Tax Debt by Amount

I Owe the IRS $75,000: What to Do in 2026

The short answer: if you owe the IRS $75,000, you've crossed two lines that change your options: the $50,000 cutoff for streamlined online payment plans and the $66,000 passport-certification threshold for 2026. You can still resolve it — through a financially verified installment agreement, hardship status, or an Offer in Compromise — but financial disclosure is now part of the deal.

You don't own a house the IRS can put a lien against and slowly wait out — which means at $75,000, its leverage lands somewhere far more immediate: your paycheck and your checking account. If a levy warning is already sitting on your kitchen counter, you're reading this at the exact moment the sequence can still be redirected.

Here's the honest version of your map: what $75,000 specifically triggers, what the enforcement sequence looks like if you wait, the real monthly numbers behind each option, and the order to do things in so you don't pay more than you have to.

⏱ Two clocks are already running. Interest plus a 0.5%-per-month late-payment penalty accrue on the full $75,000 every month it sits unresolved. And because your balance exceeds the $66,000 threshold for 2026, the IRS can certify your debt to the State Department at any time — blocking new passports and renewals — with no separate warning deadline you control.

Why owing the IRS $75,000 is different from owing $40,000

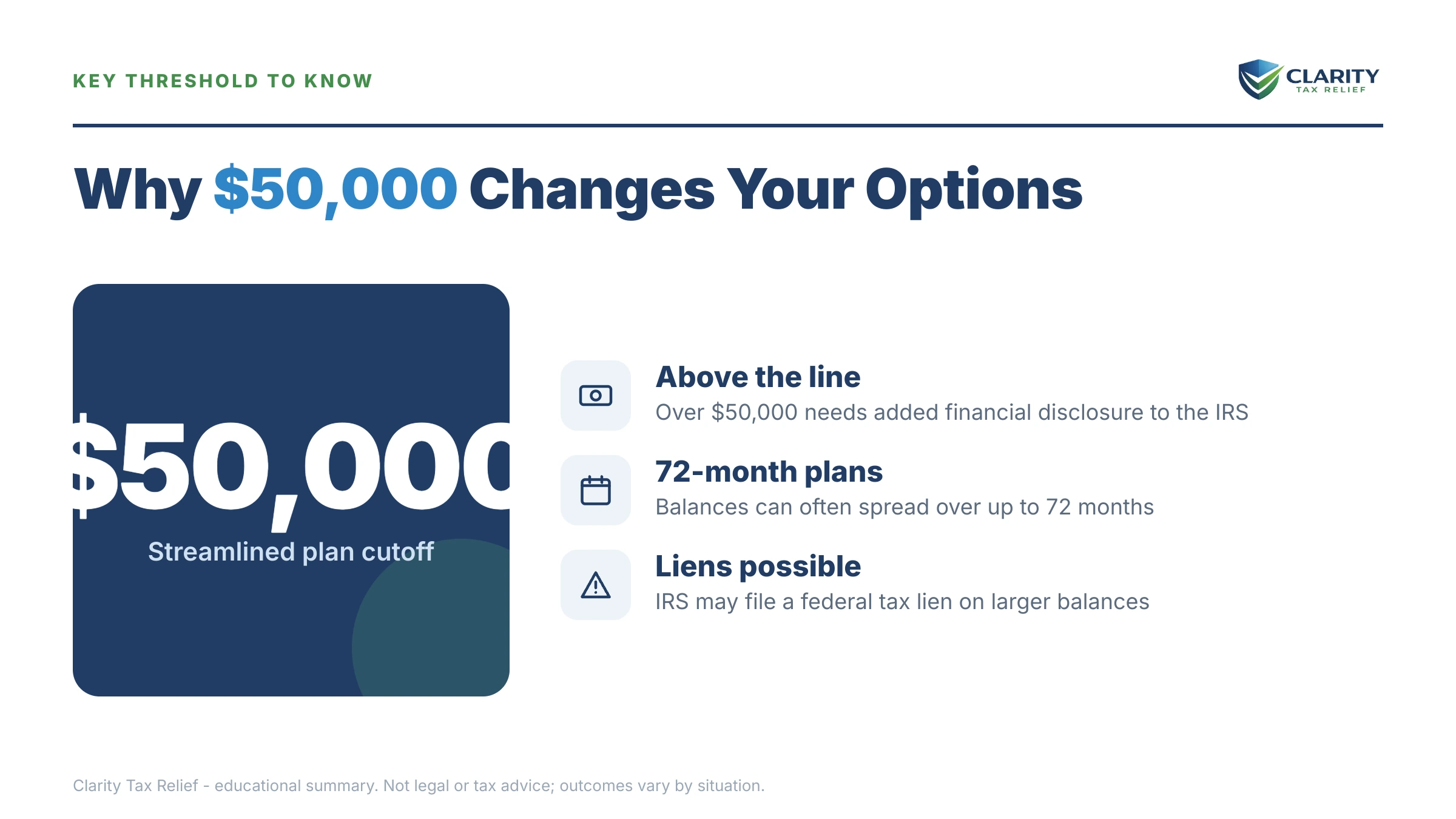

A $75,000 IRS balance sits above both the $50,000 online payment-plan cutoff and the $66,000 passport-certification threshold — the two lines that most change how the IRS treats you. Below $50,000, you can click through a 72-month plan online in twenty minutes with no questions asked. At $75,000, that door is closed: you're in irs payment plan over 50000 territory, where the IRS generally wants a financial statement before it agrees to anything long-term.

The second line matters even if you never travel. Above $66,000 (the 2026 inflation-adjusted figure), your debt meets the definition of "seriously delinquent," and the IRS can certify it to the State Department under the rules covered in our guide to passport revoked tax debt. Certification is generally blocked while you're in a pending or approved agreement — one more reason the arrangement itself is the protection.

Here's exactly where $75,000 lands against every threshold that matters:

| Balance line | What it triggers | Where $75,000 stands |

|---|---|---|

| $10,000 or less | Guaranteed installment agreement — IRS must accept a qualifying plan | Crossed — not available |

| $25,000 or less | Streamlined agreement with minimal paperwork | Crossed — not available |

| $50,000 or less | Online long-term plan up to 72 months, no financial statement | Crossed — unless you pay the balance down first |

| $66,000+ (2026) | Passport certification as "seriously delinquent tax debt" | You're over it — certification risk is live |

| $100,000+ | Higher odds of assignment to a revenue officer; 10-business-day pay windows on first bills | Not crossed — keep it that way; accruals push balances up fast |

What happens if you ignore a $75,000 IRS debt

Ignoring a $75,000 balance ends in a wage or bank levy — and the sequence that gets there is automated, so it runs whether or not a human ever reviews your file. IRS staffing fell roughly 27% in 2025, which makes the agency harder to reach by phone, but the notice-and-levy machine never stopped. The stages arrive in this order:

- The bill and reminders (CP14, then CP501/CP503). No enforcement yet — but the 0.5% monthly penalty and daily-compounding interest are already growing the balance.

- CP504 — intent to levy your state refund. The IRS can now seize your state tax refund under IRC §6331(d). This is not the final notice, but it's the last cheap exit.

- CP508C — passport certification. Because you're above $66,000, this can arrive at any point in the sequence, cutting off passport issuance and renewal.

- Notice of Federal Tax Lien. A public-record claim against everything you own or later acquire. As a renter you may not feel it today — you will when you apply for a mortgage or financing.

- LT11 or Letter 1058 — final notice of intent to levy. This starts a hard 30-day clock and your Collection Due Process rights (requested on Form 12153). Our lt11 notice guide covers exactly how to answer it.

- The levy itself. A bank levy freezes funds for 21 days before the money leaves — the window explained in irs bank levy 21 days. A wage levy is worse: it's continuous, hitting every paycheck until released.

Notice what's missing from that list: nothing in it reduces what you owe. Every stage only adds cost. The balance is at its smallest today.

Owe $75,000 and a levy notice is in the mail?

If an LT11 or Letter 1058 has arrived, a real 30-day appeal window is running — and at $75,000 your passport is already exposed. Get your notices and options reviewed free by an experienced tax professional before that window closes. No pressure, no obligation.

Your options when you owe the IRS $75,000

The IRS has six realistic resolution tracks for a $75,000 balance, and one worksheet — Form 433-F — decides which ones you can get. (For the general mechanics of dealing with the IRS on your own, our pillar on how to settle tax debt yourself covers the shared ground; everything below is specific to a balance this size.)

- Short-term plan (up to 180 days). $0 setup fee, no financial disclosure. Only realistic if money is genuinely coming — a bonus, a settlement, a sale — because the full $75,000 plus accruals is due within the window.

- Pay down below $50,000, then go streamlined. Pay $25,001 or more, and the remaining balance qualifies for an online 72-month plan with no financial statement (direct debit required at the upper end). This is the single most-used move at your amount — the rules on the other side of that line are covered in i owe the irs 50000.

- Non-streamlined installment agreement. The default track at $75,000: you submit income, expenses, and assets on form 433-f instructions, and the IRS sets a payment from what's left after its allowable-expense standards. Interest and penalties continue while you pay.

- Partial-payment installment agreement (PPIA). If the 433-F math shows you can't full-pay $75,000 before the 10-year collection statute runs out, a partial payment installment agreement lets you pay what you actually can — and whatever remains at the CSED can expire uncollected. Expect periodic financial reviews.

- Currently Not Collectible. If paying anything would leave you unable to cover rent, food, and utilities, irs currently not collectible status pauses levies entirely. The debt remains, interest grows, refunds get offset, and a lien is likely — but enforcement stops while you recover.

- Offer in Compromise. Settling $75,000 for less is real but strictly means-tested. The IRS computes your Reasonable Collection Potential — asset equity plus a multiple of your monthly disposable income — and accepts only when that number is genuinely below the debt. It accepted roughly 1 in 5 offers in FY2024. The fee is $205 plus 20% down on lump-sum offers, both waived with low-income certification (AGI at or below 250% of the poverty level), and an offer is auto-accepted if the IRS doesn't decide within 2 years — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. You can estimate your own numbers with our Offer in Compromise Calculator, and how does an offer in compromise work walks the full process.

Two side doors worth checking before you commit to any track. First, penalty relief: if the prior three years were clean, first-time abatement can strip penalties from the oldest year — and starting summer 2026, the new Automatic Exemption from Penalty (AEP) applies that relief automatically, no request needed. Second, accuracy: if part of the $75,000 comes from an IRS adjustment you never contested, the balance itself may be reducible before you negotiate how to pay it.

| Option | Upfront cost | What you pay | Timeline |

|---|---|---|---|

| Short-term plan | $0 setup | Full balance + accruals within 180 days | Set up in days |

| Pay down + streamlined plan | $25,001+ lump sum; online setup fee (lowest with direct debit) | Roughly $695/mo on ~$50,000 over 72 months, plus ongoing accruals | Online same-day once under $50k |

| Non-streamlined agreement | Setup fee (reduced for direct debit; waived or refunded for low income) | ~$1,042+/mo to full-pay in 72 months; 433-F sets the real number | Weeks by phone or mail |

| Partial-pay agreement (PPIA) | Setup fee + full 433-F disclosure | Only what the math shows; remainder can expire at the CSED | Weeks to months; periodic reviews |

| Currently Not Collectible | $0 (433-F disclosure required) | $0/mo; balance keeps growing, refunds offset | Weeks; reviewed if income rises |

| Offer in Compromise | $205 fee + 20% of offer (lump sum) — both waived with low-income certification | Your Reasonable Collection Potential, not a percentage of the debt | Months to 2 years; auto-accepted if undecided at 2 years (narrow exceptions apply) |

The math on $75,000: a worked example

Say you owe $75,000 — about $59,000 in tax across two years plus $16,000 in penalties and interest. You rent, take home $5,400 a month, have $2,500 in savings and a car worth $4,000 more than its loan. A CP504 already arrived. Here's how the three main tracks price out (hypothetical — your allowable-expense math will differ):

- Full-pay agreement: $75,000 ÷ 72 months ≈ $1,042/month before the interest and 0.5% monthly penalty that keep accruing — realistically budget $1,150+. On $5,400 take-home with city rent, the 433-F math may not support it.

- Pay down + streamlined: if a 401(k) loan or family loan can produce $25,001, the remaining $49,999 fits a 72-month online plan at roughly $695/month — no financial disclosure, and the agreement blocks passport certification.

- Offer in Compromise: if IRS allowable expenses leave you $150/month of disposable income, a lump-sum offer prices at ($150 × 12) + $6,500 in asset equity = about $8,300. That's not a discount the IRS grants — it's what the formula produces when your finances genuinely can't reach $75,000. If your disposable income were $900/month instead, the same formula yields $17,300 — and the IRS would likely push you toward a payment plan instead.

Notice the spread: the "right" answer for the same $75,000 ranges from $8,300 to over $80,000 paid, entirely depending on your financial facts. That's why running the 433-F numbers before you call is the single highest-leverage hour you can spend.

How to respond when you owe the IRS $75,000, step by step

- Pull your real balance — log into your IRS online account and get the year-by-year breakdown of tax, penalties, and interest. The number in your head is usually stale — interest compounds daily.

- Protect your appeal rights if a levy notice arrived — if you received an LT11 or Letter 1058, file Form 12153 within 30 days of the notice date. That requests a Collection Due Process hearing and generally holds off the levy while your case is heard.

- File every missing return — the IRS will not approve an installment agreement or an Offer in Compromise while required returns are unfiled. Filing also stops the 5%-per-month failure-to-file penalty, which is 10 times the late-payment penalty — though in months where both penalties apply, the failure-to-file portion drops to 4.5% (5% combined).

- Run the Form 433-F math before you call — list income, IRS allowable expenses, and asset equity. That one worksheet tells you which track you're on: full-pay plan, pay-down to streamlined, partial-pay, hardship status, or an offer.

- Lock in the agreement and keep it alive — set up direct debit so a missed payment never defaults the plan, and fix your withholding or quarterly estimates — a new balance next April can void the whole agreement.

When you can handle $75,000 yourself — and when help changes the outcome

You can resolve a $75,000 debt on your own when the situation is simple: one or two filed years, you agree with the amounts, steady W-2 income, and the 433-F math clearly supports a monthly payment. Calling the IRS with your worksheet done — or paying below $50,000 and clicking through the online plan — requires patience, not a professional.

Experienced help earns its cost in specific situations: a levy already in motion or a 30-day final-notice clock running; multiple unfiled years that have to be reconstructed before anything else can happen; self-employment income where the IRS disputes your expense figures; a passport certification you need reversed on a deadline; or borderline OIC math, where how assets and income are presented can move the accepted number by thousands. At this balance, a positioning mistake costs more than the review that would have caught it.

Terms you'll hear at $75,000, decoded

- Streamlined installment agreement — the low-paperwork payment plan available only at $50,000 or below; the line you're currently above.

- Form 433-F — the Collection Information Statement listing your income, expenses, and assets; it's the document that decides your monthly payment.

- Reasonable Collection Potential (RCP) — the IRS's formula for the most it believes it can ever collect from you; the floor for any Offer in Compromise.

- PPIA — a partial-payment installment agreement: monthly payments sized to your budget, with any remainder potentially expiring at the collection deadline.

- CSED — the Collection Statute Expiration Date, generally 10 years from assessment, pausable by offers, appeals, and bankruptcy. Full detail in how long can the irs collect back taxes.

- Seriously delinquent tax debt (CP508C) — the passport-certification label applied above $66,000 in 2026; an active agreement generally prevents or reverses it.

Owe IRS $75,000: your questions, answered

Can the IRS garnish my paycheck if I owe $75,000?

Yes, but only after it sends a final notice of intent to levy (LT11 or Letter 1058) and 30 days pass without a response. A wage levy is continuous — it stays on every paycheck until the debt is resolved or the levy is released — while a bank levy holds funds for 21 days before they're sent to the IRS. Getting into any agreement, even a basic payment plan, generally stops new levies from starting.

Will I lose my passport if I owe the IRS $75,000?

You're exposed: $75,000 is above the $66,000 seriously-delinquent-debt threshold for 2026, so the IRS can certify your debt to the State Department, which can deny passport applications and renewals. Certification generally doesn't apply while you're in a pending or active installment agreement, Offer in Compromise, or Collection Due Process hearing — so getting into an arrangement is the practical way to prevent it or get it reversed.

Can I get an IRS payment plan for $75,000?

Yes, but not through the streamlined online system, which caps long-term plans at $50,000. At $75,000 you'll typically submit financial information on Form 433-F by phone or mail, and the IRS sets your payment based on income minus allowable expenses. The workaround many people use: pay the balance below $50,000 first, then set up a streamlined 72-month plan online with no financial disclosure.

Can I settle a $75,000 tax debt for less than I owe?

Possibly, through an Offer in Compromise — but it's means-tested, not automatic. The IRS accepts an offer only when your assets plus future income (your Reasonable Collection Potential) genuinely fall short of $75,000, and it accepted roughly 1 in 5 offers in FY2024. The application costs $205 plus 20% down on lump-sum offers, though low-income certification waives both.

Will the IRS file a tax lien on a $75,000 debt?

It's likely if the balance stays unresolved — a federal tax lien is common well below $75,000. Even as a renter, the lien attaches to everything you own now or acquire later, shows up in public records, and can complicate a future home purchase or business financing. Tax liens no longer appear on consumer credit reports, but lenders who search public records will still find them.

What monthly payment will the IRS want on $75,000?

It depends on your Form 433-F math: income minus IRS allowable living expenses. Full-paying $75,000 over 72 months runs roughly $1,042 a month before the interest and penalties that keep accruing — plan on more. If your budget genuinely can't support that number, a partial-payment installment agreement or Currently Not Collectible status may set the payment lower, or at zero.

Does a $75,000 IRS debt expire after 10 years?

The IRS generally has 10 years from assessment to collect — that's the CSED. But the clock pauses during an Offer in Compromise review, bankruptcy, certain appeals, and other events, so the real end date is often later than year ten. Waiting it out at $75,000 usually means living through liens and levies for a decade; the CSED matters most as leverage inside a partial-payment agreement.

Your next 24 hours

- Find your most recent IRS notice and check two things: the notice code in the top corner (an LT11 or Letter 1058 means a 30-day clock is running) and the current balance with accruals.

- Gather three items: your last filed return, every IRS letter you've received, and one month of pay stubs or income records — that's everything needed to run the 433-F math.

- Get the free case review. At $75,000 your passport exposure is live and the balance grows every month it waits — send us your notices at the 2-minute form or call (888) 825-7779 and an experienced tax professional will map which track your numbers actually support.

Primary sources: the IRS's official pages on payment plans and installment agreements and the Offer in Compromise program carry the current thresholds and forms. If the IRS system is causing you demonstrable hardship, the Taxpayer Advocate Service is an independent, free avenue inside the agency.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.