Penalty Relief

941 Penalty Abatement: Reasonable Cause for Payroll Penalties (2025)

The short answer: 941 penalty abatement removes penalties on your quarterly payroll tax return. You qualify two ways — first-time abatement if you have a clean three-year history, or reasonable cause if something outside your control caused the late deposit. File all 941s first, then request relief by phone, letter, or Form 843.

Buried in payroll penalties?

Send us your 941 notices. An experienced tax professional will tell you whether first-time abatement or reasonable cause fits your situation — and whether a Trust Fund Recovery Penalty is coming. Free, confidential, no pressure.

⏱ Timing that matters: the failure-to-deposit penalty climbs fast — 2% if 1–5 days late, 5% at 6–15 days, 10% after that, and up to 15% once the IRS sends a notice and you don't pay within 10 days. You generally have 3 years from the return due date (or 2 years from payment) to request a refund of a penalty you already paid using Form 843.

Why you got hit with a 941 penalty

Form 941 is the quarterly return where you report the income tax, Social Security, and Medicare you withheld from employee paychecks, plus the employer's share. The money you withhold is called trust fund tax — you're holding it in trust for the government. The IRS takes lateness here far more seriously than a personal income tax bill, because the cash already left your employees' checks.

Most 941 penalty abatement requests target one of three penalties:

- Failure to deposit — you didn't send withheld taxes on the right schedule (monthly or semiweekly). This is the most common payroll penalty and the one that escalates the fastest. See the IRS breakdown of the failure to deposit penalty.

- Failure to file — the 941 itself was late, charged at roughly 5% of unpaid tax per month, up to 25%.

- Failure to pay — the balance shown on the return wasn't paid, charged at 0.5% per month.

Interest is also added, but interest only comes off if the penalty it was charged on comes off. The IRS explains all of this on its penalties page.

What happens if you ignore payroll penalties

Unpaid 941 balances don't sit quietly. The automated collection system moves faster on payroll tax than almost anything else, and it can reach the people behind the business personally:

- Balance-due notices — the penalty and interest grow every month the deposit stays unpaid.

- Revenue Officer assignment — payroll cases are often handed to a person, not a computer. They can show up at your business.

- Trust Fund Recovery Penalty (TFRP) — the IRS can assess the unpaid withheld portion personally against owners, officers, or anyone responsible for paying it. This is a separate fight; see our guide to the Trust Fund Recovery Penalty.

- Liens and levies — against the business and, once the TFRP is assessed, against responsible individuals.

The takeaway: deal with 941 penalties before they grow into a personal liability. If your business is already behind, start with our walkthrough on 941 back taxes for businesses.

First-time abatement for 941 penalties

The simplest path is first-time abatement (FTA). It's an administrative waiver — you don't need a dramatic story, just a clean record. You qualify if:

- You filed all required returns (or valid extensions).

- You had no penalties for the three tax periods before the one you're asking about.

- You've paid, or arranged to pay, any tax due.

FTA usually covers a single quarter. If you owe penalties for several quarters in a row, FTA generally clears the earliest one, and you'll need reasonable cause for the rest. Our full first-time penalty abatement guide walks through how to ask and what disqualifies you.

Reasonable cause: what actually qualifies

When FTA doesn't fit, reasonable cause is the next door. The standard the IRS uses is whether you exercised "ordinary business care and prudence" but still couldn't deposit on time. The reason has to connect to the dates you were late. Strong reasonable-cause facts include:

- Serious illness, hospitalization, or death of the owner or the person who ran payroll.

- A fire, flood, hurricane, or other disaster that destroyed records or shut the business down.

- Theft or embezzlement — for example, a bookkeeper who diverted deposit funds.

- A bank or payroll-provider error that you can document and that you acted to fix.

- Inability to get records you needed despite reasonable effort.

What usually doesn't work on its own: "we ran short on cash and paid suppliers first." Because payroll tax is trust fund money, the IRS expects deposits to come ahead of other bills. A cash crunch can support reasonable cause only when it's tied to a genuine, sudden event outside your control. The IRS describes the test on its penalty relief due to reasonable cause page, and our deeper guide to reasonable-cause penalty abatement covers the evidence that wins.

A quick worked example

Say a contractor owes $40,000 in withheld payroll tax for one quarter and deposits it 20 days late. The failure-to-deposit penalty at the 10% tier is $4,000, plus interest. The owner had emergency heart surgery during that quarter and was hospitalized for two weeks — the same two weeks the deposit was due.

With hospital records and dates that line up, that's a textbook reasonable-cause request. If the business also had no penalties in the prior three years, first-time abatement could remove the penalty even faster, with no story required at all. Either way, the $4,000 penalty — and the interest charged on it — can come off.

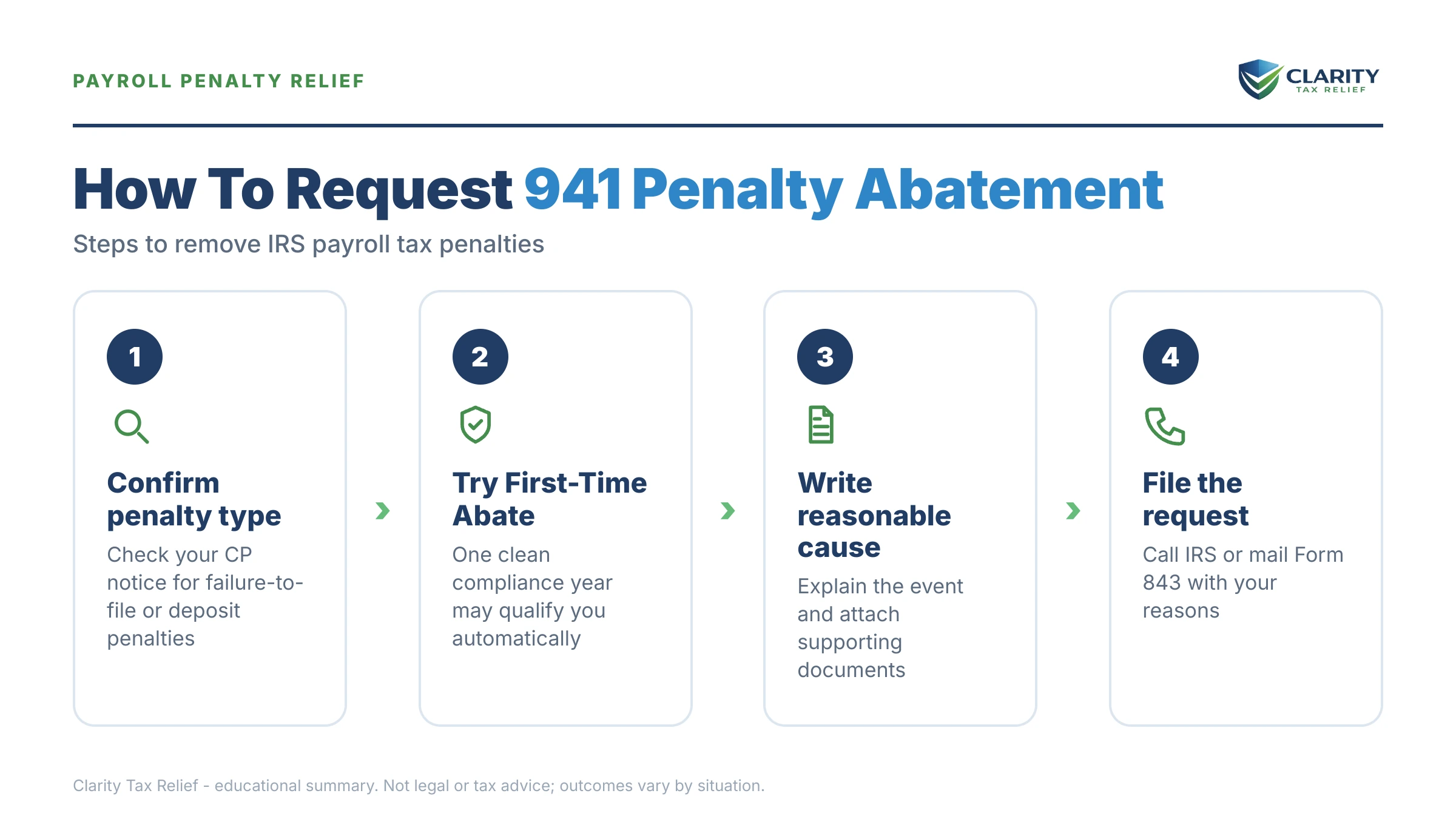

How to request 941 penalty abatement, step by step

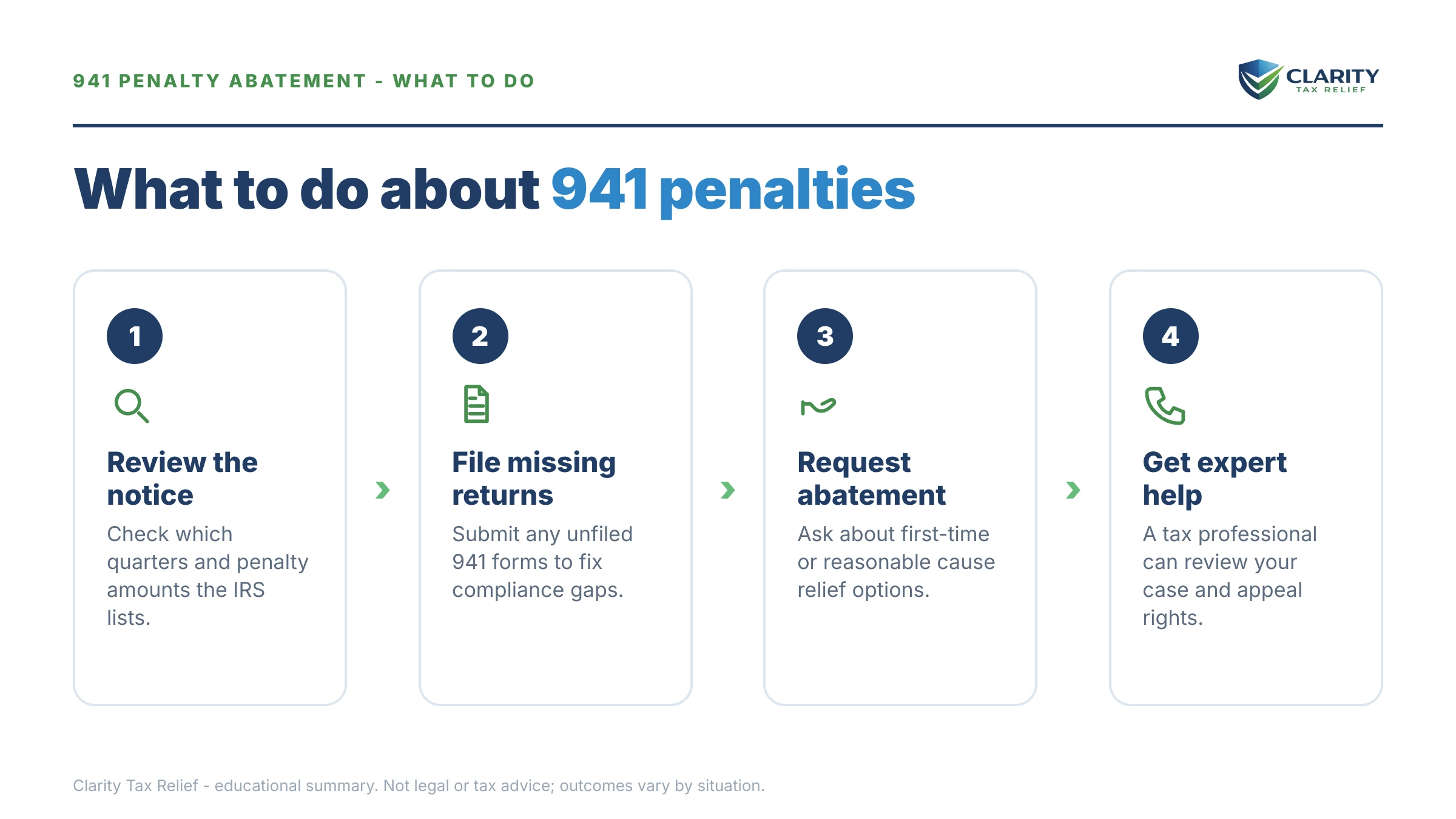

- Get current first. File every missing 941 and pay (or arrange to pay) the trust-fund portion. The IRS rarely abates penalties while returns are missing or withheld tax is still unpaid.

- Pull the numbers. Identify the exact quarter, the penalty type, and the dollar amount from your notice or account transcript so your request is specific.

- Try first-time abatement. Call the IRS Business and Specialty Tax line at the number on your notice and ask whether the quarter qualifies for FTA. It's often granted on the spot.

- If FTA doesn't apply, write the reasonable-cause request. State what happened, the exact dates, how it stopped you from depositing on time, and when you got back on track. Attach proof — hospital records, insurance claims, police or fire reports, bank letters.

- Use Form 843 to claim a refund if you already paid the penalty. See our Form 843 walkthrough and the IRS About Form 843 page. Watch the 3-year/2-year refund window.

- Keep copies and appeal if denied. Reasonable-cause denials can be appealed. Don't treat the first "no" as final.

One caution about scams: anyone promising to wipe out your payroll penalties for "pennies on the dollar" before reviewing your records is selling you something. Abatement depends on your facts — your compliance history and what actually happened.

941 penalty abatement questions, answered

Can 941 penalties be removed?

Yes. Penalties on Form 941 — failure to file, failure to pay, and failure to deposit — can be removed two ways: first-time abatement if you have a clean compliance history, or reasonable cause if something outside your control caused the late deposit. Interest is only removed if the penalty it was charged on is removed.

What counts as reasonable cause for late payroll taxes?

Reasonable cause means events you could not control despite using ordinary business care: serious illness or death of the person who handled payroll, a natural disaster, fire, theft of records, or a bank or payroll-provider error. A simple cash shortage usually does not qualify on its own, because the IRS expects deposits to come before other bills.

How do I request 941 penalty abatement?

You can call the IRS Business and Specialty Tax line to request first-time abatement, or write a letter or file Form 843 for reasonable cause. Identify the exact quarter and penalty, explain what happened with dates, and attach proof. Always make sure all 941s are filed and any trust-fund tax is paid first.

Does first-time abatement apply to 941 penalties?

Yes. First-time abatement applies to employment tax penalties on Form 941 if you have filed all required returns and had no penalties in the prior three years. It usually covers one quarter. Reasonable cause can cover additional quarters if you have a valid explanation backed by documents.

Will penalty abatement remove the Trust Fund Recovery Penalty?

No. The Trust Fund Recovery Penalty is a separate assessment against individuals personally responsible for withheld taxes, not a penalty on the business return. First-time abatement and reasonable cause apply to failure-to-file, failure-to-pay, and failure-to-deposit penalties — not to the Trust Fund Recovery Penalty, which is fought on different grounds.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.