Offer in Compromise

Offer in Compromise Application Fee Waiver: Who Qualifies and How to Claim It (2026)

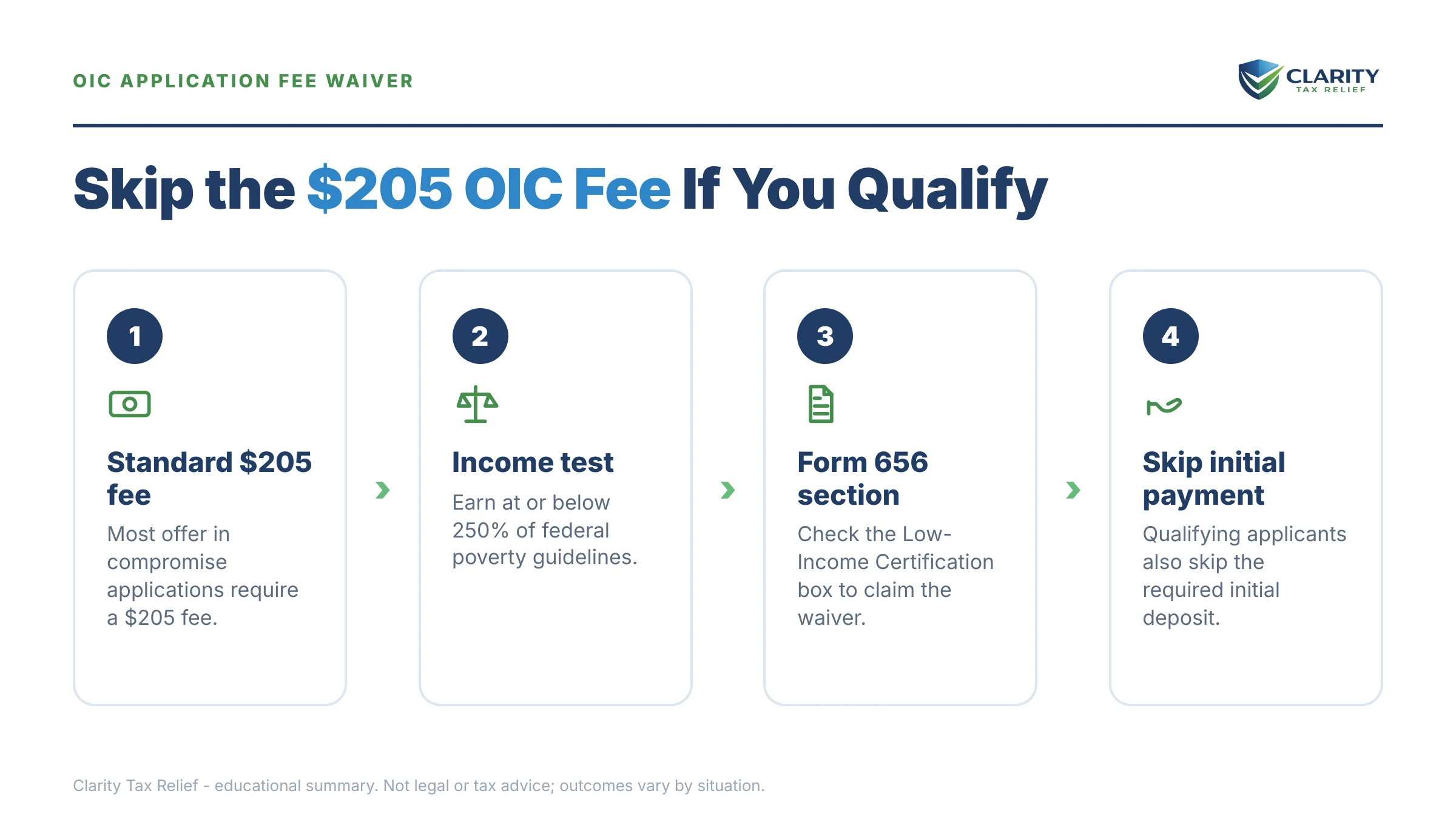

The short answer: the offer in compromise application fee waiver is the Low-Income Certification on Form 656. If your income is at or below 250% of the federal poverty guidelines for your household size, the IRS waives the $205 application fee, the 20% down payment, and every payment while your offer is under review.

You priced out an offer in compromise and the entry cost stopped you cold: $205 just to apply, plus 20% of whatever you offer, due the day the envelope goes in the mail — money that isn't refunded if the answer is no. On a fixed Social Security check, that's a lot to risk on a maybe. The IRS built a waiver for exactly this situation, and claiming it takes one checkbox.

That checkbox sits in its own labeled section of Form 656 — the visual guide below maps the key facts, deadlines, and options, so you know what you're looking for before you sign anything.

⏱ The real clock: there is no deadline to claim the fee waiver — you claim it whenever you file Form 656. But the balance underneath isn't waiting: the failure-to-pay penalty adds up to 0.5% per month, and interest accrues on top, until the debt is resolved. Every month you delay applying, the number you're trying to compromise gets bigger.

What the offer in compromise application fee waiver actually covers

The Low-Income Certification on Form 656 waives three costs at once: the $205 application fee, the 20% initial payment on a lump-sum offer, and every monthly installment while a periodic offer is under review. It is not a separate application or a letter you write — it is a section of Form 656 itself, and you claim it by checking the box and indicating which income test you pass.

The third item is the one most people miss, and it's often the biggest. On a periodic-payment offer, taxpayers without the certification must keep making their proposed monthly payments the entire time the IRS is reviewing the offer — which routinely takes many months. With the certification, you pay $0 from the day you mail the offer until the day the IRS accepts it. Here's the side-by-side:

| Cost item | Without certification | With Low-Income Certification |

|---|---|---|

| Application fee with Form 656 | $205, not refunded if rejected | $0 |

| Lump-sum offer: initial payment | 20% of the offer amount, up front | $0 |

| Periodic offer: payments during IRS review | Your proposed monthly payment, every month | $0 until acceptance |

| If the offer is rejected | Fee kept; payments applied to your balance, not returned | Nothing out of pocket to lose |

Three boundaries matter. First, the waiver does not reduce the offer amount itself — if the IRS accepts your $3,600 offer, you still pay $3,600, just on the schedule you proposed. Second, it does not change your odds of acceptance; that's decided by the financial math, covered below. Third, it's for individuals only. A corporation, partnership, or LLC taxed as one cannot claim it — a business offer in compromise pays the fee and required payments no matter how tight the company's finances are.

One quiet exception worth knowing: an offer in compromise based on doubt as to liability — where you argue you don't actually owe the assessed amount — is filed on Form 656-L and carries no fee and no down payment for anyone, at any income. The fee, and this waiver, apply only to offers based on inability to pay. (If you're new to how offers work at all, the shared background lives in our guide to how an offer in compromise actually works — this page stays focused on the waiver.)

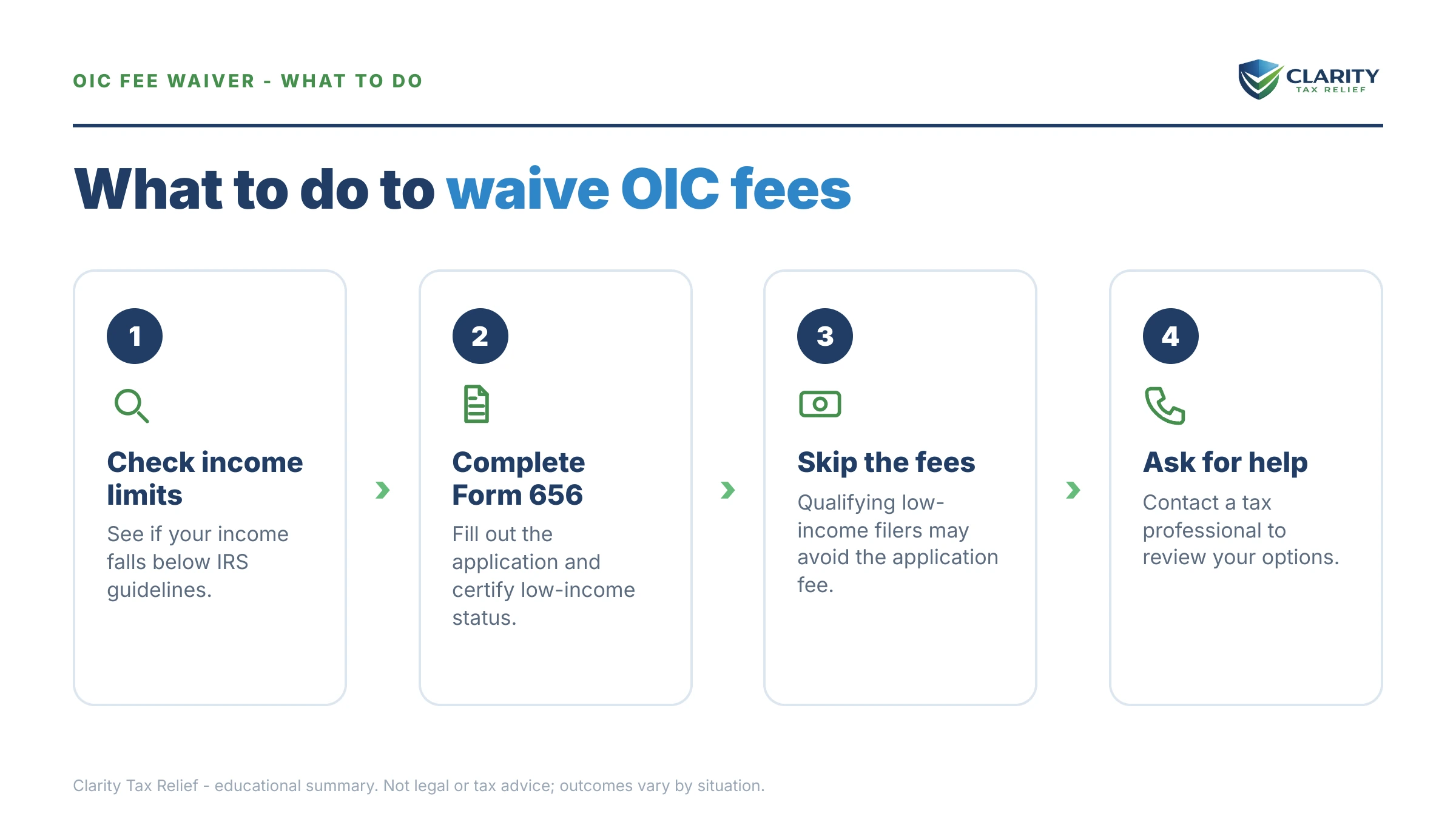

Who qualifies: the two low-income certification tests

You qualify for the OIC fee waiver if your income is at or below 250% of the federal poverty guidelines for your household size — and the IRS gives you two different ways to measure it, of which you only need to pass one.

| Test | What the IRS measures | Where the numbers come from |

|---|---|---|

| AGI test | Adjusted gross income from your most recently filed tax return, compared to 250% of poverty for your household size | Your Form 1040 AGI line vs. the table printed in the current Form 656 booklet |

| Monthly income test | Your household's gross monthly income right now, multiplied by 12, compared to the same 250% threshold | Current pay stubs and benefit statements vs. the same Form 656 table |

The dollar thresholds change every year with the poverty guidelines, run higher in Alaska and Hawaii, and scale up with household size — generally you, your spouse, and your dependents, as the Form 656 instructions define it. Always use the table in the current-year Form 656 booklet, not a figure from an old blog post or last year's form; an outdated table can make you wrongly believe you miss the cutoff.

The two-test design matters enormously for retirees. Social Security is only partially taxable — and for many retirees, none of it is — so your AGI can be dramatically lower than the gross income you actually live on. A retiree whose bank statements look borderline under the monthly test may pass the AGI test easily. If your income dropped recently (retirement, a spouse's death, losing a part-time job), the reverse applies: last year's AGI may be too high, but your current monthly income times 12 passes. Run both before concluding anything.

Two edge cases people ask about. If you and your spouse owe the same joint tax years, one Form 656 generally covers both of you — one offer, one certification, one fee waived. And if you owe both personal tax and a separate business liability, those are separate offers: the personal one can carry the certification; the business one cannot. This page's deeper companion, our guide to the OIC low income certification, walks through the household-size counting rules line by line.

What happens if the upfront cost keeps you from applying at all

Doing nothing costs far more than $205 — an unresolved IRS balance grows every month while automated collection escalates around it. This is the trap the waiver exists to prevent: people who genuinely can't pay their debt also can't spare the entry fee, so they never apply, and the balance compounds. Here's the sequence a $92,700 debt follows when it just sits:

- The balance grows monthly. The failure-to-pay penalty adds up to 0.5% per month, and interest accrues on the whole balance — penalties included.

- Every refund disappears. Any federal refund you're ever due is offset against the debt until it's resolved.

- Collection notices escalate. Annual reminders give way to intent-to-levy notices, each one adding enforcement power.

- A federal tax lien can attach to everything you own, including your home.

- Social Security gets levied. Through the Federal Payment Levy Program, the IRS can take up to 15% of your monthly benefit — continuously, without a court order.

- Bank accounts become reachable. After a final notice and your 30-day appeal window, a bank levy freezes funds for 21 days before they're sent to the IRS.

In 2026, none of this requires a human being. IRS staffing fell sharply in 2025, but the notice stream, offsets, and levy programs are automated — the machine escalates whether or not anyone ever reads your file. A pending offer, by contrast, is one of the few things that genuinely changes your account's posture while it's reviewed.

Can't spare $205 — let alone 20% down?

That's exactly who the Low-Income Certification is for. Send us your income picture and an experienced tax professional will tell you — free — whether you pass either test and what a realistic offer looks like, before another month of penalties and interest posts to your balance.

Fee waiver vs. the alternatives when you can't afford to pay the IRS

An offer in compromise is one of four realistic paths when full payment is impossible — and with the Low-Income Certification, it's the only settlement path that can cost nothing to pursue. But it isn't automatically the right one. Here's how the options line up for someone on a limited income:

| Option | Typical eligibility | Upfront cost |

|---|---|---|

| OIC with Low-Income Certification | Income ≤ 250% of poverty guidelines, plus finances showing the IRS can't collect the full debt | $0 — fee, down payment, and review-period payments all waived |

| OIC without certification | Same financial test, income above 250% of poverty | $205 fee + 20% of the offer (lump sum) or monthly payments during review |

| Currently Not Collectible (CNC) | Income covers only allowable living expenses; collection pauses but the debt remains and grows | $0 |

| Installment agreement | Balances ≤ $50,000 can be set up online for up to 72 months; larger balances need financial disclosure | Setup fee varies; reduced for low-income taxpayers. Interest and penalties continue |

| Doubt-as-to-liability offer (Form 656-L) | You have a genuine dispute about whether you owe the assessed amount | $0 — no fee for anyone |

The closest cousin is Currently Not Collectible status, and the trade-off is real: CNC costs nothing and stops collection, but the debt keeps growing and the IRS revisits your finances later, while an accepted offer actually ends the debt. Which fits depends on your assets and your collection-statute clock — our comparison of CNC vs offer in compromise works through that decision. For larger debts with other unsecured problems attached, the bankruptcy or offer in compromise question deserves its own analysis before you commit either way.

One honesty checkpoint before the math: the IRS accepted roughly 1 in 5 offers in FY2024. The waiver removes the cost of asking; it does not tilt the answer. Nobody can promise acceptance, and anyone who does is selling something.

And a state warning: if you also owe California, the FTB runs its own separate offer program with its own forms, its own financial standards, and no connection to the IRS's fee rules — never assume the federal waiver carries over. See our FTB offer in compromise guide for how California handles it.

A worked example: $92,700 in IRS debt on a Social Security income

Say you're retired, single, and owe the IRS $92,700 across two old tax years from the final years of a business that's long gone. Your only income is a $2,100 monthly Social Security benefit — $25,200 a year. You rent, you drive a 12-year-old car with about $2,400 in equity, and you keep roughly $1,200 in savings as a cushion. This is hypothetical, but the math is exactly what the IRS runs.

Step 1 — the waiver. A one-person household grossing $25,200 a year sits comfortably below the 250%-of-poverty threshold, and because much of that Social Security likely isn't taxable, the AGI test is even easier to pass. Either test works; check the box.

Step 2 — the offer math. The IRS decides offers using reasonable collection potential (RCP): what your assets are worth plus what your future income can spare. Here, monthly income of $2,100 against roughly $2,100 in allowable living expenses leaves $0 per month of future income the IRS can count. Assets: about $2,400 in car equity plus $1,200 in savings ≈ $3,600. RCP ≈ $0 + $3,600 = $3,600 — the most the IRS could realistically ever collect against a $92,700 debt. You can rough out your own numbers in a few minutes with our Offer in Compromise Calculator — it estimates, it doesn't promise.

Step 3 — what the waiver saves. Without the certification, a $3,600 lump-sum offer costs $205 + $720 (20%) = $925 due at filing — money that is not returned if the offer is rejected (it's applied to the balance instead). With the certification: $0 at filing, $0 during the entire review. If the IRS agrees $3,600 is its realistic ceiling and accepts, you pay the $3,600 on the schedule you proposed — the timing mechanics are covered in OIC payment options: lump sum vs. periodic.

Two fine-print points from the same scenario. The 10-year collection statute pauses while an offer is under review, so an offer that fails can leave the IRS more time to collect — part of why the numbers should be checked before filing, not after. On the other side of the ledger, the law also protects you from limbo: if the IRS doesn't decide within 2 years, the offer is deemed accepted automatically — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

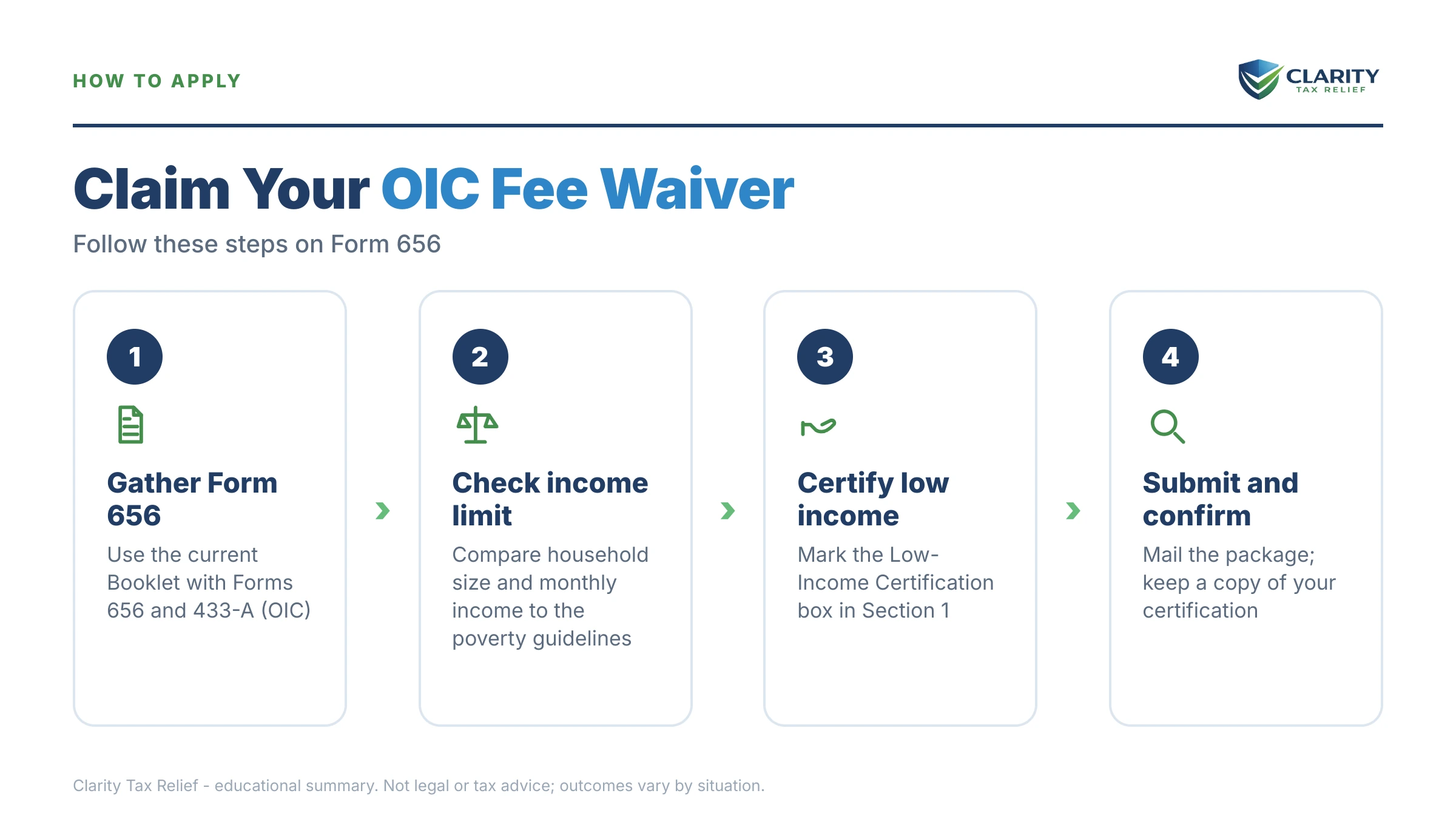

How to claim the OIC fee waiver, step by step

- Run both low-income tests. Use the 250%-of-poverty table printed in the current Form 656 booklet and check both your AGI and your household gross monthly income times 12 — you only need to pass one.

- Complete Form 433-A(OIC). Document your household income, expenses, and assets — this same package supports both your offer amount and your certification.

- Check the Low-Income Certification box. Mark the certification in its labeled section of Form 656 and indicate which test you pass.

- Mail the offer package without payment. Send Form 656, Form 433-A(OIC), and your supporting documents without the $205 fee and without any down payment or monthly installments.

- Respond to every IRS request on time. Answer each document request by its stated deadline while your offer is under review — missed deadlines get offers returned, not rejected, with no appeal.

The forms are the whole game here. Our Form 656 walkthrough covers the offer form section by section, and the Form 433-A walkthrough shows how the financial statement translates into the numbers the IRS actually uses. Precision matters more than speed: a returned offer for missing pages restarts everything.

When you can handle this yourself — and when help changes the outcome

Plenty of people in this situation can file a waiver-backed offer on their own, and you should know that before anyone charges you a dime. If your income is a single Social Security deposit, your assets are a car and a small bank account, all your returns are filed, and you're comfortable working through two IRS forms carefully, the DIY path is genuinely open. Start with the IRS's own Offer in Compromise Pre-Qualifier tool to sanity-check your numbers. And if your income qualifies you for the fee waiver, it very likely qualifies you for free professional representation too — a Low Income Taxpayer Clinic can handle an offer at no charge, and the Taxpayer Advocate Service exists for cases stuck in the machinery.

Experienced help changes outcomes in specific situations, not all of them: multiple years including unfiled returns (an offer can't be processed until everything's filed); home equity or retirement accounts that inflate your RCP unless valued and argued correctly; money given away or spent down in recent years, which the IRS can add back as dissipated assets; a levy already hitting your Social Security, where sequencing the levy release and the offer matters; and a prior offer that came back rejected, where the fix is usually in the math, not the paperwork — see OIC rejected — now what for how appeals and refiling work. If your case is simple, keep your money. If it has any of those wrinkles, a review before filing is cheaper than a rejection after.

Terms on Form 656, decoded

- Low-Income Certification — the section of Form 656 that waives the application fee, down payment, and review-period payments when your income is at or below 250% of the federal poverty guidelines.

- AGI (adjusted gross income) — the income figure from your tax return after certain deductions; for retirees it often excludes most Social Security, which is why it's frequently the easier test.

- Reasonable Collection Potential (RCP) — the IRS's calculation of what it could realistically collect from you: asset equity plus countable future income. Offers at or above RCP get accepted; offers below it get rejected.

- Lump-sum vs. periodic offer — a lump-sum offer is paid in a few payments shortly after acceptance and normally requires 20% down at filing; a periodic offer spreads payments monthly and normally requires payments during review. The certification waives both requirements.

- TIPRA payments — the IRS's shorthand for those required upfront and review-period payments, named for the 2005 law that created them; "TIPRA waived" on your file means your certification was honored.

- Returned vs. rejected — a rejected offer was reviewed and denied, and you can appeal; a returned offer was never reviewed (missing forms, unfiled returns, unpaid required fees) and carries no appeal rights. The certification prevents the most common return reason for low-income filers: missing money.

Not sure your finances fit the two tests, or whether an offer beats CNC for your numbers? An experienced tax professional can run both in one free call — request a case review or dial (888) 825-7779.

OIC fee waiver questions, answered

How much is the offer in compromise application fee in 2026?

The application fee is $205 in 2026, paid when you mail Form 656. It is waived entirely if you qualify for the Low-Income Certification — income at or below 250% of the federal poverty guidelines for your household size. Doubt-as-to-liability offers, filed on Form 656-L, carry no application fee for anyone.

Who qualifies for the OIC application fee waiver?

Individual taxpayers whose income falls at or below 250% of the federal poverty guidelines for their household size and state. You can pass with either your adjusted gross income from your most recent return or your current household gross monthly income multiplied by 12 — only one test needs to work. Businesses like corporations and partnerships cannot claim the certification.

Does the fee waiver also cover the 20% down payment?

Yes. The Low-Income Certification waives the $205 fee, the 20% initial payment on a lump-sum offer, and the monthly installments otherwise required while a periodic offer is under review. You pay nothing until the IRS accepts your offer — then you pay the offer amount itself on the schedule you proposed.

Is the $205 OIC fee refundable if my offer is rejected?

No. The application fee and any required payments are not returned if your offer is rejected — payments are applied to your tax balance instead. That's why the certification matters so much on a tight budget: qualifying means you risk nothing out of pocket to find out whether the IRS will accept your offer.

Does claiming low-income certification hurt my chances of acceptance?

No. The certification only controls what you pay to apply; acceptance is decided by the reasonable collection potential math on Form 433-A(OIC). In practice, the low income that qualifies you for the waiver often supports a lower offer too, because it usually means little future income the IRS can count.

Do I have to send proof of income with the certification?

You don't attach separate proof for the checkbox itself, but your Form 433-A(OIC) already documents household income with pay stubs, benefit statements, and bank records. The IRS checks your certification against that package. If it disagrees, it will contact you to request the fee and required payments before continuing.

Can a business claim the OIC fee waiver?

No. The Low-Income Certification is available only to individuals, including sole proprietors filing on their personal liability. A corporation, partnership, or LLC taxed as one must pay the $205 fee and required payments with its offer. Business offers also face stricter review, especially when payroll taxes are involved.

Does Social Security count toward the 250% income limit?

For the monthly-income test, yes — household gross monthly income includes Social Security benefits. For the AGI test, only the taxable portion of your benefits appears in adjusted gross income, and for many retirees little or none of it is taxable. That's why retirees often pass the AGI test even when their gross income looks borderline.

What happens if I claim the waiver but don't actually qualify?

The IRS reviews the certification when it screens your offer for processability. If it decides you don't qualify, it will notify you and ask for the $205 fee and any required payments; if you don't send them, your offer can be returned without review. An honest, documented claim is never penalized — just verified.

Is there any fee for a doubt-as-to-liability offer?

No. Offers based on doubt as to liability — arguing you don't actually owe the assessed amount — are filed on Form 656-L and carry no application fee and no down payment for anyone, regardless of income. The fee and the low-income waiver only apply to Form 656 offers based on inability to pay.

Your next 24 hours

- Find your AGI. Pull your most recent tax return, note the adjusted gross income line, and compare it against the 250%-of-poverty table in the current Form 656 booklet on the IRS's Offer in Compromise page.

- Gather your income picture. Your Social Security benefit statement (or award letter), your last three months of bank statements, your most recent return, and any IRS notice showing the balance — that's everything both tests and Form 433-A(OIC) need.

- Get the numbers checked free. Fill out the 2-minute case review form or call (888) 825-7779 — an experienced tax professional will confirm whether you pass a certification test and whether an offer beats your alternatives, before another month of penalties and interest lands on the balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.