Tax Debt by Amount

I Owe the IRS $50,000: What to Do in 2026 (Every Real Option)

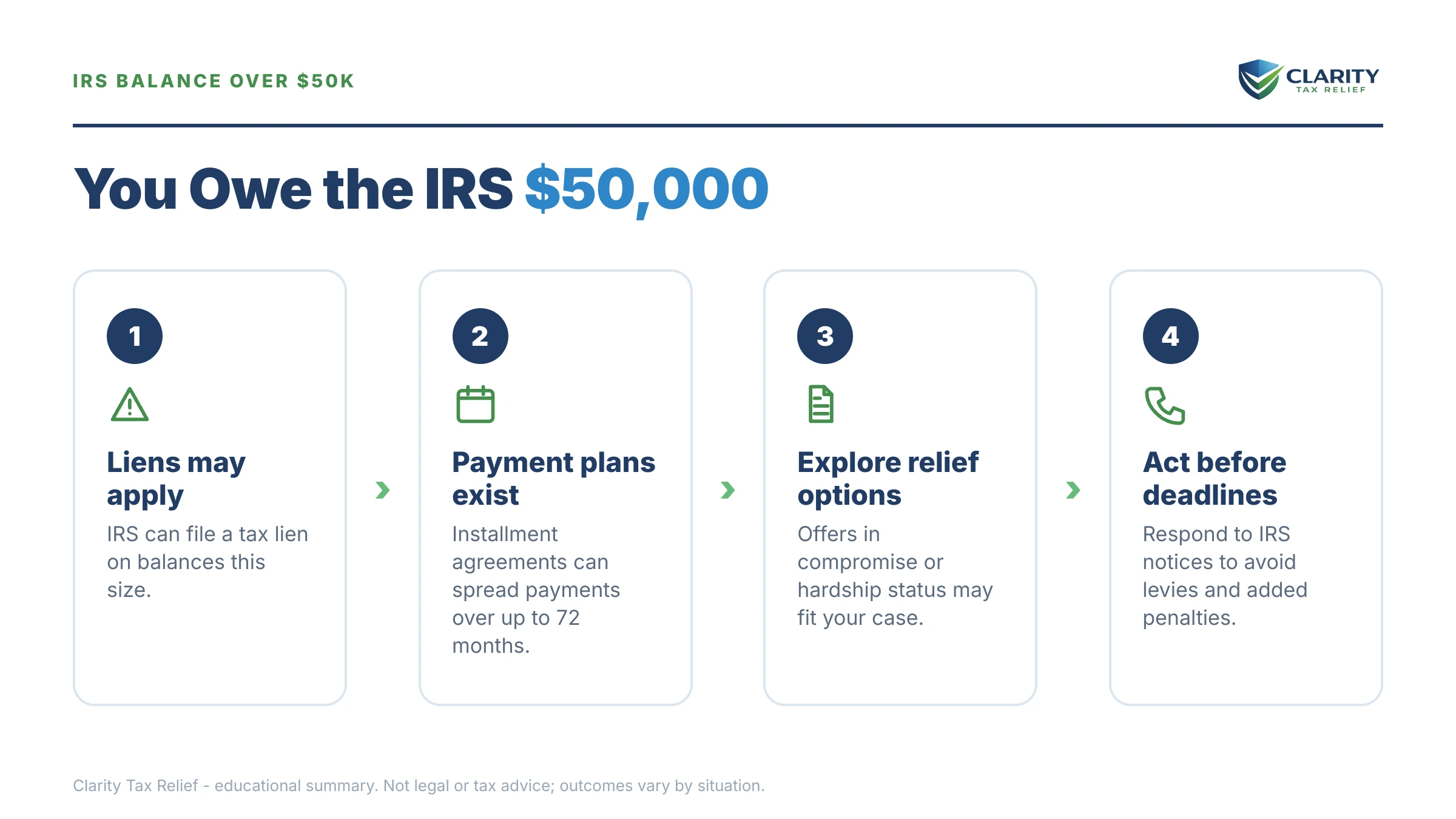

The short answer: if you owe the IRS $50,000, you're sitting exactly at the cutoff for a streamlined online payment plan — up to 72 months, without a full financial statement. Let penalties and interest push the balance past $50,000 and that door closes. Act now: set up an agreement, request penalty relief, or document hardship.

Maybe it started with a retirement-account withdrawal that carried a bigger tax bill than anyone warned you about, and a few years of penalties did the rest. Now your IRS account reads $50,000, and on a fixed income that number feels like a wall. It isn't — but $50,000 is the single most deadline-sensitive amount in the IRS system, because it sits directly on the line that separates the simple resolution paths from the complicated ones.

⏱ Your real clock: there's no letter deadline printed on a balance itself, but two lines are approaching. Penalties and interest grow the debt every month — and once your balance passes $50,000, you lose access to the streamlined online payment plan. Keep drifting and at $66,000 (the 2026 threshold) the IRS can certify the debt for passport denial.

Why $50,000 is a threshold, not just a big number

A $50,000 assessed balance is the maximum the IRS allows for a long-term online payment plan of up to 72 months. At $50,000 even, you can still resolve this from your kitchen table without handing the IRS a financial statement. At $50,001, the rules change: you're into irs payment plan over 50000 territory, where the IRS can demand a full Form 433-F disclosure of your income, expenses, accounts, and assets before agreeing to anything.

That's why the timing on this page matters more than on almost any other balance. The threshold is measured against what you owe today — tax, penalties, and interest combined — not what the original bill said. A debt that was $46,000 when the first notice arrived can cross $50,000 while you're deciding what to do.

Here's how your options shift at each balance level, and where $50,000 sits:

| Balance owed | Simplest available path | What changes at this level |

|---|---|---|

| Up to $10,000 | Guaranteed installment agreement | The IRS must generally accept a qualifying plan — the lowest-friction band |

| $10,001–$25,000 | Streamlined agreement, no financial statement | Online setup, up to 72 months; see I owe the IRS $20,000 |

| $25,001–$50,000 (you are here) | Streamlined agreement with direct debit | Still up to 72 months online, but direct-debit payments are generally required at this band |

| $50,001–$65,999 | Non-streamlined agreement with Form 433-F | Financial disclosure required; the IRS reviews your assets before agreeing |

| $66,000+ | Agreement plus passport-risk management | Eligible for "seriously delinquent" passport certification in 2026 |

| $100,000+ | Managed resolution, often with a revenue officer | Asset review and active enforcement — see I owe the IRS $100,000 |

Where a $50,000 balance usually comes from

Most $50,000 IRS debts are built in layers, not in one bad year. A common pattern: a lump-sum event — a 401(k) or IRA distribution, a home sale, a pension payout with too little withheld — creates a tax bill in the low-$30,000s, and then the failure-to-pay penalty and daily-compounding interest add the rest over two or three years.

The other common builders are two or three years of self-employment income without estimated payments, or a CP2000 underreporter adjustment stacked on an existing balance. Knowing which tax years make up your $50,000 matters, because penalty relief and the 10-year collection statute run separately for each year.

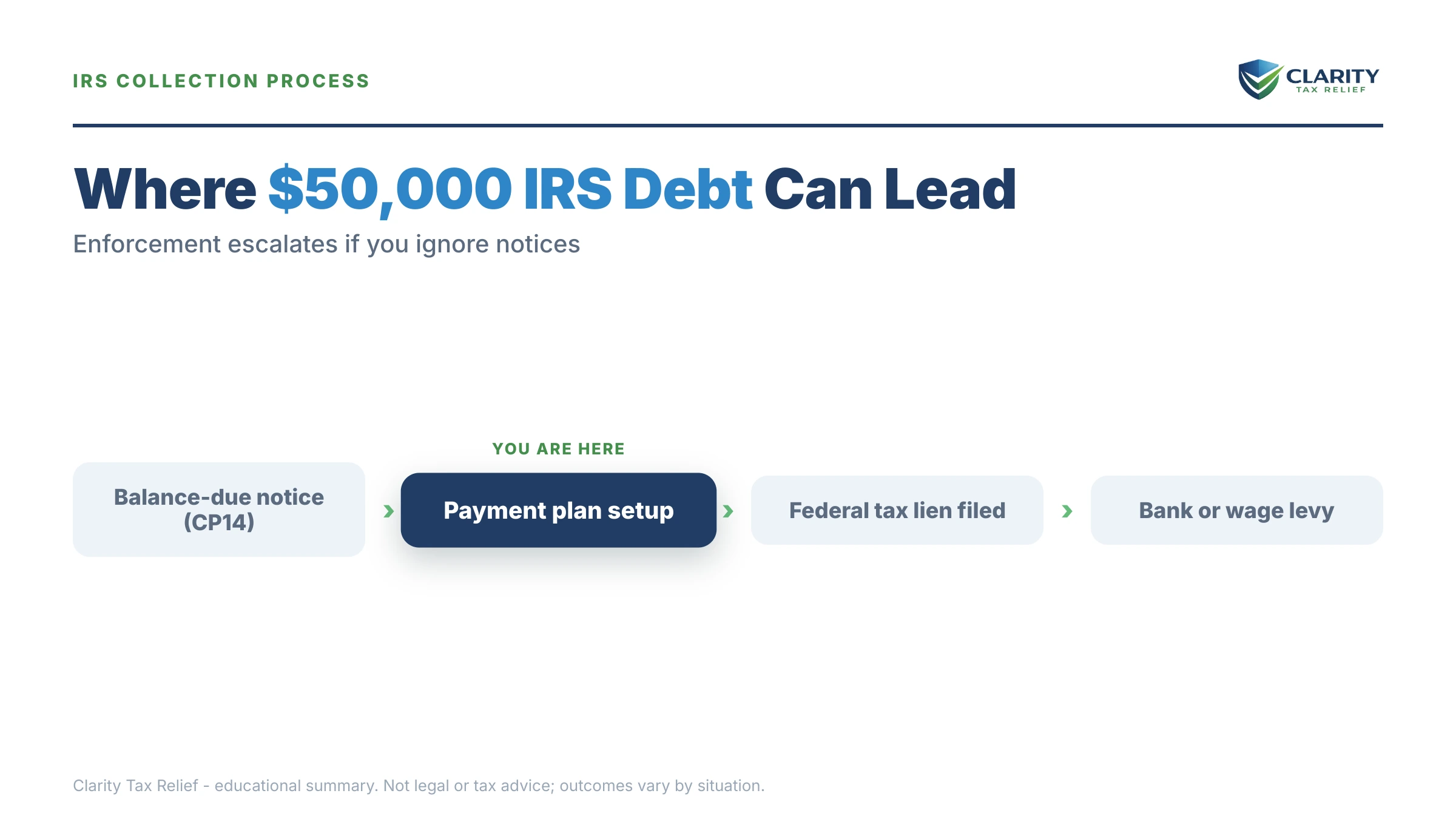

What happens if you ignore a $50,000 IRS debt

An unpaid $50,000 balance moves through an automated notice sequence that ends in levies — and in 2026, staffing cuts have made humans harder to reach while the automated escalation runs exactly on schedule. The stages, in order:

- CP14 — the first bill. Typically about 21 days to respond before the reminder cycle begins. No enforcement yet, but the balance is already accruing.

- CP501 and CP503 — reminders. Still just bills. Each one arrives with more penalty and interest attached.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a Notice of Federal Tax Lien becomes a realistic risk at this balance.

- LT11 or Letter 1058 — final notice of intent to levy. This starts a 30-day clock and your Collection Due Process rights. After it runs, levies are authorized.

- Enforcement. Bank levies (a 21-day hold before funds leave), continuous wage levies, and — critical for retirees — up to 15% of Social Security through the Federal Payment Levy Program. If you're on benefits, read can the IRS garnish Social Security before assuming you're protected.

Even in quiet stretches, a CP71 annual reminder arrives every year the balance stands, and refunds are offset until it's paid. Meanwhile the accruals do the IRS's work for it: at 0.5% per month, the failure-to-pay penalty alone adds about $250 a month on a $50,000 balance (until it caps at 25% of the tax), with interest compounding daily on top. That's the engine that pushes $50,000 past the streamlined line — and eventually toward the $66,000 passport threshold covered in passport revoked for tax debt.

Owe the IRS around $50,000 right now?

Your balance is growing every month, and once it crosses $50,000 the simplest resolution path closes. Get a free case review before the accruals decide for you — an experienced tax professional will map your exact options in one call.

Your options when you owe the IRS $50,000

Five real IRS programs can resolve a $50,000 balance, and which one fits is decided by your income and assets — not by marketing. The mechanics of each program are covered in our DIY hub, how to settle tax debt yourself; here's how they compare at exactly this balance:

| Option | Upfront cost | Who it fits at $50,000 |

|---|---|---|

| Short-term plan (up to 180 days) | $0 setup | Only if you can raise the full $50,000 within six months — rare at this balance, but it stops the notice sequence immediately |

| Streamlined installment agreement | Setup fee (reduced online and with direct debit; waived for qualifying low income) | Up to 72 months, no financial statement, available only while the balance is at or below $50,000 — usually with direct debit at this band |

| Partial-pay installment agreement | Setup fee plus financial disclosure | You can pay something, but not enough to retire $50,000 before the collection statute runs; the IRS reviews your finances periodically |

| Currently Not Collectible (CNC) | $0, but requires financial disclosure | Income barely covers IRS-allowed living expenses — common on fixed incomes; collection pauses while the debt (and interest) remains |

| Offer in Compromise | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Assets and future income genuinely can't cover $50,000; the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty abatement | $0 | Clean compliance for the prior 3 years (first-time abatement), or reasonable cause like serious illness — can remove thousands before you finance the rest |

Two honest notes on this list. First, penalty abatement should almost always come before the payment plan — removing a failure-to-pay penalty first means you finance a smaller number. Starting in summer 2026, the new Automatic Exemption from Penalty (AEP) applies some of this relief automatically, so check your account before assuming you must request it. Second, if you have home equity or retirement savings, compare borrowing costs against IRS accruals: a lower-rate loan that pays the IRS in full sometimes beats six years of interest and setup on a plan. Run your own accrual math with our IRS penalty & interest calculator to see what waiting actually costs.

A worked example: $50,000 owed on Social Security income

Say you're 70, retired, with $2,350 a month in Social Security and a $700 pension — $3,050 total — and a $50,000 balance left over from taxes on a retirement-account withdrawal. This is hypothetical, but the math is real:

- Do nothing: the failure-to-pay penalty adds about $250 a month (0.5% of $50,000) until it caps, plus daily-compounding interest. Worse, the Federal Payment Levy Program can take 15% of your Social Security — about $352 of your $2,350 benefit, every month, until the debt is resolved.

- The 72-month plan: $50,000 ÷ 72 ≈ $695 a month for principal alone; the IRS sets the actual payment high enough to cover accruals too (the late-payment penalty drops to 0.25% per month on an active plan). On $3,050 of income, that payment probably fails the affordability test.

- Currently Not Collectible: if IRS allowable-expense standards show your necessary living costs consume essentially all $3,050, you're a CNC candidate — no levy, no Social Security offset through FPLP, while the 10-year collection clock keeps running. See IRS hardship on Social Security for how fixed-income CNC cases are documented.

- Offer in Compromise: the IRS totals your reachable asset equity plus a multiple of monthly disposable income. If you have, say, $100 a month of disposable income ($1,200 over a lump-sum offer's 12-month multiplier) and $9,000 in non-exempt equity, the math points to an offer around $10,200 — but significant home equity can push that figure above $50,000 and end the analysis. At this income level, low-income certification (AGI at or below 250% of the poverty level) would waive the $205 fee, the 20% down payment, and payments during review.

The takeaway: on a fixed income, the "right" answer is usually CNC or an offer — not the payment plan the IRS website steers you toward. On a working income, the streamlined plan is usually the fastest, cheapest protection. Same $50,000, opposite answers.

How to respond to a $50,000 IRS balance, step by step

- Pull your exact balance. Log into your IRS online account and write down the assessed balance plus accrued penalties and interest for each tax year — the payment-plan threshold is measured against what you actually owe today, not what the debt started as.

- File any unfiled returns. The IRS will not approve any agreement while required returns are missing, and unfiled years hide the true total you are negotiating around.

- Choose your path with the numbers. If you can afford roughly $700–$850 a month, set up a 72-month plan online before accruals push the balance past $50,000; if you cannot, gather the figures for Currently Not Collectible status, a partial-pay agreement, or an Offer in Compromise.

- Request penalty relief. First-time abatement — or the Automatic Exemption from Penalty arriving in summer 2026 — can strip the failure-to-pay penalty from a qualifying year and shrink the balance you are financing.

- Get experienced help if a levy is moving or your income is fixed. A levy already in motion, multiple balance years, or Social Security income changes both the risks and the best order of operations — have an experienced tax professional review your file before you commit to a plan.

When you can handle this yourself

Plenty of people resolve a $50,000 balance without hiring anyone. You're a good DIY candidate if the debt is from one or two years you agree with, all your returns are filed, and you can genuinely afford the roughly $700+ monthly payment — the streamlined plan takes about 20 minutes to set up through the IRS payment plans page, and our DIY hub walks through every screen.

Experienced help changes outcomes in four specific situations: a levy or Social Security offset already in motion, multiple years with unfiled returns mixed in, a balance about to cross the $50,000 or $66,000 lines, and any case where CNC-versus-offer math decides the result — because how your income and expenses are documented on the financial statement is the whole case. If money is the obstacle, a Taxpayer Advocate Service case or a low-income taxpayer clinic may also be available at no cost.

What your IRS transcript shows when you owe $50,000

Your account transcript is the source document behind the notices — it shows exactly how the $50,000 was built, year by year. These are the codes you'll most likely see on a balance-due account:

| Code | What it means | What to do |

|---|---|---|

| 150 | Tax assessed from a filed return (or an IRS-prepared substitute) | Confirm the assessed amount matches the return you actually filed for each year |

| 196 | Interest charged to the account | Track how much of your $50,000 is interest — it compounds daily and can't usually be waived alone |

| 276 | Failure-to-pay penalty posted | Prime abatement target — check first-time abatement or AEP eligibility for that year |

| 971 | A notice was issued | Match each 971 date to the letter in your stack so you know where you are in the sequence |

| 582 | Lien indicator on the account | A Notice of Federal Tax Lien is in play — resolve or appeal before selling or refinancing anything |

Terms you'll keep seeing, decoded

- Streamlined installment agreement: a payment plan approved without a financial statement — available only while your balance is at or below $50,000.

- CSED: the Collection Statute Expiration Date — generally 10 years after each assessment, though appeals, offers, and bankruptcy pause the clock.

- Currently Not Collectible (CNC): a hardship status that pauses levies and garnishment while the debt continues to exist and accrue interest.

- Reasonable Collection Potential (RCP): the IRS's formula — asset equity plus future disposable income — that decides whether an Offer in Compromise gets accepted.

- FPLP: the Federal Payment Levy Program, which lets the IRS take up to 15% of federal payments, including Social Security benefits.

- Notice of Federal Tax Lien (NFTL): a public filing that attaches the government's claim to everything you own; different from a levy, which actually takes property.

If your finances point toward an offer rather than a plan, the IRS's own program page at Offer in Compromise includes a pre-qualifier worth running before you spend anything.

Owe the IRS $50,000? Your questions, answered

Can I get an IRS payment plan if I owe exactly $50,000?

Yes — $50,000 is the top of the online long-term payment plan range, so you can still set up an agreement of up to 72 months through your IRS online account. If penalties and interest push your assessed balance even one dollar past $50,000, the online streamlined path closes and the IRS can require a Form 433-F financial statement. Paying the balance down below the line before applying restores the simpler route.

What is the monthly payment on $50,000 owed to the IRS?

Roughly $695 per month covers the principal alone over the maximum 72 months; the IRS sets the actual payment high enough to also cover interest and the reduced late-payment penalty, so plan on somewhat more. You can propose a shorter payoff to cut total interest. If that payment is genuinely unaffordable, a partial-pay agreement or Currently Not Collectible status may fit instead — both require financial disclosure.

Will the IRS settle a $50,000 debt for less than I owe?

Only if your finances qualify — an Offer in Compromise is accepted when the IRS concludes your assets and future income cannot cover the $50,000, and it accepted roughly 1 in 5 offers in FY2024. The application costs $205 plus a 20% down payment on lump-sum offers, both waived if your income is at or below 250% of the federal poverty level. Anyone promising a settlement before reviewing your finances is selling, not advising.

Can the IRS take my Social Security for a $50,000 tax debt?

Yes — through the Federal Payment Levy Program the IRS can take up to 15% of your monthly Social Security benefit, and the levy continues until the debt is resolved. On a $2,350 benefit that is about $352 a month. You get warning first, typically a CP91 notice, and setting up an agreement or proving hardship stops or prevents it. SSI is not subject to this levy program.

Will the IRS file a tax lien if I owe $50,000?

It can, and at this balance a Notice of Federal Tax Lien is a realistic risk once notices go unanswered. A lien attaches to everything you own, including your home, and complicates selling or refinancing. Setting up a direct-debit streamlined agreement at or below $50,000 is the standard way to reduce the chance of a lien filing — one more reason to act while your balance is still at the line.

Can I lose my passport over $50,000 in tax debt?

Not at $50,000 — the 2026 threshold for passport certification is $66,000 in seriously delinquent tax debt. But that threshold includes penalties and interest, and an ignored $50,000 balance grows toward it every month. Once certified, the State Department can deny your passport application or renewal. Getting into a payment plan or other agreement generally prevents certification even if the balance later crosses the line.

Does a $50,000 IRS debt expire?

Eventually — the IRS generally has 10 years from the date each tax was assessed to collect (the CSED). But the clock pauses during bankruptcy, a pending Offer in Compromise, collection appeals, and certain other events, so the real expiration date is often later than year ten. Waiting out the statute means living under lien and levy risk the whole time, which is rarely a workable plan on $50,000.

What if I owe the IRS $50,000 and can't pay anything at all?

Ask for Currently Not Collectible status — if IRS allowable-expense standards show your income barely covers necessities, collection pauses: no levies, no garnishment. The debt does not disappear and interest keeps accruing, but the 10-year collection clock keeps running while you are protected. The IRS reviews CNC periodically and can reactivate collection if your income rises, so treat it as shelter, not a settlement.

Your next 24 hours

- Find your exact number. Log into your IRS online account and write down the assessed balance, penalties, and interest for each year — and note which side of the $50,000 line you're on today.

- Gather three things: your most recent tax return, proof of monthly income (pay stubs, Social Security award letter, pension statements), and a rough list of your monthly living expenses. Every option on this page is decided by those numbers.

- Get your $50,000 balance reviewed free — call (888) 825-7779 or use the 2-minute form. Interest and penalties are compounding while the streamlined window is still open; one call maps which program actually fits your finances.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.