Offer in Compromise

Effective Tax Administration Offer: The IRS's Rarest OIC, Explained (2026)

The short answer: an effective tax administration offer is the rarest of the three Offer in Compromise types. You concede that you owe the tax and could technically pay it in full — but you ask the IRS to accept less because full collection would cause economic hardship or would be fundamentally unfair. It's filed on Form 656 with Form 433-A (OIC).

You ran the Offer in Compromise numbers and hit a wall: on paper, the IRS says you could pay every dollar — but only by selling the roof over your head or draining the one account you'll ever retire on. That trap has a name, and the effective tax administration offer is the narrow door the tax code built out of it. It's rare, it's judgment-driven, and it's winnable when the case is built the way offer examiners are trained to read it.

The image below shows you exactly where the effective tax administration option appears on Form 656 — the checkbox is easy to find, but the explanation section next to it is where ETA offers are won or lost.

⏱ The real clock: there is no filing deadline for an effective tax administration offer, but your balance is not standing still. The failure-to-pay penalty adds 0.5% per month and interest compounds daily until the debt is resolved — on an $83,100 balance, a year of waiting typically adds thousands before you've filed a single form.

What an effective tax administration offer is — and why it exists

An effective tax administration offer asks the IRS to accept less than you owe even though your assets and income could technically pay the debt in full. Every other settlement path starts from "I can't pay." ETA starts from the opposite: the IRS agrees you can pay — and settles anyway, because collecting in full would either push you into genuine economic hardship or be so unfair that it would damage public confidence in the tax system.

Congress created this ground so the collection machine would have a safety valve for cases the standard formulas get wrong: the retiree whose only asset is the home they'll need care in, the disabled worker whose savings must fund a lifetime of treatment, the taxpayer whose "collectible" equity exists only on paper. The IRS's official overview lives on its Offer in Compromise page; this article covers what that page doesn't — how the ETA ground actually gets decided.

Be clear-eyed going in: ETA is an exception the IRS grants sparingly, not a loophole. Anyone promising you a "pennies on the dollar" outcome through ETA is selling the scam, not the program.

ETA vs. the other two OIC grounds: which one you're actually filing

The IRS accepts Offers in Compromise on exactly three grounds — doubt as to liability, doubt as to collectibility, and effective tax administration — and each demands different proof. Most people searching for ETA actually belong in one of the other lanes, so sort this out before you spend the filing fee.

| Offer type | What you're arguing | When it fits |

|---|---|---|

| Doubt as to liability | "The assessed amount is wrong." | Disputed audit results, substitute-for-return balances, identity mix-ups. Filed on Form 656-L with no application fee. |

| Doubt as to collectibility | "My assets and income can't cover the debt." | The vast majority of accepted offers. Formula-driven: your offer must equal your reasonable collection potential. |

| DCSC (collectibility with special circumstances) | "Even my RCP would cause hardship." | RCP is below the debt, but paying it would require liquidating assets you live on. You offer less than RCP. |

| Effective tax administration | "I could full-pay, but collection would cause hardship or be unfair." | RCP is at or above the full debt. Hardship documented to the standard in Treasury Regulation §301.6343-1. |

One important detour: if your real problem is that the balance itself is inflated — the IRS filed returns for you, or a 1099 got double-counted — the cheaper fix may be amending a return to lower a tax debt or a doubt-as-to-liability offer, not ETA. ETA concedes the number is correct.

The dividing line: your reasonable collection potential

Reasonable collection potential (RCP) is the single number that decides which offer type you file: your net realizable asset equity plus 12 months of disposable income (for a lump-sum offer) or 24 months (for a periodic offer). If RCP is at or above your full balance, ETA is your only settlement ground; if RCP falls short, you're in collectibility territory. Our guide to reasonable collection potential walks the full calculation — and you can estimate your own number in a few minutes with our Offer in Compromise Calculator.

Run this math honestly before anything else. Filing an ETA offer when your RCP is actually below the debt wastes months, because the examiner will reclassify and re-run your case under the collectibility rules anyway.

The economic hardship test: what the IRS actually accepts

The IRS measures economic hardship for an ETA offer by the levy-release standard in Treasury Regulation §301.6343-1: collection that would leave you unable to pay reasonable basic living expenses. That's a specific legal test, not a vibe. Patterns that meet it include:

- Long-term illness or disability — your assets are earmarked, in practice, for treatment or care that will continue for years, and liquidating them for the IRS leaves nothing for medical needs.

- Income-producing assets you live on — the equity exists, but selling it destroys the income stream that pays your rent and groceries (a work vehicle, tools, or the modest rental that is your retirement income).

- A dependent's care needs — selling the home would displace a disabled child or parent whose care is built around it.

- Retirement-only assets late in life — you're at or near retirement age, the account can never be rebuilt, and draining it converts a tax debt into decades of poverty.

What fails the test, reliably: a lifestyle downgrade, private-school tuition, a mortgage bigger than the local housing standard, or "I'd rather not sell." The hardship version of ETA is also limited to individuals — entities can't have basic living expenses.

Documentation decides these cases. A diagnosis letter, a Social Security disability determination, twelve months of treatment invoices, and a physician's statement about future costs will do more than ten pages of narrative.

Public policy and equity offers: the even rarer path

A public policy or equity ETA offer argues that collecting in full — even without hardship — would undermine fairness or public confidence in the tax system. This is the rarest acceptance the IRS grants. The classic fact patterns involve a taxpayer who relied on specific written IRS advice that turned out wrong, or whose liability exists because of processing errors or delays entirely outside their control. If your case is "the penalties feel unjust," that's not an ETA argument — it's a penalty abatement request, which is free to make and far more often granted.

What happens if you do nothing about an $83,100 balance

An $83,100 IRS balance sits above the $66,000 passport-certification threshold for 2026, so ignoring it risks more than levies. The collection system is automated — IRS staffing fell roughly 27% in 2025, but the notice stream and levy programs never paused — and at this balance the sequence runs with real teeth:

- The balance compounds. The failure-to-pay penalty adds 0.5% per month and interest compounds daily on top of it. Every month of silence raises the number any future settlement must address.

- The notice ladder climbs. A first bill leads to reminder notices, then a CP504 intent to levy your state refund, then a final notice (LT11/Letter 1058) that opens a 30-day window before wage and bank levies become legal.

- A federal tax lien gets filed. At $83,100, a Notice of Federal Tax Lien is a realistic next step — it attaches to your home equity and complicates any sale or refinance.

- Passport certification. Above $66,000 and unresolved, the IRS can certify your debt to the State Department, which can deny a passport renewal. A pending offer or payment plan generally prevents this.

- Levies reach gig income. The IRS can levy your bank account (funds are held 21 days before they're sent) and serve levies on the platforms that pay you.

Here's the flip side, and it matters: a properly submitted offer generally suspends levy action while it's pending, and your transcript will show code 480 when the offer posts. Filing doesn't just open a settlement path — it stops the escalation while the IRS decides.

Think your case is bigger than the RCP formula?

ETA and hardship offers live or die on how the case is built. Send us your numbers — balance, assets, and the circumstances the formula ignores — and an experienced tax professional will tell you which offer ground actually fits, free and confidential. Interest is accruing either way; the review costs nothing.

Your options compared: ETA offer vs. everything else

An ETA offer is one of five realistic paths for a balance you technically could — but practically can't — pay, and it's rarely the fastest. Weigh the whole board before committing; the DIY roadmap for each program is in our guide to how to settle tax debt yourself.

| Option | Upfront cost | Typical timeline | What it does |

|---|---|---|---|

| ETA offer | $205 fee + 20% of the offer for lump sum (both waived with low-income certification) | Commonly many months; auto-accepted if the IRS doesn't decide within 2 years — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count | Settles the full debt for the accepted amount if hardship or equity is proven |

| Collectibility / DCSC offer | Same as ETA | Similar review window | Settles for your RCP — or less than RCP with documented special circumstances |

| Payment plan | $0 setup for short-term (up to 180 days); modest setup fee for monthly agreements | Active within days to weeks | Pays in full over time (up to 72 months online at ≤$50,000; financials required above that); interest and penalties continue |

| Currently Not Collectible | $0 | Weeks to establish; reviewed periodically | Pauses collection during hardship; the debt remains and interest accrues |

| Penalty abatement | $0 | Weeks to months | Removes qualifying penalties (first-time abatement, or the new Automatic Exemption from Penalty rolling out from summer 2026); tax and interest remain |

Note what ETA is competing against. If your hardship is temporary, CNC costs nothing and takes weeks. If your hardship is permanent and your equity is locked in assets you need to survive, ETA is the only option that ends the debt for less — which is why it's worth the longer road when the facts genuinely fit.

A worked example: $83,100, three years unfiled, and a hardship case

Say you're a gig worker who just caught up after three years of not filing, and the assessed balances — tax, late-filing and late-payment penalties, and interest — total $83,100. You have a chronic condition that caps how many hours you can drive. Here's the offer math, all figures hypothetical:

- Future income: $4,300/month average from the apps, minus $3,850 in IRS-allowable living expenses (including $600/month of documented out-of-pocket medical costs) = $450/month disposable. Lump-sum multiplier: $450 × 12 = $5,400.

- Condo: $235,000 market value × 80% quick-sale = $188,000, minus the $148,000 mortgage = $40,000 in countable equity.

- IRA: $52,000 balance, less roughly $14,000 in taxes and early-withdrawal costs you'd eat to liquidate it = about $38,000 counted.

- RCP: $5,400 + $40,000 + $38,000 = $83,400 — three hundred dollars more than the $83,100 you owe.

By $300, a doubt-as-to-collectibility offer is off the table: the formula says you can full-pay. But look at what "full pay" actually requires — selling your only housing and draining the only retirement account you'll ever have, while a medical condition is already shrinking your earning years. Cashing out the IRA would also detonate its own tax bill the following April, the same trap covered in our guide to the early 401(k) withdrawal tax bill.

That's a textbook ETA fact pattern. A credible offer here might be $16,000 — a $12,800 family loan plus what your budget can absorb — submitted with the 20% down payment ($3,200) and a hardship file: the diagnosis, a physician's statement on work limitations, twelve months of treatment invoices, and a projection of future medical costs. The offer amount isn't formula-driven; it's the number you can pay without creating the hardship you're documenting, and it has to tie back to your Form 433-A (OIC) line by line. And if your AGI is at or below 250% of the federal poverty level, the low-income certification waives the fee, the down payment, and payments during review — check it before you write any check.

How to file an effective tax administration offer, step by step

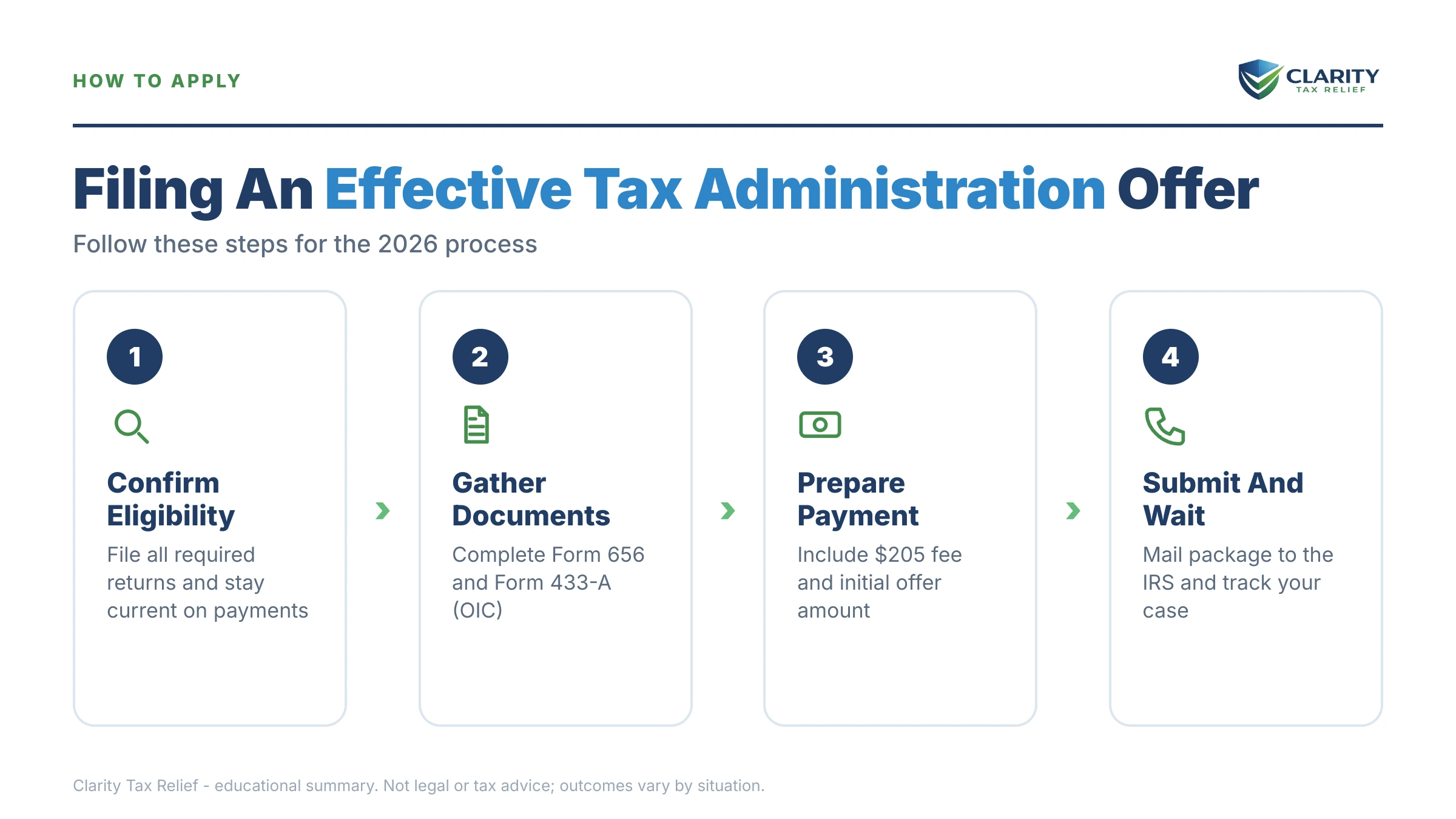

An effective tax administration offer is filed on Form 656 with Form 433-A (OIC), the $205 fee, and a documented hardship explanation — in this order:

- File every missing return — The IRS returns any offer unprocessed — and keeps the fee — if a required return is unfiled. If you have unfiled years, file them and let the assessed balances post before you submit anything.

- Run the RCP math to confirm your ground — Calculate your reasonable collection potential from your net asset equity and monthly disposable income. If RCP covers the full debt, ETA is your ground; if it falls short but paying it would still cause hardship, file as doubt as to collectibility with special circumstances instead.

- Complete Form 433-A (OIC) and Form 656 — Disclose every asset, income source, and expense on Form 433-A (OIC), then check the Exceptional Circumstances (Effective Tax Administration) box on Form 656 and attach your written hardship explanation.

- Attach third-party proof of hardship — Support every claim with documents: medical records, disability determinations, caregiver costs, appraisals, prescription and treatment bills. Assertions without evidence are the fastest route to rejection.

- Send the fee and initial payment — or the low-income certification — Include the $205 application fee and, for a lump-sum offer, 20% of your offer amount. If your AGI is at or below 250% of the federal poverty level, the low-income certification waives the fee, the down payment, and payments during review.

- Respond fast and stay compliant — Answer the offer examiner's document requests by their deadlines and stay current on this year's estimated taxes — a new balance can sink a pending offer. If rejected, appeal within 30 days on Form 13711.

For line-by-line help with the paperwork itself, see our Form 656 walkthrough and Form 433-A walkthrough.

When you can handle this yourself — and when help changes the outcome

You can file an ETA offer yourself: the forms are public, the fee is $205, and nothing about the process requires representation. DIY makes sense when your hardship is simple and self-evident — one clear medical condition, clean records, one tax year, and a paper trail you can assemble in a weekend. It also makes sense to skip ETA entirely if your real need is time, not forgiveness: a payment plan or CNC status is faster and free to request.

Experienced help earns its cost in the harder versions of this case: multiple unfiled years that have to be reconstructed from platform records before any offer can even be processed, an RCP calculation that sits within a few thousand dollars of the debt (where the offer ground itself is arguable), self-employment income the examiner will want to average and challenge, or a rejection you need to fight — hardship is a judgment call, and judgment calls are exactly what the appeals process exists to review. An OIC rejection appeal on Form 13711 must be filed within 30 days, and ETA appeals are worth taking seriously. If the IRS itself is mishandling a genuine hardship case, the Taxpayer Advocate Service is a free, independent escalation path.

Terms on Form 656, decoded

- Effective tax administration (ETA): the offer ground for taxpayers who could full-pay but shouldn't be made to, due to hardship or fairness.

- Exceptional circumstances: Form 656's label for the ETA checkbox and the explanation section that carries your hardship argument.

- Reasonable collection potential (RCP): net realizable asset equity plus 12 or 24 months of disposable income — the IRS's measure of what it could ever collect from you.

- Economic hardship: the §301.6343-1 standard — collection that leaves you unable to pay reasonable basic living expenses.

- Quick-sale value: the discounted value (typically 80% of market) the IRS assigns to assets when computing your equity.

- DCSC: doubt as to collectibility with special circumstances — the hybrid that lets you offer less than your RCP when even RCP would cause hardship.

Effective tax administration offer questions, answered

What is an effective tax administration offer in compromise?

It's the third and rarest ground for an Offer in Compromise: you concede that you owe the tax and that you could technically pay it in full, but you ask the IRS to accept less because full collection would create economic hardship or would be unfair given exceptional circumstances. It's filed on Form 656 with a complete financial disclosure on Form 433-A (OIC).

How often does the IRS accept effective tax administration offers?

Rarely — ETA acceptances are a small fraction of the roughly one-in-five offers the IRS accepted overall in FY2024. The IRS publishes no ETA-only acceptance rate, but offer examiners are trained to treat ETA as an exception, not a default. Your odds rise sharply when hardship is documented with third-party evidence — medical records, care costs, disability determinations — rather than asserted in a letter.

What counts as economic hardship for an ETA offer?

The IRS uses the levy-hardship standard in Treasury Regulation §301.6343-1: collection would leave you unable to pay reasonable basic living expenses. Classic examples are a long-term illness or disability that will exhaust your assets, assets you need to generate the income you live on, or a home whose sale would leave a disabled family member without care. Simple inconvenience or a lifestyle downgrade doesn't qualify.

Can a business file an effective tax administration offer?

Only on public policy or equity grounds — the economic hardship version of ETA is limited to individuals, because hardship is defined by a person's basic living expenses. A corporation or partnership that could full-pay must argue that collection would undermine fairness or public confidence in the tax system, which is an even higher bar. Sole proprietors file as individuals, so their business income and hardship count.

What's the difference between ETA and doubt as to collectibility with special circumstances?

The dividing line is your reasonable collection potential. If your RCP is at least the full debt, you're in ETA territory. If your RCP is below the debt but paying even that RCP would cause hardship — for example, it would require draining a retirement account you live on — you file a doubt-as-to-collectibility offer with special circumstances (DCSC) and offer less than your RCP. Both use the same hardship standard and the same forms.

Do I have to file all my back tax returns before an ETA offer?

Yes. The IRS returns any offer unprocessed if you have unfiled required returns, and it keeps your application fee. If you're a gig worker with several unfiled years, filing those returns is step one — and it fixes the balance the offer will settle, because until you file, the IRS may be working from inflated substitute-for-return numbers.

How much should I offer on an effective tax administration offer?

There's no formula like the RCP calculation used for collectibility offers. You offer the amount you can genuinely pay without creating the hardship you're documenting — often funds from a family loan, a modest asset you can spare, or payments your budget can absorb. Offer examiners expect the number to tie back to your Form 433-A (OIC); an arbitrary lowball invites rejection.

What happens if my effective tax administration offer is rejected?

You have 30 days from the rejection letter to appeal using Form 13711, and ETA cases are worth appealing — hardship judgments are subjective, and the IRS Independent Office of Appeals reverses offer examiners more often on judgment calls than on math. While the offer and appeal are pending, levies generally stay on hold, though interest keeps accruing and the collection statute is paused.

Your next 24 hours

- Pin down the exact number. Pull your IRS account transcripts or most recent notices and write down the assessed balance for each year — and note any year that still isn't filed, because no offer moves until every return is in.

- Start the hardship file. Gather last year's return, income statements from every platform that pays you, and the documents that prove your circumstances: medical bills, a diagnosis or disability letter, caregiver costs, your mortgage statement, and retirement account balances.

- Get the offer ground called correctly before you spend anything. A free case review with an experienced tax professional — (888) 825-7779 or the 2-minute form — will tell you whether your facts point to ETA, DCSC, or a faster option entirely. Interest and the monthly penalty accrue until the debt is resolved, so the sorting is worth doing now.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.