Tax Debt & Credit

Does Owing the IRS Affect Credit? What Lenders Can Still See (2026)

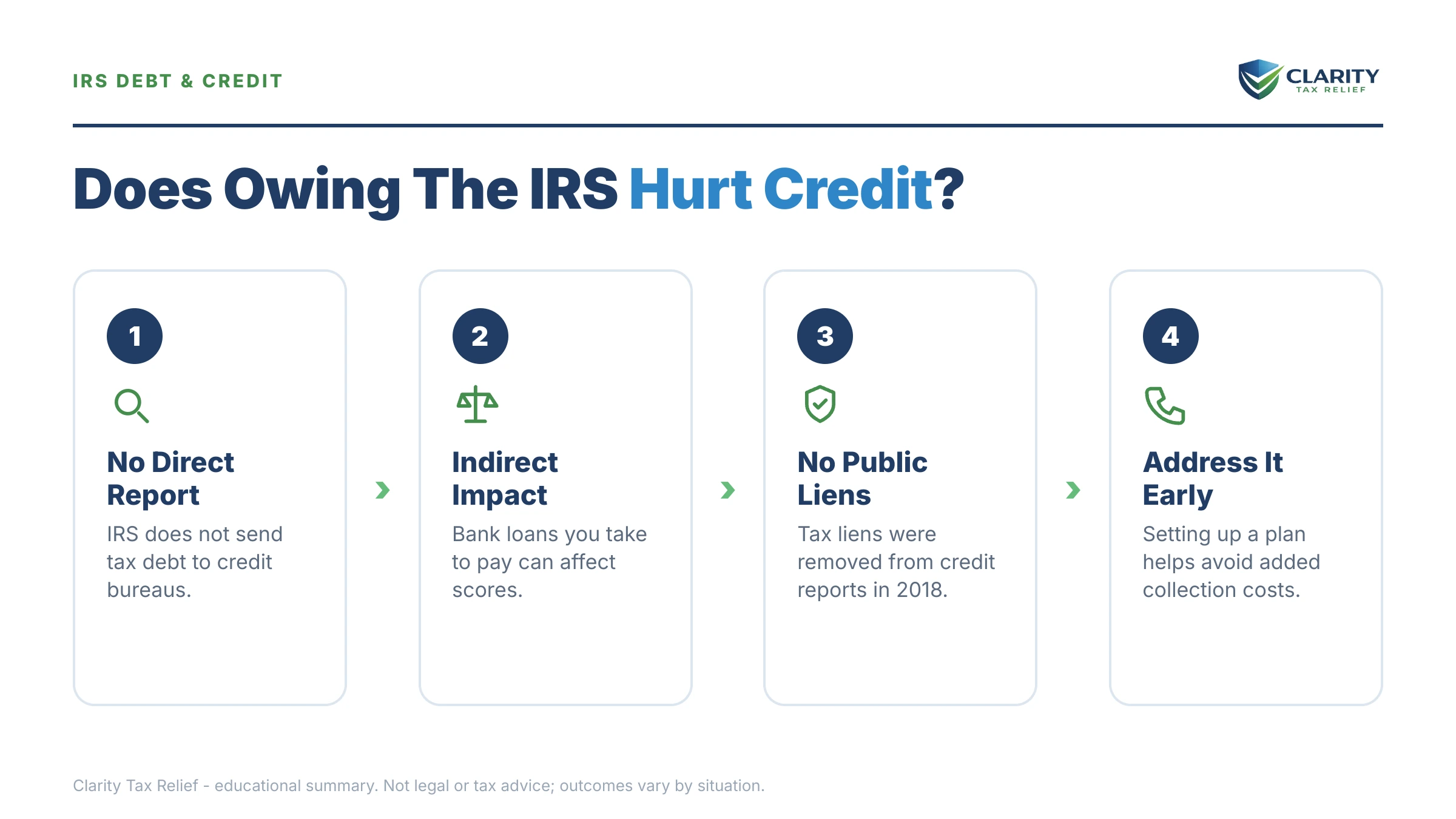

The short answer: no — owing the IRS does not directly affect your credit. The IRS doesn't report tax debt to Equifax, Experian, or TransUnion, and tax liens were removed from all three credit reports in April 2018. But lenders can still find IRS debt through public records and loan applications.

You're self-employed, a couple of strong 1099 years left you with an IRS balance you're still working down, and now there's a loan application in front of you. Before you hit submit, you want to know whether that tax debt will torpedo your score. The honest answer has two layers — and the second layer, the one the credit bureaus never show you, is where borrowers get blindsided.

⏱ The real clock: there's no credit-bureau deadline, because the IRS never reports to the bureaus. But the failure-to-pay penalty adds 0.5% of your balance each month (capped at 25% total; it drops to 0.25% while an approved payment plan is active and rises to 1% after a final intent-to-levy notice), interest accrues on top, and the longer a balance sits unresolved, the more likely the IRS files a public-record lien that any lender or title company can find.

Does owing the IRS affect credit reports directly? No — and here's why

The IRS does not report tax debt to any credit bureau — Equifax, Experian, and TransUnion have carried no IRS balances, payment plans, or tax liens since April 2018. The IRS isn't a lender and doesn't furnish account data the way your credit card company does. There is no "IRS tradeline" on any consumer credit report.

That wasn't always true in practice. Before 2018, a filed federal tax lien landed in the public-records section of your report and could knock your score down badly. The three bureaus removed all tax liens — federal and state — from consumer reports by April 2018, after accuracy problems with public-record data. They haven't come back. The full history is in our guide to the tax lien on credit report question.

So the direct answer is clean: your score doesn't move when a balance-due notice arrives, doesn't move as penalties stack up, and doesn't even move if the IRS files a lien. If that were the whole story, this article would end here. It isn't.

How lenders still find out you owe the IRS

Lenders don't rely on your credit report alone — and IRS debt surfaces through four channels the bureaus never touch. This is especially true for self-employed borrowers, whose income gets verified straight from IRS records. The table below maps each piece of an IRS debt to what actually shows up where.

- Loan application questions. The standard mortgage application (Form 1003) asks directly whether you're delinquent or in default on any federal debt. Answering falsely on a loan application is fraud — this question, not your score, is where IRS debt first enters underwriting.

- Public-record searches. A filed Notice of Federal Tax Lien is recorded at the county level. It's off your credit report, but a title company or lender running a records search finds it immediately — here's where a tax lien public record lives and how to look yours up.

- Your tax transcripts. Mortgage lenders routinely pull IRS transcripts with Form 4506-C to verify income — standard practice for self-employed applicants. Unfiled years and balance-due history can surface there.

- Your bank statements. A monthly debit to "IRS USATAXPYMT" on the statements you hand an underwriter invites the question, and the payment gets counted against your debt-to-income ratio.

| Item | On your credit report? | How lenders still see it |

|---|---|---|

| IRS balance due / back taxes | No | Application questions (Form 1003) + transcripts pulled via Form 4506-C |

| Federal tax lien (NFTL) | No — removed from all three bureaus in 2018 | County recorder; every title search finds it |

| IRS installment agreement | No | Bank statements; monthly payment counted in your DTI |

| IRS bank or wage levy | No — but the bills that bounce afterward do report | Missed payments on other accounts hit your report |

| Accepted Offer in Compromise | No | Sits in the IRS public inspection file for a year |

| Loan or credit card used to pay the IRS | Yes — reports like any consumer debt | Utilization and the new tradeline show immediately |

| State tax warrant or lien (e.g., New York) | No | Public court and county records |

Notice the pattern: the debt itself is invisible to your score, but nearly every consequence of leaving it unresolved is visible somewhere a lender looks. The image below shows this split — what stays off your report versus what lenders can still find — at a glance.

What happens if you do nothing: the sequence that eventually reaches your finances

Unpaid IRS debt escalates through an automated notice sequence, and the later stages — lien and levy — are the ones that damage your borrowing power. Your credit score sleeps through the whole process; your bank account and your title search do not.

- First bill (CP14). A balance-due notice with roughly 21 days to respond. Nothing touches credit or public records — this is the cheapest moment to act.

- Reminders (CP501, CP503). Still just bills. The balance grows monthly through penalties and interest, but remains invisible to lenders.

- CP504 — intent to levy your state refund. Enforcement begins under IRC §6331(d). Still nothing on credit, but the account is now flagged for stronger action.

- Notice of Federal Tax Lien. The IRS can file a lien in county records securing its claim against everything you own. It never appears on your credit report — but from this day forward, every title search, refinance, and business-loan records check surfaces it.

- LT11 / Letter 1058 — final notice of intent to levy. A 30-day clock starts, along with your Collection Due Process appeal rights (Form 12153). This is the last exit before seizure.

- Levy. A bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. When a levy empties the account your mortgage and card payments draft from, those bounced payments are what finally hit your credit report — the IRS debt damages your score by proxy.

Two more thresholds matter as a balance grows. At $66,000 (the 2026 figure), the IRS can certify your debt to the State Department and block your passport. And every month of delay compounds the math — you can estimate how fast your own balance is growing with our Penalty & Interest Calculator. In 2026, with IRS staffing down roughly 27%, humans are harder to reach than ever — but this entire sequence runs on automated systems that never got cut.

Owe the IRS with a loan, refi, or mortgage application coming?

There's no credit-bureau clock — but penalties and interest accrue every month, and an unresolved balance is one lien filing away from surfacing in your lender's records search. Get your balance and lien exposure reviewed free by an experienced tax professional before you apply.

Your options — and what each one does to your borrowing power

Every IRS resolution program keeps your credit report clean; the difference between them is cost, eligibility, and how a lender reads your situation afterward. The table uses a $48,300 balance — a common size for a self-employed filer after two under-withheld years — but the eligibility lines apply at any amount. For the full playbook on each program, see how to settle tax debt yourself.

| Option | Eligibility at a glance | Effect on credit & borrowing |

|---|---|---|

| Pay in full | Anyone with the funds | Nothing ever reports; stops accrual; cleanest position for underwriting |

| Short-term plan (up to 180 days) | Can pay the full balance within 180 days; $0 setup fee | Never reports; resolved before most loan timelines even matter |

| Streamlined installment agreement | Balance ≤ $50,000; up to 72 months, set up online | Never reports; monthly payment counts in DTI; direct debit is your best lien prevention |

| Guaranteed installment agreement | Balance ≤ $10,000 — not available at $48,300 | Never reports; near-automatic approval at small balances |

| Offer in Compromise | Means-tested; $205 fee (waived with low-income certification); roughly 1 in 5 accepted in FY2024 | Never reports; accepted offers sit in a public inspection file for one year |

| Currently Not Collectible | Documented hardship on Form 433-F | Never reports; pauses levies, but a lien remains possible and the balance keeps growing |

| Credit card or personal loan payoff | Depends on your available credit | The one option that DOES report — utilization spike plus a new tradeline |

One resolution path genuinely does hit your credit: bankruptcy. A Chapter 7 or 13 filing appears on your report for years even in the cases where it clears the tax debt — understand what does bankruptcy clear IRS debt actually covers before considering that trade.

A worked example: $48,300, self-employed, loan application in six months

Say you owe $48,300 across two years of self-employment tax that quarterly payments didn't cover. Because the balance is under $50,000, a streamlined installment agreement is available online without a full financial disclosure. Spread over the maximum 72 months, that's $48,300 ÷ 72 ≈ $671 per month — though interest and the 0.5% monthly failure-to-pay penalty keep accruing, so paying more than the minimum shortens the real payoff.

Now compare the "protect my credit" instinct of putting it on plastic. Charging $48,300 to credit cards would spike your utilization and add a new tradeline — visible score damage — plus card interest and processing fees, all to retire a debt that was never on your report in the first place. Run that comparison properly in our guide to the best way to pay the IRS.

For the loan application itself: the $671 payment lands in your debt-to-income ratio, and you'll disclose the agreement when asked about federal debt. But an agreement in good standing with no lien filed is a situation many lenders can work with. An ignored $48,300 that ripens into a recorded lien is not.

Buying a house or refinancing while you owe the IRS

A filed tax lien blocks real-estate lending in a way your credit score never will, because it attaches to the property's title. Before a lien exists, many lenders will approve a borrower whose IRS debt sits in a current installment agreement, counting the payment in DTI — the specifics are in can I buy a house if I owe the IRS. After a lien is recorded, the title company finds it on day one, and most lenders require it paid, subordinated, or discharged before closing; the same problem hits a refinance with an IRS lien in place.

If a lien has already been filed, it isn't permanent. The IRS releases a lien after the debt is satisfied, and in some cases — including converting to a direct-debit installment agreement and meeting the IRS's criteria — you can request a full lien withdrawal with Form 12277, which removes the public filing itself rather than just marking it paid. The IRS explains how liens attach and end at its page on understanding a federal tax lien.

How to respond, step by step

- Pull your full IRS balance. Log into your IRS online account and confirm what you owe across every year — resolution starts with the real number, not the last notice you opened.

- Search public records for a filed lien. Check the county recorder where you live or own property; a Notice of Federal Tax Lien is public even though it's off your credit report.

- Choose a resolution before the lien stage. Pick the option that fits your finances — payment plan, Offer in Compromise, or hardship status — because an agreement in place is your best lien prevention.

- Set up direct debit if you choose a payment plan. Direct-debit agreements put you on the strongest footing for keeping a lien off the record and for requesting withdrawal of one already filed.

- Clean up any filed lien after you resolve the debt. Request a release once you've paid, or a withdrawal on Form 12277 if you meet the IRS criteria, so title searches stop flagging you.

Payment plans can be set up directly at the IRS's payment plans and installment agreements page, and one-time payments at IRS.gov/payments.

When you can handle this yourself

Most people asking this question don't need professional help — they need a resolution in place before a lender looks. If your balance is one you can pay within 180 days, or it's under $50,000 and a streamlined online agreement fits your budget, set it up yourself this week and your credit question is answered: nothing reports, nothing gets filed, done.

Experienced help changes the outcome in specific situations: a lien already recorded weeks before a home purchase, where the sequencing of payoff, subordination, or withdrawal decides whether you close; multiple unfiled years surfacing on the transcripts your lender pulls; a levy already in motion draining the account your other bills draft from; or Offer in Compromise math on self-employment income, where the IRS's calculation of your future income is nothing like guesswork. In those cases, the cost of getting the order of operations wrong usually exceeds the cost of help.

Terms on your credit file and IRS paperwork, decoded

- Notice of Federal Tax Lien (NFTL): the public document the IRS records to secure its claim against your property — off credit reports since 2018, but visible in any records search.

- Lien vs. levy: a lien is a claim that sits on what you own; a levy is the actual taking of money or property.

- Public record: filings at courts and county recorders that anyone — including lenders and title companies — can search, independent of the credit bureaus.

- DTI (debt-to-income ratio): your monthly debt payments divided by monthly income; lenders count an IRS installment payment here even though it never appears on your report.

- Tradeline: an individual account entry on a credit report; the IRS never creates one, but a loan you take out to pay the IRS does.

- CSED: the collection statute expiration date — generally 10 years from assessment, after which the IRS's ability to collect (and any lien securing it) ends, subject to events that pause the clock.

IRS debt and credit: your questions, answered

Does the IRS report tax debt to credit bureaus?

No. The IRS does not report balances, payment plans, or enforcement actions to Equifax, Experian, or TransUnion, and it doesn't furnish data to the bureaus the way lenders do. Your score will not change because you owe the IRS. The exposure is indirect: public-record lien filings, loan-application questions about delinquent federal debt, and transcript pulls during underwriting.

Do tax liens still show up on credit reports in 2026?

No. All three credit bureaus removed tax liens from consumer credit reports by April 2018, and they have not returned in 2026. A filed Notice of Federal Tax Lien is still a public record, though — county recorders and title searches surface it immediately, which is why liens still block mortgages and refinances even when your credit score is untouched.

Does an IRS payment plan hurt your credit score?

No. An installment agreement is never reported to the credit bureaus, so setting one up doesn't lower your score and paying it on time doesn't raise it. Lenders who see the payment on your bank statements will count it in your debt-to-income ratio, so a $671 monthly IRS payment can reduce how much house or car you qualify for even though it never touches your report.

Can I get a mortgage if I owe the IRS?

Often, yes — many lenders will approve a borrower with IRS debt if there is no filed tax lien and an installment agreement is in place and current, with the monthly payment counted in your debt-to-income ratio. A filed lien changes things: it clouds title, and most lenders will require it paid, subordinated, or discharged before closing. Get the resolution in place before you apply, not during underwriting.

Will an IRS bank levy show up on my credit report?

Not directly — the levy itself is never reported. The damage comes one step later: a levy freezes the funds in your account for 21 days and then sends them to the IRS, and if your mortgage, card, or auto payments bounce as a result, those missed payments absolutely do hit your credit report. That chain reaction is the most common way IRS debt ends up damaging a credit score.

Does owing state taxes affect your credit?

Like IRS debt, state tax debt no longer appears on credit reports — the bureaus removed tax liens and civil judgments from all consumer reports. But states create public records too, and some are more aggressive than the IRS: a New York tax warrant, for example, is a civil judgment and lien filed in public court records, where any lender or landlord running a public-records search will find it.

Is it better to pay the IRS with a credit card to protect my credit?

Usually not. IRS debt doesn't report to the bureaus, but credit card debt does — so moving a tax balance onto cards converts invisible debt into visible utilization, which can drop your score, and adds processing fees on top. A direct IRS payment plan is often cheaper and keeps your report clean. Compare the true costs before you swipe.

Your next 24 hours

- Find your real number. Log into your IRS online account and write down the exact total across all years — then check your county recorder for any lien filing you didn't know about.

- Gather three things: your most recent tax return, the latest IRS notice you received, and a rough picture of monthly income and expenses. That's everything needed to match you to an option.

- Get a free case review — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779. Your credit report isn't the clock here; the 0.5% monthly penalty and daily interest are, and both stop escalating the day a resolution is in place.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.