Offer in Compromise

Reasonable Collection Potential: How the IRS Decides Your Offer in Compromise (2026)

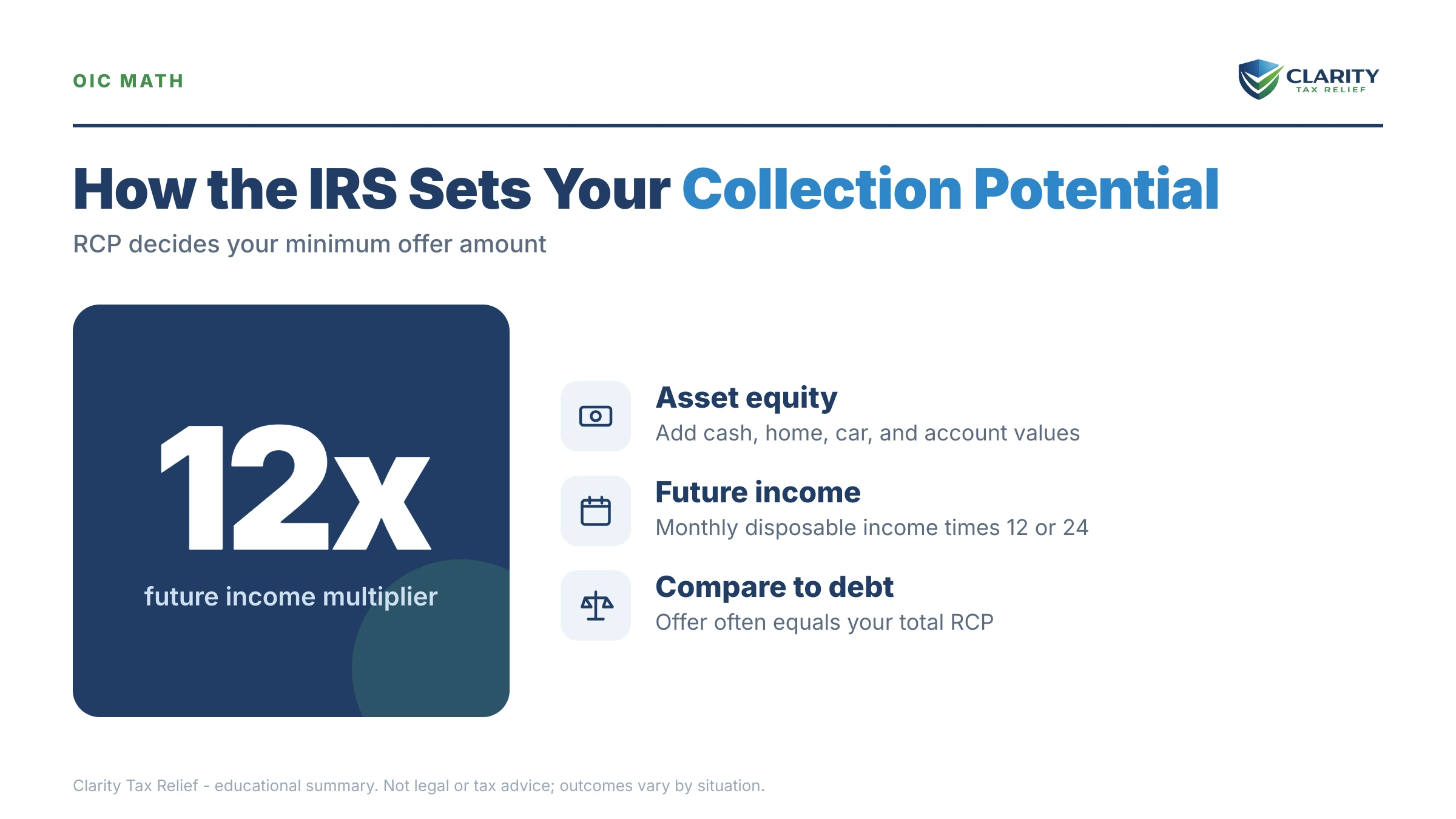

The short answer: reasonable collection potential (RCP) is the IRS's calculation of the most it could ever collect from you — the net equity in your assets plus your monthly disposable income multiplied by 12 (lump-sum offer) or 24 (periodic offer). The IRS won't accept an Offer in Compromise below that number.

You've probably seen the phrase "reasonable collection potential" buried in the Form 656 booklet or in an IRS letter, and it sounds like bureaucratic filler. It isn't. It's the single number that decides whether your offer gets accepted — and if a levy notice is sitting on your kitchen table right now, it's also the number that determines whether an offer can realistically make that levy go away.

The good news: RCP isn't a mystery or a negotiation. It's arithmetic, computed line by line from Form 433-A (OIC) — which means you can run the same math the IRS runs before you spend a dime. The image below shows you exactly what that financial worksheet looks like and where your RCP takes shape.

⏱ The clocks that matter: RCP itself has no filing deadline — but if an LT11 or Letter 1058 started your levy countdown, you have 30 days from the date printed on that notice to request a Collection Due Process hearing on Form 12153. And interest plus the monthly failure-to-pay penalty keep accruing on your balance until it's resolved, whichever route you take.

What reasonable collection potential actually is

Reasonable collection potential is the IRS's estimate of everything it could squeeze from your assets and future paychecks before the collection statute runs out. Under the most common offer ground — doubt as to collectibility — the rule is simple: the IRS accepts an offer only when it equals or beats your RCP, and your RCP is less than the full balance you owe.

That's the entire game. Marketing that promises settlements without mentioning RCP is selling you a coin flip. The IRS accepted roughly 1 in 5 offers in FY2024, and the single biggest reason for the other 4 is an offer that came in below the IRS's own RCP figure — see the real numbers in our offer in compromise acceptance rate 2026 breakdown.

If you're new to how the program works end to end — forms, fees, timelines — start with our guide to how an offer in compromise actually works. This page goes deep on just the math.

The reasonable collection potential formula: two halves

RCP = net realizable equity in your assets + your future income over 12 or 24 months. Every line of Form 433-A (OIC) feeds one of those two halves.

Half one: net realizable equity in assets

The IRS values what you own at quick-sale value — roughly 80% of fair market value — because a forced sale never fetches full price. From that discounted value, you subtract any loan against the asset. A few buffers apply: the Form 656-B booklet lets you exclude $1,000 of bank balances and a set amount of vehicle equity (check the current booklet for the vehicle figure). No asset counts below zero.

For a renter, this half is often small: no home equity, maybe a financed car that's underwater at quick-sale value, a modest checking account. That's not a flaw in your case — it's the reason renters with low disposable income are often stronger offer candidates than homeowners with the same debt.

Cash, investment accounts, and crypto count at full value. Retirement accounts generally count too, reduced for the taxes and costs of getting the money out. And be careful with anything you recently sold, spent, or gave away: the IRS can add the value of dissipated assets back into your RCP as if you still had the money.

Half two: future income

Future income is your monthly disposable income — total household income minus IRS-allowed expenses — multiplied by 12 for a lump-sum offer or 24 for a periodic offer. Not by the 10-year collection statute. That 12/24 cap, introduced under Fresh Start, is why offers became viable for ordinary wage earners at all. The mechanics of this half get their own deep dive in our guide to the OIC future income calculation.

Notice the trap: choosing a periodic offer to spread out payments doubles the income half of your RCP. Here's what each structure costs and how the timelines compare:

| Offer type | Income multiplier | Upfront cost | Payment window |

|---|---|---|---|

| Lump-sum cash | 12 × monthly disposable income | $205 fee + 20% of the offer | 5 or fewer payments after acceptance |

| Periodic payment | 24 × monthly disposable income | $205 fee + first monthly payment; payments continue during review | 6–24 monthly payments |

| Either type with low-income certification | Same 12 or 24 | $0 fee, $0 down, no payments during review | Same as chosen type |

Two footnotes to that table. First, the 20% down payment and periodic payments made during review are applied to your tax debt even if the offer is rejected — see whether the OIC down payment is refundable before you send it. Second, if your adjusted gross income is at or below 250% of the federal poverty level, OIC low income certification wipes out the fee, the down payment, and the payments-during-review requirement entirely.

Once you understand the two halves, you can rough out your own number in a few minutes — estimate it with our Offer in Compromise Calculator before you commit to the paperwork.

Allowable living expenses: where most RCP math goes wrong

The IRS caps your living expenses at its published Allowable Living Expense standards — not at what you actually spend. This is the step that inflates most people's disposable income and, with it, their RCP.

The standards work in layers. Food, clothing, housekeeping, and personal care come from a national table you can claim in full without receipts — even if you spend less. Housing and utilities are capped at a county-by-county local standard for your family size: if your rent plus utilities is under the cap, the IRS uses your actual number; if it's over, you generally get only the cap. Vehicle ownership and operating costs have their own tables. Court-ordered payments, health insurance, and documented out-of-pocket medical costs are allowed on top.

Three practical consequences for your RCP:

- Claim every standard you're entitled to. People routinely under-claim the national standards because their real grocery bill is lower. That's leaving RCP-inflating dollars on the table.

- High rent in a cheap-standard county hurts. If your actual rent exceeds the local cap, the difference gets treated as disposable income you supposedly have — even though your landlord has it.

- Special circumstances can override the tables. Documented medical needs, a disabled dependent, or other necessary costs above the standards can be allowed — but only if you prove them on Form 433-A (OIC), not by asserting them later.

The full county tables and how examiners apply them are covered in our guide to IRS allowable living expenses standards.

A worked example: $4,800 owed, a renter, and a levy notice

Say you owe the IRS $4,800 from a year your withholding fell short, you rent your apartment, and an LT11 final notice of intent to levy just arrived. This is hypothetical, but the arithmetic is exactly what an offer examiner would run.

Asset half. Checking account: $1,150, minus the $1,000 booklet exclusion = $150. Car: fair market value $6,000 × 80% quick-sale value = $4,800, minus a $5,200 loan balance = negative, so it counts as $0. No home, no retirement account. Net realizable equity = $150.

Income half. Take-home-equivalent monthly income: $2,900. Allowable expenses under the standards — local housing/utilities cap, national food and clothing tables, car operating costs, health insurance — total $2,850. Monthly disposable income = $50. Lump-sum offer: $50 × 12 = $600.

RCP = $150 + $600 = $750. Because $750 is well below the $4,800 owed, an offer of $750 or more is mathematically viable. And at this income level, low-income certification likely applies — so the $205 fee and the 20% down payment ($150 on a $750 offer) would both be waived.

Now flip one number. Same renter, but monthly disposable income of $400 instead of $50: future income becomes $400 × 12 = $4,800. Add the $150 in equity and RCP is $4,950 — more than the debt. The offer gets rejected because the math says you can full-pay, and the right move becomes a payment plan instead. One expense line moved the answer from "strong offer candidate" to "no offer at all." That sensitivity is the whole reason the 433-A (OIC) deserves care.

What happens if you get the RCP math wrong — or ignore the levy

A bad offer doesn't just get rejected; it costs money, time, and collection-statute protection while the levy machinery waits at the end. The sequence runs like this:

- Offer returned as non-processable. Unfiled returns, missing fee or down payment, or current-year estimated payments not made — the IRS sends the package back with no appeal rights, and collection resumes immediately.

- Offer rejected on RCP grounds. The examiner's worksheet says your RCP exceeds your offer. The rejection letter states the IRS's own RCP figure and gives you a window — printed on the letter, typically 30 days — to appeal with Form 13711.

- The collection statute was paused the whole time. A pending offer tolls the 10-year collection clock, so a doomed offer hands the IRS extra months to collect.

- Levy action resumes. The IRS generally can't levy while a processable offer is pending or on appeal — but once the offer dies, the LT11 that arrived before you filed is still live. A bank levy freezes funds for a 21-day hold before they're gone; a wage levy is continuous until released.

And if you never respond to the levy notice at all — no offer, no plan, no hearing request — the 30-day window on the LT11 closes, your Collection Due Process rights lapse, and the levies above start without further warning. The LT11 notice guide covers that clock in detail.

Facing a levy and wondering if your RCP supports an offer?

Send us your notice and a snapshot of your finances. An experienced tax professional will run the actual RCP math — assets, standards, multipliers — and tell you honestly whether an offer, a plan, or hardship status fits, before your levy notice's 30-day window closes. Free and confidential.

If your RCP is higher than your debt: your real options

An offer below your RCP gets rejected — but a high RCP doesn't leave you defenseless, especially on a smaller balance. Here's how the options line up:

| Option | Who's eligible | Cost and catch |

|---|---|---|

| Short-term payment plan | Can full-pay within 180 days | $0 setup; interest and penalties continue until paid |

| Guaranteed installment agreement | Individuals only; income-tax balance of $10,000 or less (excluding penalties and interest); all returns filed; timely filing and payment for the past 5 years with no installment agreement in that period; can full-pay within 3 years | IRS must accept it; setup fee applies; no financial disclosure |

| Streamlined installment agreement | Owe $50,000 or less — up to 72 months online | No 433 financials; interest and penalties keep accruing |

| Currently Not Collectible | Allowable expenses meet or exceed income (genuine hardship) | Collection pauses; debt and interest remain; reviewed periodically |

| Offer in Compromise | RCP below the balance owed; all returns filed; current on this year's payments | $205 fee + down payment (waived with low-income certification); months-long review |

For the renter in our example who fails the RCP test at $400/month disposable income: $4,800 fits a guaranteed installment agreement — roughly $134/month over 36 months, though paying faster cuts the interest and the 0.5%-per-month late-payment penalty that keep accruing. If disposable income is genuinely $0 or negative, IRS currently not collectible status pauses the levy without requiring any payment at all — and sometimes beats a marginal offer.

One more path if your finances change mid-plan: you can generally pursue an offer even after a plan is in place — the trade-offs are covered in can I apply for OIC while on payment plan.

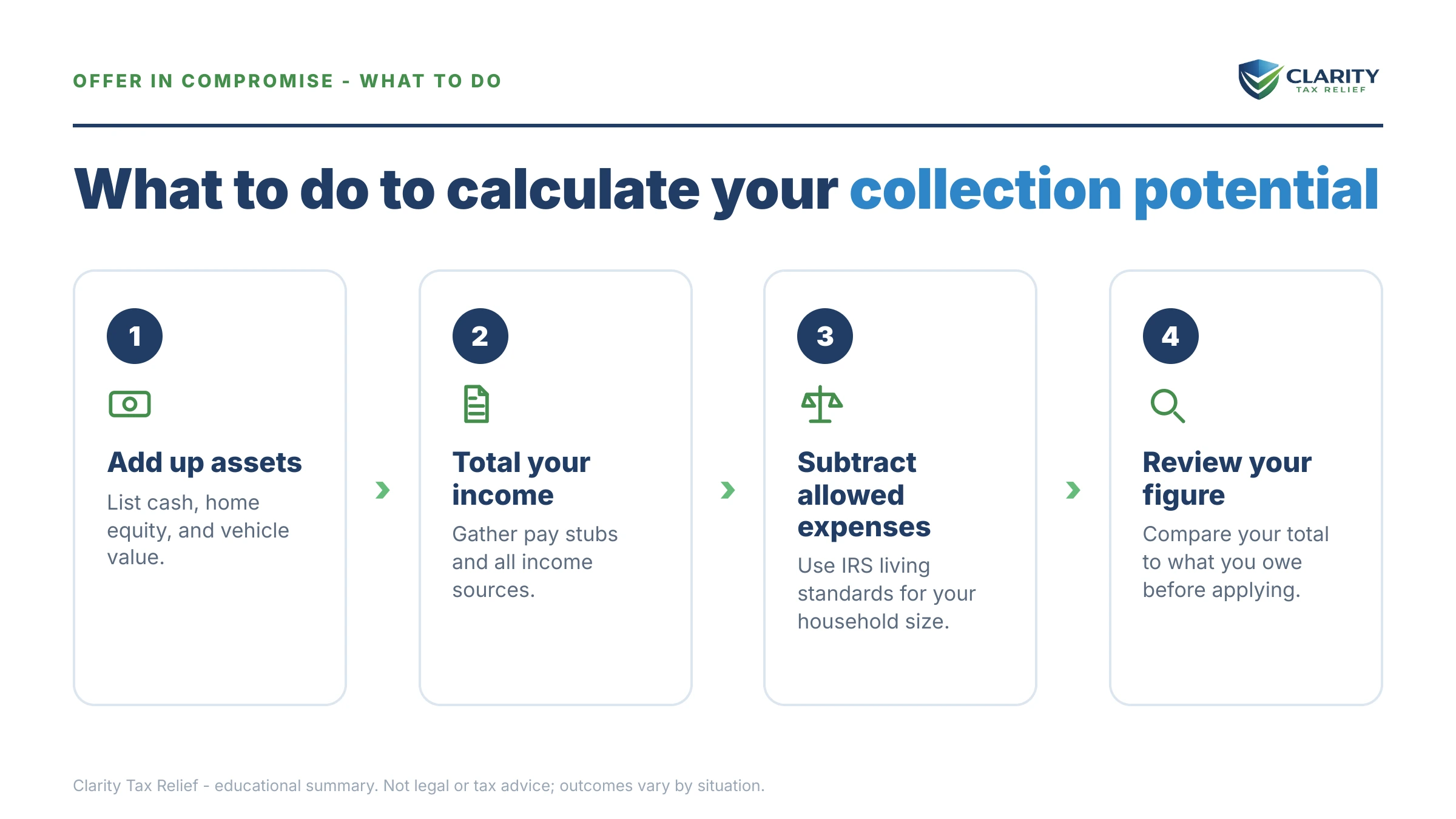

How to calculate your reasonable collection potential, step by step

- List every asset at quick-sale value — roughly 80% of fair market value for cars, real estate, and valuables; face value for cash and bank balances.

- Subtract loans and allowed exclusions — loan balances come off each asset, and the Form 656-B booklet lets you exclude $1,000 of bank balances plus a set amount of vehicle equity. Never let an asset go below zero.

- Compute your monthly disposable income — total household income minus IRS Allowable Living Expense standards for your county and family size, not your actual budget.

- Multiply by 12 or 24 — use 12 for a lump-sum offer (paid in 5 or fewer payments) or 24 for a periodic offer (paid over 6 to 24 months).

- Add the two halves and compare to your balance — if the total is below what you owe, an offer at or above that total is viable; if it meets or exceeds your debt, pivot to a payment plan or hardship status instead.

The numbers all flow from one document, so the real work is the financial statement itself — our Form 433-A instructions walk through it line by line, and the Form 656 walkthrough covers the offer form it attaches to.

When you can run the RCP math yourself — and when help changes the outcome

If your finances are simple — one W-2 income, a bank account, a financed car, no recent asset transfers — you can credibly compute your own RCP with the Form 656-B booklet and the ALE tables, and decide from there. And if the math shows you can full-pay $4,800 within 180 days or on a guaranteed installment agreement, you don't need anyone: set it up yourself at IRS.gov and skip the offer entirely.

Experienced help earns its cost in specific situations: a levy already in motion, where sequencing the CDP hearing, the offer, and a release matters more than any single form; self-employment or fluctuating income, where the future-income figure is genuinely arguable; assets you sold or spent in the last few years that could be added back; expenses above the standards that need a documented special-circumstances case; and borderline RCPs where a few hundred dollars of monthly expense allowance decides whether an offer exists at all. The examiner will run the math either way — the question is whether your 433-A (OIC) gives them a defensible reason to reach the lower number.

Terms in the RCP math, decoded

- Net realizable equity — what an asset is worth at quick-sale value after subtracting loans against it; the asset half of RCP.

- Quick-sale value — the discounted value (roughly 80% of fair market value) the IRS assigns because a forced sale never brings full price.

- Future remaining income — your monthly disposable income times 12 or 24; the income half of RCP.

- Allowable Living Expense (ALE) standards — the IRS's national and county expense tables that cap what you may deduct from income, regardless of actual spending.

- Dissipated asset — money or property you spent or transferred while owing taxes that the IRS can add back into your RCP as if you still had it.

- Doubt as to collectibility — the offer ground based purely on RCP math: the IRS settles because it can't collect the full balance, not because the debt is disputed.

Reasonable collection potential questions, answered

What is reasonable collection potential in an Offer in Compromise?

Reasonable collection potential is the IRS's estimate of the most it could ever collect from you — the net equity in your assets plus a multiple of your monthly disposable income. It's the floor for any acceptable offer under doubt as to collectibility. If your RCP is below your balance and your offer meets or beats that RCP, the offer is viable; offer less than your RCP and expect rejection.

How does the IRS calculate reasonable collection potential?

The IRS adds two numbers: net realizable equity in your assets (valued at roughly 80% of fair market value, minus loans) and future income (monthly income minus allowable living expenses, multiplied by 12 for lump-sum offers or 24 for periodic offers). The math comes straight from your Form 433-A (OIC), so every line on that form moves the result.

Can I offer the IRS less than my reasonable collection potential?

Generally no — under doubt as to collectibility, the IRS rejects offers below its RCP figure. The main exception is effective tax administration, where you can prove collecting your full RCP would cause economic hardship, such as an older taxpayer whose only asset is money needed for medical care. Special circumstances documented on Form 433-A (OIC) can also justify deviations from the standard expense tables.

Does the IRS use my actual rent and bills or its own numbers?

A mix. Housing and utilities are capped at the local Allowable Living Expense standard for your county and family size — if your actual rent is lower, the IRS uses your actual number; if it's higher, you typically get only the cap. Food, clothing, and miscellaneous costs use national standards you can claim without receipts. Documented health costs above the standards can be allowed with proof.

What happens if my RCP is higher than the amount I owe?

Your offer will be rejected, because the math says the IRS can collect in full. That isn't the end of the road: a balance under $10,000 usually fits a guaranteed installment agreement, balances up to $50,000 fit streamlined plans of up to 72 months, and genuine hardship can qualify you for currently not collectible status instead.

Does a pending Offer in Compromise stop an IRS levy?

Generally yes — the IRS can't levy while a processable offer is pending, while a rejection is being appealed, or for 30 days after rejection. It does not automatically release a levy already seizing wages, and it never stops interest from accruing. The bigger catch: a pending offer pauses the 10-year collection statute, so a doomed offer just gives the IRS more time.

How long does the IRS take to decide an offer?

Most offers take several months to a year or more, depending on complexity and the examiner's workload. By law, an offer is deemed accepted if the IRS doesn't make a decision within 2 years of submission — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. IRS staffing cuts in 2025 have stretched review times, which makes getting the RCP math right the first time even more valuable.

Your next 24 hours

- Find the date on your levy notice. If you're holding an LT11 or Letter 1058, the date printed at the top starts your 30-day Collection Due Process window — write it down before anything else.

- Gather the RCP inputs: your last tax return, three months of pay stubs and bank statements, loan balances on your car, and your rent and utility bills. That's everything the math needs.

- Get the numbers run for free. Use the 2-minute form or call (888) 825-7779 — an experienced tax professional will compute your actual RCP and map the offer-versus-plan decision before the levy clock runs out.

Primary sources: the IRS's official Offer in Compromise page hosts the Form 656-B booklet and pre-qualifier; the IRS payment plans page covers the fallback options; and the Taxpayer Advocate Service can intervene when a levy is causing hardship during review.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.