IRS Notices

IRS LT16 Notice: What It Means and What to Do (2026)

The short answer: an LT16 notice is a letter from the IRS Automated Collection System (ACS) saying your account is overdue — an unpaid balance, unfiled tax returns, or both — and asking you to call. It is not a levy notice yet, but your account is now in active collections. Respond by the date printed on the letter.

You're rebuilding after the divorce — new address, new bank account, half the income — and now a one-page IRS letter is telling you to "please call us about your overdue taxes or tax return." An LT16 is deliberately vague, and that vagueness is what makes it frightening. It's also fixable: this page maps exactly what the letter means, what it can and cannot do to you, and the order to fix it in.

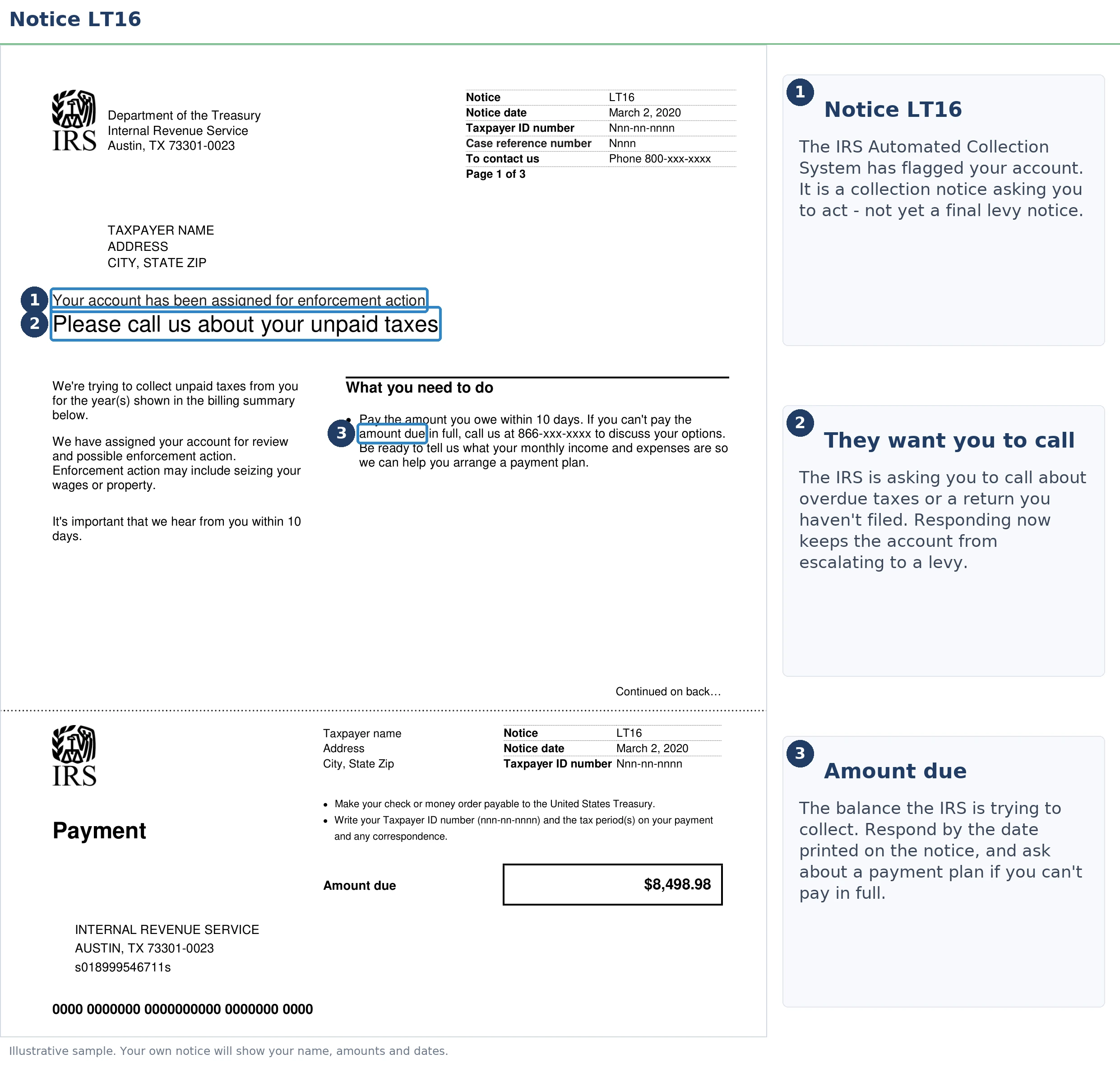

The LT16 is unusual among IRS collection letters in one specific way: it's the one common ACS letter that can cover both an unpaid balance and unfiled returns at the same time. That means your first job is figuring out which problem — or both — put your name in the ACS queue. The image below shows exactly what an LT16 looks like and where to find the response date, the tax years involved, and the phone line the letter wants you to call.

⏱ Your deadline: the response date printed on your LT16 — that date on your copy controls. There is no grace period after it: interest and a 0.5% monthly late-payment penalty keep compounding, and ACS queues the next, more forceful letter in the sequence.

Why you got an LT16 notice

The IRS sends an LT16 when the Automated Collection System — ACS, the IRS's centralized phone-based collection unit — has taken over your account for an unpaid balance, missing returns, or both. Unlike the CP-series bills that come from the service center that processed your return, an LT-series letter means your account has moved from billing into active collection status. (For general letter triage across every notice type, see our hub on why did I get a letter from the IRS — this page covers only the LT16.)

Three situations commonly trigger it. You filed and owe, and earlier CP-series bills went unanswered — often because they went to an old address after a move or divorce. Or the IRS's records show one or more returns were never filed. Or both: a balance from one year, a missing return from another. The letter lists the specific tax years, so read that section before anything else.

One more 2026 reality worth knowing: the IRS workforce shrank roughly 27% in 2025, so the humans behind the ACS phone line are stretched thin. The letters, however, are generated automatically — the system that mailed your LT16 doesn't slow down just because the phone queue does.

LT16 vs. LT11: where this letter sits in the ACS series

An LT16 is a collection contact letter, not a levy notice — the letter that authorizes wage and bank levies is the LT11 notice, and it hasn't arrived yet. The LT series can feel like alphabet soup, so here's the decoder:

| Letter | What it says | What it demands |

|---|---|---|

| LT14 | "We need to talk" — balance due | Contact ACS about an unpaid balance |

| LT16 (you are here) | Overdue taxes and/or overdue returns | Call ACS; pay, arrange payment, or file — by the printed date |

| LT18 | Overdue returns — sharper follow-up | Submit the missing returns now |

| LT19 | Pay the amount you owe | Full payment or a payment arrangement |

| LT24 | Financial information needed | A completed Form 433 collection statement |

| LT26 | File your overdue tax returns | The missing returns, before the IRS files for you |

| LT11 | Final Notice of Intent to Levy | Response within 30 days or levies become legal |

The takeaway: LT16 is mid-sequence. You still have room to choose your resolution instead of having one imposed — but the room shrinks with every letter that follows.

What happens if you ignore an LT16

An ignored LT16 moves your account toward the LT11 final notice — the letter that lets the IRS levy wages and bank accounts 30 days after it's issued. The sequence is automated, and it runs in stages:

- More ACS letters. Depending on your account, that's an LT19 demanding payment, an LT26 demanding returns, or an LT24 demanding a completed financial statement. The balance grows monthly the entire time.

- A federal tax lien becomes likely. A filed lien is a public claim against everything you own — a real problem if the divorce left you planning to sell or refinance the house.

- LT11 / Letter 1058 — the final notice. This starts a 30-day clock and your Collection Due Process rights, requested on Form 12153. Miss that window and you lose your strongest appeal right.

- Levy. Bank accounts can be frozen with a 21-day hold before the money leaves; a wage levy is continuous until released; Social Security can be reduced by up to 15% through the Federal Payment Levy Program.

- If returns are missing: a substitute-for-return assessment. The IRS files for you using only reported income — no deductions, no credits, no filing status better than single — and then collects on that inflated number.

None of this happens tomorrow. All of it happens eventually, on autopilot, and each stage costs more to unwind than the one before it.

Holding an LT16 right now?

Before you dial the ACS line, get your LT16 reviewed free — an experienced tax professional will confirm whether it's a balance, missing returns, or both, and what to say (or not say) before the date on your letter passes. Call (888) 825-7779 or use the 2-minute form.

Can't pay the balance on your LT16? Your real options

A balance under $50,000 fits the IRS's streamlined installment agreement range — spread over up to 72 months, usually without a full financial disclosure. The LT16 itself only offers "call us and pay," but ACS can approve every program below. Here's how they compare for a mid-five-figure balance:

| Option | Who it fits | Cost & catch |

|---|---|---|

| Pay in full | You have the cash or can raise it | $0 setup; stops all accruals and the letter sequence immediately |

| Short-term plan (180 days) | Money is coming — a bonus, a home-sale closing, a settlement | $0 setup; interest and penalties still accrue until paid |

| Streamlined installment agreement | Balances up to $50,000; up to 72 months, set up online | Setup fee applies (lower with direct debit); accruals continue while you pay |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses | Requires financial disclosure (Form 433-F); debt remains and a lien is still possible |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt | $205 fee, 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief | Clean compliance the prior 3 years, or a reasonable-cause event | Free to request; starting summer 2026, the new Automatic Exemption from Penalty (AEP) applies some relief with no request at all |

A worked example (hypothetical). Say you owe $27,500 from a jointly filed year and you're now on one income. A short-term plan means roughly $27,500 ÷ 6 ≈ $4,583 a month for six months — realistic only if house-sale proceeds are coming. A 72-month streamlined agreement starts near $27,500 ÷ 72 ≈ $382 a month, though the IRS sets the actual payment slightly higher because interest and the 0.5% monthly failure-to-pay penalty keep accruing until the balance hits zero — paying $475–$500 instead shaves months and real dollars off the total. An Offer in Compromise only enters the picture if the IRS's math shows it could never collect $27,500 from your equity and future income; post-divorce, with home equity split and income halved, that math sometimes genuinely works — but it's a calculation, not a wish. You can estimate what waiting costs with our IRS Penalty & Interest Calculator.

Divorced and holding an LT16 for a joint tax year

Both spouses on a joint return owe 100% of the tax — the IRS can collect the entire balance from either person, regardless of what the divorce decree says. If your decree assigns the tax debt to your ex, that gives you a claim against your ex in state court; it is not a defense the IRS will honor. Our guide to divorce and IRS debt: who pays covers that split in detail.

Three things change the answer for divorced LT16 recipients. First, if the debt exists because your ex underreported income or overstated deductions without your knowledge, innocent spouse relief (Form 8857) can remove your liability for their portion. Second, if the LT16 flags an unfiled year, confirm whose obligation it was — a year your ex was supposed to file jointly and didn't is a mess you want documented now, not at the levy stage. Third, update your address with the IRS immediately; the most dangerous letter in this sequence is the LT11 you never receive because it went to the marital home.

If your LT16 is about unfiled returns

Filing beats paying, every time: the failure-to-file penalty runs 5% per month — ten times the 0.5% monthly failure-to-pay penalty. If your LT16 lists missing returns, filing them is the single highest-value move you can make this week, even if you can't send a dollar with them.

Filing also blocks the substitute-for-return. When the IRS files a substitute return for you, it uses only the income reported by employers and banks, allows no deductions or dependents, and assesses the worst-case tax. Your own late return replaces that number with the real one. And if any missing year would have produced a refund, you have only three years from that return's original due date to claim it — a deadline that expires quietly.

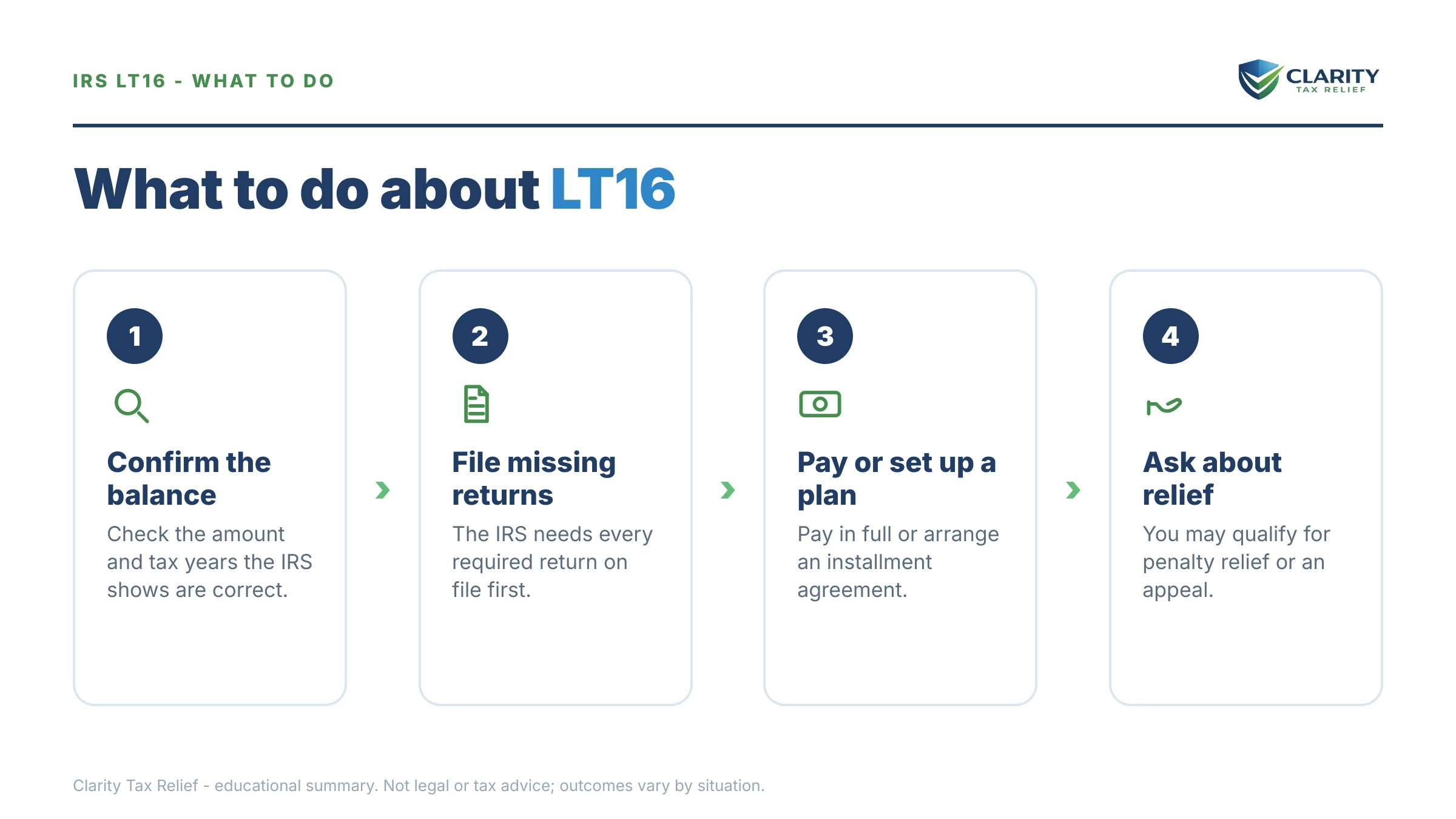

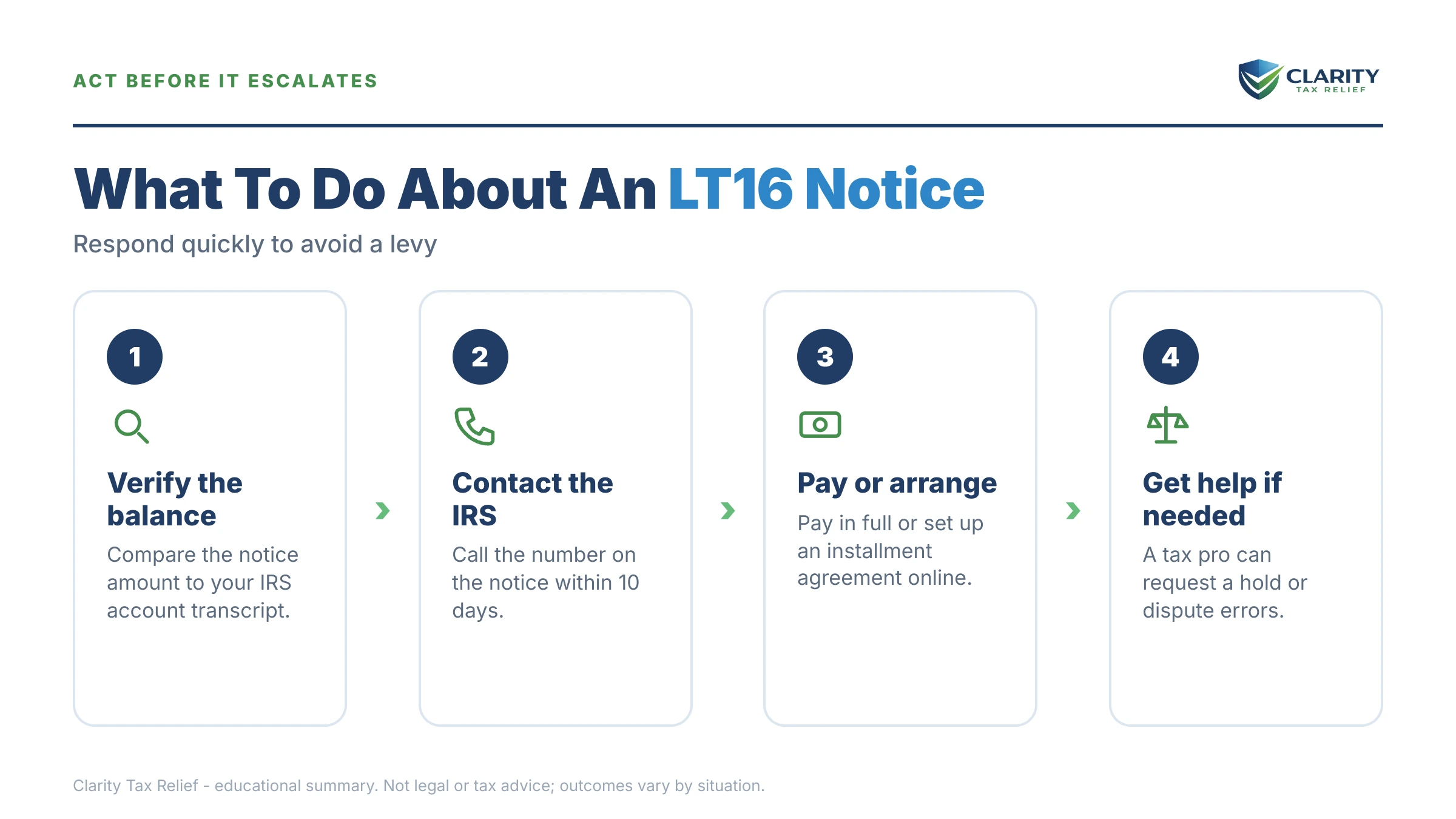

How to respond to an LT16, step by step

- Decode the letter. Identify whether your LT16 lists a balance due, missing returns, or both, and note the response date and the tax years printed on it.

- Verify with your own records. Log into your IRS online account and compare its balance and filed-return history against the letter before you call anyone.

- File any missing returns. Filing stops the 5%-per-month failure-to-file penalty and blocks the IRS from filing a substitute return without your deductions.

- Pick your resolution before you dial. Decide on full payment, a 180-day short-term plan, an installment agreement, hardship status, or an offer before you call, so ACS doesn't decide for you.

- Call ACS — or have a professional call for you. Use the number on the notice, write down the agent's name and ID number, and get any agreement's terms confirmed in writing.

If you're calling yourself, go in prepared — our guide on what to say when calling the IRS about back taxes includes scripts for exactly this conversation. Payments and plan setup live at IRS.gov/payments and the IRS payment plans page.

When you can handle an LT16 yourself

You can usually resolve an LT16 on your own when you agree with the balance, your returns are all filed, and you can pay within 180 days or afford the streamlined monthly payment. In that case: verify the numbers online, set up the plan through your IRS account, and confirm the LT16's tax years are all covered by it. No professional needed.

Experienced help changes the outcome in a narrower set of situations: multiple unfiled years (the order you file in affects penalties and refund claims), a joint-liability fight with an ex-spouse (innocent spouse cases are won on documentation), income that ACS will demand a financial statement to analyze, or a prior final notice on the same year — meaning levy authority may already exist and the timeline is shorter than the LT16 suggests. A professional holding your Form 2848 power of attorney can also sit on the ACS hold line so you don't have to. If ACS won't work with you or a levy would create genuine hardship, the independent Taxpayer Advocate Service exists for exactly those cases.

Terms on your LT16, decoded

- ACS (Automated Collection System): the IRS's centralized, phone-based collection unit — no single officer owns your case; whoever answers works from the same file.

- Levy: the actual taking of money or property — wages, bank funds, certain federal payments.

- Lien: a public legal claim against your property that secures the debt; it takes nothing by itself but complicates selling or refinancing.

- CDP (Collection Due Process): your right, after a final levy notice, to a hearing requested on Form 12153 — the strongest appeal right in the collection process.

- SFR (Substitute for Return): a return the IRS prepares for a non-filer using only reported income, with no deductions or credits.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, though appeals, offers, and bankruptcy pause the clock.

LT16 questions, answered

Is an IRS LT16 notice serious?

Yes — an LT16 means your account is in active collections with the IRS Automated Collection System, not just the billing cycle. Nothing can be levied on this letter alone, but the balance grows monthly and the next stage is the LT11 final notice, which authorizes wage and bank levies after 30 days. Respond by the date printed on the letter.

Do I have to call the phone number on my LT16?

No — calling is what the letter asks for, but it isn't the only way to respond. You can set up a payment plan through your IRS online account, file missing returns by mail or e-file, or authorize an experienced tax professional with Form 2848 to call ACS for you. With IRS staffing down roughly 27% since 2025, expect long hold times if you dial yourself.

Can the IRS levy my bank account after an LT16?

Not based on the LT16 alone. Wage and bank levies require a final notice of intent to levy — the LT11 or Letter 1058 — plus a 30-day window for you to request a Collection Due Process hearing. The exception: if you already received a final notice for the same tax year in the past, levy authority may already exist, so check your notice history in your IRS online account.

What if my LT16 is about unfiled returns and I don't owe anything?

File the returns anyway, as fast as you can. If you're owed refunds, you can only claim them within three years of the original due date — after that the money is gone for good. If you don't file, the IRS can prepare a substitute for return using only reported income, with no deductions or credits, and turn a no-balance year into a bill.

My ex-spouse caused this tax debt — do I still have to pay it?

If the balance comes from a jointly filed return, yes — both signers owe 100% of it, and the IRS is not bound by your divorce decree. Your decree gives you a claim against your ex in state court, not a defense against the IRS. If your ex hid income or you signed under pressure, innocent spouse relief through Form 8857 may remove your share of the liability.

What happens if I ignore an LT16 notice?

The account keeps moving through the automated collection sequence. Expect follow-up ACS letters demanding payment or financial information, a possible federal tax lien, and eventually the LT11 final notice — after which the IRS can levy bank accounts (with a 21-day hold) and garnish wages continuously. Interest and a 0.5% monthly failure-to-pay penalty accrue the entire time.

How do I know my LT16 is real and not a scam?

A genuine LT16 arrives by postal mail with your name, the tax years involved, and an IRS return address — the IRS does not initiate contact by text, email, or social media. Verify the balance yourself by logging into your account at IRS.gov before paying anything. Real payments go only to the United States Treasury or through IRS.gov, never gift cards or payment apps.

Your next 24 hours

- Find three things on your LT16: the response date, the tax years listed, and whether it names a balance due, missing returns, or both. Those three facts determine your entire plan.

- Gather your file: the letter itself, your last filed return, recent pay stubs, and — if a joint year is involved — your divorce decree. Then log into your IRS online account to see what the IRS sees.

- Get the free case review before the date on your letter passes: (888) 825-7779 or the 2-minute form. Every week you wait, interest and the monthly penalty compound — and the next letter in the ACS sequence gets closer to levy power.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.