IRS Letters

IRS Letter 692: How to Respond to Additional Audit Findings (2026)

The short answer: IRS Letter 692 — "Request for Consideration of Additional Findings" — arrives with a revised audit report (Form 4549) after you responded to the original exam findings. You typically have 15 days from the date on the letter to agree, send more documents, or request an appeal before the IRS moves toward a Notice of Deficiency.

You thought the back-and-forth was done. You already answered the audit once — mailed in the records, made your case — and now the IRS has answered back with Letter 692 and a "corrected" report that still shows a balance. That's frustrating, especially when the audit dug into your first return after a divorce. But this letter is actually good news in one specific way: the examiner read your response, and you still have a decision to make — you just have very little time to make it.

Two things make Letter 692 different from every other audit letter: it means the numbers changed (or the examiner formally rejected your evidence), and it carries one of the shortest response windows in the entire exam process. The image below shows exactly what this letter looks like and where to find the two items that matter most — your response date and the revised balance on the attached Form 4549.

⏱ Your deadline: the response date printed on your Letter 692 — typically 15 days from the letter's date. That printed date controls. Miss it and the examiner closes your case as unagreed, which triggers a statutory Notice of Deficiency and takes the free IRS Appeals path off the table for now.

Why you got IRS Letter 692

Letter 692 means an IRS examiner reviewed your response to an audit report and issued revised findings you must now accept or dispute. It never arrives out of nowhere — it only follows an earlier exam report, usually one sent with a Letter 525 audit report or Letter 915, that you (or your preparer) answered.

The examiner's reply comes in one of three flavors, and the attached revised Form 4549 tells you which one you got:

- Partial win. The examiner accepted some of your documentation and reduced the proposed tax — but not to zero. This is the most common version.

- Evidence rejected. The examiner considered your response and kept the original numbers. The letter documents that your material was reviewed and found insufficient.

- Findings expanded. Less common, but your response can open new issues — the revised report proposes more than the original did. Compare both reports line by line before assuming the balance went down.

For a plain-English overview of how audit letters fit into IRS mail generally, see why did I get a letter from the IRS — this page stays focused on what's unique to the 692.

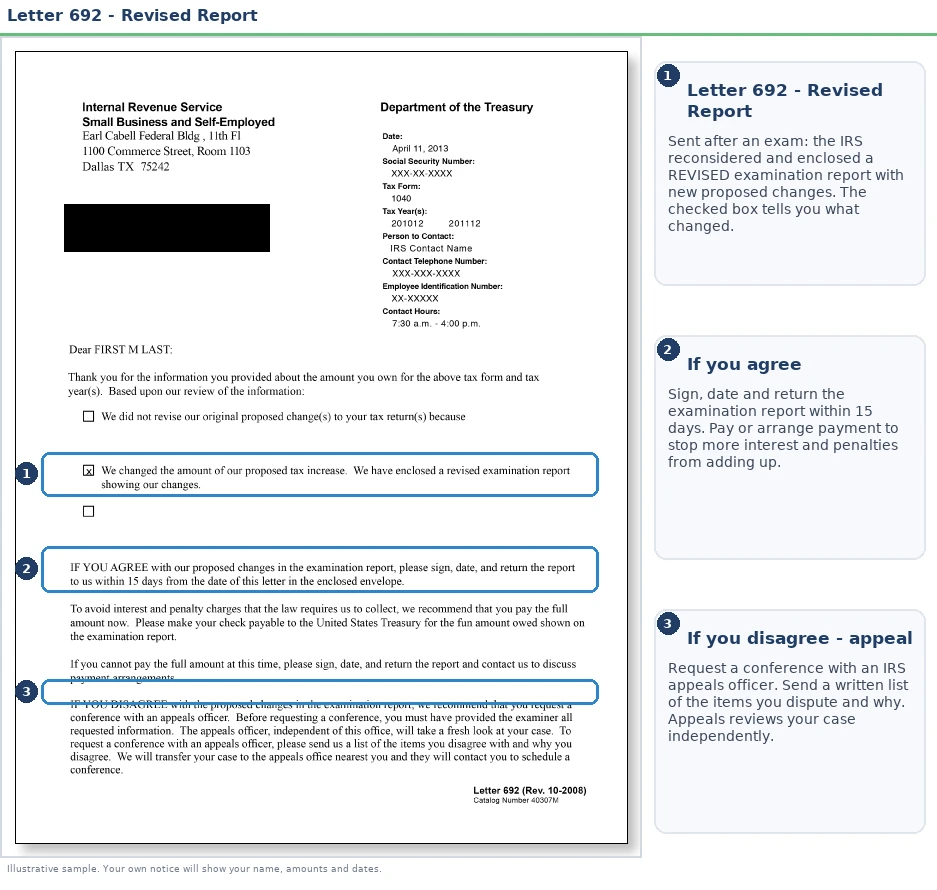

What's actually inside: the revised Form 4549

The document that matters in the Letter 692 packet is the revised Form 4549, Income Tax Examination Changes — the letter itself is mostly a cover page. The 4549 shows, line by line, each adjustment the examiner is proposing, the recalculated tax, any penalties, and interest computed to a stated date.

Read three spots carefully:

- The adjustments section — which specific items (filing status, a dependent, a credit, a deduction) the examiner changed or kept.

- The penalty line — audit adjustments frequently carry the 20% accuracy-related penalty, and it should have been recalculated on the revised, lower tax if your numbers came down.

- The signature block — signing the 4549 is consent to immediate assessment. It closes the case as "agreed" and waives your right to a Notice of Deficiency and Tax Court. Never sign it as an acknowledgment of receipt; it is far more than that.

If your audit involved a dependent both you and your ex-spouse claimed — a very common trigger in the first year after a divorce — the tiebreaker rules the examiner applied are explained in our guide to both parents claiming the same child.

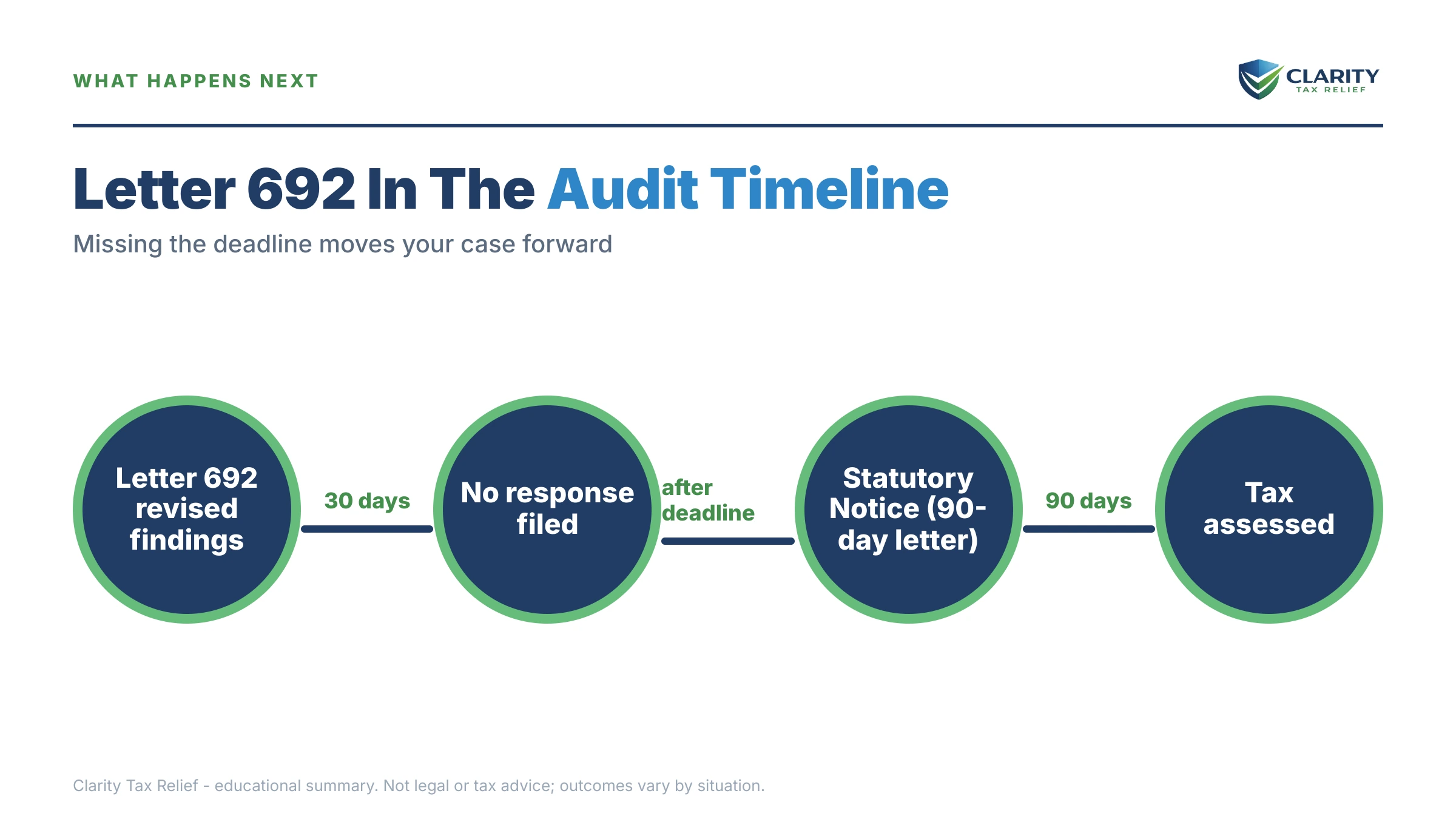

What happens if you ignore Letter 692

Ignoring Letter 692 doesn't end your audit — it converts it into an unagreed case that moves, stage by stage, toward assessment and collection. Nothing is levied at this point, and no one is accusing you of fraud. But each stage below strips away an option you have today:

- Letter 692 — you are here. Typically 15 days to agree, send new evidence, or request an Appeals conference. This is the last stop where a phone call to the examiner can still change the numbers.

- Notice of Deficiency. The IRS issues a CP3219A Notice of Deficiency (or Letter 531). You now have 90 days to petition the U.S. Tax Court — the 90-day letter and Tax Court petition process. The informal Appeals door closes for now.

- Assessment and first bill. If the 90 days pass without a petition, the tax is assessed. A balance-due notice arrives, interest keeps compounding, and the 0.5%-per-month failure-to-pay penalty starts running on the assessed amount.

- Collection notices, then final notice. Unpaid audit assessments feed into the same automated collection stream as any other tax debt, ending at a Letter 1058 final notice of intent to levy — a 30-day clock, then wage and bank levies become legally possible.

| Letter or notice | Where it falls in the audit | Typical response window |

|---|---|---|

| Letter 525 / Letter 915 (30-day letter) | Transmits the original examination report | 30 days to agree or protest |

| Letter 692 | Examiner's revised findings after your response | Typically 15 days — the printed date controls |

| CP3219A / Letter 531 (Notice of Deficiency) | Statutory notice before assessment of unagreed changes | 90 days to petition the U.S. Tax Court |

| Letter 1058 (Final Notice of Intent to Levy) | Collection stage, after assessment goes unpaid | 30 days before levies become legally possible |

One 2026 reality check: IRS exam staffing is thinner after the 2025 workforce cuts, but this pipeline is largely automated. Silence is read as agreement-by-default, and the machine moves to the next stage on schedule.

Holding a Letter 692 right now?

Your response date is printed on the letter, and it's typically only 15 days out. Send us the letter and the revised report — an experienced tax professional will tell you whether the examiner's numbers hold up and which response protects you, free and confidential, before that date passes.

Your options after Letter 692

Letter 692 gives you four real choices, and the right one depends on whether the revised numbers are correct and how much is in dispute. Here they are side by side:

| Option | Upfront cost | Typical timeline | Best when |

|---|---|---|---|

| Sign Form 4549 and pay | $0 (plus the balance) | Days — case closes as agreed | The revised numbers are right and you can pay |

| Sign, then set up a payment plan | $0 for short-term plans; a setup fee applies to long-term plans | Weeks to establish once the bill posts | Numbers are right but you can't pay in full |

| Send additional documentation | $0 | Weeks — examiner can revise again | You have records the examiner hasn't seen |

| Small-case appeal (Form 12203) | $0 | Often several months at Appeals | Dispute is $25,000 or less per tax period |

| Formal written protest to Appeals | $0 to file (drafting help often advisable) | Often longer than small-case appeals | Any period's dispute exceeds $25,000 |

| Wait for the 90-day letter, petition Tax Court | Modest court filing fee (around $60) | Many months; most cases settle before trial | You want maximum leverage and formal review |

Three details that decide which row is yours:

- The $25,000 line. If the total proposed change is $25,000 or less for each tax period, the Form 12203 small-case appeal is a one-page request — no legal citations required, just the items you dispute and why. Above that line, a formal protest must lay out facts, law, and a penalties-of-perjury statement. Our overview of IRS audit appeal rights covers what Appeals officers can do that examiners can't — including settling based on the hazards of litigation, meaning the realistic risk each side faces in court.

- Agreeing doesn't mean paying today. Signing the 4549 triggers assessment and a bill; from there you can pay online, arrange an installment agreement, or pursue penalty relief. Interest continues either way — you can estimate what penalties and interest add over time with our penalty and interest calculator.

- Penalties are separately negotiable. Even if the tax adjustment stands, the accuracy-related penalty can sometimes be removed for reasonable cause — for example, where you relied in good faith on a divorce decree or on a preparer's advice about who claims the child. Raise the penalty specifically in any appeal; don't treat the bottom-line number as one indivisible block.

A worked example: the revised report says $11,300

A hypothetical shows how the same Letter 692 balance can end three very different ways. Say you owe $11,300 per the revised Form 4549: you're recently divorced, the audit disallowed your head-of-household filing status and the child tax credit because your ex-spouse claimed your daughter, and the examiner accepted only part of the school records you sent. The breakdown: $9,100 in tax, a $1,820 accuracy-related penalty (20% × $9,100), and roughly $380 of interest computed from the return's original due date.

- Path 1 — sign and set up a plan. $11,300 is under the $50,000 online threshold, so a streamlined installment agreement over up to 72 months works out to roughly $157 a month ($11,300 ÷ 72) before the interest and 0.5%-per-month failure-to-pay penalty that continue to accrue on the shrinking balance. Here's how to set up an IRS payment plan online.

- Path 2 — appeal the split issues. Suppose your custody order and school records genuinely support head-of-household even if the credit goes to your ex under the tiebreaker rules. If Appeals allows the filing status but not the credit, the tax portion might drop from $9,100 to $5,400; the 20% penalty recalculates to $1,080, and the balance falls to roughly $6,480 plus interest — a five-figure problem becomes a four-figure one.

- Path 3 — do nothing. The same $11,300 rides through a Notice of Deficiency, gets assessed, and grows monthly until a final levy notice arrives. Nothing about waiting makes the number smaller.

The point isn't that appeals always win — they don't. It's that on a Letter 692, the difference between paths is decided in about two weeks, and the math is worth running before the window closes.

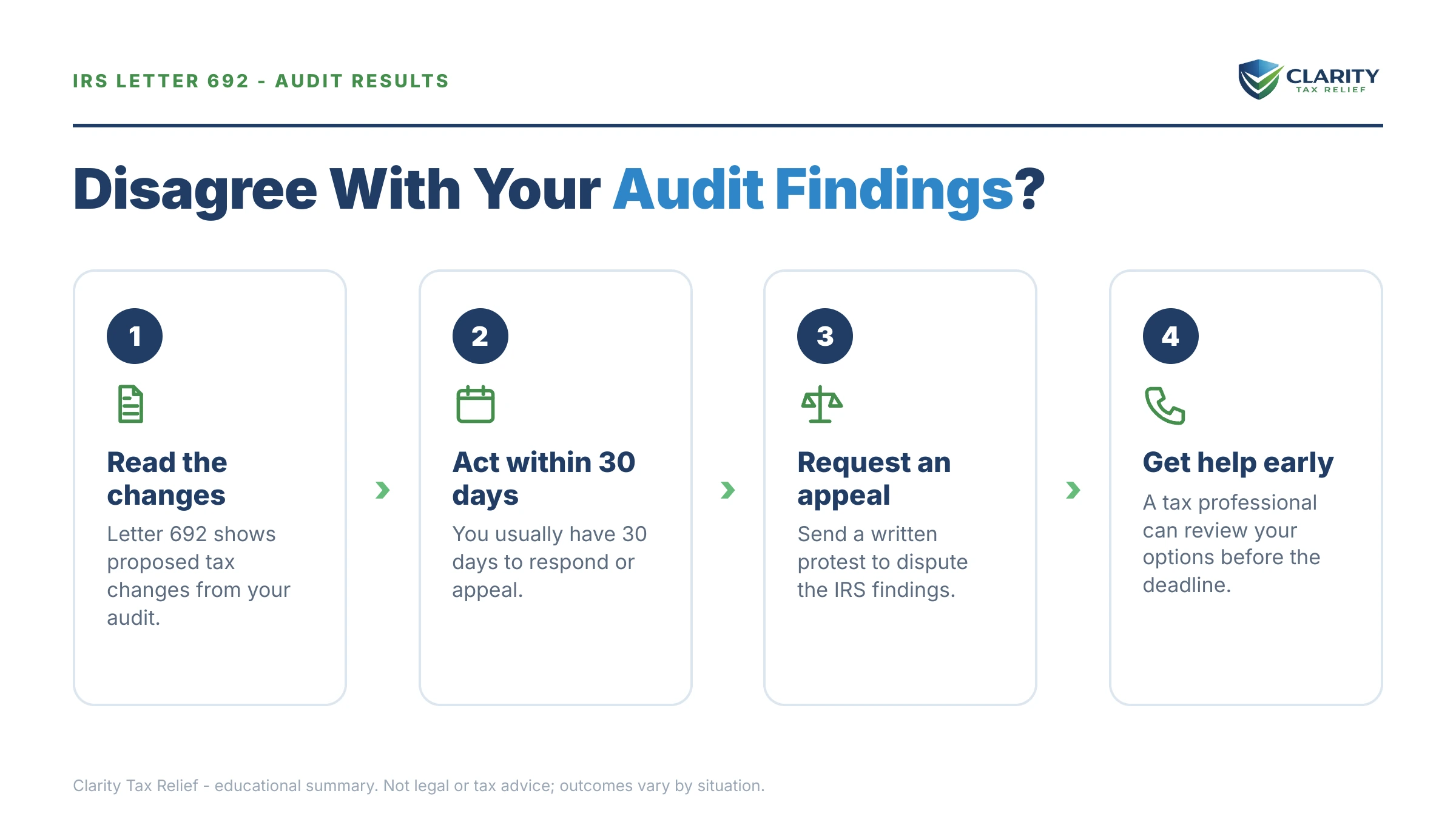

How to respond to Letter 692, step by step

- Find your response date. It's printed near the top of Letter 692 — that date, not a general rule, controls your window. Mark it today.

- Compare the revised Form 4549 to the original report. Go line by line and note exactly which items changed, which didn't, and whether the penalty was recalculated on the new numbers.

- Choose your path. Agree and sign, send additional documentation, request an Appeals conference, or deliberately wait for the Notice of Deficiency to preserve Tax Court.

- Send your response before the date on the letter. Use certified mail with return receipt (or fax, if the letter allows it) and keep copies of every page you send.

- Line up payment or representation. If you agreed, arrange payment or a payment plan once the bill arrives; if you're appealing, consider having an experienced tax professional draft the protest.

If you need more time, call the examiner at the number on the letter before the date passes and ask for a short extension — a documented request beats silence every time.

When you can handle Letter 692 yourself — and when help changes the outcome

You can usually handle Letter 692 on your own when the revised report is small and clearly correct. If the examiner accepted most of your evidence, the remaining balance is one you agree with, and you can pay it in full or through a simple plan within 180 days, signing the 4549 and paying at IRS.gov is a clean, cheap ending. Same if the only open item is a document you actually have — mail it with a one-page cover letter and let the examiner revise again.

Experienced help tends to change outcomes in four situations:

- The dispute is legal, not documentary — filing status, dependency tiebreakers, or who a divorce decree binds. Examiners apply rules; Appeals officers weigh how those rules would fare in court, and framing that argument well is a skill.

- The amount justifies it. On a five-figure adjustment, a partial concession at Appeals routinely outweighs the cost of representation. On a few hundred dollars, it rarely does — and an honest professional will say so.

- Penalties are a big slice. A 20% accuracy penalty argued separately, with a reasonable-cause position, is often the most winnable piece of the case.

- You're near or past the deadline. Once a Notice of Deficiency issues, the moves left — a Tax Court petition or, later, audit reconsideration — are more procedural and less forgiving of mistakes.

Terms on your Letter 692, decoded

- Form 4549 — the examination-changes report attached to your letter; signing it consents to immediate assessment of the revised amount.

- 30-day letter — the earlier letter (such as Letter 525) that sent the original audit report with 30 days to protest; the 692's window is typically half that.

- Notice of Deficiency — the statutory "90-day letter" the IRS must send before assessing audit changes you haven't agreed to; it starts your Tax Court clock.

- Independent Office of Appeals — a separate IRS division that reviews unagreed cases and can settle them based on litigation risk, not just the examiner's position.

- Agreed vs. unagreed case — signing the 4549 makes your case "agreed" (assessed immediately, no Tax Court); not signing keeps it "unagreed" and preserves those rights.

- Accuracy-related penalty — the 20% penalty commonly added to audit adjustments, which can be contested separately from the tax itself.

Letter 692 questions, answered

What is IRS Letter 692?

Letter 692, titled "Request for Consideration of Additional Findings," is the IRS examiner's reply after you responded to an audit report. It comes with a revised Form 4549 showing the auditor's updated numbers, and it gives you a short window — typically 15 days — to agree, send more documentation, or request an appeal before the case moves toward a Notice of Deficiency.

How many days do I have to respond to Letter 692?

Typically 15 days, and the exact response date is printed on your copy — that date controls. It is one of the shortest windows in the audit process, far shorter than the 30 days on the original examination report or the 90 days on a Notice of Deficiency. If you need more time, call the number on the letter and ask before the date passes; examiners can often grant a short extension.

What happens if I miss the Letter 692 deadline?

The examiner closes your case as unagreed and the IRS issues a statutory Notice of Deficiency, which starts a 90-day clock to petition the U.S. Tax Court. You don't lose the fight, but you lose the easiest venue: the free IRS Appeals conference. If the 90 days pass too, the tax is assessed, billing begins, and your remaining paths are usually audit reconsideration or paying and claiming a refund.

Is Letter 692 the same as a 30-day letter?

No. A 30-day letter (such as Letter 525 or Letter 915) transmits the original audit report and gives you 30 days to protest. Letter 692 comes later — after the examiner considered your response and revised the report — and it typically allows only 15 days. Both preserve your right to an Appeals conference; Letter 692 is simply your last, shortest chance to use it before a Notice of Deficiency.

Can I send new documents with my Letter 692 response?

Yes — the letter's title, "Request for Consideration of Additional Findings," is an invitation to do exactly that. If you have records the examiner hasn't seen — a custody order, school or medical records showing where your child lived, receipts — send copies (never originals) with a short cover letter before the response date. The examiner can revise the report again if the new evidence holds up.

Do I need Form 12203 or a formal written protest to appeal?

It depends on the amount. If the total proposed change is $25,000 or less for each tax period, you can use Form 12203, a simple one-page small-case request. If any period exceeds $25,000, you must file a formal written protest that states the facts, the law you rely on, and a penalties-of-perjury declaration. Either one must be sent before the date on your Letter 692.

Does signing the Form 4549 with Letter 692 mean I have to pay immediately?

No. Signing Form 4549 means you agree with the numbers and give up your right to a Notice of Deficiency and Tax Court — it does not require payment on the spot. The IRS will assess the tax and mail you a bill; at that point you can pay in full, set up a payment plan, or pursue penalty relief. Interest keeps accruing until the balance is paid.

Can I still go to Tax Court if I skip the Letter 692 appeal?

Yes. If you don't respond, the IRS must issue a Notice of Deficiency before it can assess the additional tax, and that notice gives you 90 days to petition the U.S. Tax Court without paying first. Many petitioned cases get routed back to Appeals for settlement anyway. The trade-off is months of added time, a court filing fee, and losing the chance to resolve the case informally now.

Your next 24 hours

- Find the response date printed near the top of your Letter 692 and count the days you have left — that number decides how fast everything else must move.

- Gather your paper trail: the original audit report, your response to it, the revised Form 4549 from this packet, and — if your case involves post-divorce filing status or a dependent — the divorce decree, custody order, and school or medical records.

- Get a free case review before the date passes: use the 2-minute form or call (888) 825-7779. An experienced tax professional can tell you within one conversation whether the revised findings are worth appealing or worth signing.

Primary sources: the IRS explains the audit appeal process at the IRS Independent Office of Appeals, payment options at IRS.gov/payments, and independent help through the Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.