Tax Debt & Family

Does IRS Debt Die With You? What Happens to Tax Debt After Death (2026)

The short answer: does IRS debt die with you? No — the balance becomes a claim against your estate, and the IRS gets paid from what you leave behind before your heirs do. But your children never inherit the debt personally, and if the estate can't cover it, the rest generally goes uncollected.

Maybe the balance has been sitting there for years, and somewhere past midnight the question stopped being "how do I pay this" and became "will my kids have to." Or maybe someone you love just died with an IRS bill on the kitchen counter, and you're afraid to open it. Either way, the answer is more reassuring than you expect — and more fixable than the silence has let you believe.

⏱ The clocks that matter: there's no notice deadline on this question, but two clocks run anyway. Penalties and interest accrue on the balance every month it sits unresolved — and the 10-year collection statute (CSED) keeps running even after death, for you and then for your estate.

Why IRS debt doesn't die with you — and doesn't follow your kids

Federal tax debt survives your death as a claim against your estate, but it never becomes your children's personal debt. Those two facts sit at the center of every version of this question. The debt was assessed against you, so when you die it attaches to what you owned — your house, your bank accounts, whatever passes through your estate — not to the people you leave behind.

That means no one calls your daughter demanding payment. No collector garnishes your son's wages for your back taxes. What the IRS can do is stand near the front of the line when your estate is settled, which shrinks — sometimes erases — what your heirs would have received.

There is one important spouse-shaped exception. If any of the debt comes from a jointly filed return, your spouse was already fully liable for every dollar of it — that liability existed before you died and continues after. If you filed single or the debt is from your separate returns, your spouse's own assets are generally out of reach, though community property states complicate this. If you're on the other side of that question, start with deceased spouse tax debt: am I responsible.

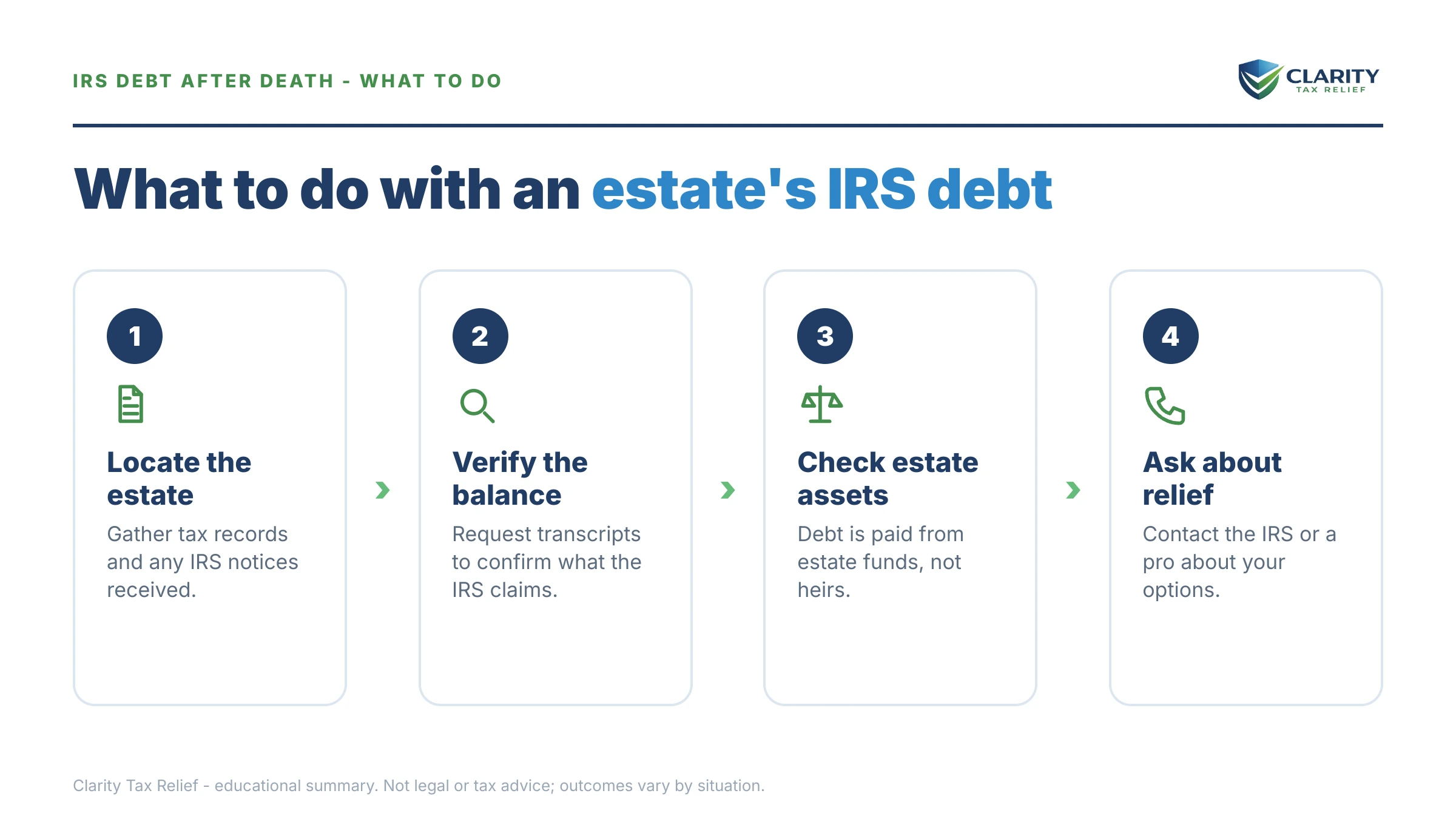

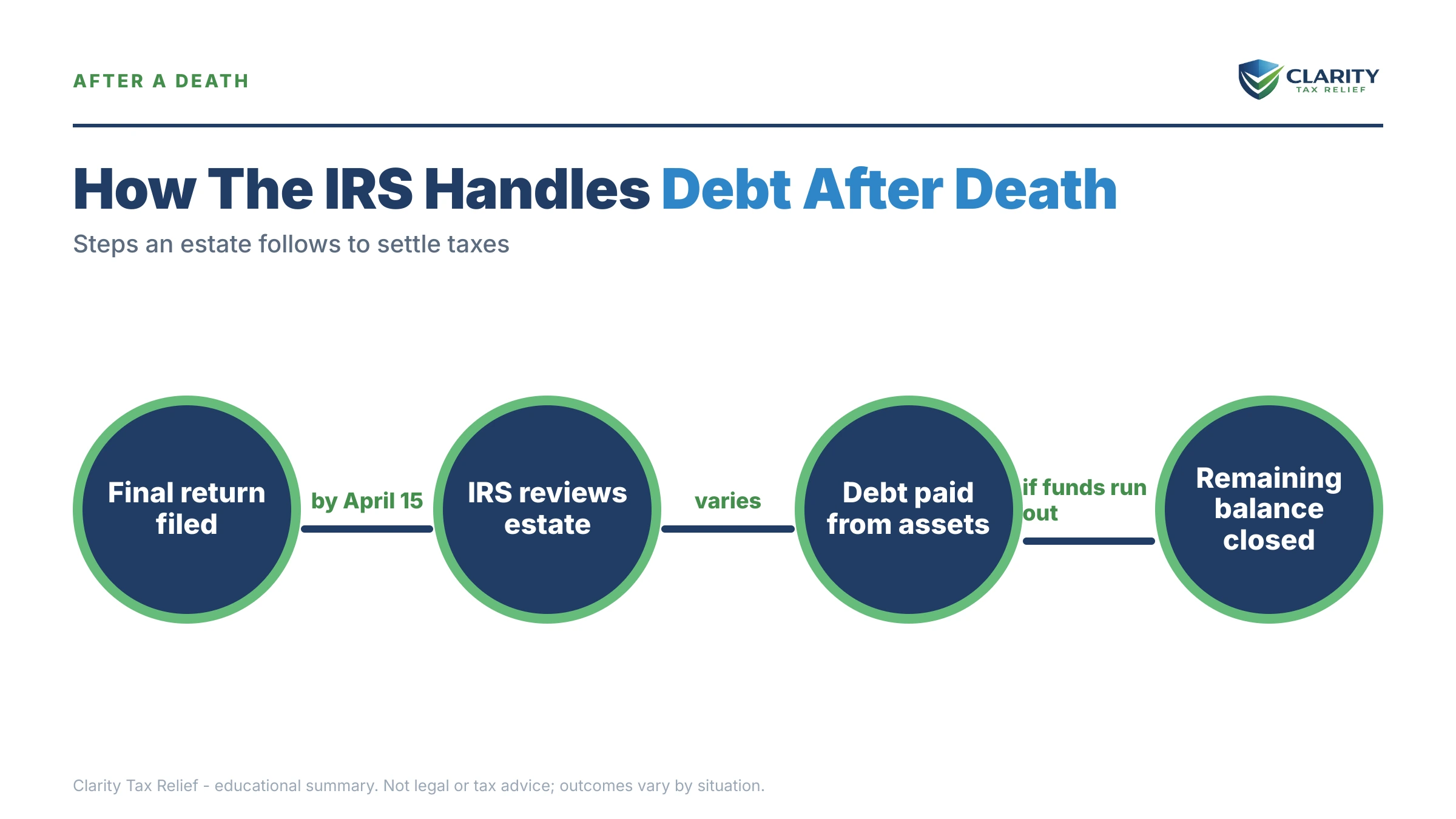

What happens to your IRS debt when you die: the sequence

After death, the IRS collects from an estate in a predictable order — and nothing about the process requires your family to pay out of pocket. Here's the sequence, stage by stage:

- A final Form 1040 gets filed. Your executor (or a surviving family member) files your last return for the year of death. Any balance on it joins the existing debt.

- The estate opens and the IRS files its claim. Federal tax claims carry priority over most other creditors — the government generally gets paid before heirs and before ordinary unsecured debts.

- Any existing federal tax lien follows the property. If a Notice of Federal Tax Lien was filed while you were alive, it stays attached to your real estate and other assets even as they change hands — the mechanics are covered in IRS lien after death.

- The executor pays claims in legal priority order. This is the one place a living person can get burned: an executor who hands assets to heirs before paying a known IRS debt can be held personally liable under 31 U.S.C. §3713 — see executor personally liable IRS.

- Whatever remains goes to heirs — clean. Once the IRS claim is satisfied (or the estate is exhausted), heirs take what's left with no tax-debt strings attached to them personally.

Notice what's missing from that sequence: any step where the IRS bills your children, your siblings, or your friends. The system takes from what you left, in order, and stops.

Carrying a balance and worried about your family?

Interest and penalties are compounding on that debt every month it sits — and every option that shrinks it works better while you're alive. Get a free, confidential review of exactly where you stand and what it would take to resolve it.

Who the IRS can collect from after you die — and who's safe

After death, the IRS can reach your probate estate and jointly liable spouses — but not heirs personally, and generally not assets that pass directly to a named beneficiary. This table is the map most families are searching for:

| Person or asset | Can the IRS collect? | Why |

|---|---|---|

| Your probate estate | Yes — first in line | Federal tax claims have priority; the executor must pay the IRS before distributing to heirs |

| Surviving spouse — jointly filed years | Yes | Joint and several liability means each spouse owes 100%, and death doesn't change that |

| Surviving spouse — your separate-return debt | Generally no | Exception: community property states, where community assets may be reachable |

| Children and other heirs | Not personally | The inheritance shrinks, but no bill is ever issued in an heir's name |

| Life insurance with a named beneficiary | Generally no | Proceeds pass outside probate — different if the estate itself is the beneficiary |

| 401(k) / IRA with a named beneficiary | Not for your debt | The beneficiary owes their own income tax on traditional-account distributions, not your balance |

| Your executor | Only if they misstep | Personal liability applies when assets are distributed to heirs before a known IRS debt is paid |

Two of those rows deserve a closer look. Assets that flow to a named beneficiary — life insurance, retirement accounts, payable-on-death bank accounts — generally never enter the probate estate, so the IRS's claim never touches them. The edge cases (a lien already attached to a policy's cash value, or an estate named as beneficiary) are covered in can the IRS take life insurance. And if you're the heir wondering whether money coming to you is exposed to your own or the decedent's tax problems, see can the IRS take my inheritance.

Does IRS debt die with you if your estate is empty?

When someone dies with more IRS debt than assets, the uncovered balance generally dies with them — unpaid and uncollectible. The IRS takes what the estate has, in priority order, and cannot invent a new debtor to chase for the rest. Once the estate is exhausted and the 10-year Collection Statute Expiration Date passes, the account is written off.

That 10-year clock runs from the date each balance was assessed, and death neither pauses nor restarts it — the full rules are in how long can the IRS collect back taxes. Tolling events that happened during life (a pending Offer in Compromise, a bankruptcy, certain appeals) can have pushed the date later, so the printed 10 years is a starting point, not a promise.

Three caveats keep an "empty estate" from being a total escape hatch. A federal tax lien filed during life follows property to whoever receives it. Joint-return years remain fully collectible from the surviving spouse. And if assets were shuffled to family members to keep them away from the IRS, transferee liability lets the government pursue those specific assets in the recipient's hands. Deliberately dying broke is not a strategy — it's covered in the honest breakdown at does the IRS ever forgive tax debt.

Your options while you're alive (when every one of them works better)

Every IRS resolution program is available to a living taxpayer and almost none of them to a dead one — which is the real reason this question deserves action, not just an answer. The general playbook lives in our guide to how to settle tax debt yourself; here's how the options line up at a balance like $76,400:

| Option | Eligibility at $76,400 | What to know |

|---|---|---|

| Installment agreement | Above $50,000, financial disclosure (Form 433-F) is typically required | Interest and penalties keep accruing while you pay; see IRS payment plan over $50,000 |

| Pay down below $50,000 first | A lump payment of $26,401+ drops you into streamlined territory | Streamlined agreements up to 72 months can be set up online without full financials |

| Partial-pay installment agreement | Monthly payment set by what your budget actually allows | Whatever remains at the CSED can expire unpaid; IRS reviews finances periodically |

| Offer in Compromise | Means-tested: assets plus future income must fall short of the balance | $205 fee and 20% down on lump-sum offers (both waived with low-income certification); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Currently Not Collectible | Genuine hardship shown through Form 433 financials | Collection pauses, interest accrues, and the 10-year clock keeps running |

| Bankruptcy | Only income taxes meeting the age and filing tests | Powerful for old debt, useless for recent debt — see does bankruptcy clear IRS debt |

| Waiting out the CSED | 10 years from each assessment, extended by tolling events | Levies, liens, and refund offsets remain possible the entire time you wait |

One more consequence specific to a balance this size: at $76,400, you're above the $66,000 passport-certification threshold for 2026. A seriously-delinquent certification can block passport renewal — a problem that resolving the debt (or getting into an approved arrangement) heads off. And before you count on the 10-year clock, estimate your own expiration dates with our CSED Calculator — it estimates, based on your assessment dates and tolling events, when each year's debt would actually expire.

A worked example: single, W-2, and $76,400 deep

Say you're a W-2 employee filing single and you owe $76,400 across a few tax years. This is hypothetical, but the arithmetic is real.

If you resolve it while alive: a straight 72-month payment plan runs about $76,400 ÷ 72 ≈ $1,061 a month, with interest and the monthly late-payment penalty still accruing on the shrinking balance, so real payoff time stretches longer. Alternatively, a one-time payment of $26,401 drops the balance to $49,999 — under the streamlined line — and the remaining plan runs roughly $695 a month, set up online without handing over full financials.

If you die with it unresolved: suppose you leave a condo with $150,000 of equity, $9,000 in checking, and a $110,000 401(k) with your sister named as beneficiary. Your probate estate is about $159,000. The executor files your final return, settles estate administration costs under state priority rules, then pays the IRS the $76,400 plus whatever interest accrued. Your heirs split roughly the remaining $80,000 or so. Your sister keeps the entire 401(k) — it passed outside the estate — though she'll owe her own income tax as she withdraws from it.

Now flip the asset picture: if your only asset at death is $12,000 in checking, the IRS collects what's left after higher-priority estate costs, and the remaining $64,000+ generally goes uncollected. Nobody bills your family for the difference. The debt didn't transfer — it just consumed what existed and expired.

How to keep IRS debt from burdening your family: step by step

- Pull your IRS account transcripts. They show every assessment date, which sets the 10-year expiration clock for each year you owe — the single most important fact in this whole question.

- File every missing return. Unfiled years block nearly every resolution program, and the failure-to-file penalty (5% per month) is ten times the failure-to-pay penalty — though in months where both apply, the failure-to-file portion drops to 4.5% (5% combined). File even when you can't pay.

- Start a resolution path now. A payment plan, hardship status, or an offer stops enforcement while you're alive and shrinks or freezes what your estate would ever face.

- Check your beneficiary designations. Retirement accounts and life insurance with named beneficiaries pass outside your estate — naming your estate instead hands those dollars to the IRS first.

- Brief the person who would handle your estate. Tell them what you owe, where your returns and notices live, and that the IRS gets paid before heirs — that one conversation protects them from personal liability.

Payment arrangements can be started directly at the IRS's payment plans and installment agreements page, and any payment — partial or full — goes through IRS.gov/payments.

When you can handle this yourself — and when help changes the outcome

Plenty of this you can do alone. If your balance is small enough to pay within 180 days, a short-term plan costs nothing to set up. If you're under $50,000 with all returns filed, the online streamlined agreement takes twenty minutes. If you're the heir of someone who died owing and there's no estate to speak of, you may genuinely need to do nothing at all — and if collectors are pressuring you anyway, the free routes in free help with IRS tax debt (including the Taxpayer Advocate Service) exist exactly for that.

Experienced help earns its cost in the harder versions: a balance above $50,000 where Form 433 disclosure determines your monthly payment, multiple unfiled years that have to be sequenced correctly, an Offer in Compromise where the asset-and-income math decides everything, an executor staring at §3713 exposure, or a joint-liability tangle after a death or divorce (that last one runs through divorce and IRS debt: who pays). In those cases, the order you fix things in changes the dollar outcome — and a wrong disclosure is hard to unwind.

Terms in this question, decoded

- CSED — the Collection Statute Expiration Date: 10 years from each assessment, after which the IRS can no longer collect that balance (tolling events extend it).

- Probate estate — the assets that pass through court supervision at death; this is what the IRS's claim attaches to.

- Federal tax lien — the government's legal claim against your property for unpaid tax; once filed, it follows the property even after death.

- Joint and several liability — on a jointly filed return, each spouse owes the entire balance, not half.

- Fiduciary liability (31 U.S.C. §3713) — an executor's personal exposure for distributing estate assets before paying a known federal debt.

- Transferee liability — the IRS's power to pursue assets that were moved to someone else to keep them out of the government's reach.

IRS debt after death: your questions, answered

Do children inherit their parents' IRS debt?

No — children never become personally liable for a parent's IRS debt, no matter how large it is. The debt is paid from the parent's estate before heirs receive anything, so the inheritance shrinks, but no bill arrives in the child's name. The one exception is transferee liability: if assets were moved to a child to dodge the debt, the IRS can pursue those specific assets.

Is a surviving spouse responsible for a deceased spouse's IRS debt?

Only in two situations. If the debt comes from a jointly filed return, the surviving spouse was already fully liable and remains so after the death. And in community property states, the IRS may reach community assets even for one spouse's separate debt. Debt from the deceased spouse's separate returns is otherwise not the survivor's personal obligation.

What happens if someone dies owing the IRS and the estate has no money?

In most cases the debt simply goes unpaid — the IRS cannot bill family members for a balance the estate can't cover. The agency can still collect anything the estate does have, and a federal tax lien filed during life follows property to whoever receives it. But once the estate is exhausted and the 10-year collection statute runs, the balance is written off.

Does the IRS 10-year collection statute keep running after death?

Yes. The Collection Statute Expiration Date is set 10 years from each assessment and does not restart or pause just because the taxpayer died. The IRS has whatever time remains on that clock to collect from the estate. Tolling events — a pending Offer in Compromise, bankruptcy, or certain appeals filed before death — can have extended the date, so pull transcripts to confirm.

Can the IRS take life insurance money after someone dies?

Generally no — proceeds paid directly to a named beneficiary pass outside the probate estate and are not used to pay the decedent's income tax debt. It changes if the estate itself is the beneficiary, because then the money becomes an estate asset the IRS can claim. Policies with cash value that were already encumbered by a federal tax lien can also get complicated.

Can the IRS take an inherited 401(k) or IRA for the original owner's tax debt?

Not when the account passes to a directly named beneficiary — it skips probate and isn't available to the decedent's creditors, including the IRS. The beneficiary will owe ordinary income tax on distributions from a traditional account, but that's their own new tax bill, not the decedent's old one. If no beneficiary was named and the account falls into the estate, the IRS can reach it.

Can an executor be personally liable for a dead person's IRS debt?

Yes, in one specific way: under 31 U.S.C. §3713, an executor who distributes estate assets to heirs while knowing about an unpaid federal tax debt can be held personally liable up to the amount distributed. Executors who pay the IRS in proper priority order before distributing anything are not personally at risk for the balance itself.

Your next 24 hours

- Find your assessment dates. Log into your IRS online account or pull your account transcripts — those dates set the 10-year clock on every year you owe, and everything else is planned around them.

- Gather three things: your most recent return, any IRS notices you've received, and a rough picture of your income and assets. That's all a real options analysis requires.

- Get the free case review. Interest and penalties compound on your balance every month it sits unresolved — an experienced tax professional can map which option fits your numbers in one call. Use the 2-minute form at claritytaxrelief.com/#consult or call (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.