IRS Audits

IRS Audit, No Receipts: What Happens and How to Respond (2026)

The short answer: facing an IRS audit with no receipts doesn't mean you automatically lose every deduction. Under the Cohan rule, the IRS must allow reasonable estimates for many business expenses — but vehicle, travel, and meal deductions require strict records. Your first move: reconstruct documentation from bank statements, card records, and third parties before your response deadline.

You searched "IRS audit no receipts" because the letter asks for documentation you don't have — the receipts went out with a move, died with an old phone, or were never saved in the first place. That gap feels like a verdict, but it isn't one. Auditors close cases on reconstructed records every week, and the law itself gives you room to estimate certain expenses. What decides your outcome is what you rebuild in the next few weeks, not what you lost.

Your audit letter — usually a Letter 566 for a mail exam, or a CP75 if the IRS is questioning credits — lists exactly which items are under review. The image below shows what this kind of audit letter looks like and where to find the items being questioned and the date that controls your response.

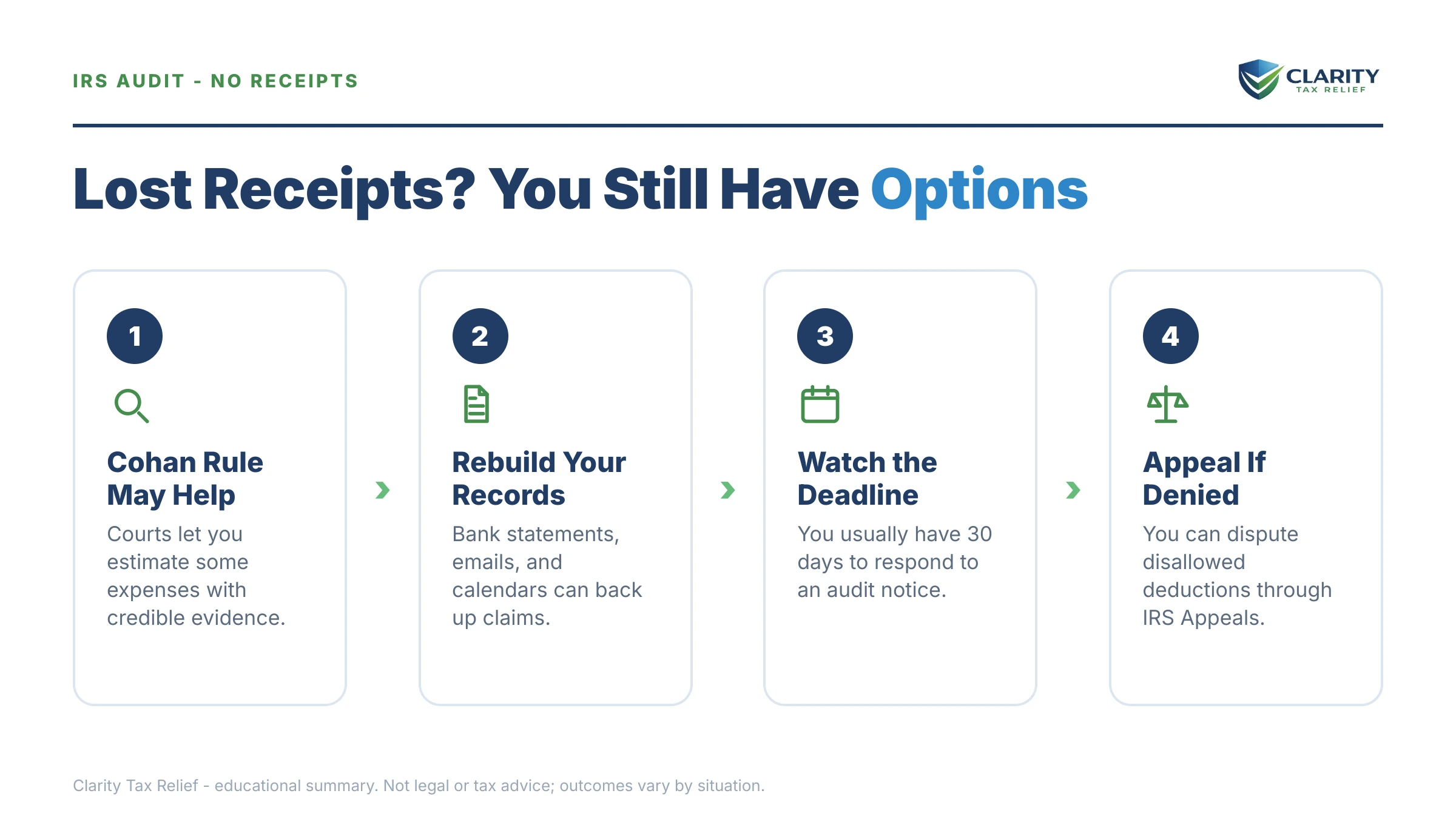

⏱ Your deadline: the response date printed on your audit letter — typically 30 days from the letter date — controls everything. Miss it and the auditor can disallow every unproven item by default. Two more clocks follow: 30 days to appeal the examination report, then 90 days to petition Tax Court once a Notice of Deficiency is issued.

Why the IRS is asking for receipts you don't have

In an audit, the burden of proving your deductions is on you, not the IRS. Income is presumed correct because employers, banks, and payment processors report it directly; deductions are the opposite — the law treats them as something you must substantiate, and an unproven deduction is treated the same as a false one: disallowed.

That's why the auditor's Information Document Request reads like it assumes you kept a filing cabinet. The system is built around documentation, and in 2026 the returns pulled for exam are increasingly selected by algorithm — deduction patterns that sit outside the statistical norm for your income and profession get flagged automatically. Our guide to IRS AI audits covers how that selection works.

Certain returns face this problem hardest: Schedule C filers with round-number expenses, and cash-heavy operations where the IRS may go further and reconstruct your income too. If that's you, see cash business audit defense and how a bank deposit method audit works — because in those exams, missing records cut in both directions.

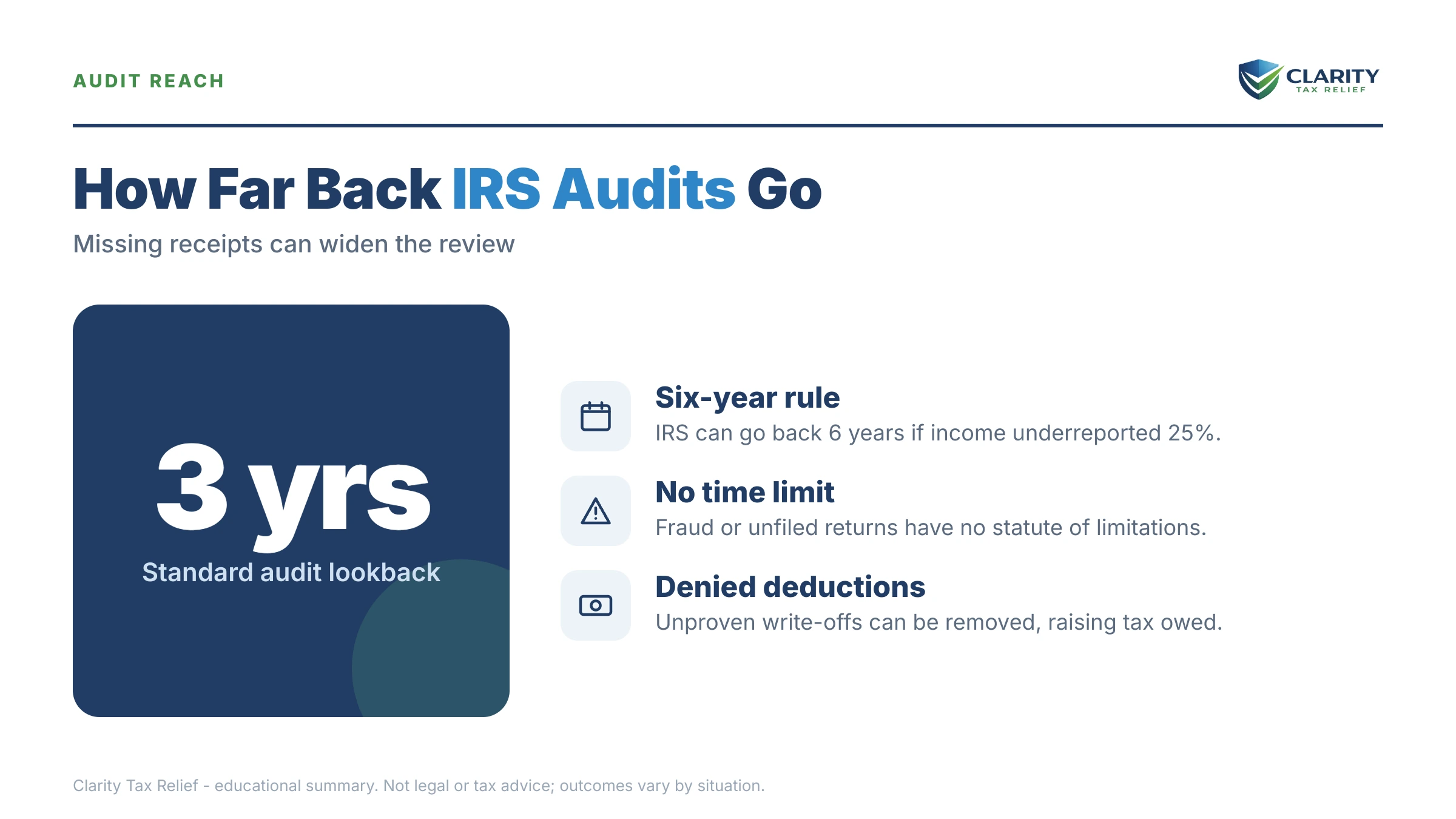

How many years are exposed matters too. The IRS generally has three years to audit a return, stretching to six in some cases — the full rules are in our guide to how far back the IRS can audit. If your records problem spans several years, assume the auditor can expand the exam to any open year.

The Cohan rule: what you can estimate without receipts

The Cohan rule requires the IRS to allow a reasonable estimate of deductible expenses when the evidence shows you clearly incurred them, even without receipts. It comes from a 1930 appeals-court case involving Broadway producer George M. Cohan, whose travel and entertainment records were nonexistent — the court held that some allowance had to be made because the spending obviously happened.

Two catches. First, the estimate is resolved against you — courts "bear heavily" on the taxpayer whose sloppiness created the problem, so you get the low end of any plausible range, not the number on your return. Second, Congress later carved out entire categories where no estimate is allowed at all, under the strict-substantiation rules of IRC §274(d).

| Expense type | Estimate allowed (Cohan)? | What the IRS wants to see |

|---|---|---|

| Supplies, materials, cost of goods | Yes, with a credible basis | Bank/card statements, vendor records, industry-typical ratios |

| Rent, utilities, insurance, phone | Yes — often fully reconstructable | Statements from the landlord, utility, insurer, or carrier |

| Contract labor, professional fees | Yes, if payments are traceable | 1099s issued, canceled checks, invoices, payment-app history |

| Vehicle & mileage | No — §274(d) | Log showing date, miles, destination, business purpose |

| Travel & lodging | No — §274(d) | Amount, dates, place, and business purpose for each trip |

| Meals & business gifts | No — §274(d) | Amount, date, place, business purpose, who attended |

| Charitable gifts of $250+ | No | Contemporaneous written acknowledgment from the charity |

| Cash charitable gifts under $250 | No | Bank record or receipt — a memory isn't enough |

Read that table strategically. If the audit questions supplies and rent, your position is strong: reconstruct and estimate. If it questions mileage and meals, estimation is off the table — but reconstruction of specific records is still allowed, and courts have accepted rebuilt mileage logs created from calendars and job records. Our guide to what to do when the IRS wants a mileage log walks through that rebuild in detail.

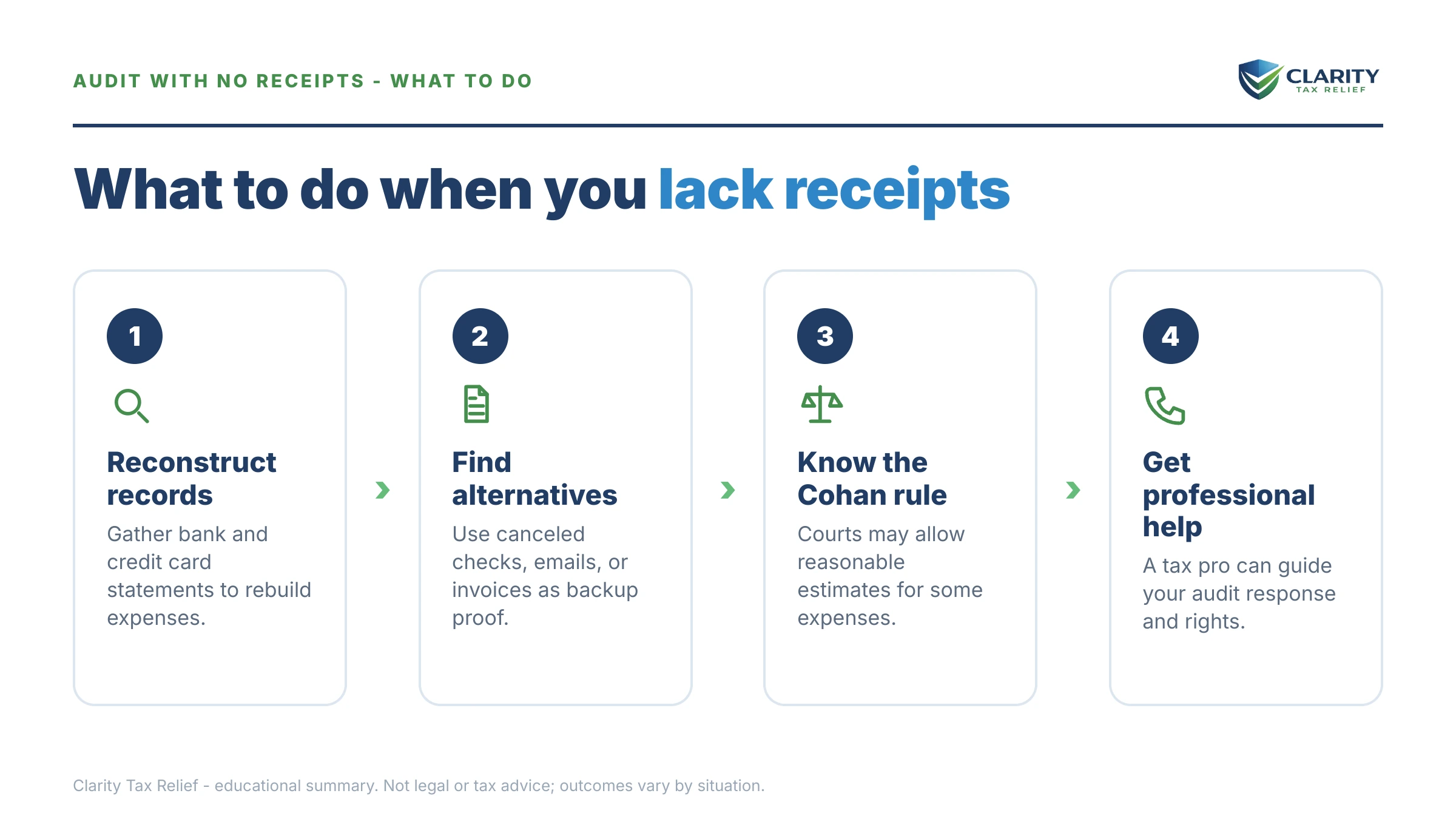

How to reconstruct records the IRS will actually accept

Auditors accept reconstructed records when they're honest, organized, and anchored to third-party data. You're not trying to fake receipts — you're building a paper trail from sources that still exist. Work through these in order:

- Bank and credit card statements. Request the full audit year from every account — most banks provide up to seven years online or on request. Annotate each business charge with what it was for. Statements prove payment; your annotations supply business purpose.

- Payment apps and online order histories. PayPal, Venmo business, Square, Amazon, and supplier portals keep transaction-level detail with item descriptions — often better than a paper receipt.

- Third-party duplicates. Vendors, landlords, insurers, and contractors can reissue invoices and payment histories. A charity can reprint an acknowledgment letter — though for gifts of $250+, note that the law requires the acknowledgment to have been obtained by the time you filed, so a fresh letter may not cure a missing one.

- Your own IRS file. A wage and income transcript shows every W-2, 1099, and 1098 filed under your Social Security numbers — useful for pinning down income-side documents and mortgage interest without hunting paper.

- Calendars, emails, texts, and photos. Appointment calendars establish business travel dates. Emails confirm jobs, deliveries, and purchases. Phone photo metadata can place you at a job site. These are the raw material for rebuilding §274(d) logs.

- Written statements. A short signed statement from a client, supplier, or worker confirming a business relationship or recurring payment carries real weight when it corroborates the numbers.

Never fabricate a receipt or backdate a document. A missing record costs you a deduction; a fake one converts a civil exam into potential fraud territory. Label every rebuilt log or schedule as a reconstruction — auditors respect the honesty, and it protects you.

What no receipts actually costs: a worked example

Disallowed deductions cost more than the tax on them — penalties and interest stack on top. Say you're a married couple filing jointly: one W-2 salary, plus a side photography business on Schedule C, and the auditor questions $6,200 of business expenses you can't find receipts for. This is a hypothetical, but the math is how it really works:

- If all $6,200 is disallowed: at a 22% bracket, income tax rises about $1,364. Because it's Schedule C income, self-employment tax adds roughly 14.1% more — about $875. That's ≈ $2,240 in extra tax.

- Then the penalty: the 20% accuracy-related penalty on $2,240 adds about $448, and interest runs from the return's original due date — call it $2,900+ all-in by the time the bill arrives.

- If you reconstruct instead: suppose bank and card statements substantiate $4,700 of the spending, and the auditor allows nothing for the rest. Disallowance drops to $1,500 — extra tax of roughly $542 ($1,500 × ~36%), and with a documented good-faith effort, the negligence penalty becomes much harder for the IRS to sustain.

Same audit, same lost shoebox — a difference of well over $2,000, decided entirely by the response packet. You can estimate how penalties and interest compound on your own numbers with our Penalty & Interest Calculator, and the penalty itself is covered in our guide to the accuracy related penalty.

What happens if you ignore the audit

An ignored audit doesn't stall — it concludes without you, with every questioned deduction disallowed. The sequence is procedural and runs on its own:

- Audit letter and document request — Letter 566, CP75, or an appointment letter, with a printed response date (typically 30 days). No response is treated as no proof.

- Examination report — Letter 525 arrives with the proposed changes: disallowed deductions, added tax, and usually the 20% penalty. You get 30 days to agree or appeal.

- Statutory Notice of Deficiency — the CP3219A notice of deficiency starts a hard 90-day clock to petition Tax Court. This is your last chance to dispute the numbers before paying.

- Assessment and collection — the balance posts to your account and the collection notice stream begins with a bill, escalating over months toward liens and levies if unpaid.

The 2026 wrinkle: with the IRS workforce down roughly 27% since 2025, reaching a human to reopen a defaulted exam is genuinely harder — but the letters, assessments, and eventual levies are automated and never paused. The cheapest point to fix a no-receipts audit is before the examination report is final.

| Notice | Response window | What you lose if it passes |

|---|---|---|

| Letter 566 / CP75 + document request | Date printed on the letter (typically 30 days) | The chance to substantiate before deductions are disallowed by default |

| Letter 525 (examination report) | 30 days | Your appeal to the IRS Independent Office of Appeals |

| CP3219A (Notice of Deficiency) | 90 days | Your right to Tax Court review before paying the tax |

| Assessment → collection notices | First bill typically gives ~21 days | Each ignored notice moves you closer to lien and levy action |

Audit letter in hand and no receipts to send?

Get your audit letter reviewed free before the response date printed on it passes. An experienced tax professional will tell you which expenses can be estimated, which must be reconstructed, and what your packet should look like — no pressure, no obligation.

Your options at every stage of a no-receipts audit

You have a distinct set of options at each stage — before the report, after the report, and even after the audit closes. Choosing the right lane matters more than arguing harder in the wrong one:

| Option | When it fits | Deadline / cost |

|---|---|---|

| Reconstruct and respond | Exam still open; records can be rebuilt from banks and third parties | Response date on your letter; costs only time (or professional fees) |

| Agree and pay | The disallowance is correct and you can pay in full | Sign the report; interest stops accruing once paid |

| Agree, then payment plan | Balance is right but unpayable at once — under $50,000 qualifies online for up to 72 months | Set up before collection notices escalate; interest continues |

| Appeal the report | You have reconstructions or estimates the auditor undervalued | 30 days from Letter 525; Form 12203 if ≤ $25,000 per period; free to file |

| Tax Court petition | Appeal window missed or Appeals failed; you want review before paying | 90 days from CP3219A — hard deadline; modest filing fee |

| Audit reconsideration | Audit already closed; you've since found or rebuilt documentation | No fee, no fixed deadline — but interest and collection continue meanwhile |

Appeals deserves special mention for no-receipts cases. Appeals officers settle based on the hazards of litigation, and they know courts apply the Cohan rule — so a reconstruction the original auditor rejected outright often gets partial credit at Appeals. Your full toolkit there is covered in IRS audit appeal rights, and if the case is already closed, audit reconsideration is the reopening path.

How to respond to an IRS audit with no receipts, step by step

- Read your audit letter and calendar the response date — the deadline printed on your letter controls everything else you do.

- Pull your bank, credit card, and payment-app records for every questioned expense category, going back through the full audit year.

- Request duplicates from third parties — vendors, landlords, insurers, charities — and pull your IRS wage and income transcript for income-side documents.

- Rebuild what can't be replaced using calendars, emails, photos, and written statements, clearly labeled as reconstructions — never fabricated receipts.

- Respond in writing by the deadline with an organized packet that matches each questioned expense to its supporting document or estimate.

- Appeal within 30 days if the examination report disallows expenses you can reasonably support — Appeals can apply the Cohan rule more generously than the auditor.

Organization is half the battle. Auditors work stacks of cases; a packet with a cover sheet listing each questioned item, the amount claimed, and the exhibit supporting it gets a materially better read than a loose pile of statements.

When you can handle this yourself — and when help changes the outcome

Plenty of no-receipts audits are safely handled without professional help. If the audit questions one or two ordinary categories, the dollars at stake are modest, and your bank statements cover most of the spending, a careful reconstruction packet mailed by the deadline will usually resolve it. Same if you review the numbers, agree the deduction wasn't supportable, and simply sign and pay — or set up a payment plan.

Experienced help changes outcomes in specific situations: the exam involves §274(d) categories like mileage or travel, where the rebuild has to satisfy exacting elements; it's a Schedule C audit touching most of the return; the auditor is reconstructing your income through bank deposits; multiple years are open; or you've already missed the report deadline and the case is heading to a Notice of Deficiency. In eggshell situations — where the records problem hides income that was never reported — get representation before you say anything to the auditor.

The honest test: if your worst case is losing a deduction you probably couldn't support anyway, handle it yourself. If your worst case is a multi-year assessment with penalties, the review is worth it before you respond, not after.

Terms on your audit paperwork, decoded

- Cohan rule — the court doctrine requiring the IRS to allow reasonable estimates of expenses that were clearly incurred, resolved against the taxpayer.

- Strict substantiation (§274(d)) — the statute barring any estimate for vehicle, travel, meal, gift, and listed-property deductions; specific records are mandatory.

- IDR (Form 4564) — the Information Document Request listing exactly which documents the auditor wants and by when.

- Examination report (RAR) — the auditor's written proposed changes, sent with Letter 525; signing it agrees to the assessment.

- Statutory Notice of Deficiency — the "90-day letter" (CP3219A) that is your final ticket to Tax Court before the tax is assessed.

- Burden of proof — in exams, the taxpayer's obligation to substantiate deductions; the IRS doesn't have to prove your expenses were fake, you have to prove they were real.

If your reconstruction is genuinely there but the auditor won't credit it, don't argue in circles — have your exam file reviewed free before the report becomes final; the Appeals posture is usually stronger with the packet built right the first time.

IRS audit with no receipts: your questions, answered

What happens if you get audited by the IRS and have no receipts?

The auditor can disallow any deduction you can't support, which raises your tax and usually adds a 20% accuracy-related penalty plus interest. But disallowance isn't automatic: under the Cohan rule, reasonable estimates are allowed for many business expenses, and bank statements, card records, and third-party documents can replace lost receipts. The outcome depends almost entirely on how well you reconstruct proof before your response deadline.

Can I use bank and credit card statements instead of receipts in an IRS audit?

Yes — for most ordinary business expenses, auditors routinely accept bank and credit card statements as proof of payment. The gap they leave is business purpose: a statement shows you paid a vendor $214, not why. Annotate each charge with what it was for, and pair statements with invoices, emails, or order histories where you can. For vehicle, travel, and meal expenses, statements alone are not enough because those categories require stricter records.

What is the Cohan rule and does it still apply in 2026?

The Cohan rule comes from a 1930 court case allowing taxpayers to deduct a reasonable estimate of expenses when records are missing but the expenses were clearly incurred. It still applies in 2026, and auditors and Appeals officers use it — but the estimate is resolved against you, meaning you get the low end of any range. It never applies to vehicle, travel, meal, gift, or listed-property deductions, which Congress carved out for strict substantiation.

Which deductions can never be estimated without records?

Vehicle and mileage, travel, meals, business gifts, and listed property fall under IRC Section 274(d), which requires records showing the amount, time, place, and business purpose — no estimates allowed. Charitable gifts of $250 or more also require a contemporaneous written acknowledgment from the charity, and even smaller cash gifts need a bank record or receipt. If your audit questions these categories, reconstruction of specific records — not estimation — is your only path.

Can you go to jail for not having receipts in an IRS audit?

No — losing your receipts is a civil matter, not a crime. The worst-case outcome of missing records is disallowed deductions, additional tax, penalties, and interest. Criminal exposure requires willful conduct like fabricating documents, hiding income, or lying to the auditor, which is why you should never invent receipts or backdate records to fill a gap. An honest reconstruction, clearly labeled as such, is both legal and effective.

How much is the penalty if the IRS disallows my deductions?

The accuracy-related penalty is 20% of the additional tax caused by the disallowance, and having no records at all is one of the ways auditors justify it under the negligence prong. On a $2,240 tax increase, that's roughly $448 on top, plus interest running from the return's original due date. A genuine, documented reconstruction effort is also your best defense against the penalty itself, since it undercuts the negligence argument.

Can I appeal if the auditor disallows everything?

Yes. The examination report typically gives you 30 days to request a conference with the IRS Independent Office of Appeals, which settles cases based on hazards of litigation and often applies the Cohan rule more generously than the original auditor. If the proposed change is $25,000 or less per tax period, the short Form 12203 works. Miss the 30-day window and you still get 90 days from the statutory notice of deficiency to petition Tax Court before paying.

What if my audit already closed and I found my records later?

You can request audit reconsideration — asking the IRS to reopen the exam because you have new documentation it never evaluated. There's no fee and no fixed deadline, though the balance keeps accruing interest and collection notices keep coming while you wait. Reconsideration works best when your packet contains genuinely new evidence, like recovered bank records or vendor duplicates, rather than a repeat of arguments the auditor already rejected.

How long should I keep receipts in case of an IRS audit?

Keep records at least three years from the date you filed, because that's the standard audit window. Hold them six years if your return involves substantial self-employment or investment income, since the window doubles when income is understated by more than 25%, and keep property and asset records for as long as you own the asset plus three years. Digital copies count — photograph receipts as you get them and the shoebox problem disappears.

For the IRS's own description of the exam process and your rights during it, see the IRS overview of IRS audits. If the process itself breaks down — a defaulted exam you responded to on time, or hardship the auditor won't acknowledge — the Taxpayer Advocate Service is an independent avenue inside the IRS. And if you end up owing, payment options live at IRS.gov/payments.

Your next 24 hours

- Find the response date on your audit letter — it's printed near the top of the Letter 566 or CP75 — and the list of questioned items. Those two things define your entire job.

- Start the paper pull tonight: download the audit year's bank and credit card statements, export payment-app and order histories, and email vendors for duplicate invoices — third-party requests take the longest, so send them first.

- Get a free case review before you respond. Use the 2-minute form or call (888) 825-7779 — an experienced tax professional will map which items to estimate, which to reconstruct, and how to present the packet before your letter's deadline arrives.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.