 is the IRS's "30-day letter" — the cover letter for your audit report (Form 4549) showing the changes an examiner wants to make to your return. It is a proposal, not a bill: nothing has been assessed yet. You typically have 30 days from the letter date to agree, or to request a review by the IRS Independent Office of Appeals.

Is Letter 525 the end of my audit?

It's the end of the examination phase, but not the end of your case. The examiner has finished and put the proposed changes in Form 4549; the letter opens your appeal window. If you respond within the deadline, the case can move to Appeals; if you don't, the IRS moves toward a Notice of Deficiency and formal assessment.

What happens if I ignore Letter 525?

The IRS issues a Notice of Deficiency (Letter 531 or CP3219A), which gives you 90 days to petition the U.S. Tax Court. If you don't petition, the tax is assessed and collection begins with a CP14 bill, escalating toward liens and levies. Ignoring the letter doesn't pause interest — it accrues on the proposed balance the whole time.

Should I sign Form 4549 if I agree?

Sign it only if you agree with every adjustment and every penalty on the report. Signing waives your right to take those items to Tax Court and lets the IRS assess the balance immediately. If you agree with some changes but not others, say so in writing — partial agreement is common, and you can appeal just the disputed items.

Can I get more time to respond to Letter 525?

Often, yes. Call the examiner listed on the letter before the deadline and ask for an extension; examiners commonly grant additional time while you gather records. Get the agreement in writing, or note the name of the person who approved it and the date. Never assume an extension — silence past the deadline moves your case forward automatically.

What's the difference between Letter 525 and Letter 531?

Letter 525 is the 30-day letter: a proposal you can still contest inside the IRS through Appeals, with no court involved. Letter 531 is the Notice of Deficiency — the 90-day letter — the IRS's formal legal determination; after it, your main remedy is a U.S. Tax Court petition. Appeals is usually cheaper and faster than court, which is why the 525 window matters.

What if I miss the 30-day deadline on Letter 525?

You lose the easy path to Appeals, but not everything. The Notice of Deficiency that follows gives you 90 days to petition Tax Court, and most petitioned cases still settle with Appeals before trial. After assessment, audit reconsideration can reopen the exam if you have new documentation. Each later stage costs more time and leverage than responding to the 525 would have.

I agree with Letter 525 but can't pay — what should I do?

Sign the report to stop the case from escalating, then set up a payment arrangement once the balance is assessed. Short-term plans give you up to 180 days with no setup fee; balances up to $50,000 can generally go on a monthly installment agreement of up to 72 months online. Interest and the late-payment penalty continue until the balance is paid.

Your next 24 hours

- Find your response date. It's printed on the first page of Letter 525 — write it down, then flip to Form 4549 and circle the total proposed change and each individual adjustment.

- Gather your proof. Pull the tax return that was examined, the full Letter 525 packet, and every record that supports the disputed items — bank statements, invoices, mileage data, contractor payments.

- Get the report reviewed free. Before your response window closes, have an experienced tax professional tell you which adjustments are worth fighting and which route — agreement, Form 12203, or formal protest — fits your numbers. Use the 2-minute form or call (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.