IRS Penalties

Missed RMD Penalty Waiver: How to Get the 25% Excise Tax Reduced or Removed (2026)

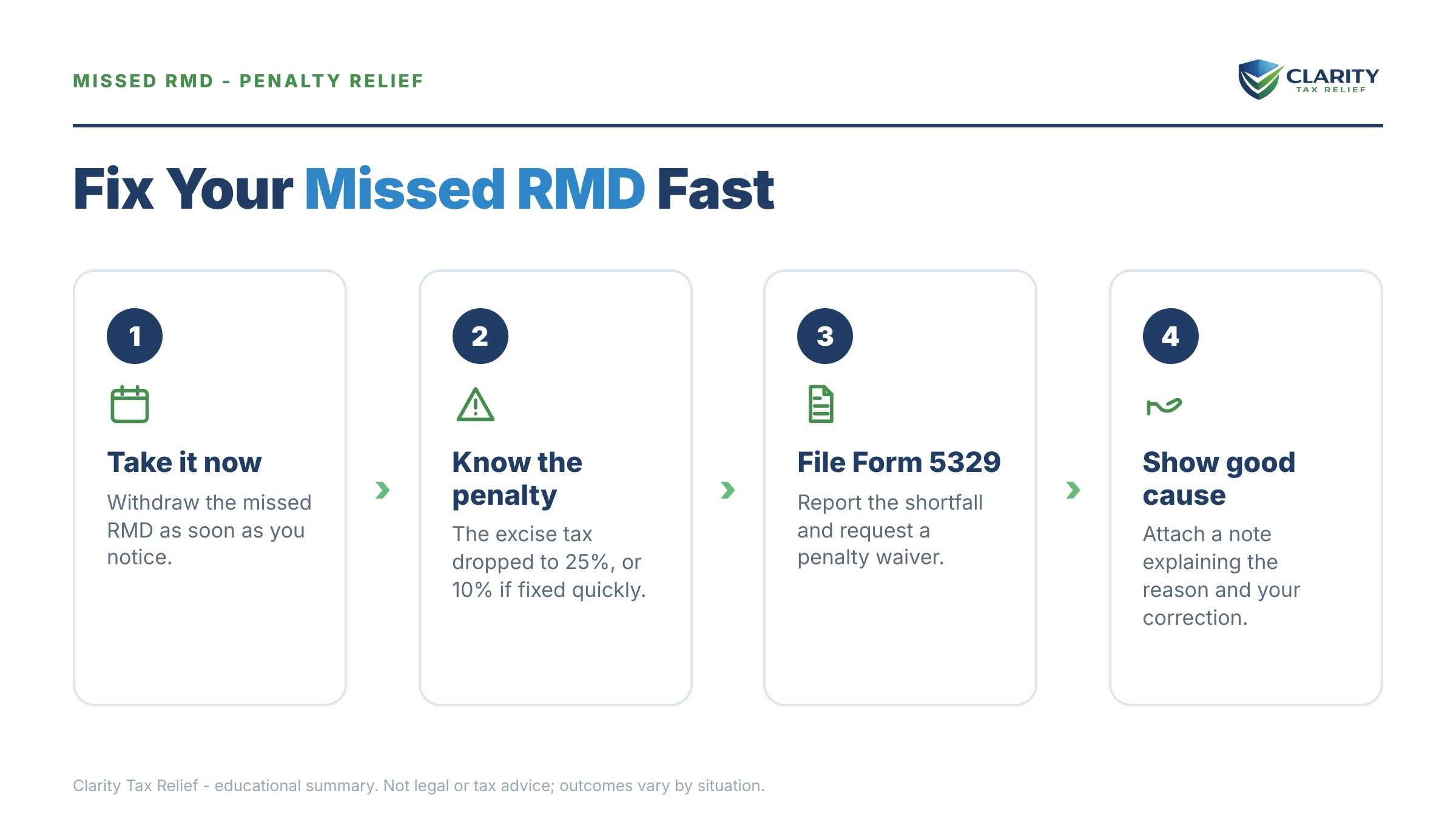

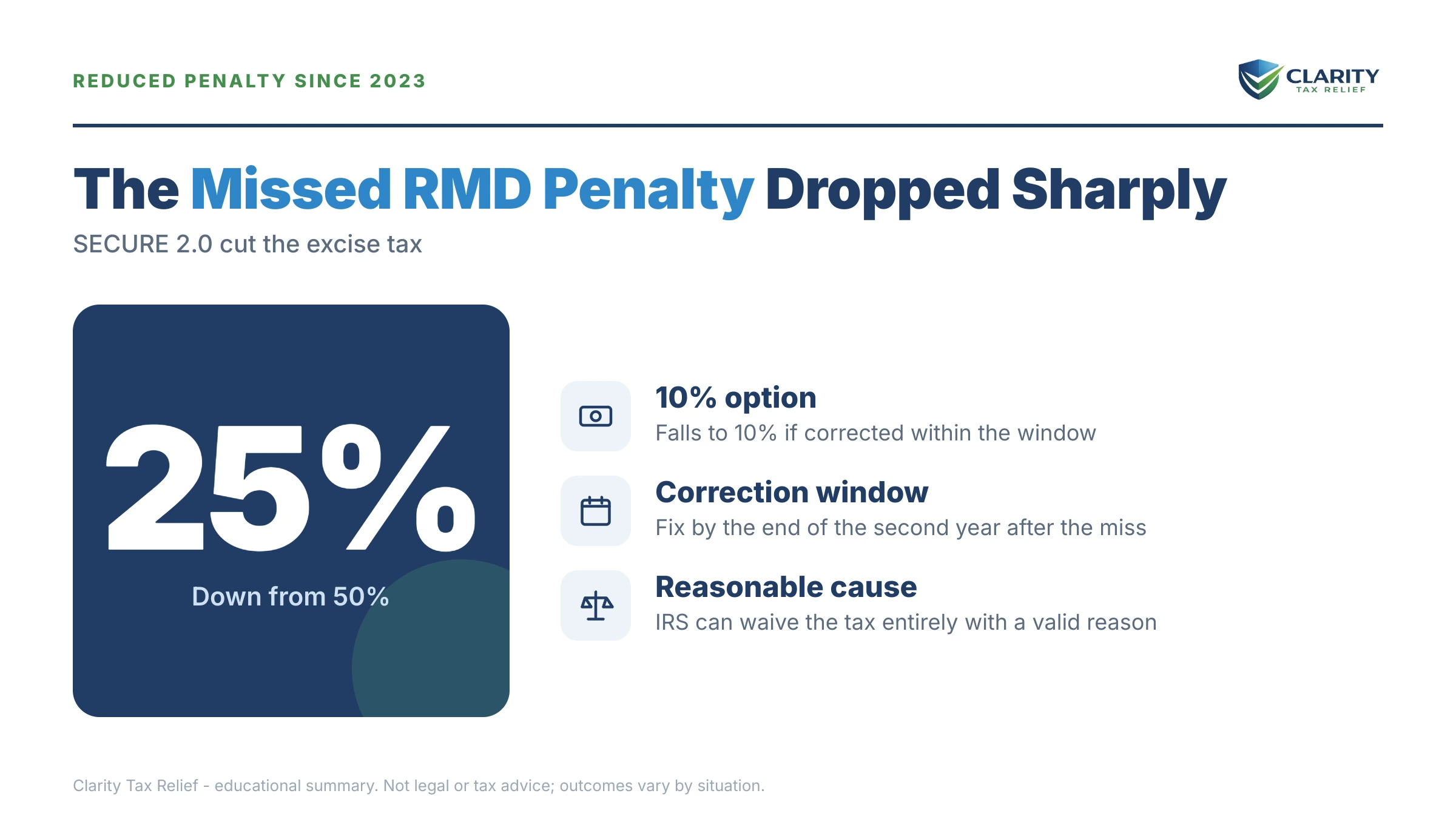

The short answer: the IRS can fully waive the missed RMD penalty for reasonable cause. Withdraw the missed amount immediately, then file Form 5329 (Part IX) with a brief explanation and the "RC" notation — and don't pay the excise tax up front. The penalty is 25% of the shortfall, or 10% if you correct it within the correction window.

Maybe you were pulling account statements together for the refinance application when it hit you: no distribution ever came out of your IRA last year. The withdrawal you meant to schedule never happened, and now you're staring at a potential four-figure excise tax on top of the mortgage paperwork. Take a breath — this is one of the most forgiving penalties in the tax code, and there is a specific, well-worn path to getting it reduced or removed entirely.

The whole missed RMD penalty waiver lives on one form — Form 5329 — and most people who search for it never find where the request actually goes. The image below shows exactly what the form looks like and where to look, so you can see the waiver mechanics before you touch a pen.

⏱ Your real clock: the 25% excise tax drops to 10% only if you fix the shortfall within the IRS correction window — generally by the end of the second tax year after the year you missed the RMD, or earlier if the IRS assesses the tax first. A reasonable-cause waiver can still take it to $0, but withdrawing the money promptly is a condition of that waiver too. Every route gets cheaper the sooner you correct it.

Why you're facing the missed RMD penalty

The missed RMD penalty is an excise tax under Internal Revenue Code §4974 — 25% of the amount you were required to withdraw but didn't, cut down from 50% by the SECURE 2.0 Act for RMDs due in 2023 and later. It isn't a late-filing or late-payment penalty on your return; it's a separate tax on the shortfall itself, which is exactly why the usual abatement tools don't apply and why it has its own waiver process.

Most misses happen for boring, fixable reasons. The RMD age moved from 72 to 73, so people who expected a custodian reminder at 72 heard nothing. A rollover to a new custodian silently wiped out an automatic-distribution setting. A first-timer used the April 1 grace period for the initial RMD and then lost track. Or a beneficiary didn't know an inherited account restarted annual RMDs in 2025.

Account-type confusion is the other big driver. Here's the 2026 map:

| Account type | Lifetime RMDs required? | The trap that causes misses |

|---|---|---|

| Traditional IRA, SEP, SIMPLE | Yes, starting at age 73 | RMDs apply even if you're still working; each IRA's RMD can be aggregated and taken from one IRA — but many people miscalculate the total |

| 401(k), 403(b), 457(b) | Yes at 73, with a still-working exception | The still-working delay applies only to your current employer's plan (and not to 5% owners) — old employers' plans still require RMDs |

| Roth IRA | No — none during the owner's lifetime | Beneficiaries who inherit a Roth IRA do have distribution requirements |

| Roth 401(k) / designated Roth accounts | No, beginning in 2024 | People who took Roth 401(k) RMDs for years assume they still must — or assume their pre-tax 401(k) is also exempt (it isn't) |

| Inherited IRA (most non-spouse, post-2019 death) | Annual RMDs from 2025 if the original owner had started RMDs, plus full payout within 10 years | The IRS excused misses for 2021–2024 while rules were finalized; a 2025+ miss is a real shortfall |

Whatever the cause, the IRS learns about the miss the same way you did — on paper. Your custodian reports the account's year-end value and RMD status on Form 5498, and the absence of a matching Form 1099-R distribution is what eventually flags the account.

How the missed RMD penalty waiver works

The IRS waives the §4974 excise tax entirely when the shortfall was due to reasonable error and you're taking reasonable steps to remedy it — and the request goes on Form 5329, Part IX, not in a phone call or a standalone letter. Those are the two conditions straight from the form's instructions, and they explain the order of operations: fix first, then ask.

Mechanically, you report the amount you were required to take and the amount you actually took. On the shortfall line (line 54 on recent versions of the form), you write "RC" and the amount you want waived in parentheses on the dotted line, subtract it, and compute the excise tax only on whatever remains — which, if you're requesting a full waiver, is zero. Attach a short statement explaining what happened and confirming you've withdrawn the money. You do not send payment for the waived amount. If the IRS disagrees, it will bill you; if it agrees, you'll typically hear nothing and owe nothing.

What counts as reasonable cause here is more forgiving than for most penalties: serious illness, a death in the family, custodian or advisor error, bad professional advice, a broken auto-distribution after a rollover, or honest confusion over the changing RMD age. The general standard is the same one covered in our guide to reasonable cause examples — events outside your control, or an honest error, plus prompt correction. For this particular penalty, the prompt correction is doing most of the work.

One thing the waiver does not touch: income tax. The late distribution is ordinary income in the year you actually take it. Catch up a 2025 miss in 2026 and you'll have two RMDs landing on your 2026 return — worth checking your withholding before the catch-up withdrawal, especially if bracket creep or Medicare premium tiers are in play.

What this looks like in dollars

Say your 2025 IRA RMD was $19,200 and you discover in July 2026 that you never took it — right as you're assembling refinance paperwork. Here's the math on your three possible outcomes:

- Do nothing: 25% × $19,200 = $4,800 in excise tax, before any additions the IRS tacks on once it assesses.

- Correct within the window, no waiver: 10% × $19,200 = $1,920 — you withdraw the $19,200 now and pay the reduced rate with Form 5329.

- Correct now and request the waiver: withdraw the $19,200, file Form 5329 with the "RC" notation and a one-page explanation, and pay $0 excise tax unless the IRS denies the request.

This is a hypothetical, and no outcome is guaranteed — but the spread between acting this week and letting it sit is the difference between $0 and $4,800-plus. For a homeowner heading into underwriting, it's also the difference between a clean IRS account and an open assessed balance a lender may ask about.

What happens if you ignore a missed RMD

A missed RMD doesn't stay a private mistake — custodian reporting eventually surfaces it, and each stage of delay closes off a cheaper outcome. The sequence runs like this:

- The correction window is open. You can still reach the two best outcomes: the 10% reduced rate, or a full reasonable-cause waiver. This is where you are now.

- The window closes. Generally at the end of the second tax year after the miss (earlier if the IRS assesses first), the 10% rate disappears. The waiver is still technically available, but the longer the shortfall sits uncorrected, the harder it is to show you took "reasonable steps to remedy" it.

- The IRS matches the data. Form 5498 shows an account subject to RMDs; no Form 1099-R shows a distribution. The mismatch can trigger a notice or exam, and the IRS assesses the excise tax itself — on its numbers, not yours. Because Form 5329 is treated as its own return, failure-to-file and failure-to-pay additions can stack on top of the excise tax at this stage.

- The assessed balance enters collection. An unpaid assessment follows the normal path: bills, then lien and levy authority. A filed federal tax lien shows up in refinance title work — see what refinancing with an IRS lien actually involves before letting it get that far. You can estimate how the additions grow on an assessed balance with our IRS Penalty & Interest Calculator.

One 2026 change works in your favor: SECURE 2.0 created a three-year statute of limitations on this excise tax that generally starts when you file your income tax return for the year — before, the clock never started at all unless you filed Form 5329. That caps very old exposure for filers, but it does nothing for a recent miss the IRS can still assess.

Just discovered a missed RMD?

Get it reviewed free before the correction window closes and the 10% rate becomes 25%. An experienced tax professional will check your shortfall math, draft the reasonable-cause request, and make sure nothing on your IRS account surprises your lender — (888) 825-7779 or the 2-minute form.

Your options to reduce or waive the RMD penalty, compared

Every path starts the same way — withdraw the missed amount — and diverges from there. Unlike the penalties covered in our guide to how much IRS penalties on back taxes grow, this one has a built-in route to zero:

| Path | Excise tax you pay | What it requires | Timing |

|---|---|---|---|

| Full reasonable-cause waiver | $0 (if granted) | Withdraw the $19,200, file Form 5329 Part IX with the "RC" notation and a written explanation; don't prepay | File now; the IRS bills you only if it denies the request — often you simply never hear back |

| Reduced 10% rate | $1,920 | Correct the shortfall within the correction window and file Form 5329 reporting it | Window generally ends the second tax year after the miss — or when the IRS assesses, whichever comes first |

| Default 25% rate | $4,800 | Nothing — this is what filing without a waiver request (or being assessed) costs for 2023-and-later misses | Due with Form 5329; interest and additions accrue on unpaid balances after assessment |

| Pre-2023 missed years (old 50% rate) | $9,600 | Older misses still carry the 50% rate — the waiver request works the same way and matters twice as much | File that year's version of Form 5329 for each missed year, as soon as corrected |

Two things this table can't show. First, an approved waiver isn't a payment plan or a settlement — the excise tax simply never becomes due, so there's no balance to finance and nothing to disclose. Second, if you already paid the excise tax and only later learned a waiver was possible, that money may be recoverable: see penalty abatement after paying for how refund claims (including Form 843 where it applies) work.

How to respond, step by step

- Withdraw the shortfall now. Take the full missed amount out of the account before you file anything — correcting the miss is a condition of the waiver, and it starts your best-case math.

- Get the right-year Form 5329. Use the version of the form for the year you missed, one form per missed year — the current-year form doesn't work for a prior-year shortfall.

- Complete Part IX with the "RC" notation. Report the required amount and what you actually took, then write "RC" and the amount you want waived in parentheses on the dotted line next to the shortfall line (line 54 on recent forms), and compute tax only on any portion you are not asking to be waived.

- Attach a short reasonable-cause statement. One page: what happened, why it was outside your control or an honest error, and the date you withdrew the money to fix it.

- File and wait — without prepaying. Attach the form to your current return or mail it standalone with your statement; the IRS bills you only if it denies the waiver.

The current form and instructions are on the IRS's About Form 5329 page, and prior-year versions are linked from the same place.

When you can handle this yourself — and when help changes the outcome

A single missed year with a clear story is one of the most DIY-friendly problems in tax resolution. If you missed one RMD, withdrew it as soon as you noticed, and can write two honest sentences about why it happened, filing Form 5329 with an "RC" request yourself is a reasonable plan — the form is one page and there's no fee to ask.

Experienced help earns its cost when the facts get layered: multiple missed years (each needs its own prior-year form, and pre-2023 years carry the 50% rate), an inherited account where the 10-year rule and annual-RMD requirements interact, a shortfall the IRS has already assessed (you're now contesting a balance, not requesting a waiver), or an existing IRS debt where this excise tax would stack onto a balance already threatening a lien. It also matters when timing is financial: if you're retired and owe back taxes already, or heading into mortgage underwriting, the order you resolve things in determines what a lender sees. A wrong guess on the reasonable-cause statement doesn't get a second first impression.

If your IRS account has other loose ends beyond the RMD, a free case review can map all of it at once before you file anything — start with the 2-minute form.

Terms on Form 5329, decoded

- RMD (required minimum distribution): the minimum amount the tax law forces out of most pre-tax retirement accounts each year once you reach RMD age, computed from the prior year-end balance and an IRS life-expectancy table.

- Excise tax (§4974): the penalty on an RMD shortfall — a separate tax of 25% (or 10% if corrected in time) on the amount you failed to withdraw, not a percentage of your income tax.

- Correction window: the period — generally through the end of the second tax year after the miss, or until the IRS assesses — during which fixing the shortfall cuts the rate from 25% to 10%.

- Reasonable cause ("RC"): the standard for a full waiver — the miss resulted from reasonable error and you're taking reasonable steps to fix it; "RC" is the literal notation you write on the form.

- Required beginning date (RBD): April 1 of the year after you reach RMD age — the one-time grace period for your first RMD that also causes two distributions to land in a single year.

- Form 5498: the custodian's annual report of your account value and RMD status — the document that tells the IRS an RMD was due, whether or not you took it.

Missed RMD penalty waiver FAQs

How do I get a missed RMD penalty waived?

Withdraw the missed amount first, then file Form 5329 for the year you missed, complete Part IX, write "RC" and the amount you want waived next to the excise-tax line, and attach a short statement explaining what happened. The IRS grants the waiver when the shortfall was due to reasonable error and you have taken steps to fix it — a documented, corrected, one-time miss is the strongest fact pattern.

Do I have to pay the RMD penalty before requesting the waiver?

No. The Form 5329 instructions tell you not to pay the excise tax on the amount you are asking to be waived. You subtract the waiver-requested amount before computing the tax, file the form with your explanation, and the IRS bills you only if it denies the request. Prepaying means chasing a refund later instead of simply not owing.

What counts as reasonable cause for a missed RMD?

Serious illness, a death in the family, a custodian or advisor error, incorrect professional advice, a rollover that broke an automatic-distribution setting, or genuine confusion after the RMD age changed are all fact patterns the IRS has accepted. The key is showing the miss was outside your control or an honest error — and that you corrected it as soon as you discovered it. "I forgot" alone is weaker, but a prompt fix plus a clean history still helps.

Is the missed RMD penalty 50% or 25%?

It depends on the year you missed. For RMDs due in 2023 or later, the SECURE 2.0 Act cut the excise tax from 50% to 25% — and to 10% if you correct the shortfall within the correction window. Missed RMDs from 2022 and earlier are still subject to the old 50% rate, which makes the reasonable-cause waiver even more valuable for older years.

What if I missed RMDs for several years in a row?

You file a separate Form 5329 for each missed year, using that year's version of the form, and you can attach one statement covering all of them. Withdraw the entire cumulative shortfall before filing. Note that years before 2023 carry the old 50% rate, so the waiver matters most on those — and multi-year misses are exactly where a professional review of the sequencing pays for itself.

Does first-time penalty abatement cover a missed RMD penalty?

No. First-time abatement applies to failure-to-file, failure-to-pay, and failure-to-deposit penalties — not to the Section 4974 excise tax on a missed RMD. The new Automatic Exemption from Penalty (AEP) arriving in summer 2026 covers the same return penalties, not this excise tax. The only path to $0 on a missed RMD is the reasonable-cause waiver requested on Form 5329 Part IX.

What about missed RMDs on an inherited IRA?

The IRS excused the penalty for certain missed inherited-IRA RMDs during 2021 through 2024 while the 10-year-rule regulations were being finalized. Starting in 2025, most non-spouse beneficiaries who inherited from someone already taking RMDs must take annual distributions again — so a 2025 or 2026 miss is a real shortfall that needs the Form 5329 waiver process, not the automatic relief of prior years. If the distribution itself created a tax bill you can't pay, see our guide to inherited IRA taxes owed.

Do I still owe income tax on the late RMD?

Yes. The waiver removes the excise tax, not the ordinary income tax — the late distribution is taxed in the year you actually take it. If you're catching up a prior-year miss and also taking this year's RMD, two distributions land in one tax year, which can bump your bracket, Medicare premiums, or the taxable share of Social Security. Plan withholding on the catch-up distribution accordingly.

For the underlying rules — RMD ages, calculation tables, and account-by-account requirements — the IRS's own required minimum distributions page is the primary source. If you end up owing any portion of the excise tax, pay it through IRS.gov/payments rather than by mailed check, so the payment posts to the right year. And if your penalty question is about quarterly payments rather than retirement accounts, the estimated tax penalty waiver follows its own form-based process (Form 2210), just as business penalty relief runs through business penalty abatement.

Your next 24 hours

- Confirm the shortfall. Pull last year's Form 5498 or your year-end statement showing the account's RMD amount, and check for a Form 1099-R — no 1099-R means no distribution was taken, and the difference is your shortfall.

- Gather your paperwork. Your most recent tax return, the account statements, and a few notes on why the miss happened and when you discovered it — that's the raw material for the reasonable-cause statement.

- Get a free case review. Before you withdraw or file anything, let an experienced tax professional confirm the math, the form year, and the strongest way to word the waiver request — the correction window is the only clock here, and it only runs one direction. Call (888) 825-7779 or use the 2-minute form.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.