IRS Resolution Programs

How Does an Offer in Compromise Work in 2026? The Formula, the Costs, and the Real Odds

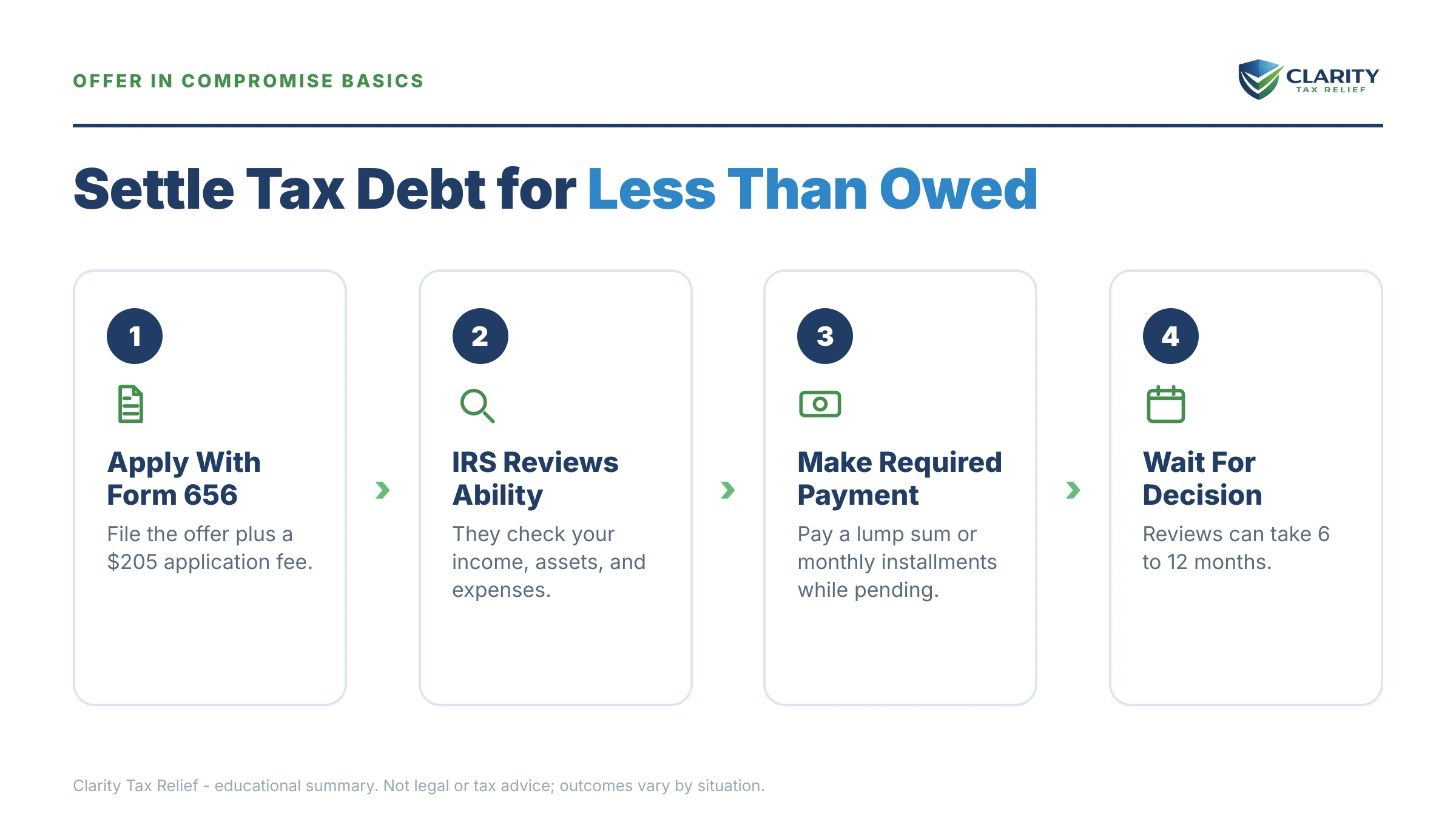

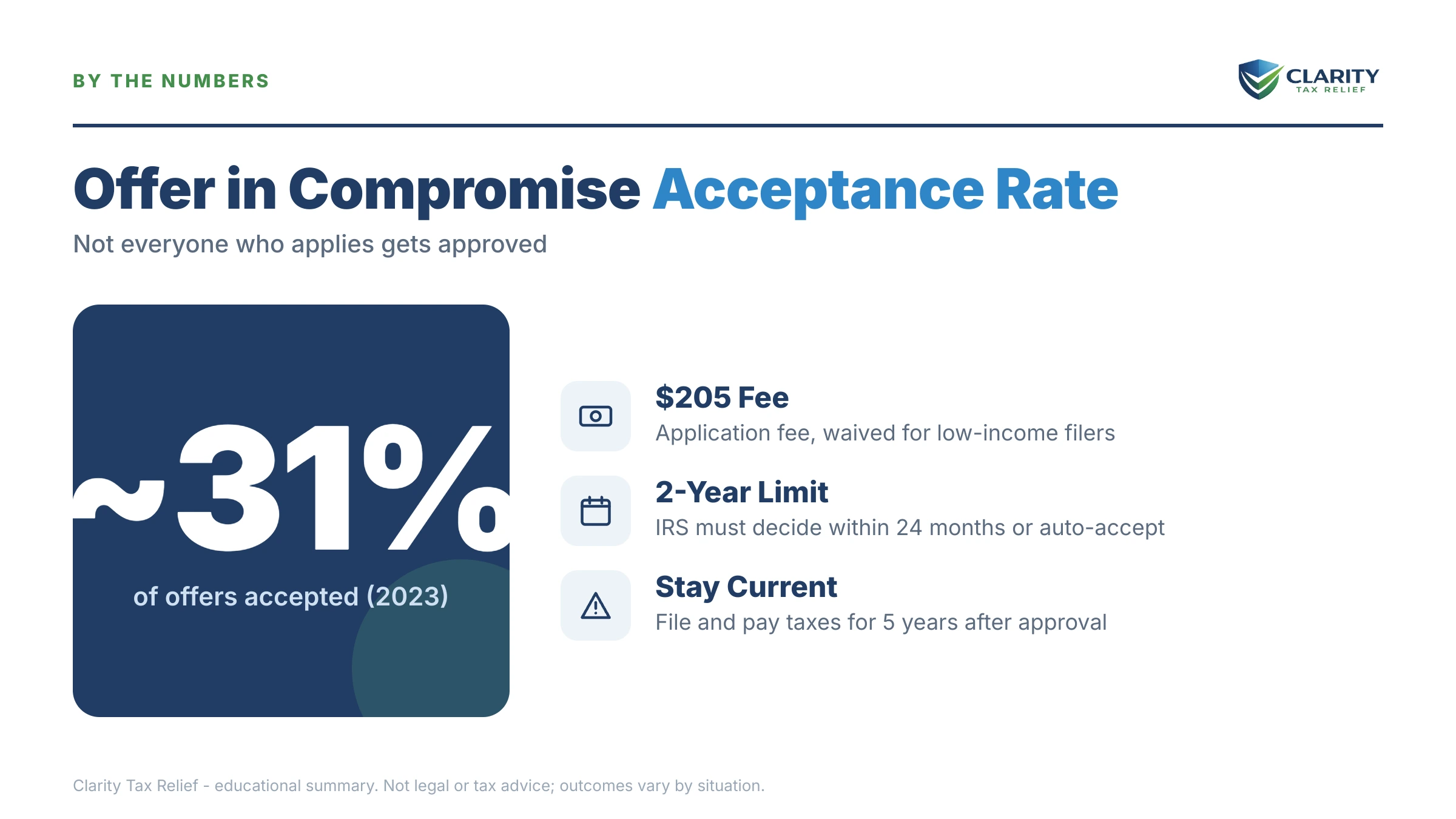

How does an offer in compromise work? You propose a settlement based on the IRS's own formula — your asset equity plus your future disposable income — using Form 656 and a $205 fee. If the IRS agrees your offer equals the most it could ever collect, it accepts and legally settles the rest. Roughly 1 in 5 offers were accepted in FY2024.

You kept the crew paid through the slow quarters, and somewhere along the way the IRS balance grew into a number — say $92,700 — that no monthly payment you can actually afford will ever catch. Now you're weighing the radio ads against reality. Here's the reality: the offer in compromise is a real program, it runs entirely on math, and you can run that math yourself before spending a dollar.

Further down, the image shows you exactly what the Form 656 offer package looks like and where your offer amount, payment option, and low-income certification live — seeing the actual paperwork makes everything in this guide concrete.

⏱ The real clocks: there's no deadline to apply for an offer in compromise — but penalties and interest keep accruing on your full balance every month until an offer is accepted or the debt is paid. And if the IRS rejects your offer, the date on the rejection letter starts a 30-day window to appeal with Form 13711.

Why the IRS agrees to settle for less at all

The IRS accepts an offer in compromise when your offer equals or exceeds the most it could realistically collect before the debt's collection deadline. That's not mercy — it's IRC §7122 telling the government to take a sure, smaller amount instead of chasing an uncollectible larger one for years.

There are three legal grounds for an offer:

- Doubt as to collectibility — your assets and income can't cover the debt. This is the basis for the overwhelming majority of offers and it's what this guide covers.

- Doubt as to liability — you dispute that you actually owe the tax. Different form (Form 656-L), no fee, different fight.

- Effective tax administration — you technically could pay, but collection would create exceptional hardship. Rare and narrowly granted.

This is also where the "pennies on the dollar" ads fall apart. Those ads imply the discount is negotiable charm. It isn't — the settlement amount is an output of a formula the IRS publishes. If the formula says you can pay in full, no firm on earth can get you an accepted offer, and anyone promising otherwise is selling you a rejection with a service fee attached.

How does an offer in compromise work, start to finish?

An offer in compromise works in five stages: you get compliant, you calculate your offer, the IRS screens the package, an offer examiner verifies your finances, and the IRS accepts, rejects, or returns the offer. The table below shows each stage and roughly how long it runs — for the full timeline breakdown, see how long does an OIC take, start to finish.

| Stage | What happens | Typical timing |

|---|---|---|

| 1. Compliance & math | You file all missing returns, get current on estimates/deposits, and calculate your reasonable collection potential | Before you mail anything — weeks to months depending on unfiled years |

| 2. Processability screen | The IRS checks forms, fee, compliance; defective offers are returned unreviewed | The first weeks after mailing |

| 3. Offer examination | An offer examiner verifies your Form 433-A (OIC) figures against bank statements and may counter with a higher amount | Commonly several months — the longest stage |

| 4. Decision | Acceptance, rejection with appeal rights, or return | Most offers are decided within roughly 6–12 months of mailing |

| 5. Appeal (if rejected) | You file Form 13711 within the 30-day window on the rejection letter | Adds months, but appeals reverse a meaningful share of rejections |

One backstop worth knowing: if the IRS doesn't decide within two years of receiving your offer, it's automatically accepted by law — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. With the IRS workforce down roughly 27% since 2025, review queues are longer than they've been in years — which cuts both ways: slower answers, but a two-year clock that occasionally runs out in the taxpayer's favor.

The formula: how the IRS calculates the offer it will accept

The IRS will accept an offer that equals your reasonable collection potential (RCP): the net value of what you own plus a multiple of what's left over each month after allowed expenses. Written out:

RCP = net realizable equity in assets + (monthly disposable income × 12 or 24)

Each piece has its own rules:

- Assets count at quick-sale value — generally 80% of fair market value — minus loans against them. Bank balances, vehicles, business equipment, real-estate equity, and retirement accounts all go in. Assets you gave away or spent down before applying can be added back as "dissipated assets."

- Monthly disposable income is your actual income minus the IRS's allowable living expense standards — national tables for food and clothing, local caps for housing and transportation. Your real spending doesn't control; the tables do. This is where most self-prepared offers overstate what they can exclude.

- The multiplier is 12 months for a lump-sum offer or 24 months for a periodic offer — never the full 10-year collection window. This multiplier is the entire reason an offer can legally come in far below the balance.

You submit that math on Form 433-A (OIC) (plus Form 433-B (OIC) if you run a business), attached to Form 656. Before you touch either form, you can estimate your own number in a few minutes with our Offer in Compromise Calculator — it estimates where your RCP lands so you know whether the program is even in play.

A worked example: could a $92,700 tax debt settle?

Say you're a small-business owner who owes $92,700 in personal income tax across two years — a stretch where you paid your employees and your suppliers before you paid yourself, and the 1040 balances stacked up. Clearly hypothetical numbers, arithmetic shown:

- Assets: a work truck worth $18,000 at quick-sale (80% of a $22,500 value) with a $12,000 loan = $6,000 equity; $4,000 in business and personal accounts after exclusions. Net realizable equity: $10,000.

- Income: you draw $7,400/month; the allowable expense standards for your county permit $6,800. Monthly disposable income: $600.

- Lump-sum offer: $10,000 + ($600 × 12) = $17,200 — with $3,440 (20%) due at filing plus the $205 fee, and the balance within five months of acceptance.

- Periodic offer: $10,000 + ($600 × 24) = $24,400 — roughly $1,017/month for 24 months, with payments starting the day you file.

Compare the alternative: a 72-month installment agreement on $92,700 runs roughly $1,288/month before you account for interest that keeps compounding on the unpaid balance. On these hypothetical facts, the formula points hard toward an offer.

Now flip one number and watch the answer change: if that same owner has $60,000 of home equity, RCP jumps to $77,200 on a lump-sum basis — still below $92,700, so an offer survives, but barely. Add $1,500/month of disposable income instead of $600 and RCP exceeds the balance entirely; the IRS would reject the offer and expect a payment plan. The formula, not the story, decides.

Lump-sum vs. periodic: the two ways to structure an offer

A lump-sum offer is usually cheaper because it uses the 12-month multiplier instead of 24 — but it requires 20% of the offer up front. Here's the full comparison, and the deeper dive lives in our guide to OIC payment options: lump sum vs. periodic.

| Feature | Lump-sum offer | Periodic offer |

|---|---|---|

| Future-income multiplier | 12 months | 24 months |

| Due with the application | 20% of the offer + $205 fee | First monthly payment + $205 fee |

| Payments during IRS review | None required after the 20% | Monthly payments must continue or the offer is returned |

| Payoff after acceptance | Within 5 months | Up to 24 months from filing |

| Low-income certification (AGI ≤ 250% of poverty) | Waives the fee and the 20% down payment | Waives the fee and all payments during review |

Note what low-income certification does: if your adjusted gross income is at or below 250% of the federal poverty level, the OIC low-income certification waives the $205 fee, the down payment, and payments while the IRS reviews — making a rejected offer cost you nothing but time.

Who qualifies — and what kills an offer before anyone reads it

An offer isn't reviewed on its merits until it clears processability, and this screen returns a large share of self-filed packages. Your offer will be sent back unread if:

- You have unfiled returns. Every legally required return must be filed first.

- You're behind on this year. Current-year estimated payments must be made; if you have employees, federal tax deposits must be current — including the two preceding quarters.

- You're in an open bankruptcy. The bankruptcy process handles the debt instead; see bankruptcy or offer in compromise for how to choose between the two.

- The fee or required payment is missing and you don't qualify for low-income certification.

A returned offer is worse than a rejected one: a return carries no appeal rights, while a rejection does. Getting compliant before filing isn't paperwork perfectionism — it's the difference between having appeal rights and not.

What happens if you do nothing about the debt

A tax debt over $66,000 puts your passport at risk in 2026 — and a $92,700 balance is well past that line. While you weigh your options, the IRS's automated collection system keeps moving through the same escalation sequence it always has, regardless of how understaffed the agency's phone lines are:

- CP14 — the first bill, with roughly 21 days to respond before reminders begin.

- CP501 / CP503 — reminder notices while penalties and interest compound monthly.

- CP504 — intent to levy your state tax refund; a federal tax lien becomes likely.

- CP508C — at $66,000+ (the 2026 threshold), the IRS can certify your debt to the State Department, blocking passport issuance and renewal. A pending offer in compromise is one of the exceptions that prevents this certification.

- LT11 / Letter 1058 — final notice of intent to levy, starting a 30-day clock on your Collection Due Process rights.

- Levy — bank accounts (funds held 21 days before they're sent to the IRS), wages (continuous until released), and business receivables.

Every stage of that ladder you climb closes options. An offer filed while you're at CP503 is evaluated on your finances; the same offer filed after a wage levy starts is evaluated on the same finances — but you've lost months of income and paid months of extra penalties waiting.

Owe more than you could ever repay?

Before you send the IRS a non-refundable fee and a 20% down payment, have an experienced tax professional run your offer math — free. We'll tell you honestly whether your numbers support an offer in compromise or whether a different program fits better, before another month of penalties and interest posts.

OIC vs. every other option: costs and timelines compared

An offer in compromise is one of five real resolution paths, and it's only the right one when the formula math works. For the full self-service playbook across all of them, start with our pillar guide on how to settle tax debt yourself; for the two closest calls, see CNC vs offer in compromise.

| Option | Upfront cost | What you pay | Best fit |

|---|---|---|---|

| Short-term payment plan | $0 setup | Full balance within 180 days | You can raise the money soon (bonus, sale, receivable) |

| Long-term installment agreement | Setup fee (reduced or waived for low income) | Monthly, up to 72 months online for balances ≤ $50,000; interest continues | You can afford the full balance over time |

| Partial-payment installment agreement | Setup fee + full financial disclosure | What your finances allow; the rest can expire at the 10-year CSED | You can pay something, but never everything |

| Currently Not Collectible | $0 | Nothing while hardship lasts; debt and interest remain | Paying anything would prevent basic living expenses |

| OIC — lump-sum | $205 + 20% of the offer | Offer amount within 5 months of acceptance | RCP is well below the balance and you can raise the cash |

| OIC — periodic | $205 + first monthly payment | Offer amount over up to 24 months | RCP is below the balance but 20% up front isn't possible |

How to apply for an offer in compromise, step by step

- Get compliant first. File every unfiled return, get current on this year's estimated payments, and — if you have employees — make the current quarter's payroll deposits; the IRS returns offers from non-compliant taxpayers without reviewing them.

- Run the RCP math. Total your asset equity at quick-sale value, subtract allowable living expenses from monthly income, and multiply what's left by 12 or 24 depending on your payment option.

- Complete Form 433-A (OIC). Document every figure with bank statements, pay records, and bills — the offer examiner verifies your numbers line by line.

- Complete Form 656 and choose your payment option. Pick lump-sum or periodic, and attach the $205 fee plus your first payment unless you qualify for low-income certification.

- Mail the package and keep your payments going. Periodic offers require monthly payments during the entire review; a missed payment can get the offer returned.

- Respond fast to the offer examiner. Requests for updated documents usually carry short reply windows — silence is the easiest way to lose an otherwise good offer.

What happens while your offer is pending

A pending offer generally suspends IRS levy action — but it also pauses the 10-year collection clock. Both effects show up on your account transcript as code 480, and both matter to your strategy:

- Collection pauses. The IRS generally won't levy while a processable offer is under review or while a timely appeal is pending. An already-filed lien, however, typically stays until the accepted offer is paid.

- The CSED tolls. The 10-year collection statute stops running while the offer is pending. If your debt is old and close to expiring, filing an offer can be a strategic mistake — it hands the IRS back the time your offer spends in review. Run that trade-off before filing.

- Installment agreement payments suspend. If you're already on a plan, you aren't required to keep paying it while the offer is evaluated.

- Interest keeps accruing on the full balance until the offer is accepted — one more reason a well-built first offer beats a rejected-then-refiled one.

If the IRS rejects your offer

A rejection letter states the RCP the IRS calculated and gives you 30 days to appeal. Three moves, in order of preference: appeal with Form 13711 if the examiner's math is wrong (valuation disputes and expense-standard errors are common and winnable); accept the examiner's counter-offer if the number is close and correct; or pivot to an installment agreement or hardship status if your finances genuinely support full payment. Whatever you do, the $205 fee stays gone and everything you've paid applies to the balance — nothing is refunded, but nothing is wasted either.

Business owners with payroll debt: the special rules

Personal income-tax debt and payroll-tax debt run through the offer program very differently, and owners routinely mix them up:

- Your personal 1040 debt — including a Trust Fund Recovery Penalty the IRS assessed against you personally for the business's unpaid withholding — can be included in a personal offer under the normal rules above.

- An operating business's own 941 debt is a different animal. The business must be current on all federal tax deposits before an offer is even processable, and the IRS treats withheld employee money as trust funds it rarely compromises. See business offer in compromise for how the entity-level math works, and an offer in compromise on back payroll taxes for why those offers face stricter scrutiny.

- Your business's value is an asset in your offer. Equipment, receivables, and goodwill go into your RCP. The examiner will also test whether your reported owner's draw is realistic against the business's bank deposits — a mismatch is a common rejection trigger for owners.

When you can handle an OIC yourself — and when help changes the outcome

You can reasonably file your own offer when your finances are simple: W-2 or steady 1099 income, no business entity, few assets, and an RCP that's obviously far below the balance. The forms are free, the IRS's pre-qualifier tool screens the basics, and low-income certification may make the attempt itself free.

Experienced help tends to change outcomes in four situations: a business with payroll debt in the mix (entity vs. personal liability determines what an offer can even cover), meaningful assets whose valuation is arguable (real estate, equipment, a going business), a levy or revenue officer already active (sequencing the offer against enforcement matters), and any offer where the CSED trade-off cuts close. In those cases the question isn't whether someone can fill out Form 656 — it's whether the RCP presented is the lowest defensible number, because that number is your settlement.

Not sure which side of that line you're on? Have an experienced tax professional look at your numbers for free — call (888) 825-7779 or use the 2-minute form and we'll tell you plainly whether your offer is one you can file yourself.

Terms on the OIC forms, decoded

- Reasonable collection potential (RCP): the IRS's calculation of the most it could collect from you — the floor for any acceptable offer.

- Quick-sale value: what an asset would fetch in a fast sale, generally 80% of fair market value.

- Allowable living expenses: the IRS's published spending caps used in place of your actual bills when computing disposable income.

- TIPRA payment: the 20% down payment required with a lump-sum offer (named for the 2005 law that created it) — waived with low-income certification.

- Returned vs. rejected: a returned offer failed a processing rule and carries no appeal rights; a rejected offer was reviewed and can be appealed within 30 days.

- Five-year compliance period: after acceptance, you must file and pay on time for five years — default it and the IRS can reinstate the original debt, minus what you paid.

The IRS's own resources are worth bookmarking: the official Offer in Compromise page at IRS.gov, the OIC Pre-Qualifier tool for a first-pass eligibility screen, and the Taxpayer Advocate Service if your offer stalls or enforcement continues while it's pending.

Offer in compromise questions, answered

How much should I offer the IRS in an offer in compromise?

Offer your reasonable collection potential: the net realizable equity in your assets plus your monthly disposable income multiplied by 12 (lump-sum offers) or 24 (periodic offers). Offering less than that number invites rejection; offering more wastes money. The IRS publishes the allowable-expense standards it uses, so you can run the math yourself before you apply — our OIC Calculator estimates it in a few minutes.

What are the chances the IRS accepts an offer in compromise?

The IRS accepted roughly 1 in 5 offers in FY2024, so most applications fail. The gap is almost always math: applicants offer less than their reasonable collection potential, or they weren't compliant on filings and deposits when they applied. Offers built accurately on the IRS's own formula fare far better than the raw average suggests, but no offer is ever guaranteed.

How long does an offer in compromise take from start to finish?

Most offers take somewhere between six months and a year from mailing to decision, and complex or appealed cases run longer. By law, if the IRS fails to make a decision within two years of receiving your offer, it is automatically accepted — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. Interest continues to accrue on your balance the entire time your offer is pending.

Does filing an offer in compromise stop IRS collections?

Generally yes — the IRS suspends levy action while a processable offer is pending and while a timely appeal of a rejection is under review. Two caveats: a filed tax lien usually stays in place until the offer is paid, and the pending offer pauses the 10-year collection statute, giving the IRS more time to collect if your offer fails.

Can I file an offer in compromise if I own a business with payroll debt?

Yes, but the rules tighten. An operating business must be current on its federal tax deposits before any offer is processable, and offers on trust-fund payroll debt are approved far less often than personal income-tax offers. If the payroll debt was assessed against you personally as a Trust Fund Recovery Penalty, it can be included in your personal offer.

Do I get my $205 fee and down payment back if the IRS rejects my offer?

No. The $205 application fee is non-refundable, and the 20% down payment on a lump-sum offer — plus any monthly payments made during review — is applied to your tax balance rather than returned. That's why running the reasonable collection potential math before you file matters: a doomed offer still costs real money.

What happens after the IRS accepts my offer in compromise?

You pay the accepted amount on the schedule you chose — within five months for lump-sum offers, up to 24 months for periodic offers — and the remaining balance is legally settled. You must then file and pay on time for the next five years; default that compliance period and the IRS can reinstate the original debt, minus what you paid.

Can I apply for an offer in compromise while I'm on a payment plan?

Yes. Submitting an offer doesn't require canceling your installment agreement first, and you are not required to keep making plan payments while the IRS evaluates the offer. If the offer is rejected and you don't appeal, the installment agreement typically resumes. Weigh the trade-off: a pending offer pauses the collection statute, while a payment plan does not.

Is the offer in compromise the same thing as the IRS Fresh Start program?

Not exactly. 'Fresh Start' was a set of 2011–2012 policy changes that loosened offer terms and lien thresholds — marketers turned it into a brand name. The offer in compromise is the actual statutory program, and it existed long before Fresh Start. Any company advertising a special 'Fresh Start application' is selling you the same Form 656 you can file yourself.

Your next 24 hours

- Pin down your exact balance and years. Log into your IRS online account (or grab your most recent notice) and write down the total owed and every tax year it covers — the offer must include all of them.

- Gather the RCP inputs. Your last filed return, three months of bank statements, loan balances on vehicles and property, and your monthly income records — everything the formula needs is in that stack.

- Get the math checked free. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will run your offer numbers with you — before another month of penalties and interest posts to your balance, and before you spend a non-refundable dollar on the application.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.