IRS Penalties

Didn't Pay Estimated Taxes: The Penalty, the Math, and How to Fix It (2026)

The short answer: if you didn't pay estimated taxes, the penalty works like interest — the federal short-term rate plus 3 points, charged on each missed quarterly installment for as long as it stayed unpaid. It's usually hundreds, not thousands, of dollars. First-time abatement can't remove it, but Form 2210 has real exceptions.

Maybe this is your first year filing on your own after a divorce, and your ex's paycheck withholding used to quietly cover the whole bill. You filed, your software added an "estimated tax penalty" line you'd never seen before, and now there's a number on top of a balance you weren't expecting. This one is fixable — and it's cheaper to fix than the letter makes it feel.

Three facts most pages bury: this penalty is not a flat fine — it's a per-quarter interest charge under IRC §6654; it's the one common penalty that first-time abatement cannot touch; and a late-year withholding increase can erase it retroactively in a way a lump-sum payment never can. The image below shows exactly what the paperwork behind this penalty looks like and where the number the IRS is charging you actually appears.

⏱ Your real clock: this penalty has no response deadline — it accrues daily on each unpaid installment until the underlying tax is paid. The next date that matters is your next quarterly deadline (September 15, 2026 for tax-year 2026 payments), which decides whether you repeat this penalty next spring.

Why you're being charged the estimated tax penalty

The IRS charges the estimated-tax penalty when you didn't pay enough tax during the year — through withholding or quarterly payments — even if you paid everything at filing. The U.S. tax system is pay-as-you-go: the law expects tax to arrive in four installments as you earn, not once in April. Miss the installments and §6654 charges you for the delay, quarter by quarter.

Divorce is one of the most common triggers, and it works in three ways at once. First, the withholding that covered you disappears — if your ex-spouse's W-2 job carried the joint bill, your own withholding may cover only a fraction of your new solo liability. Second, your filing status changed, so last year's joint return no longer tells you what "enough" looks like. Third, the prior-year safe harbor gets tricky: after a joint year, you can only count your allocated share of the joint tax — figured under Publication 505 rules based on each spouse's separate liability, not simply half. Filers who assume half routinely come up short.

The same penalty hits first-year freelancers, retirees taking IRA distributions with no withholding, and anyone with a one-time income spike — a home sale, a 401(k) withdrawal, an asset split in the divorce itself. If quarterlies are new to you, how quarterly estimated taxes work covers the system from the top; this page covers what happens after you've already missed them.

How the penalty for not paying estimated taxes is calculated

The estimated-tax penalty equals the IRS underpayment interest rate — the federal short-term rate plus 3 percentage points — applied separately to each missed quarterly installment for the exact number of days it went unpaid. The rate resets every quarter; it has run in the 7–8% annual range in recent years. Our estimated tax penalty rate 2026 page tracks the current figure.

Mechanically, the IRS (or Form 2210) splits your required annual payment into four installments, checks what you actually paid by each due date, and charges the rate on each shortfall from its due date until you pay it or until April 15 of the following year, whichever comes first. That per-installment structure is why paying in full at filing stops the penalty but doesn't erase it — the Q1 installment was still eleven-plus months late.

Two quirks work in your favor:

- Withholding counts as paid evenly all year. Extra withholding in November is treated as if a quarter of it arrived by each installment date — retroactively covering quarters you missed. An estimated payment in November only counts from November. If you returned to W-2 work mid-year after a divorce, cranking up withholding is the single most powerful fix.

- The annualized income method (Schedule AI). The default calculation assumes your income arrived evenly across the year. If most of it landed late — a Q4 consulting contract, a December asset sale — Schedule AI recalculates each installment based on when you actually earned the money, often shrinking the penalty substantially.

You never owe this penalty at all if your balance due after withholding is under $1,000, or if you hit a safe harbor (the table further down shows the thresholds). If you're doing the math on your own numbers, our IRS penalty and interest calculator can estimate what you're facing. For the calculation mechanics in even more depth, see our companion guide to the underpayment penalty estimated taxes rules.

Worked example: $7,400 owed after a divorce year

Say you divorced in early 2025, filed single for the first time in April 2026, and owed $7,400 — none of it prepaid, because your old joint withholding was gone and quarterlies never crossed your mind. Your four required installments were $1,850 each, due April 15, June 15, and September 15, 2025, and January 15, 2026.

Using an illustrative 7% annual rate, each missed installment accrues from its due date to April 15, 2026:

- Q1 ($1,850, ~12 months late): roughly $130

- Q2 ($1,850, ~10 months late): roughly $108

- Q3 ($1,850, ~7 months late): roughly $76

- Q4 ($1,850, ~3 months late): roughly $32

Total estimated-tax penalty: about $346 — real money, but under 5% of the balance. Here's the part that matters more: if you can't pay the $7,400 itself, the failure-to-pay penalty (0.5% per month, about $37) plus interest (roughly $43 a month at 7%) starts stacking on top — around $80 a month on a balance that isn't shrinking. The estimated-tax penalty is the smallest problem on the notice; the unpaid balance behind it is the one that grows. Our hub on how much IRS penalties on back taxes really cost shows how these charges compound across every penalty type.

What happens if you ignore the penalty and the balance

The estimated-tax penalty itself never escalates — but the unpaid balance it rides on feeds straight into the IRS's automated collection sequence. Here is the order things happen if nothing gets paid:

- Assessment. The penalty posts when your return processes — either the figure you computed on Form 2210, or the IRS's own calculation, billed on a CP30 notice.

- Stacking charges. On any unpaid tax, the failure-to-pay penalty (0.5% per month) and daily-compounding interest begin immediately and run until paid.

- CP14 notice. The first formal bill, typically giving about 21 days before the sequence moves on.

- CP501 and CP503. Reminder bills — no enforcement yet, but the balance is larger with each one.

- CP504. Intent to levy your state tax refund under IRC §6331(d), and lien territory begins.

- LT11 / Letter 1058. The final notice: a 30-day clock, Collection Due Process rights, and after that, wage and bank levies become legally available.

In 2026, with IRS staffing down roughly 27%, it's harder than ever to reach a human — but this sequence is fully automated and never paused. The machine escalates on schedule whether or not anyone at the IRS reads your file.

Facing an estimated-tax penalty on a balance you can't pay?

Interest and the failure-to-pay penalty are accruing on that balance every month it sits. An experienced tax professional will review your return, your penalty math, and your waiver options free — and map the cheapest way out before the collection notices start.

Your options when you can't pay the balance in full

The IRS has several programs for a balance like this, and at $7,400 nearly all of them are open to you. What each one costs and how fast it works:

| Option | Cost | Timeline & what it does |

|---|---|---|

| Pay in full | $0 fees; stops all further charges | Immediate — penalty, interest, and the notice sequence all stop the day the balance hits zero |

| Short-term payment plan | $0 setup; interest + 0.5%/mo continue | Up to 180 days to pay in full; set up online in minutes; enforcement stays off |

| Installment agreement | Setup fee varies (lower with direct debit); interest + reduced FTP continue | Up to 72 months online for balances ≤ $50,000; a $7,400 balance qualifies for a guaranteed agreement |

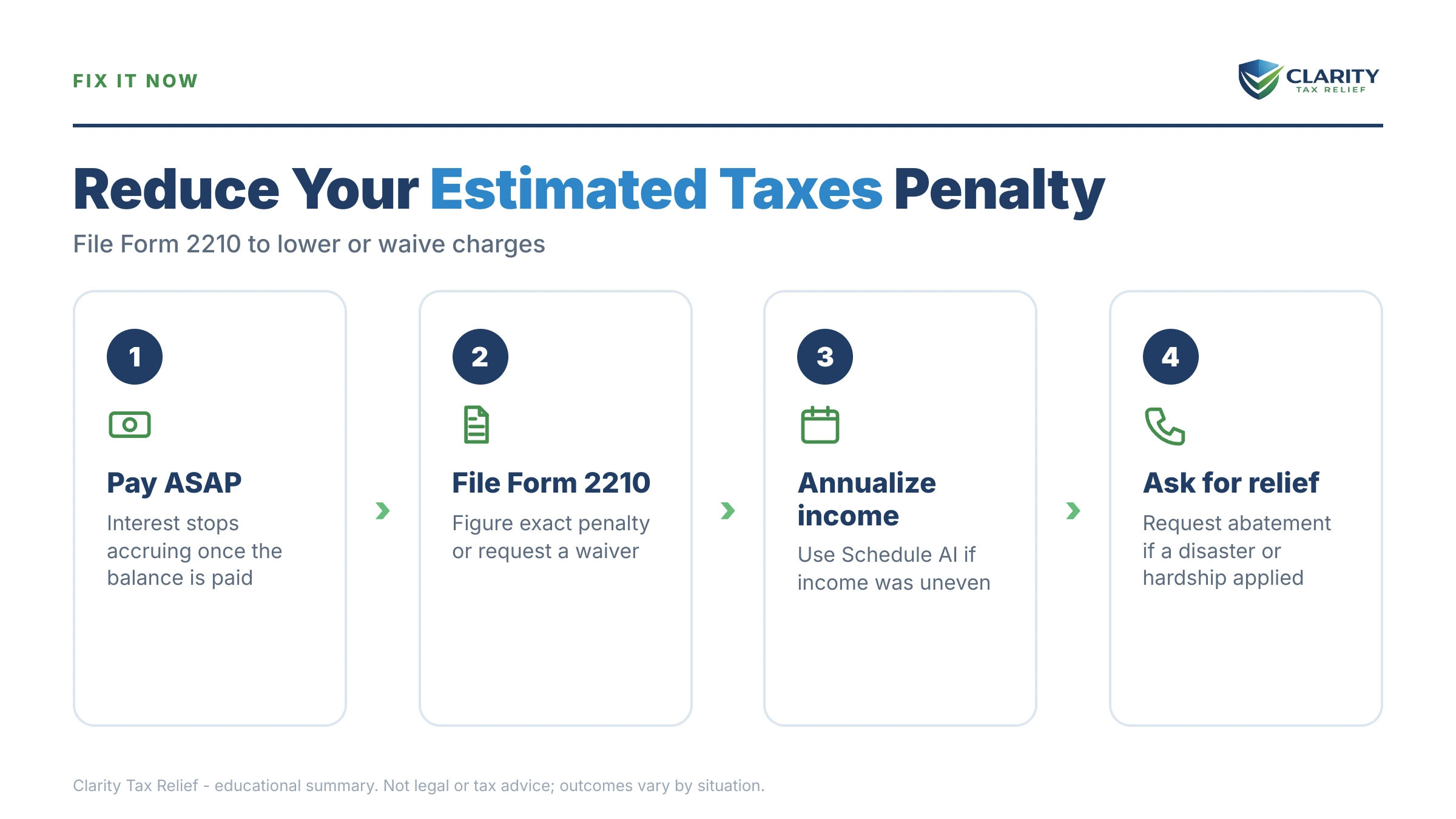

| Form 2210 waiver / recalculation | $0 — filed with or after your return | Weeks to months; removes or shrinks the penalty itself (not the tax) if grounds apply |

| Currently Not Collectible | $0 setup; charges keep accruing | Pauses collection if paying would cause genuine hardship; requires financial disclosure; balance remains |

At $7,400 you sit below the $10,000 line for a guaranteed installment agreement — if you've filed and paid on time for the past five years and can pay within three years, the IRS must accept your plan. Even $210 a month retires the balance in about three years, and the notice sequence never starts. An Offer in Compromise almost never makes sense at this balance level: the application costs $205 and the IRS accepted roughly 1 in 5 offers in FY2024 — a payment plan is faster and cheaper here.

One more angle if you're divorced and the balance comes from a joint year: your divorce decree may say your ex pays it, but the IRS isn't bound by the decree. Divorce and who pays IRS debt covers when that matters and what relief exists.

How to respond, step by step

- Find the exact penalty number. Check the estimated-tax penalty line near the signature section of your Form 1040, or the CP30 notice if the IRS calculated it for you. Verify it against your IRS online account.

- Pay whatever you can toward the underlying tax now. The penalty and interest run only on unpaid amounts, so every dollar you pay today stops charges on that dollar immediately.

- Check whether a Form 2210 exception or waiver applies. Run the under-$1,000 rule, both safe harbors (with divorce-year allocation if last year's return was joint), the annualized income method if your income arrived late in the year, and the Part II waiver grounds.

- Set up a payment arrangement for any balance you can't pay. A short-term plan (up to 180 days, $0 setup) or an installment agreement stops the collection-notice sequence; at $7,400 you're under the $10,000 guaranteed installment agreement threshold.

- Fix the current year before the next quarterly deadline. Make your next Form 1040-ES payment or raise your W-2 withholding so you land in a safe harbor and never see this penalty again.

Can the estimated tax penalty be waived?

First-time penalty abatement does not apply to the estimated-tax penalty — relief runs exclusively through the Form 2210 exceptions and waivers. This surprises people, because FTA wipes out failure-to-file and failure-to-pay penalties routinely. The §6654 penalty is carved out, and the Automatic Exemption from Penalty (AEP) that begins replacing FTA in summer 2026 follows the same boundaries.

What does work, on Form 2210 Part II:

- Casualty, disaster, or unusual circumstances — where charging the penalty would be inequitable. A divorce that destroyed your withholding setup isn't automatic, but it's a legitimate unusual-circumstances argument, decided case by case.

- Retired after 62 or became disabled — during the tax year or the one before, with reasonable cause for the underpayment.

- Federally declared disaster areas — the IRS often waives or adjusts the penalty automatically when deadlines are postponed.

And before requesting any waiver, recalculate: Schedule AI (for back-loaded income) and the actual-dates withholding election shrink many penalties without needing anyone's permission. Our full guide to the estimated tax penalty waiver walks through Form 2210 Part II line by line. If you're confusing this penalty with the ones FTA does cover, failure to file penalty vs failure to pay sorts out which penalty is which.

How to avoid the underpayment penalty next year (safe harbors)

You owe no estimated-tax penalty — no matter how much you owe in April — if your withholding and quarterly payments hit a safe harbor. These are the thresholds:

| Your situation | What you must pay in during the year |

|---|---|

| Everyone | 90% of this year's total tax, or |

| Prior-year AGI ≤ $150,000 ($75,000 married filing separately) | 100% of last year's total tax |

| Prior-year AGI > $150,000 ($75,000 MFS) | 110% of last year's total tax |

| Balance due under $1,000 after withholding | No penalty applies at all |

| Zero tax liability last year (full 12-month year, U.S. citizen/resident) | No penalty applies at all |

The prior-year safe harbor is the practical one: it's a fixed number you can compute in January, regardless of how this year goes. The divorce catch, once more — after a joint year, "last year's tax" means your allocated share under Publication 505, not the full joint amount and not automatically half. Payments for tax-year 2026 are due April 15, June 15, and September 15, 2026, and January 15, 2027; the full calendar with weekend adjustments is in quarterly estimated tax deadlines 2026.

One more caution for Californians: the FTB runs its own underpayment penalty with different thresholds and its own installment rules — never assume the IRS numbers carry over. See the FTB estimated tax penalty guide for the state side.

When you can handle this yourself

Most people can resolve an estimated-tax penalty without professional help. If the penalty is a few hundred dollars, the math looks right, and you can pay the balance within 180 days, just pay it — or set up a plan online — and fix your withholding for the current year. Requesting a disaster-area waiver or filing a straightforward Form 2210 is also well within DIY range.

Experienced help changes the outcome in a narrower set of situations: the balance spans multiple years or sits on top of unfiled returns; your income is lumpy enough that a Schedule AI recalculation could cut the penalty meaningfully but the computation is beyond your software; you're allocating a joint prior-year liability after divorce and the numbers are disputed; or the underlying balance is large enough that the collection sequence — not the penalty — is the real threat. In those cases, the order you fix things in (returns first, then penalty math, then the balance) changes what you ultimately pay, and a free review costs nothing to find out where you stand — start with the 2-minute form.

Terms on your notice, decoded

- Safe harbor — a payment threshold (90% of this year or 100–110% of last year) that eliminates the penalty entirely, no matter what you owe in April.

- Form 2210 — the form that calculates the underpayment penalty, applies the annualized income method, and requests waivers.

- Underpayment installment — one of the four quarterly amounts you were required to pay; the penalty is computed on each one separately.

- Annualized income method (Schedule AI) — an optional recalculation that matches installments to when you actually earned the income, cutting the penalty for back-loaded years.

- CP30 — the notice the IRS sends when it calculates the estimated-tax penalty for you and reduces your refund or bills you.

- Failure-to-pay penalty — a separate 0.5%-per-month charge on unpaid tax after the filing deadline; this one is eligible for first-time abatement.

Didn't-pay-quarterlies questions, answered

How much is the penalty for not paying estimated taxes?

It's computed like interest, not a flat fine: the IRS underpayment rate (the federal short-term rate plus 3 percentage points) applied to each missed quarterly installment for the time it went unpaid. On a typical $5,000–$10,000 shortfall, that works out to a few hundred dollars, not thousands. The exact rate resets every quarter, so the same missed payment costs slightly more or less depending on the year.

Will the IRS calculate the penalty for me, or do I have to file Form 2210?

Yes — if you file without Form 2210, the IRS figures the penalty itself and bills you, usually on a CP30 notice. You only need to file Form 2210 if you're requesting a waiver, using the annualized income method, or treating withholding as paid on the dates it actually was. If the IRS's figure looks high, recompute it: the default method assumes your income arrived evenly all year, which overstates the penalty for anyone whose income landed late in the year.

Does first-time penalty abatement apply to the estimated tax penalty?

No. First-Time Abate covers failure-to-file, failure-to-pay, and failure-to-deposit penalties — the Section 6654 estimated-tax penalty is excluded, and the Automatic Exemption from Penalty (AEP) replacing FTA starting in summer 2026 follows the same lines. The only relief paths are the Form 2210 exceptions and waivers: the under-$1,000 rule, the safe harbors, casualty or unusual circumstances, and the retired-or-disabled waiver.

Do I still owe the penalty if I pay my full tax bill by April 15?

Usually yes, if you missed the quarterly installments. The penalty is charged installment by installment, so paying in full at filing stops it from growing but doesn't erase the charge for the months each quarterly payment ran late. One exception: withholding is treated as paid evenly through the year, so a late-year withholding increase can retroactively cover earlier quarters in a way an April payment cannot.

What is the safe harbor after a divorce?

You can still use the prior-year safe harbor, but if last year's return was joint, you don't get to count the whole joint tax — your share is allocated under the rules in IRS Publication 505, based on what each spouse's separate tax would have been. Many newly divorced filers underpay because they assume it's simply half. If AGI on that joint return was over $150,000, the 110%-of-prior-year version of the safe harbor applies.

Can the estimated tax penalty be waived?

Yes, in limited situations, using Form 2210 Part II. The IRS can waive it for a casualty, disaster, or other unusual circumstance that makes the penalty inequitable, and for taxpayers who retired after age 62 or became disabled during the year and had reasonable cause. A divorce that upended your withholding isn't an automatic waiver, but it can support an unusual-circumstances request — the IRS decides case by case.

Do I owe a penalty if I owe less than $1,000?

No. If your total balance due after withholding and refundable credits is under $1,000, the estimated-tax penalty doesn't apply at all — no Form 2210 needed. You also owe no penalty if you had zero tax liability in the prior year, were a U.S. citizen or resident, and that prior year covered a full 12 months — even if you owe a large amount this year.

Your next 24 hours

- Find your penalty number. Pull your filed return and locate the estimated-tax penalty line near the signature section — or the CP30 notice if the IRS billed you — so you know exactly what's penalty versus tax versus interest.

- Gather three documents: last year's return (the joint one, if you divorced), this year's income records, and any IRS notice you've received. That's everything needed to check the safe harbors, Schedule AI, and the waiver grounds.

- Get a free case review. Interest and the failure-to-pay penalty accrue on the unpaid balance every month it sits — call (888) 825-7779 or use the 2-minute form, and an experienced tax professional will map the cheapest path through the penalty, the balance, and next year's quarterlies.

Primary sources: the IRS's About Form 2210 page covers the penalty calculation and waiver request; Estimated Taxes at IRS.gov explains who must pay quarterly and how; and IRS.gov/payments is where balances and 1040-ES payments are actually paid.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.