Owe the IRS

Filed Taxes and Owe More Than Expected? Here's What to Do (2026)

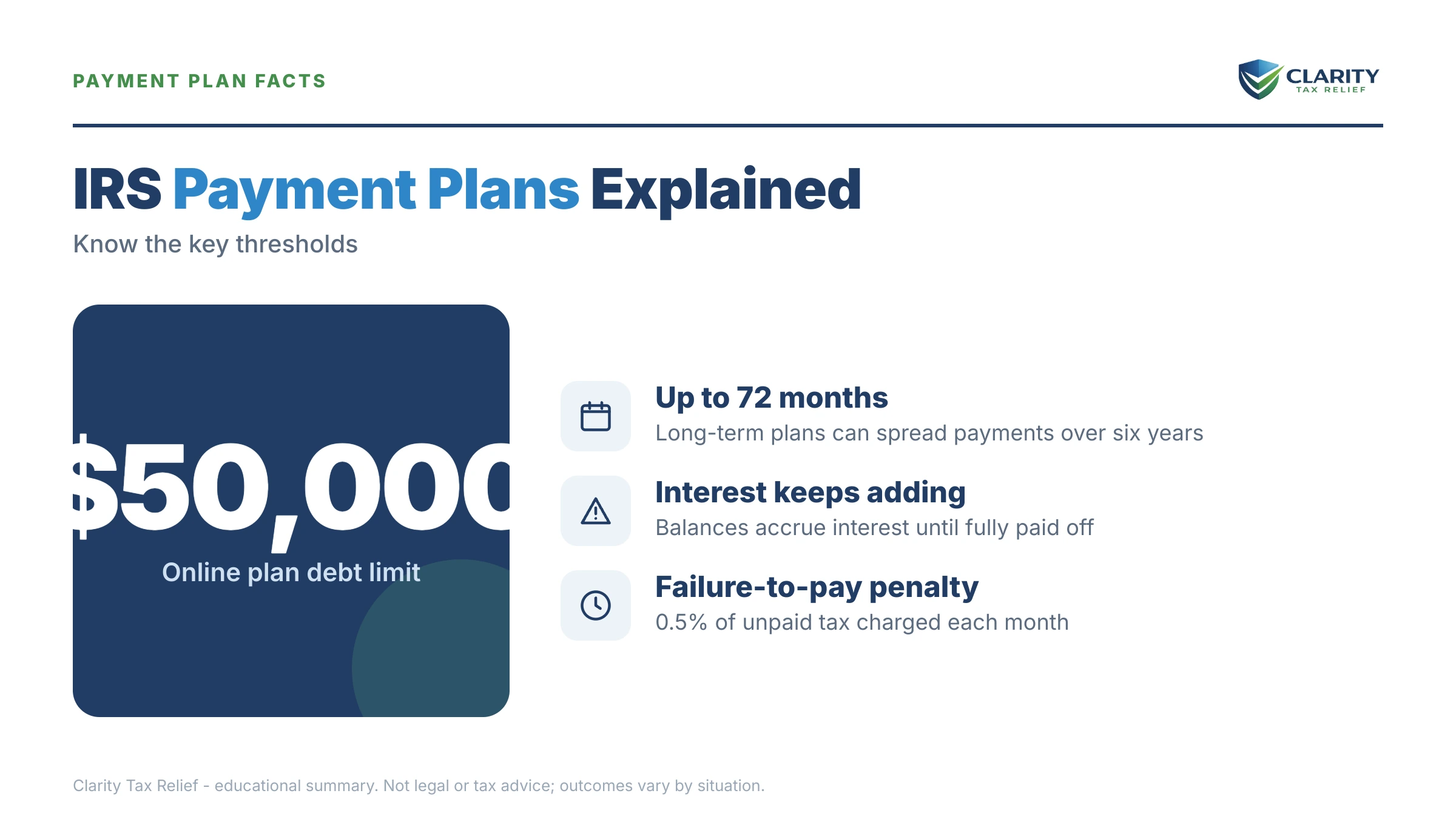

The short answer: if you filed taxes and owe more than expected, the balance was legally due on the April deadline — it's now growing by a 0.5% monthly penalty plus daily interest. You don't have to pay it all today: balances of $50,000 or less qualify for an online IRS payment plan of up to 72 months.

You hit "submit," braced for a small refund or maybe breaking even — and the software showed a balance due with a comma in it. You've re-run the numbers twice, and the figure won't budge. Take a breath: the number is almost certainly explainable, the IRS hasn't done anything yet, and you're catching this at the cheapest moment it will ever be.

Here's what most people miss: filing taxes and owing more than expected means you know about the debt before the IRS has even mailed a bill. That head start is real leverage — you can lock in a payment arrangement before the first notice ever prints. The image below maps how a refund turns into a surprise balance and where the money leaks out of your withholding.

⏱ The clock that matters: your balance was due on the April filing deadline, no matter when you filed. From that date, the failure-to-pay penalty adds 0.5% per month and interest compounds daily. Once the IRS's first bill (a CP14) arrives, you typically have about 21 days before the notice sequence starts escalating.

Why you filed taxes and owe more than expected

Most surprise tax bills for W-2 employees come from income that was withheld at a lower rate than the bracket it actually landed in. Your regular paycheck withholding was probably fine — it's the money around the paycheck that created the gap:

- Bonuses and RSUs withheld at the flat 22% supplemental rate. When a bonus or vested stock stacks on top of a salary, that income is often really taxed at 32% or 35%. The 10–13 point gap on every supplemental dollar is the single most common source of five-figure surprises.

- Stock, crypto, or fund sales with zero withholding. Capital gains show up on your return with nothing prepaid against them. Brokerages don't withhold; the whole tax lands in April.

- A second job or mid-year job change. Each employer withholds as if its paycheck were your only income, so both under-withhold. If this is you every spring, the fix is a withholding one — see two jobs owe taxes every year.

- Side income on a 1099. Gig work — think Amazon Flex owe taxes situations — arrives untaxed and adds self-employment tax on top of income tax. If this was your first year of it, the first year self employed owe taxes guide walks the specific math.

- A W-4 that no longer matches your life. A raise into a new bracket, dropping a dependent credit, or an old W-4 carried over from a lower-income year all quietly shrink withholding relative to what you owe.

- An underpayment penalty already baked into the number. If your prepayments fell far enough short during the year, tax software adds an estimated-tax underpayment charge on top of the tax itself — see underpayment penalty estimated taxes for how that piece is computed.

First, make sure the number is real

A surprise balance is only as real as the return that produced it — and mistyped W-2 entries, duplicated 1099s, and stock sales reported without cost basis are all common, fixable errors. Before you arrange payment on a big number, spend one evening checking:

- W-2 Box 2 versus what the software shows. A transposed digit in federal withholding directly inflates the balance dollar-for-dollar.

- Every 1099, entered once. Imported and manually-entered copies of the same 1099 double the income silently.

- Cost basis on every stock or crypto sale. If basis imported as zero, the software taxed the entire sale proceeds as gain — a classic cause of wildly inflated balances.

- Credits and adjustments you skipped in a hurry — retirement contributions, student loan interest, education credits.

If you find a genuine error, a corrected return can shrink the debt and the penalties tied to it — here's how amending a return to lower a tax debt works, and why you shouldn't wait for the amendment to process before handling the part you clearly owe.

A $48,300 surprise, by the numbers

Say you're a single W-2 employee and the return you just filed shows $48,300 due — a big RSU vest withheld at the flat 22% while your marginal rate was 35%, plus a stock sale with nothing prepaid. This is clearly hypothetical, but the math is exact:

- Failure-to-pay penalty: 0.5% × $48,300 = about $241 every month, capping eventually at 25% of the balance.

- Interest: compounds daily at the federal underpayment rate on the tax and the penalty. On a balance this size, the combined monthly drift runs well into the hundreds — you can estimate your own growth with our Penalty & Interest Calculator.

- Short-term plan (180 days, $0 setup): paying it off in six months means roughly $8,050/month plus accruals — realistic only if a bonus or sale proceeds are coming.

- 72-month installment agreement: $48,300 ÷ 72 ≈ $671/month as a baseline. With direct debit and an on-time-filed return, the failure-to-pay penalty drops to 0.25% per month while the plan is active, so a payment that actually retires the debt in 72 months lands closer to $800/month once interest is counted.

One more number matters at this balance: $50,000 is the ceiling for setting up a long-term plan online without financial disclosure. At $48,300, roughly $500+ of monthly growth means the balance can cross that line within a few months of drifting. Act while you're under it, and the whole setup is a same-day online task.

What happens if you ignore the balance

An unpaid balance due starts a fully automated IRS notice sequence that runs from a simple bill to a levy-empowered final notice. No human decides to escalate your file — the system does, in this order:

- CP14 — the first bill. It arrives weeks after your return processes and typically gives about 21 days. Everything is still cheap to fix here — see the CP14 notice guide.

- CP501 / CP503 — reminders. Still just bills, but each one arrives with a bigger balance attached as penalties and interest compound.

- CP504 — intent to levy. The IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien becomes a live possibility. The CP504 notice guide covers what it does and doesn't authorize.

- LT11 / Letter 1058 — final notice. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After it runs, wage garnishment and bank levies are on the table — details in the LT11 notice guide.

Two 2026-specific realities sharpen this. First, the IRS workforce shrank about 27% in 2025 — humans are harder to reach, but the automated notices, liens, and levies never paused. Second, a balance left to grow for years, stacked with a repeat next April, can approach the $66,000 seriously-delinquent threshold at which the IRS can certify your debt to the State Department and block passport renewal.

Staring at a five-figure balance you didn't see coming?

A $48,300 surprise grows by roughly $241 in penalty alone every month it sits — before interest. Get a free review of your return and your realistic options from an experienced tax professional before the first IRS bill even arrives: call (888) 825-7779 or use the 2-minute form.

Your options when you can't pay it all at once

The IRS offers five real alternatives to paying a surprise balance in one lump sum, and eligibility for each is set by hard numbers, not negotiation skill. The full DIY playbook lives in our guide to how to settle tax debt yourself; here's how each option applies to a filed-and-owe balance:

| Option | Who it fits | Cost & catch |

|---|---|---|

| Short-term payment plan | You can pay in full within 180 days | $0 setup; penalties and interest continue until paid |

| Guaranteed installment agreement | Balance $10,000 or less, returns filed and paid on time for 5 years | Approval is required by law if criteria are met; up to 3 years to pay |

| Streamlined installment agreement | Combined balance $50,000 or less; up to 72 months | Online setup, no financial disclosure; direct debit expected over $25,000 — see the streamlined installment agreement guide |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses | Collection pauses; the debt, interest, and penalties remain and the IRS reviews your income |

| Offer in Compromise | Income and assets genuinely can't cover the debt before the collection statute expires | $205 fee + 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance history for the prior 3 years | Removes the failure-to-pay penalty; from summer 2026, Automatic Exemption from Penalty (AEP) applies without a request — see first-time penalty abatement |

Two honest notes. An Offer in Compromise rarely fits a W-2 employee with steady income and a sub-$50,000 balance — the IRS's math usually shows it can collect in full through a plan, and no one can promise otherwise. And Currently Not Collectible is a hardship pause, not forgiveness: the balance keeps growing while collection sleeps.

How much you owe changes your realistic options

Your total assessed balance — not your income — determines which IRS arrangements you can set up online versus which require financial disclosure. This is why acting before penalties push you into the next band matters:

| Balance band | Realistic options | Watch out for |

|---|---|---|

| Under $10,000 | Pay in full, 180-day plan, or guaranteed installment agreement | Even here, the 0.5%/month penalty makes drifting expensive |

| $10,000 – $25,000 | Streamlined plan online, any payment method, up to 72 months | Refunds in future years are offset to the balance until it's gone |

| $25,000 – $50,000 | Streamlined plan online with direct debit, up to 72 months | Accruals can push you over $50,000 and off the online path — a $48,300 balance is months from the line |

| Over $50,000 | Installment agreement with Form 433 financial disclosure; possibly partial-pay or OIC | Lien filing becomes more likely; see I owe the IRS $50,000 for what changes |

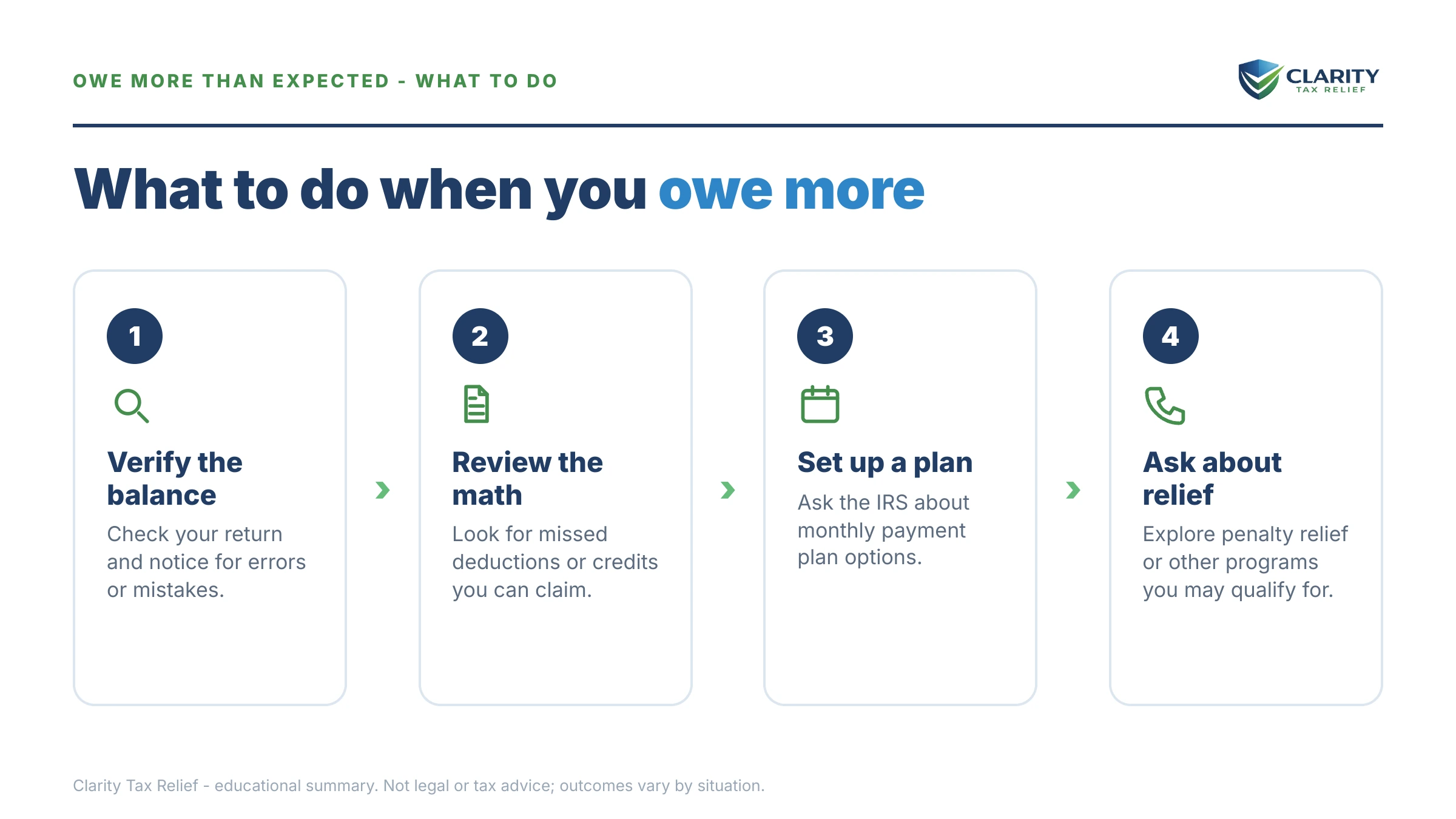

How to respond, step by step

- Verify the number. Compare every W-2 and 1099 against what's on the return, confirm stock sales include cost basis, and check your IRS online account once the return posts.

- Pay whatever you can today. Every dollar paid at IRS.gov/payments shrinks the base that the 0.5% monthly penalty and daily interest grow from.

- Set up an arrangement before the first bill arrives. At $50,000 or less, you can apply online for a payment plan the same day — you don't have to wait for a CP14.

- Request penalty relief. If your prior three years are clean, ask about First-Time Penalty Abatement — and note that automatic exemption (AEP) begins rolling out in summer 2026.

- Fix your withholding. File a new Form W-4 with your employer now so next April doesn't repeat this one.

Stop it from happening again next April

A new Form W-4 filed with your employer is the single change that prevents next year's surprise bill, and it takes effect within a pay cycle or two. Run your numbers through the IRS Tax Withholding Estimator; if bonuses or RSUs caused the gap, the cleanest fix is a flat extra-withholding amount on W-4 line 4(c) rather than fiddling with dependents and adjustments. If side income drove the balance, quarterly estimated payments — not withholding tweaks — are the right tool, since no employer withholds on 1099 money.

And if this year's balance is still unresolved when next year's return comes due, file it anyway: the failure-to-file penalty is 5% per month, ten times the failure-to-pay rate, and an unfiled year forfeits your penalty-relief eligibility going forward.

When you can handle this yourself — and when help changes the outcome

You can handle a surprise balance yourself when you agree with the number and can pay it within 72 months. If the return is right, the balance is under $50,000, and a monthly payment fits your budget, the online payment-plan application plus a penalty-abatement request is a genuinely DIY project — plan details are on the IRS payment plans page.

Experienced help changes the outcome in a narrower set of situations: the balance is wrong and needs an amendment coordinated with a payment arrangement; penalties and interest are about to push you past the $50,000 online threshold; you have prior unfiled years that block relief; the payment the IRS would ask for genuinely doesn't fit your budget (where partial-pay agreements and hardship status require careful financial presentation); or the debt spans multiple years. In those cases, the order you fix things — returns first, then penalties, then the balance — often changes the total you pay by thousands.

Owing more than expected: your questions, answered

Why do I owe so much in taxes this year when nothing changed?

Usually something did change — in your income mix, not your paycheck. Bonuses and vested RSUs are withheld at a flat 22% even when the money lands in a 32% or 35% bracket, and stock sales, crypto gains, and side income carry no withholding at all. A second job can also cause it, because each employer withholds as if its paycheck were your only income.

Do I have to pay the full amount right away if I already filed?

No — but the balance was legally due on the April filing deadline, so it is already accruing a 0.5% monthly failure-to-pay penalty plus daily-compounding interest. You can take up to 180 days with a short-term payment plan ($0 setup) or spread balances of $50,000 or less over up to 72 months with an online installment agreement. Filing on time already saved you the far larger failure-to-file penalty.

What happens if I file my taxes but don't pay what I owe?

Filing without paying starts the automated collection sequence: a CP14 bill first, then CP501/CP503 reminders, then a CP504 intent-to-levy notice, then an LT11 final notice that permits wage garnishment and bank levies after 30 days. Because you filed, the penalty is only 0.5% per month instead of 5% — a tenth of what non-filers pay — but interest compounds daily the entire time.

Can I get a payment plan if I owe the IRS more than $25,000?

Yes. Individuals owing $50,000 or less in combined tax, penalties, and interest can set up a long-term installment agreement online for up to 72 months; between $25,000 and $50,000, the IRS generally expects direct-debit payments. Above $50,000 a plan is still available, but you'll typically need to submit financial disclosure on a Form 433 series statement — one reason not to let a $48,300 balance grow past the line.

Will the IRS settle my tax bill for less than I owe?

Only through an Offer in Compromise, and only when your income and assets genuinely can't cover the debt before the collection statute runs out — the IRS accepted roughly 1 in 5 offers in FY2024. A W-2 employee with steady income and a balance under $50,000 usually shows enough collection potential that a payment plan, not a settlement, is the realistic outcome. Penalty abatement is often the more achievable reduction.

Should I amend my return if the balance looks wrong?

Amend only if you find a genuine error — a mistyped W-2 Box 2, a duplicated 1099, a missed deduction or credit, or stock sales reported without cost basis. File Form 1040-X with documentation, but don't wait for it to process before arranging payment on the part you clearly owe, because penalties and interest accrue on the unpaid balance the whole time. If the amendment is accepted, the IRS adjusts the balance and the related penalties down.

How do I make sure I don't owe again next year?

File a new Form W-4 with your employer now — the fix takes effect within a pay cycle or two. Use the IRS Tax Withholding Estimator, and if bonuses or RSUs caused the gap, add a flat extra dollar amount on W-4 line 4(c) rather than adjusting allowances. If side income is the cause, quarterly estimated payments are the tool; withholding changes alone rarely cover untaxed 1099 income.

Your next 24 hours

- Pull the exact figure. Open your filed return and write down the balance due and the tax year — that's the number every option below is built on.

- Gather three things: the return itself, every W-2 and 1099 behind it, and a realistic monthly amount your budget can carry.

- Get a free case review. Penalties and interest are compounding on the balance right now, and the first IRS bill hasn't printed yet — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your cheapest path while you still have the head start.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.