IRS Forms

Form 12203 Appeal Request: How to Appeal Your IRS Audit Results (2026)

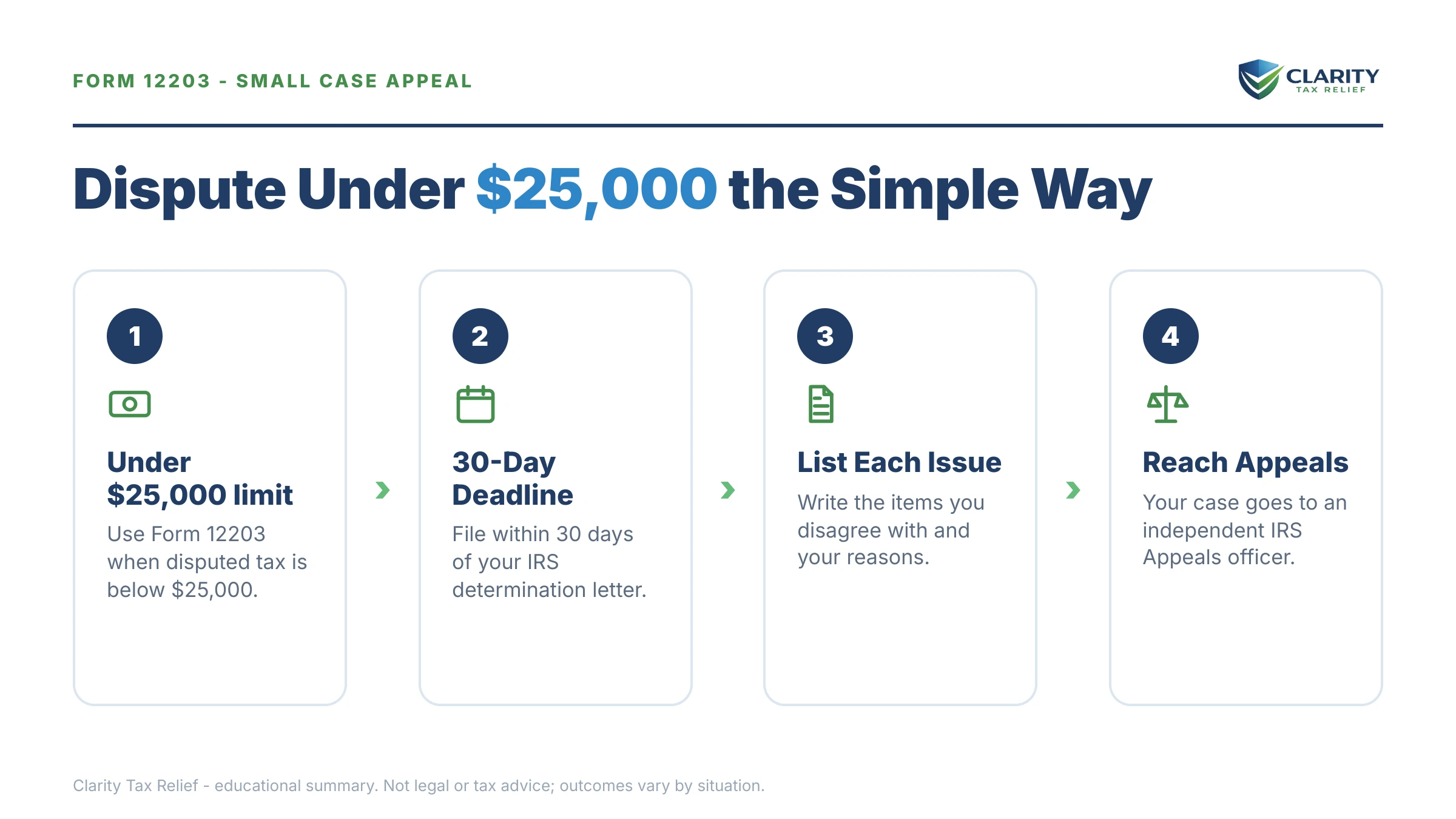

The short answer: Form 12203, Request for Appeals Review, lets you appeal IRS audit findings of $25,000 or less per tax period without writing a formal protest. File it by the response date on your 30-day letter — typically 30 days — and your case goes to the IRS Independent Office of Appeals before assessment.

You survived the exam itself — and then the follow-up letter arrived proposing changes you know are wrong, with a report attached and a choice: sign and agree, or fight. A Form 12203 appeal request is how you fight without hiring a lawyer or going to court, and the window to file it is already open. This page shows you exactly how it works.

Two numbers control everything here: the $25,000-per-period ceiling that decides whether you can use this one-page form at all, and the response date printed on your letter. The image below shows exactly what Form 12203 looks like and where each entry goes, so you can match it against the letter in your hand.

⏱ Your deadline: the response date printed on your 30-day letter — typically 30 days from the letter's date. File Form 12203 by that date or the IRS closes the exam unagreed, issues a Notice of Deficiency, and your chance at a pre-assessment appeal is gone.

Why you're holding a 30-day letter — and where Form 12203 fits

Form 12203 exists for one moment: the IRS examined your return, proposed changes, and gave you roughly 30 days to disagree before the changes become a bill. The letter that opens that window is called a 30-day letter — commonly Letter 525 or Letter 950 — and it arrives with Form 4549, the examination report that itemizes every adjustment, penalty, and interest figure the examiner wants to add.

The letter offers three paths: sign the report and agree, do nothing, or appeal. Appealing sends your file to the IRS Independent Office of Appeals — a separate function whose job is to settle disputes without litigation. Appeals officers can do something the examiner cannot: weigh the "hazards of litigation" and concede issues, in whole or in part, based on how the case would likely fare in court.

If you're not sure your letter is actually a 30-day letter — the IRS sends dozens of look-alikes — start with our guide to why you got a letter from the IRS, then come back. Form 12203 only works in this specific window, for this specific kind of dispute.

The $25,000 rule: who qualifies for a Form 12203 appeal request

Form 12203 is limited to disputes of $25,000 or less per tax period — and "per period" is the detail almost everyone misses. The IRS totals the proposed tax, penalties, and interest for each year separately. Each year that stays at or under $25,000 qualifies as a "small case request." Any year that goes over pushes that year — and practically speaking, your whole appeal — into formal-written-protest territory.

That distinction cuts both ways. A one-year exam proposing $30,000 fails the test. But a multi-year exam proposing far more in total can still qualify, because the $25,000 ceiling applies to each tax year on its own, not to the combined balance.

A worked example: $68,500 across three years still qualifies

Say you're a single W-2 employee and the IRS examined your 2022–2024 returns because your broker reported stock sales with zero cost basis — making every dollar of proceeds look like pure gain. The exam report proposes $23,900 for 2022, $22,400 for 2023, and $22,200 for 2024: $68,500 in total, each figure including a 20% accuracy-related penalty stacked on the tax.

Because no single year exceeds $25,000, all three years fit on one Form 12203 — even though the combined amount is nearly triple the ceiling. If the same $68,500 had landed on one tax year, you'd need a formal written protest instead.

Now the substance. Your actual basis in those shares was documented on purchase confirmations the examiner never saw. If the records knock out $17,000 of one year's proposed tax, the penalty computed on that tax falls with it: $17,000 in tax plus the $3,400 penalty (20% of $17,000) — a $20,400 swing from a single year's documentation. This is a hypothetical, not a promise — but it's exactly the kind of math Appeals exists to reconsider, and exactly why "I disagree" needs documents behind it.

What happens if you miss the 30-day window

Miss the deadline on a 30-day letter and the dispute doesn't end — it moves to venues where your footing gets progressively worse. The sequence runs like this:

- The window closes. The exam closes "unagreed." Your right to a pre-assessment Appeals conference through Form 12203 lapses.

- The Notice of Deficiency arrives. The IRS issues a CP3219A Notice of Deficiency — the statutory "90-day letter" — formally proposing to assess the tax.

- The 90-day clock runs. You have 90 days (150 if you're outside the U.S.) to file a Tax Court petition. This is your last chance to dispute the tax without paying it first.

- Assessment and billing. No petition means the tax is assessed. The first bill arrives, and the automated collection notice sequence begins — with interest compounding the whole way.

- Collection appeals only. Once lien and levy notices start, your remaining hearing right is a Collection Due Process request — and in a CDP hearing you generally cannot re-argue the tax itself if you already had the chance to dispute it and passed.

Notice the pattern: every stage you slide past trades a cheap, flexible forum for a slower, stricter one. The table below maps each window and the right attached to it.

| Letter or stage | Response window | The right you keep — or lose |

|---|---|---|

| 30-day letter (Letter 525, 915, or 950) | Typically 30 days from the letter date | File Form 12203 or a formal protest → Appeals review before any tax is assessed |

| CP3219A Notice of Deficiency | 90 days (150 if outside the U.S.) | Petition the U.S. Tax Court without paying the tax first |

| After assessment | No fixed window | Audit reconsideration or pay-and-claim-a-refund — slower, and the IRS holds the balance against you meanwhile |

| Lien filing or final levy notice (LT11 / Letter 1058) | 30 days from the notice date | CDP hearing on collection only — usually not the underlying tax |

Your 30-day window is already running

Get your exam report and Form 12203 reviewed free before the response date on your letter passes. An experienced tax professional will tell you which items are worth fighting — and how to word each one.

Your appeal routes, compared

Form 12203 is one of six ways to challenge an IRS determination, and each route has its own gate. Filing the wrong one wastes days of a window you can't get back:

| Appeal route | When it applies | Limit or deadline |

|---|---|---|

| Form 12203 (small case request) | You disagree with exam findings and hold a 30-day letter | ≤ $25,000 per tax period; file by the letter's response date |

| Formal written protest | Exam dispute over $25,000 for any single period | Same 30-day-letter deadline; strict content requirements |

| Tax Court petition | After a CP3219A Notice of Deficiency | 90 days from the notice; no prepayment required |

| Form 12153 CDP hearing | After a lien-filing notice or final levy notice | 30 days from the notice date; collection issues, not usually the tax |

| Audit reconsideration | Deadlines missed, but you have new documentation | Available any time before the balance is fully paid |

| Form 13711 OIC appeal | Your Offer in Compromise was rejected | 30 days from the rejection letter |

One more cost to price in: appealing doesn't pause interest. Interest keeps accruing on whatever portion of the proposed tax Appeals ultimately sustains, calculated back to the return's original due date — you can estimate what months of waiting could add with our Penalty & Interest Calculator. Two ways to limit it: pay any portion you actually agree with now, or send a deposit toward the disputed amount, which generally stops interest on that amount as of the day the IRS receives it.

What to write on Form 12203

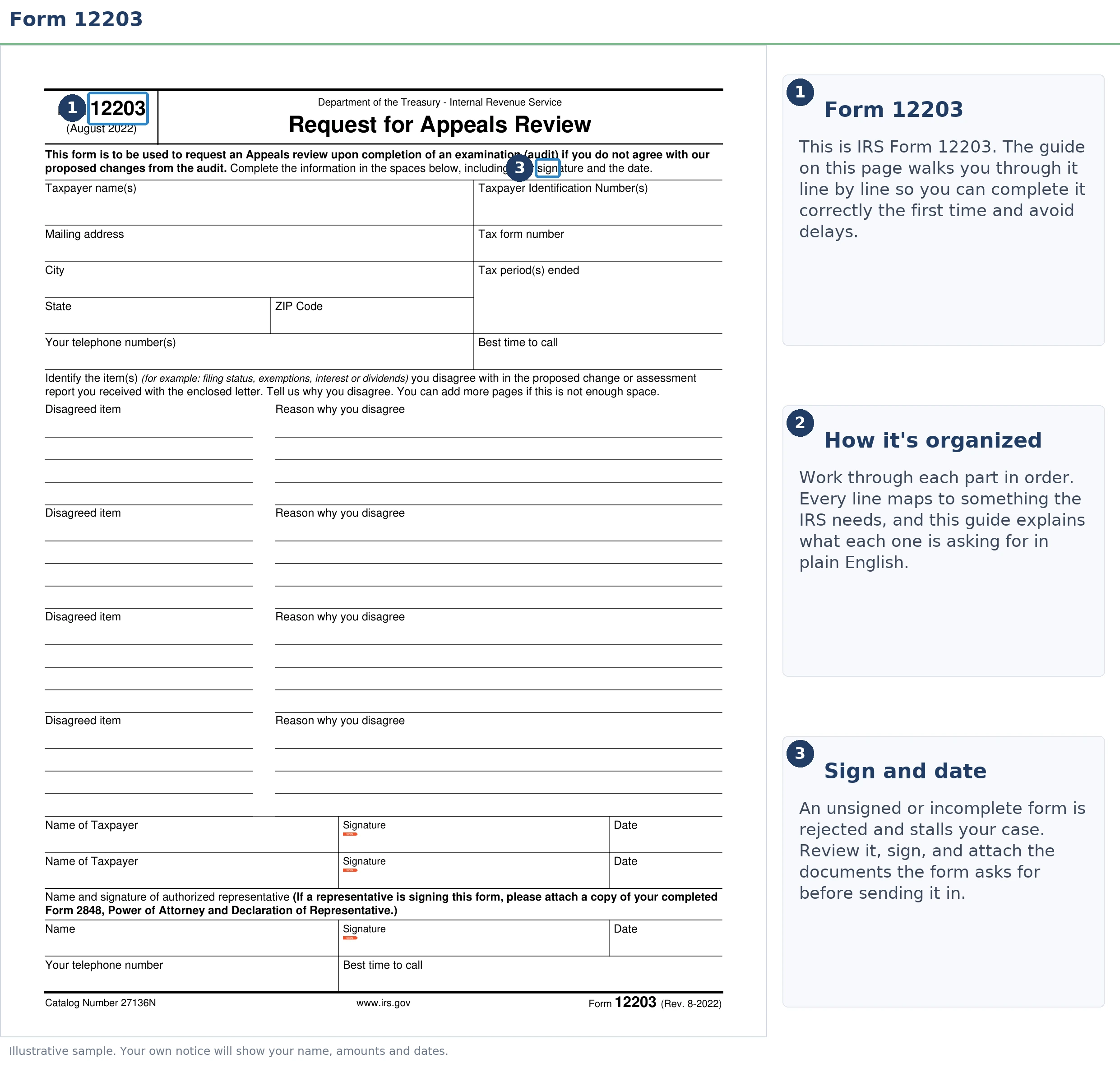

The entire appeal fits on one page, and the disagreed-items section decides whether it works. The form asks for your name, taxpayer identification number, address, and phone; the tax form you filed (for most readers, Form 1040) and the tax periods you're appealing; each item you disagree with and a brief reason why; your representative's information if someone is handling it for you; and your signature.

Three rules make the difference between an appeal that gets traction and one that stalls:

- One adjustment per entry, with a factual reason. "Disallowed cost basis — actual basis of $55,000 documented on attached purchase confirmations" gives the Appeals officer something to work with. "The examiner is wrong" gives them nothing.

- Facts and documents, never protests about fairness. Appeals settles on evidence and litigation risk. Arguments the IRS considers frivolous — constitutional objections, "wages aren't income" — forfeit consideration entirely and can trigger penalties.

- Dispute the penalties separately. If the report stacks an accuracy-related penalty on the tax, list it as its own disagreed item and state your reasonable-cause facts. Penalties are often the most negotiable line on the report — and if you've already lost a penalty fight elsewhere, a penalty abatement appeal follows similar logic.

One scope note: Form 12203 is built for examination disputes. If a different IRS letter — a penalty denial, for instance — lists its own appeal instructions or a different form, follow that letter. The appeal route is always dictated by the document in your hand.

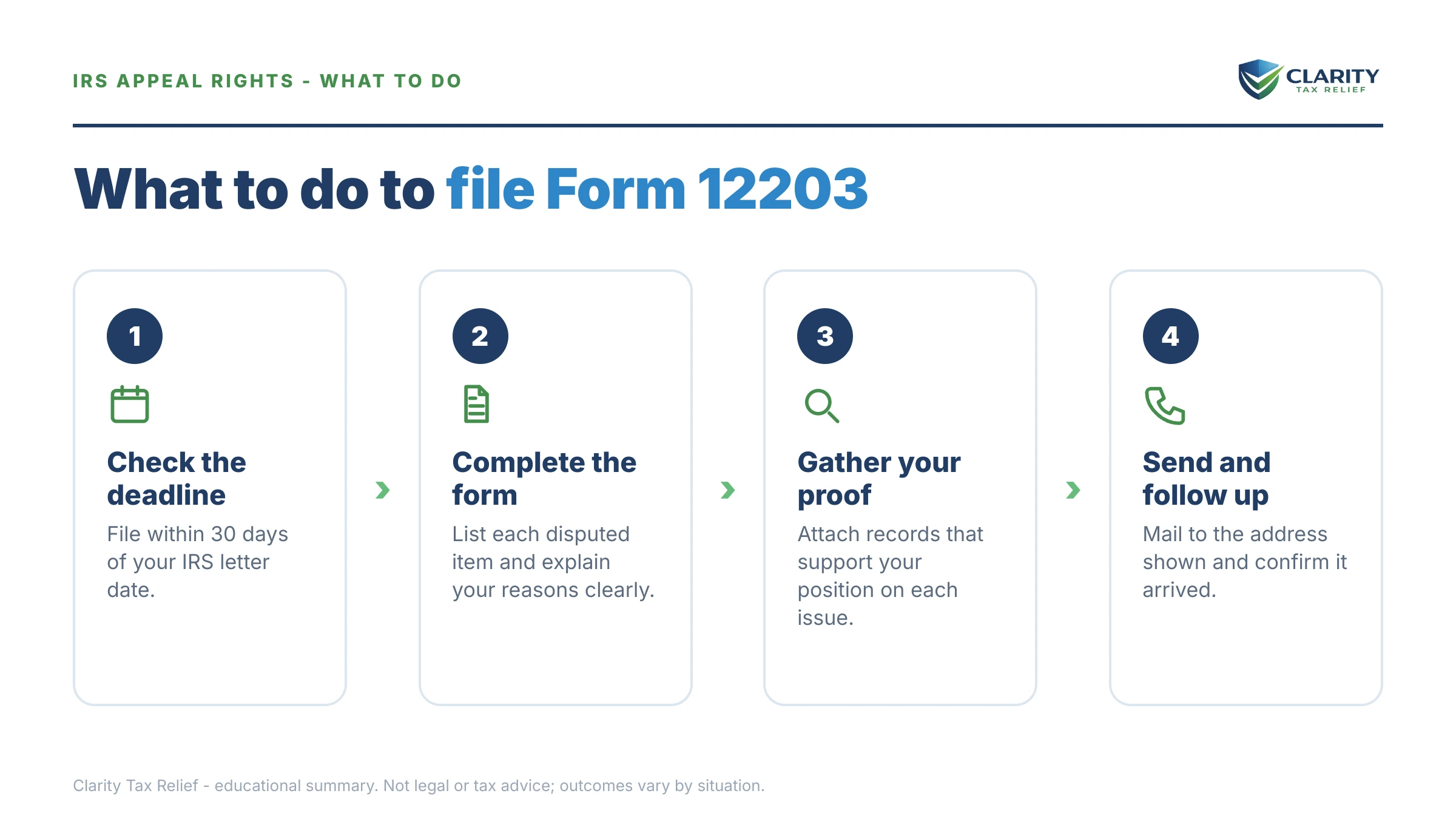

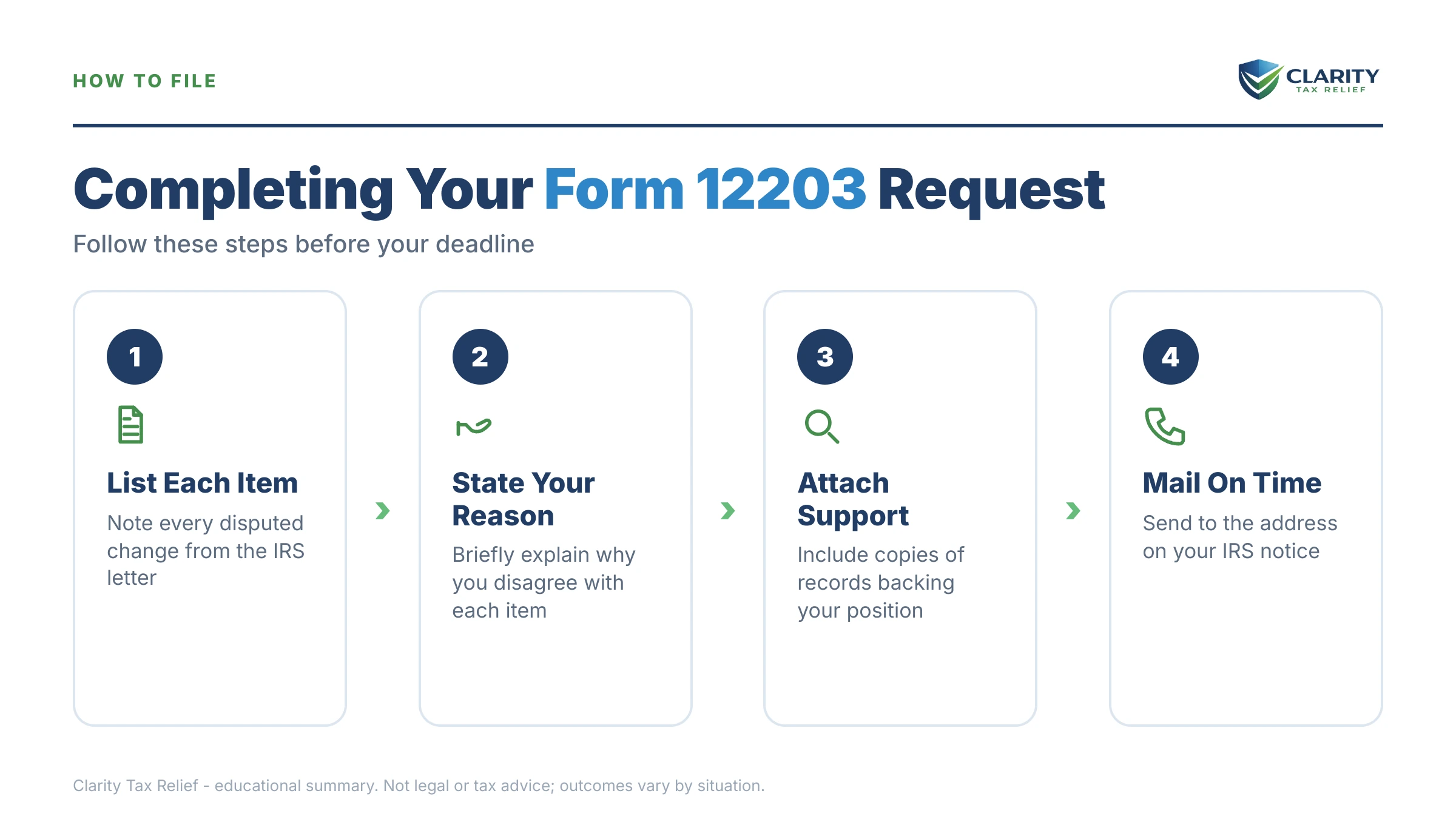

How to respond with Form 12203, step by step

- Find your deadline. Locate the response date on your 30-day letter — usually 30 days from the letter date — and write it down. Everything else works backward from that date.

- Confirm you qualify. Total the proposed tax, penalties, and interest for each tax period. If every period is $25,000 or less, Form 12203 works; if any period is over, you need a formal written protest instead.

- List each disagreed item. Enter every adjustment you dispute in its own entry, with a short factual reason — "cost basis of $55,000 documented on attached broker statements," not "this is unfair."

- Attach copies of your proof. Include copies (never originals) of the records that support each item: broker statements, receipts, corrected forms, canceled checks.

- Send it to the address on your letter. Mail or fax Form 12203 to the office that sent your 30-day letter — not to Appeals directly — and keep proof of mailing or the fax confirmation.

- Prepare for the Appeals conference. Organize your documents by issue, decide whether a representative will speak for you, and be ready to discuss a settlement number for each item.

When you can handle this appeal yourself

Plenty of Form 12203 appeals are genuinely do-it-yourself. If you're disputing one or two clear-cut items — a documented basis figure, a payment the exam missed, a dependent you can prove — and you have the paper to back each one, the small-case process was designed for exactly you. File the one-page form, attach clean copies, show up prepared, and you may resolve it without spending a dollar on help.

Experienced help changes outcomes in the harder versions: any period over $25,000, where a formal protest's format requirements can sink an otherwise-winnable case; multi-year exams where conceding one year's issue affects the others; penalty disputes that turn on how reasonable-cause facts are framed; and any case where the IRS asks you to extend the assessment statute, since that decision shapes all your leverage. A representative can also attend the Appeals conference for you entirely — you'd authorize that with Form 2848 — which matters when the weakest thing in the room would be an anxious taxpayer talking too much.

A practical 2026 note: Appeals is working through the same staffing cuts as the rest of the IRS, so conferences take longer to schedule and are frequently held by phone or video. Slow doesn't mean stalled — but it does mean your written submission carries more weight than ever, because it may be most of what the officer reads before forming a view.

Terms on your letter, decoded

- 30-day letter — the exam-closing letter (Letter 525, 915, or 950) that gives you roughly 30 days to accept the findings or appeal.

- Small case request — the simplified appeal, filed on Form 12203, available when each tax period's total is $25,000 or less.

- Form 4549 — the examination report attached to your letter, itemizing every proposed adjustment, penalty, and interest figure.

- Independent Office of Appeals — the IRS function, separate from exam, that resolves disputes without litigation and has authority to settle.

- Hazards of litigation — Appeals' authority to concede all or part of an issue based on the risk the IRS would lose it in court.

- Notice of deficiency — the statutory "90-day letter" (CP3219A) that issues if you don't appeal or Appeals can't resolve the case, opening your Tax Court window.

For the source documents: the IRS's official page for the form is About Form 12203, the Appeals process is described at the IRS Independent Office of Appeals, and if your case stalls inside the system, the Taxpayer Advocate Service exists for exactly that.

Form 12203 questions, answered

What is Form 12203 used for?

Form 12203, Request for Appeals Review, is the simplified "small case request" for disputing IRS examination findings of $25,000 or less per tax period. You typically file it in response to a 30-day letter such as Letter 525 or Letter 950, and it sends your case to the IRS Independent Office of Appeals before the tax is assessed. It is not used for collection disputes — those go through Form 12153.

Is the $25,000 limit on Form 12203 per year or in total?

Per tax period, not in total. The IRS applies the $25,000 small-case ceiling to each tax year (or period) separately, counting proposed tax, penalties, and interest for that period. So a three-year exam proposing $68,500 in total can still qualify for Form 12203 if no single year exceeds $25,000 — but a single year at $30,000 cannot, even if it is your only disputed year.

Where do I send Form 12203?

To the IRS office named in your 30-day letter — the address or fax number is printed on the letter itself, and that office forwards your case to Appeals. Do not mail it directly to the Independent Office of Appeals; that can delay routing past your deadline. Send copies, keep the originals, and use certified mail or keep a fax confirmation so you can prove the date it was filed.

What if I owe more than $25,000 for one tax year?

You can still appeal, but you must file a formal written protest instead of Form 12203. A protest is a signed letter that states the facts, the adjustments you dispute, the law or authority you rely on, and a penalties-of-perjury declaration. The deadline is the same — the response date on your 30-day letter — and getting the format wrong can cost you the appeal, which is where experienced help earns its keep.

How long does an Appeals review take after filing Form 12203?

There is no fixed timeline — several months is common, and with IRS staffing down roughly 27% since 2025, waits have stretched longer for many cases. Interest continues to accrue on any amount ultimately sustained. If the assessment statute is running short, the IRS may ask you to sign Form 872 to extend it as a condition of Appeals consideration — a decision worth professional input before you sign.

Does filing Form 12203 stop penalties and interest?

No. Interest keeps running on whatever portion of the proposed tax is ultimately upheld, calculated back to the return's original due date. You can limit the damage two ways: pay any portion you agree with now, or send a deposit toward the disputed amount — if you lose, interest generally stops on the deposited amount as of the date the IRS received it.

What is the difference between Form 12203 and Form 12153?

Form 12203 appeals what you owe; Form 12153 appeals how the IRS collects it. You file Form 12203 before assessment, in response to a 30-day letter after an exam, to dispute the proposed tax itself. Form 12153 requests a Collection Due Process hearing after a lien filing or final levy notice — and in a CDP hearing you generally cannot re-argue the underlying tax if you already had a chance to dispute it.

What happens if Appeals does not agree with me?

You are not out of options. Appeals often settles cases partially, conceding some issues based on the hazards of litigation, so a mixed result is common. If no agreement is reached, the IRS issues a CP3219A Notice of Deficiency, which starts a 90-day window to petition the U.S. Tax Court without paying first. After that, your remaining paths are paying and claiming a refund, or audit reconsideration with new documentation.

Your next 24 hours

- Find the response date printed near the top of your 30-day letter, then total the proposed amount for each tax year on the attached Form 4549 — that tells you whether Form 12203 or a formal protest is your route.

- Gather your evidence: the letter and exam report, your return for each audited year, and the documents that prove the items you dispute — broker statements, receipts, canceled checks.

- Get a free case review before you spend a day of the window guessing — the 2-minute form or (888) 825-7779. An experienced tax professional will tell you which items are worth fighting and how to word each one before your letter's deadline arrives.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.