IRS Forms

Form 656 Instructions: How to Fill Out an Offer in Compromise (2026)

The short answer: Form 656 is the application for an IRS Offer in Compromise, and the official Form 656 instructions live in the Form 656-B booklet. You complete the form, attach Form 433-A(OIC) with proof of your finances, and include the $205 fee plus a first payment — both waived if you qualify for low-income certification.

You've done three years of gig work without filing, the balance has crept to around $4,800 with penalties stacking on top, and every ad you see says one form can settle it for less. That form is Form 656 — and it genuinely can, but only when the package around it is built exactly the way the IRS's screeners expect. This guide walks you through every part of it.

Form 656 is only two pieces of a thicker package — the image below shows you exactly what the form looks like and where the fields that sink the most offers sit, so keep it in view as we go part by part.

⏱ The real clock: Form 656 has no filing deadline — but penalties and interest keep accruing on your balance every month until an offer is accepted. And if the IRS rejects your offer, the rejection letter opens a short appeal window, typically 30 days, so a sloppy first submission costs you real money and real rights.

What Form 656 actually is (and why the booklet matters)

Form 656 is the contract you propose to the IRS: a specific dollar amount, on a specific payment schedule, to settle specific tax years for good. It's not a hardship letter and it's not a negotiation opener — the number you write on it has to be defensible under the IRS's own formula, or the offer fails. For the background on how the program works end to end, see our guide to how an offer in compromise works; this page stays on the form itself.

The IRS publishes Form 656 inside the Form 656-B booklet, which also contains Form 433-A(OIC) for individuals, Form 433-B(OIC) for businesses, the low-income certification table, and the mailing-address chart. Always download the current booklet before you start — the IRS revises it, and offers filed on outdated form versions get bounced back unread. One more distinction up front: Form 656 is for offers based on your inability to pay. If your argument is that you don't actually owe the tax, that's a different application — see OIC doubt as to liability, which uses Form 656-L and has no fee.

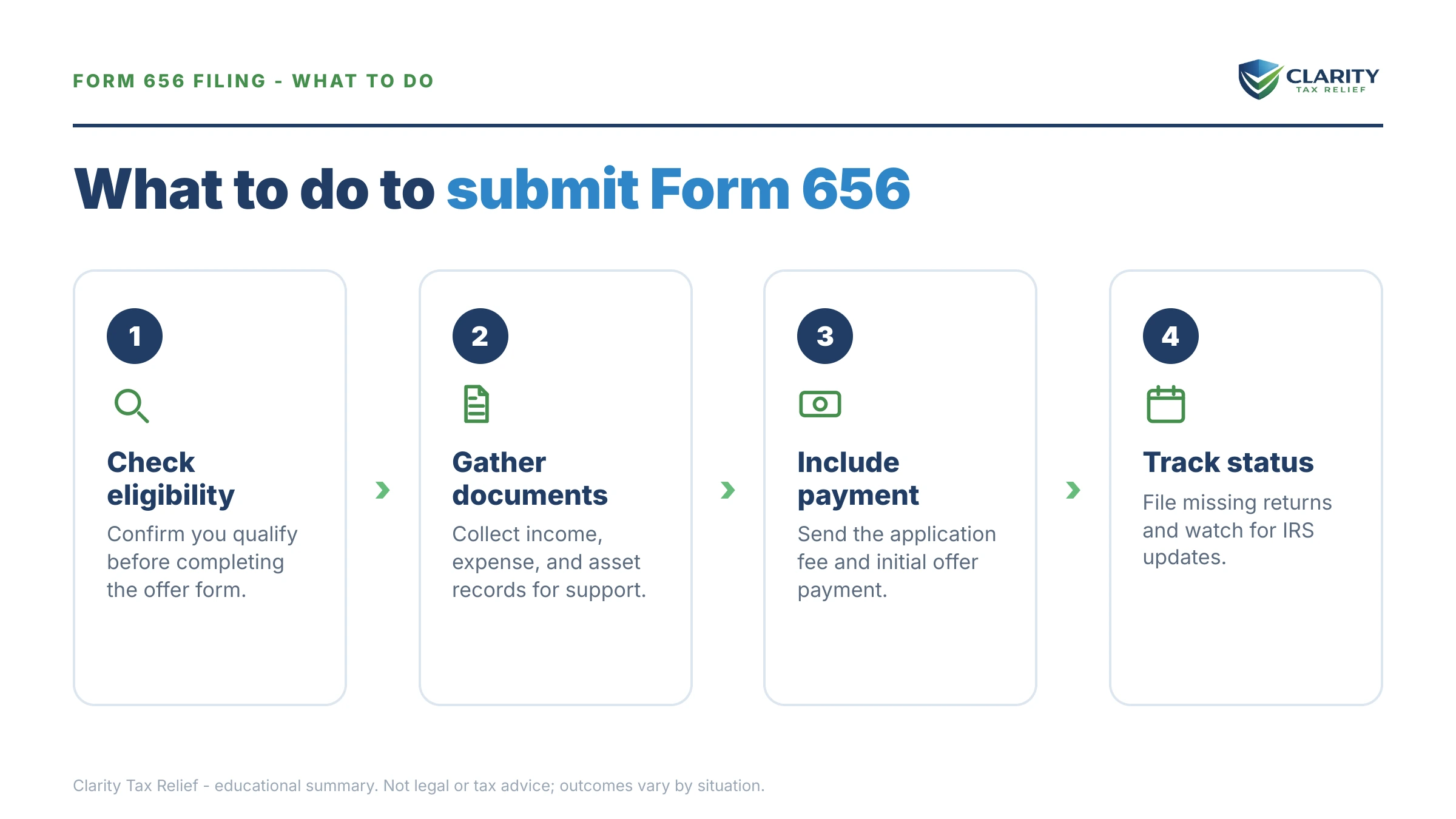

Before you touch Form 656: the eligibility gate

The IRS checks whether your offer is "processable" before anyone reads your numbers. Fail this screening and the entire package comes back with no appeal rights. To pass, you must have:

- Every required return filed. This is the wall most gig workers hit. If you have three unfiled years, those returns must be filed and processed first — start with our guide for people who haven't filed in 3 years. You can't compromise a debt the IRS hasn't finished assessing.

- Current-year estimated tax payments made. Self-employed filers must be paying this year's quarterlies before offering on last year's debt. The IRS reads a missed current quarter as proof the problem will just repeat.

- No open bankruptcy case. A pending bankruptcy makes the offer non-processable; the debt gets handled inside the bankruptcy instead.

- Payroll deposits current, if you have employees. Business offers run under stricter rules — see our guides to a business offer in compromise and the business offer in compromise payroll path for trust-fund debt.

Two useful side effects once a processable offer is pending: IRS levies generally pause while it's reviewed, and the 10-year collection statute pauses too — the clock stops running in your favor. Already on an installment agreement? You can still file; see can I apply for OIC while on payment plan for how the two interact.

Form 656 instructions, part by part

Form 656 walks you through eight decisions in order, and three of them — the tax periods, the payment option, and the certification — decide whether your offer survives. Here's what each part is really asking:

Your identification and tax periods. List your name, SSN, and every tax year and tax type you want compromised — income tax by year, plus any civil penalties, listed separately. This list is the single most unforgiving field on the form: a tax year you leave off Form 656 survives the offer and the IRS keeps collecting on it even after everything else settles. Pull your account transcripts and match the list exactly.

Business information. Only if you're offering on debt owed by a business entity — sole proprietors report their business inside Form 433-A(OIC) instead.

Reason for offer. Nearly everyone checks Doubt as to Collectibility — "I can't pay this in full before the collection statute runs." The narrow alternative, Effective Tax Administration, is for people who technically could pay but shouldn't have to (severe hardship, exceptional circumstances). Doubt as to Liability, again, lives on Form 656-L — never on this form.

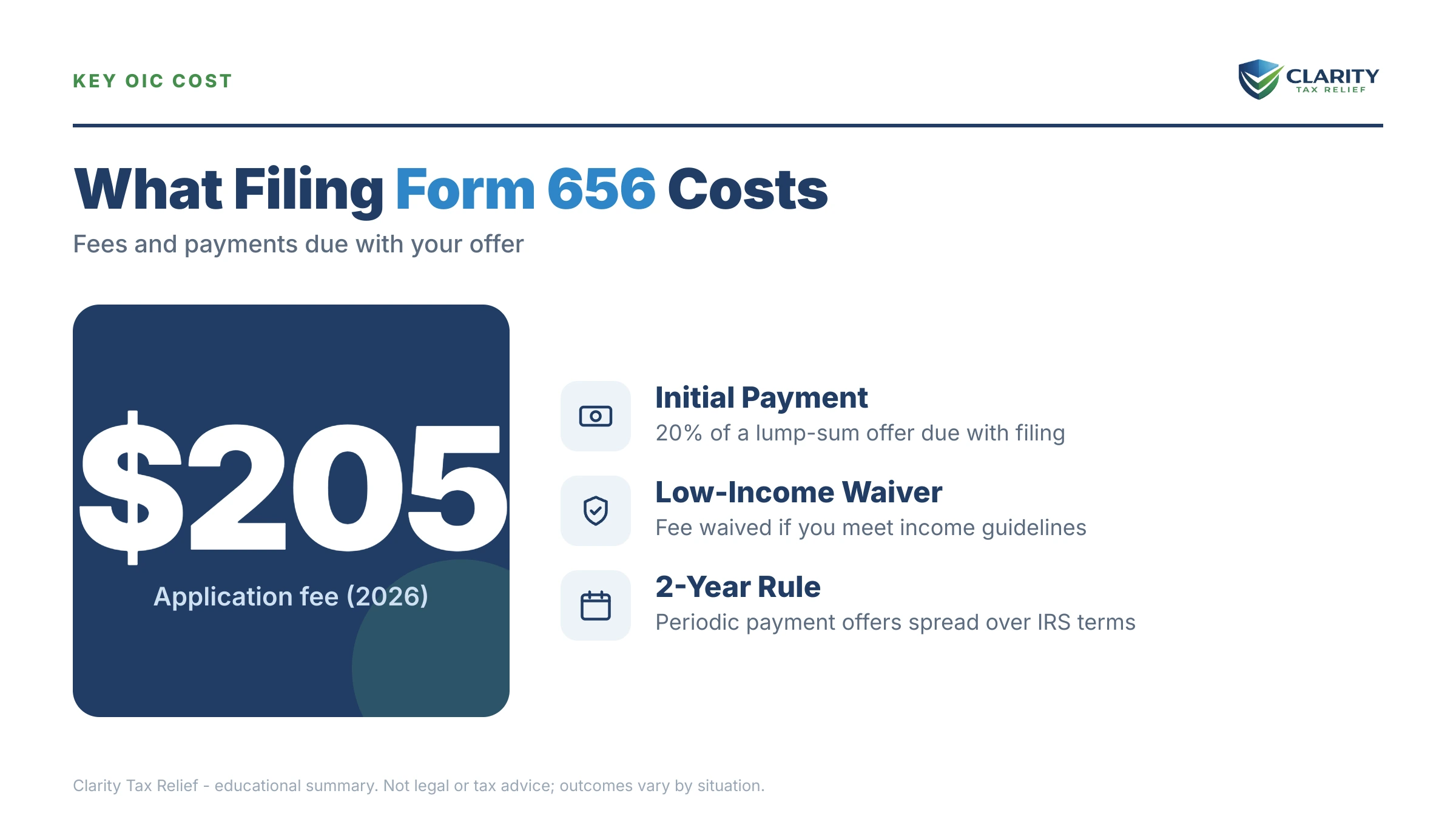

Low-income certification. A checkbox with an income table built into the form. If your adjusted gross income is at or below 250% of the federal poverty level for your household size, checking it waives the $205 fee, the 20% down payment, and all payments during review. For a gig worker with a lean year, this box can take the out-of-pocket cost of applying to zero — details in our guide to the OIC low income certification.

Payment terms. You choose one of two structures, and the choice changes both your required offer amount and what you send with the package:

| Payment option | Sent with Form 656 | During IRS review | After acceptance |

|---|---|---|---|

| Lump-sum cash offer | $205 fee + 20% of the offer | No further payments | Balance in 5 or fewer payments within 5 months |

| Periodic payment offer | $205 fee + first monthly payment | Monthly offer payments continue — miss one and the offer can be treated as withdrawn | Remaining monthly payments, 6–24 months total |

| Either, with low-income certification | $0 — fee and down payment waived | $0 required | Offer paid per the accepted terms |

The trade-off is bigger than it looks: a lump-sum offer is calculated with 12 months of future income, a periodic offer with 24 — so the periodic route usually means offering roughly twice as much future income for the privilege of paying slowly. Full comparison in OIC payment options: lump sum vs. periodic.

Source of funds and payment designation. State where the offer money will come from (savings, a family loan, sale of an asset). Be truthful — the offer examiner will see your bank statements. Note that money sent with an offer is applied to your tax debt if the offer fails; it doesn't come back.

The offer terms. This is the fine print you're agreeing to, and it binds you after acceptance: you must file and pay every tax on time for the 5 years following acceptance, or the compromise defaults and the original debt — minus what you paid — comes back. The terms also confirm the collection statute pauses while the offer is pending. One piece of good news buried here: under current policy, the IRS no longer keeps your refund for the calendar year your offer is accepted — see will the IRS keep my refund after an OIC for how refunds are treated around an offer.

Signatures. If the liability is joint, both spouses sign. An unsigned or single-signed joint offer is a processability failure — the most preventable return there is.

How much to offer: the math behind the number

The IRS accepts an offer when it equals or beats your Reasonable Collection Potential — the total of your net asset equity plus your monthly disposable income times 12 (lump sum) or 24 (periodic). That formula, not your total debt and not your negotiating nerve, sets the number for Form 656; the full mechanics are in our guide to reasonable collection potential. You can estimate your own figure with our Offer in Compromise Calculator before you commit anything to paper.

A worked example (hypothetical). Say you owe $4,800 across three gig years you've just filed. Your car is worth $4,000 with $3,500 left on the loan — at the IRS's 80% quick-sale value, that's ($4,000 × 0.8) − $3,500 = −$300, so zero countable equity. Your bank account averages $400, mostly protected by the IRS's small-balance allowance. Your income runs $2,600 a month against $2,480 in allowable living expenses, leaving $120 of monthly disposable income. A lump-sum offer would be roughly $0 assets + ($120 × 12) = $1,440 against the $4,800 owed. A periodic offer would run $120 × 24 = $2,880. And if your AGI sits under the 250%-of-poverty line, the low-income certification means the $1,440 lump-sum offer goes in with no $205 fee and no $288 down payment.

Now the honest comparison: that same $4,800 fits a guaranteed installment agreement (balances of $10,000 or less) at roughly $4,800 ÷ 72 = about $67 a month plus accruing interest, set up online in minutes with no financial disclosure. The offer saves more money; the payment plan costs less effort and carries no risk of months of review ending in rejection. Which wins depends on whether that $120 of disposable income is real and durable — exactly the judgment call worth a professional look.

What happens if your Form 656 package is wrong

A flawed Form 656 doesn't get negotiated — it gets returned or rejected, and the two failures carry very different rights. Here's the sequence a bad package follows:

- Processability screening. Unfiled returns, missing signatures, a missing 433-A(OIC), the wrong form revision, or an open bankruptcy → the offer is returned, with no appeal rights. Collection resumes where it left off, and you start over from zero.

- Examiner review. A processable offer gets an offer examiner who verifies every line against your bank statements and asks for anything missing. Ignore a document request, or stop the required monthly payments on a periodic offer, and the offer is returned or treated as withdrawn mid-review.

- The decision. If the examiner's math says you can pay more than you offered, the offer is rejected — with a letter stating the IRS's calculated amount and a short window, typically 30 days, to appeal using Form 13711 OIC appeal.

- After a failed offer. Interest accrued the whole time, the collection statute was paused (so the IRS lost nothing), and the notices pick back up. The IRS accepted roughly 1 in 5 offers in FY2024 — the difference is overwhelmingly package quality and offer math, which is why the first submission is the one to get right.

Building a Form 656 package right now?

Before you mail it, let an experienced tax professional pressure-test it free — the offer math, the 433-A(OIC), the tax-period list, and whether the low-income certification applies. Interest keeps building on your balance while an incomplete offer bounces back and forth.

If Form 656 isn't the right fit: your other options

An Offer in Compromise is the hardest IRS program to qualify for, and Form 656 is worth filing only when the math genuinely works. Here's how it stacks against the alternatives:

| Option | Key eligibility | Best when |

|---|---|---|

| Offer in Compromise (Form 656) | All returns filed; offer meets or beats your Reasonable Collection Potential | Assets and future income truly can't cover the debt before the statute runs |

| Guaranteed installment agreement | Balance $10,000 or less; up to 72 months; no financial disclosure | Small balance and steady enough income — the simplest path for a $4,800 debt |

| Short-term payment plan | Full payment within 180 days; $0 setup fee | Money is coming (busy season, a payout) — you just need runway |

| Currently Not Collectible | Allowable expenses meet or exceed income — genuine hardship | You can't pay anything now but your finances may recover — compare CNC vs offer in compromise |

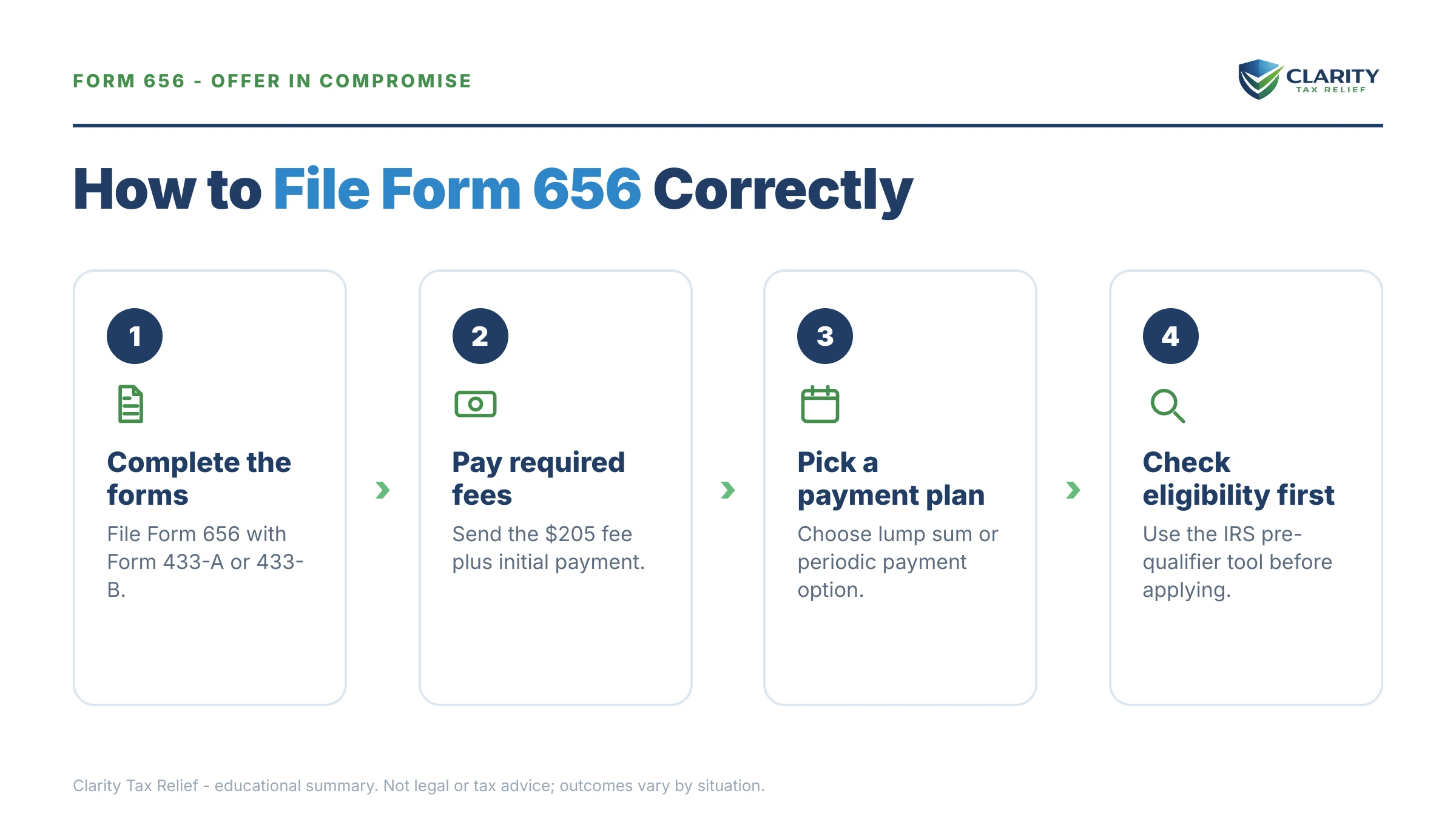

How to file Form 656, step by step

- File every missing return — the IRS returns offers from non-filers without reading the numbers, so unfiled years must be fixed first.

- Complete Form 433-A(OIC) — gather three months of bank statements, income records, and honest asset values before you start.

- Calculate your offer amount — net asset equity plus 12 months of disposable income (lump sum) or 24 months (periodic).

- Fill out Form 656 — list every tax year and tax type you owe, check one reason for the offer, pick a payment option, and sign.

- Attach payment or the low-income certification — the $205 fee plus any required down payment, as separate checks, unless the certification waives them.

- Mail the complete package and track it — use the address chart in the Form 656-B booklet for your state, send it with tracking, and keep a full copy.

Then expect quiet. Review commonly runs many months — our guide to how long does an offer in compromise take maps the whole timeline — and by law an offer the IRS doesn't decide within 2 years is automatically accepted, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count.

When you can handle Form 656 yourself — and when help pays for itself

Plenty of taxpayers file Form 656 successfully without help, and some shouldn't file it at all. You can reasonably go it alone if your finances are simple — W-2 or single-source income, one or two tax years, no real assets — and your offer math clearly clears the formula. And if you owe under $10,000 with steady income, run the payment-plan comparison first: a $67-a-month agreement you set up online tonight may beat months of offer review entirely.

Experienced help changes outcomes in specific situations: multiple unfiled years that have to be reconstructed and sequenced before the offer (our gig-worker scenario exactly), self-employment income the IRS will average and challenge, home or retirement equity that has to be valued and argued, a prior returned or rejected offer, or a levy already in motion that needs to be paused while the package is built. The 433-A(OIC) — walked through line by line in our Form 433-A instructions — is where offers are really won or lost, because every allowable-expense judgment on it moves your required offer up or down by 12 or 24 times that monthly amount.

Terms on Form 656, decoded

- Reasonable Collection Potential (RCP): the IRS's formula for the most it could ever collect from you — net asset equity plus a multiple of monthly disposable income — and the floor your offer must meet.

- Low-income certification: the checkbox that waives the fee, down payment, and review-period payments when your AGI is at or below 250% of the federal poverty level.

- Lump-sum cash offer: an offer paid in five or fewer installments within five months of acceptance, calculated with 12 months of future income.

- Periodic payment offer: an offer paid monthly over 6–24 months, calculated with 24 months of future income, with payments continuing during review.

- Returned vs. rejected: returned means the package failed screening — no appeal rights; rejected means it was investigated and turned down — appealable, typically within 30 days.

- Offer terms: the contract clauses you sign, including 5 years of perfect filing and paying after acceptance — default and the original debt comes back.

Form 656 questions, answered

Do I have to send Form 433-A(OIC) with Form 656?

Yes, for almost everyone. An individual filing a doubt-as-to-collectibility offer must attach Form 433-A(OIC) with proof of income, expenses, and assets — the IRS treats Form 656 without it as non-processable and returns the whole package. The only offer that skips the financial statement is a doubt-as-to-liability offer, which uses a different form entirely, Form 656-L.

How much does it cost to file Form 656 in 2026?

The application fee is $205, and a lump-sum offer must also include 20% of the offer amount with the package. If your adjusted gross income is at or below 250% of the federal poverty level for your household size, the low-income certification on Form 656 waives the fee, the 20% down payment, and payments during review. Money you send with the offer is not refunded if the offer fails — the IRS applies it to your balance.

Can I file Form 656 if I have unfiled tax returns?

No. The IRS checks filing compliance before it reads a single number on your offer, and it returns Form 656 packages from non-filers as non-processable. You must file every required return — and, if you're self-employed, be current on this year's estimated tax payments — before the offer can even enter the queue. File first, then offer.

What is the difference between a returned and a rejected Form 656?

A returned offer failed a processability check — unfiled returns, a missing signature, a missing 433-A(OIC), or an open bankruptcy — and comes back with no appeal rights; you fix the problem and start over. A rejected offer was actually investigated and turned down on the numbers, and the rejection letter gives you a short window, typically 30 days, to appeal using Form 13711. Rejection preserves rights; a return does not.

How long does the IRS take to decide on Form 656?

Most offers take many months — often the better part of a year — because an offer examiner has to verify every figure on your 433-A(OIC). By law, an offer the IRS doesn't decide within 2 years is automatically accepted, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count — though very few cases run that long. While the offer is pending, levies generally pause but the 10-year collection statute pauses too.

Do I keep making payments while the IRS reviews my offer?

It depends on the payment option you check on Form 656. A periodic payment offer requires you to keep sending the monthly offer payment during the entire review — miss one and the offer can be treated as withdrawn. A lump-sum offer requires only the 20% down payment up front. Taxpayers who qualify for the low-income certification owe nothing during review under either option.

What happens after the IRS accepts my Form 656 offer?

You pay the accepted offer amount on the schedule you chose — a lump-sum offer is paid in five or fewer installments within five months of acceptance. Then the offer terms keep working: you must file and pay every tax on time for the next 5 years. Default during that window and the compromise is revoked, with the original balance, minus what you paid, back on the books.

Primary sources worth bookmarking: the IRS's official Offer in Compromise page (with the current Form 656-B booklet and a pre-qualifier tool), the IRS payments page for the alternatives, and the Taxpayer Advocate Service if your offer stalls inside the IRS.

Your next 24 hours

- Pull your IRS account transcripts and write down every year with a balance and every year with no return filed — that list becomes both your filing to-do and your Form 656 tax-period list.

- Gather the 433-A(OIC) raw material: your last three months of bank statements, income records from every gig platform, and honest values for your car and anything else you own.

- Get a free case review before you mail anything — send us the numbers at the 2-minute form or call (888) 825-7779, and an experienced tax professional will tell you whether Form 656 beats a payment plan for your situation while interest is still accruing either way.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.