IRS Forms

Form 433-A Instructions: How to Fill Out the IRS Collection Information Statement (2026)

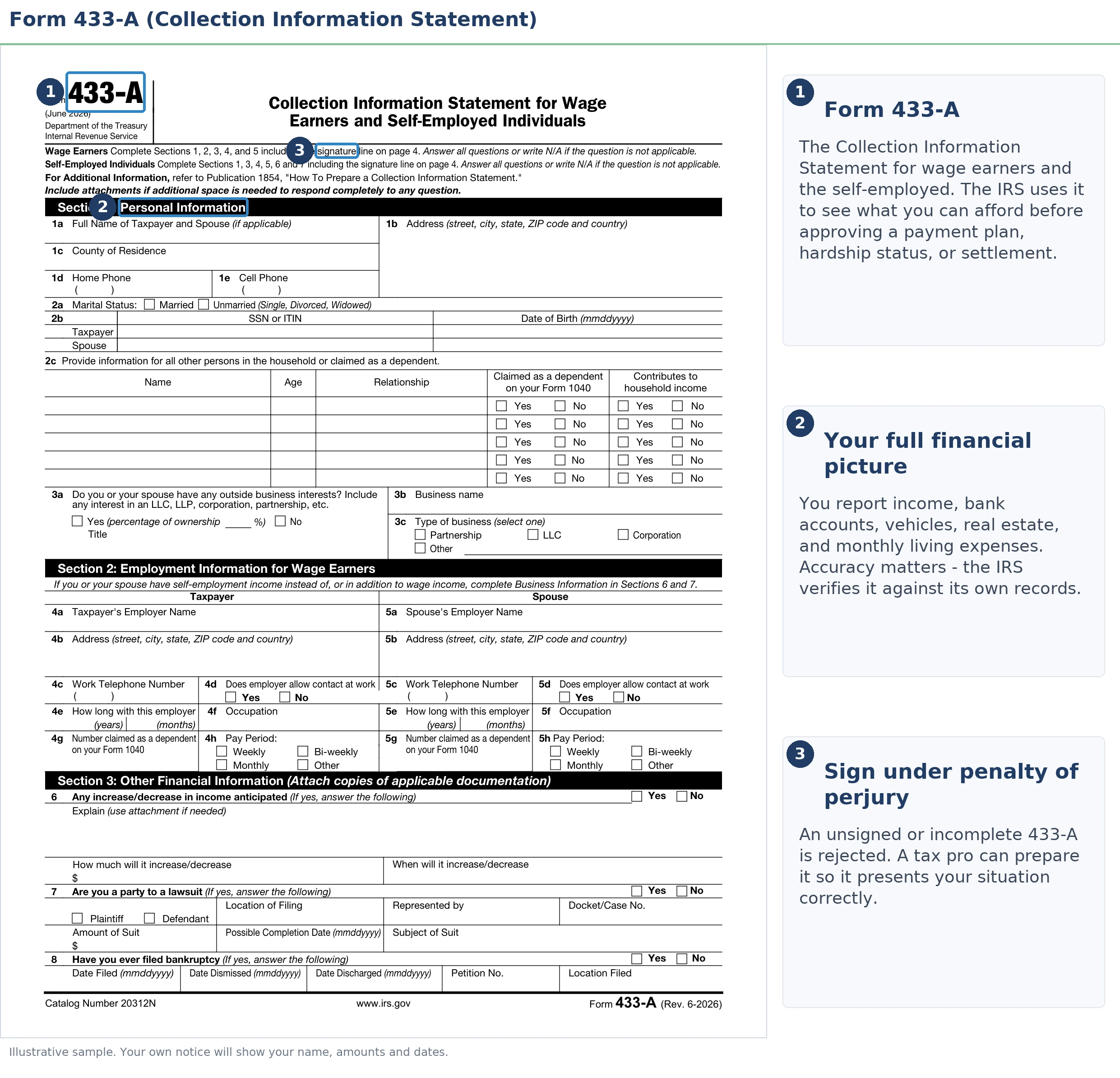

The short answer: Form 433-A is the IRS Collection Information Statement for wage earners and self-employed taxpayers. Complete all seven sections, attach roughly three months of bank statements plus proof of income and expenses, and sign under penalty of perjury. The numbers you enter set your monthly payment, hardship eligibility, or offer amount.

These Form 433-A instructions exist because the IRS just asked you to hand over a complete map of your finances — every account, every asset, every dollar in and out. Maybe a revenue officer left the form after a visit, or an LT24 notice told you a "completed Form 433" is required. The request feels invasive, and it is. But here's the leverage most people miss: the numbers you write, far more than anything the IRS decides, determine what you pay each month for years.

Fill it out well and you set the terms of your own resolution. Fill it out carelessly — a blank expense line, one strong month presented as typical income — and you lock in a payment you can't sustain. The image below shows you exactly what Form 433-A looks like and where the handful of lines that control your monthly payment sit; orient yourself there before you write a single number.

⏱ Your deadline: the response date on the letter or document request (often a Form 9297) your revenue officer gave you — there is no single statutory window, so the date on YOUR request controls. Miss it and the cooperative options narrow fast, while penalties and interest keep accruing monthly on the underlying balance.

Why the IRS is asking you for Form 433-A

The IRS demands Form 433-A when it won't take your word for what you can pay — usually because you owe more than $50,000, a revenue officer has your case, or you're requesting hardship status or an Offer in Compromise. Below those thresholds, payment plans are largely formula-driven and no financial statement is needed. Above them, everything runs through this form.

Three triggers cover most cases. First, a balance too large for a streamlined agreement: online payment plans top out at $50,000, so bigger debts require financial disclosure. Second, field collection — if a revenue officer contacted you (often after a Letter 725-B revenue officer visit), the full 433-A is their standard opening demand. Third, you asked for something that requires proof: a payment lower than the formula, Currently Not Collectible status, or an offer.

If you're not sure why the IRS is contacting you at all, start with our guide to why you got a letter from the IRS — this article assumes you already know you owe and have been told to produce financials.

433-A vs. 433-F vs. 433-A(OIC): which form you actually need

Three versions of the collection statement exist, and completing the wrong one wastes your deadline. The IRS employee or letter that made the request dictates the version — you don't get to choose the shorter one because it's easier.

| Form | Who requires it | What it's used for |

|---|---|---|

| Form 433-F | ACS — the IRS phone and notice unit (LT27 and similar letters) | Payment plans and hardship status when no revenue officer is assigned |

| Form 433-A | A revenue officer in field collection | Installment agreements above the streamlined thresholds, partial-pay plans, CNC, business-owner cases |

| Form 433-A(OIC) | The Offer in Compromise unit (packaged with Form 656) | Calculating your offer amount — your Reasonable Collection Potential |

The 433-F is a two-page summary; the full 433-A runs several times longer and demands far more detail, especially for the self-employed. If ACS asked for the short form, see our Form 433-F instructions instead. And if your debt sits inside a corporation, partnership, or multi-member LLC, the business itself files Form 433-B — the 433-A covers you personally, including a sole proprietorship or single-member LLC.

Form 433-A instructions, section by section

Form 433-A has seven sections, and Section 5 — monthly income and expenses — is the one that sets your payment. The rest exist so the IRS can verify Section 5 and find anything you could sell or borrow against. Here's the map:

| Section | What it asks | Watch out for |

|---|---|---|

| 1 — Personal information | Household members, dependents, dates of birth | Household size drives your allowable expense standards — count everyone accurately |

| 2 — Employment (wage earners) | Employer, pay frequency, withholding | Purely 1099? Your income belongs in Sections 6–7, carried into Section 5 |

| 3 — Other financial information | Lawsuits, bankruptcy, trusts, safe deposit boxes, past asset transfers | Assets transferred for less than full value can be added back to your ability to pay |

| 4 — Personal assets | Bank accounts, digital assets, retirement, life insurance cash value, real estate, vehicles | Equity uses quick-sale value (typically 80% of market) minus loans — don't overstate |

| 5 — Monthly income & expenses | The ability-to-pay statement | Blanks become zeros; claim every allowable expense, including current-year estimated taxes |

| 6 — Business information | Business accounts, receivables, assets, EIN | Listing receivables hands the IRS your client list — a future levy roadmap |

| 7 — Sole proprietor income & expenses | Monthly business profit and loss | Average 6–12 months of income; one strong month overstates your ability to pay for years |

Section 4: value assets the way the IRS does

The IRS measures assets at quick-sale value — typically 80% of fair market value — minus what you owe on them. A truck worth $24,000 with a $19,000 loan isn't $24,000 of collectible value; it's $24,000 × 0.80 − $19,000 = $200 of equity. Taxpayers who write retail values here hand the IRS ability-to-pay they don't actually have. List loan balances for everything, and don't forget items the IRS will find anyway: digital assets, cash-value life insurance, and retirement accounts all have dedicated lines now.

Section 5: the lines that decide your payment

Income minus allowable expenses equals the monthly payment the IRS expects — that's the entire game. Two habits protect you here. First, no blanks: an empty expense line is treated as zero, and every $100/month you fail to claim raises your expected payment by $100. Second, if you're self-employed, include your current-year estimated tax payments as a monthly expense. The IRS allows them because staying current is a condition of every resolution — and forgetting this line is the single most expensive 1099-contractor mistake on the form.

Sections 6–7: the self-employed trap

Contractor income swings, but the form asks for a monthly figure. Present an average of your last 6–12 months of net business income — not last month, not your best quarter — and keep it consistent with the bank statements you're attaching, because the IRS will reconcile them. Be equally deliberate in Section 6: accounts receivable you list are assets the IRS can levy, so understand that you're disclosing exactly where your money comes from before it reaches you.

The allowable-expense math that sets your number

The IRS doesn't accept your actual living expenses on Form 433-A — it caps most categories at published national and local standards. Food, clothing, and miscellaneous costs get a national allowance based on household size, generally without receipts. Housing, utilities, and vehicle costs are capped at the lesser of what you actually spend or the standard for your county. So $3,400 rent in a county with a $2,150 housing standard usually counts as $2,150 — and the extra $1,250 comes out of the money the IRS thinks you can send it every month.

Three categories escape the caps: documented health care costs, court-ordered payments (child support, alimony), and current-year taxes are generally allowed at actual amounts. And in some installment-agreement cases the IRS will permit your real expenses for a transition period rather than forcing an immediate lifestyle cut — worth requesting in writing rather than conceding the standard. Our breakdown of the IRS allowable living expenses standards covers each category in detail.

Worked example: a 1099 contractor who owes $76,400

Say you're a self-employed contractor who owes $76,400 across two tax years — squarely in the range where financials are mandatory (our guide to owing the IRS $75,000 covers that band's options). Here's how the 433-A math might run. All figures are hypothetical:

- Income (Sections 6–7): average monthly receipts of $9,100 minus $2,600 of business expenses = $6,500 net per month.

- Allowable expenses (Section 5): housing and utilities capped at $2,150 + vehicle ownership $590 + vehicle operating $310 + national standards $815 + health insurance $420 + out-of-pocket medical $85 + current-year estimated taxes $1,150 = $5,520.

- Monthly ability to pay: $6,500 − $5,520 = $980.

- Asset check (Section 4): work truck at $24,000 × 80% quick-sale = $19,200, minus a $16,500 loan = $2,700 equity, plus roughly $1,800 in checking.

What the IRS does with that: $76,400 ÷ $980 ≈ 78 months to full payment. If several years remain before the collection statute expires, the IRS sees a debt that's fully collectible over time — so the realistic outcome on these numbers is an installment agreement around $980/month, not a settlement, and an offer would likely be rejected because future income covers the balance.

Now see why the estimated-tax line mattered: without that $1,150 entry, disposable income jumps to $2,130 and the IRS expects more than double the payment — from a single forgotten line. Over a 78-month agreement, every $100/month of documented expense you fail to claim costs you $7,800. That is what "instructions" really means on this form: not where to put your name, but which entries move thousands of dollars.

What happens if you ignore a Form 433-A request

Ignoring a 433-A request doesn't pause your case — it converts it from a negotiation into unilateral enforcement. The sequence runs in stages:

- The deadline passes. Your revenue officer documents non-compliance against the date they set. The cooperative options — a payment you helped calculate, hardship status, an offer — start closing.

- Summons power. The IRS can legally compel the financial records you didn't provide, from you directly or straight from your bank. You end up disclosing everything anyway, minus the goodwill.

- Lien filing. A Notice of Federal Tax Lien attaches to everything you own — and at $76,400, a lien is a routine step, not a threat.

- Levy — built from records the IRS already has. Every client who issued you a 1099 is on file. A bank levy freezes funds for 21 days before they're sent; a levy on a client payment takes that payment in full, because non-wage levies have no paycheck-style exemption. See how an IRS levy on a 1099 contractor actually reaches contractor pay.

One 2026 reality worth naming: the IRS workforce shrank roughly 27% in 2025, but liens and levies are generated by automated systems that never stopped. Fewer humans to negotiate with is a reason to engage before enforcement starts, not evidence that it won't.

About to sign your 433-A?

The figures on this form set your payment for years, and you sign under penalty of perjury. Get your Form 433-A reviewed free before the deadline on your revenue officer's request — we'll check the asset values, the expense claims, and the resolution the numbers actually support.

Your options once the 433-A math is done

Monthly disposable income plus asset equity — the two numbers this form produces — determine which resolution the IRS will accept. Where you land depends heavily on how much you owe:

| Balance owed | Financial statement needed? | Realistic paths |

|---|---|---|

| Under $10,000 | No | Guaranteed installment agreement (the official IRS program name) — formula-based approval |

| $10,001–$25,000 | No | Streamlined payment plan, set up online |

| $25,001–$50,000 | Usually no | Streamlined plan (direct debit typically required near the top of the band), up to 72 months |

| $50,001–$100,000 | Yes — 433-F or 433-A | Non-streamlined agreement, partial-pay plan, CNC, or an offer if the math supports one |

| Over $100,000 | Yes — full 433-A | Revenue-officer-managed case; every option runs through your financials |

The main destinations for a 433-A filer:

- Non-streamlined installment agreement — your payment ≈ your monthly disposable income. See what changes in an IRS payment plan over $50,000. Interest and penalties continue accruing while you pay.

- Partial-pay installment agreement — when disposable income can't retire the debt before the collection statute expires, a partial payment installment agreement pays what the math supports, with periodic financial re-reviews.

- Currently Not Collectible — if allowable expenses meet or exceed income, IRS Currently Not Collectible status pauses collection entirely. The debt and interest remain, and a lien is still possible.

- Offer in Compromise — the IRS compares your debt to your Reasonable Collection Potential: asset equity plus 12 months of disposable income for a lump-sum offer (paid in five or fewer installments) or 24 months for a periodic offer. It costs a $205 application fee and 20% down on lump-sum offers — both waived with low-income certification (AGI at or below 250% of the poverty level) — and the IRS accepted roughly 1 in 5 offers in FY2024, so this is math-driven, never a given. You can estimate your own numbers with our Offer in Compromise Calculator, and the Form 656 instructions walk through the offer application itself.

- Penalty relief on top — whichever path you take, first-time abatement (and the Automatic Exemption from Penalty replacing it starting summer 2026) can trim the penalty portion of the balance if your prior three years were clean.

How to complete and submit Form 433-A, step by step

- Confirm the version you need — the full 433-A for a revenue officer, 433-F for the IRS phone unit, or 433-A(OIC) for an offer — and download the current revision from IRS.gov.

- Gather your proof — the last three months of bank statements, pay stubs or a 6–12-month profit-and-loss, loan balances, and receipts for any expense above the IRS standards.

- Complete Sections 1 through 7 — average self-employment income over 6–12 months, value assets at quick-sale value, and claim every allowable expense, including current-year estimated taxes.

- Run the math before you sign — income minus allowable expenses is the monthly payment the IRS will expect, so make sure the resolution you want matches that number.

- Copy everything, sign, and submit by the deadline — send it to the requesting revenue officer or the address on your letter, never a generic IRS box, and keep a full copy of the package.

- Pair it with a specific proposal — request the exact installment agreement, hardship status, or offer your numbers support, because a bare 433-A invites the IRS to set terms for you.

When you can handle Form 433-A yourself — and when help changes the outcome

Plenty of people complete this form competently on their own. That's realistic when your finances are simple: one income source, no business assets, a balance you agree with, and expenses that fit comfortably inside the IRS standards. If the math clearly supports the payment plan you want anyway, careful DIY plus the section guide above will get you there.

Experienced help earns its cost in specific situations: a revenue officer is managing your case and setting deadlines; you're self-employed with income that needs defensible averaging; business receivables or equipment are on the table; you have unfiled years (the IRS generally won't finalize any agreement until required returns are in); you're presenting a non-liable spouse's finances; or you're attempting offer math, where a single valuation choice can swing the result by five figures. A representative also files Form 2848 power of attorney and takes the revenue officer calls so you're never negotiating a sworn document live on the phone.

The dishonest version of this section would tell you everyone needs a professional. They don't. But a 433-A signed under penalty of perjury is not a form to guess on — if any paragraph above described your situation, get a second set of eyes first.

If a revenue officer set your deadline and the worked-example math above looks uncomfortably close to your own, have an experienced tax professional pressure-test your Form 433-A before you sign — start with a free case review.

Terms on Form 433-A, decoded

- Collection Information Statement (CIS): the IRS's name for the 433 series — a sworn snapshot of everything you own, earn, and spend.

- Quick-sale value (QSV): what an asset would bring in a fast sale, typically 80% of fair market value; the IRS uses it, minus loans, to compute your equity.

- Allowable living expenses: the national and local caps the IRS applies to most expense categories — published as the IRS Collection Financial Standards.

- Reasonable Collection Potential (RCP): asset equity plus a multiple of your monthly disposable income — the floor the IRS sets for any Offer in Compromise.

- Dissipated assets: money or property you gave away or spent on non-essentials while owing tax; the IRS can add it back as if you still had it.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, though offers, appeals, and bankruptcy pause the clock.

You can download the current form and official instructions from the IRS's About Form 433-A page, and review payment-plan terms on the IRS payment plans page.

Form 433-A questions, answered

What is IRS Form 433-A used for?

Form 433-A is the Collection Information Statement the IRS uses to measure what you can actually pay. Its seven sections inventory your assets, income, and monthly expenses, and that math sets your installment agreement amount, supports hardship status, or feeds an Offer in Compromise calculation. Revenue officers require it in most field collection cases; the shorter Form 433-F covers most phone-handled cases.

What is the difference between Form 433-A and Form 433-F?

Form 433-F is the condensed version used by the IRS's automated collection phone unit, while Form 433-A is the full statement required by revenue officers and, in its 433-A(OIC) variant, for offers. If a revenue officer or your letter names Form 433-A specifically, you cannot substitute the shorter form. If ACS asked for a 433-F, you don't need the longer one.

What documents do I need to attach to Form 433-A?

Plan on your most recent three months of bank statements, current pay stubs or a profit-and-loss statement if self-employed, statements for investment and retirement accounts, loan balances for vehicles and real estate, and proof of any expense above the IRS standards, such as medical bills or court-ordered payments. Revenue officers sometimes request six or twelve months of statements — provide exactly what your request specifies.

Does the IRS verify what I put on Form 433-A?

Yes. The IRS cross-checks your entries against the W-2s and 1099s filed under your Social Security number, your bank statements, property and DMV records, and your prior returns. You sign the form under penalty of perjury, so an omitted account or invented expense can sink a negotiation — or create far worse problems. Claim every legitimate expense aggressively, but never hide an asset.

What if my actual expenses are higher than the IRS standards?

The IRS caps most categories at its national and local standards, so rent above your county's housing standard usually counts only up to the cap. There are exceptions: health care, court-ordered payments, and current-year taxes are generally allowed at documented actual amounts, and in some installment-agreement cases the IRS permits actual expenses for a transition period. Document anything above a standard and argue for it in writing.

Do I have to include my spouse's income on Form 433-A?

The form asks for household income and expenses, so a non-liable spouse's income typically appears even when only you owe the tax. The IRS generally uses it to prorate shared household expenses rather than to reach the spouse's earnings directly, though community property states work differently. How a non-liable spouse's finances are presented can materially change the payment math, so handle this section deliberately.

How long is a Form 433-A good for?

The IRS commonly treats a Collection Information Statement as current for about a year, though a revenue officer can request updated figures any time your case stretches on. The flip side works for you too: if your income drops — a lost contract, a health event — you can submit an updated 433-A and ask the IRS to lower your payment or move you to hardship status.

Should I use Form 433-A or Form 433-A(OIC) for an Offer in Compromise?

Use Form 433-A(OIC), the offer-specific version packaged with Form 656 in the offer booklet. It follows the same structure but adds offer math, including the future-income multiplier and certain asset exclusions that don't appear on the standard form. If a revenue officer is also working your case, you may end up completing both versions at different stages — the entries need to be consistent.

What happens after I submit Form 433-A?

The IRS reviews the form, verifies your figures against its records, and may ask follow-up questions or request more documentation before responding to the resolution you proposed. Nothing happens automatically: a 433-A submitted without a specific proposal invites the IRS to set terms itself. Always pair the form with the exact installment amount, hardship request, or offer your numbers support.

Your next 24 hours

- Find your deadline. Pull out the letter or the document request your revenue officer gave you and locate the response date — that date, not anything else, is your clock.

- Start the paper pile. Gather your last three months of bank statements, your invoices or pay records for the past year, loan balances, and your most recent filed return — everything Sections 4 through 7 will demand.

- Get the numbers checked before you sign. Book a free case review at the 2-minute form or call (888) 825-7779 — an experienced tax professional will run your 433-A math, flag missed expense claims, and match the form to the resolution it actually supports, while penalties and interest are still accruing on the balance underneath it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.