Offer in Compromise

Does an OIC Remove a Tax Lien? Lien Handling During and After an Offer in Compromise (2025)

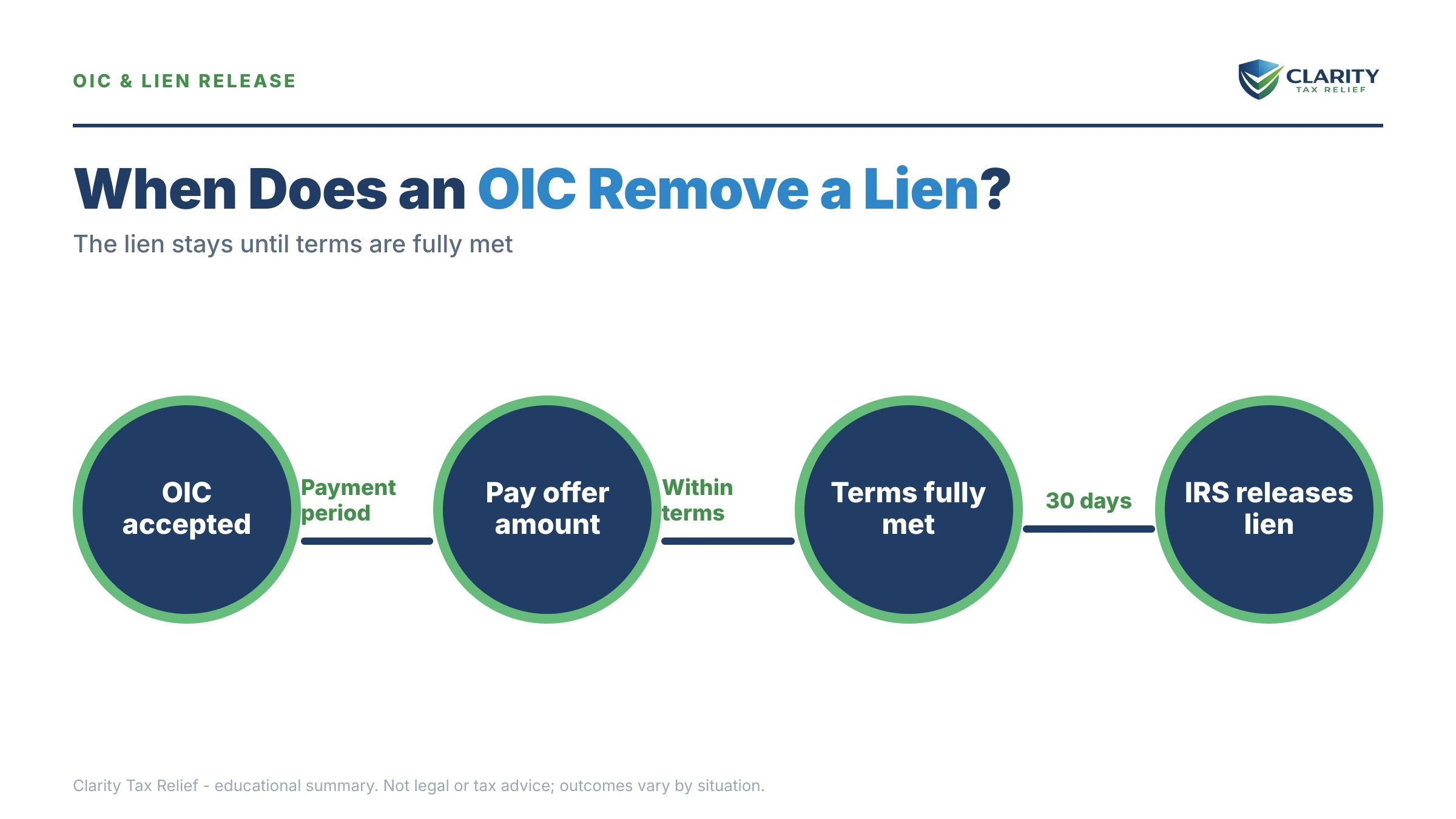

The short answer: no — an Offer in Compromise (OIC) does not remove a federal tax lien by itself. The IRS keeps the lien in place while your offer is pending, and only releases it after your accepted offer is paid in full. Release normally happens within 30 days of your final payment.

Not sure if an OIC even fits your situation?

An offer is real — but anyone promising to settle your debt for "pennies on the dollar" before reviewing your finances is selling you something. An experienced tax professional will look at your actual numbers and tell you, honestly, whether you qualify and what happens to your lien along the way. Free, confidential, no pressure.

⏱ The timeline that matters: once your accepted OIC is fully paid, the IRS is required to release the federal tax lien within 30 days. A lien withdrawal (which erases the public filing) is separate — you must request it on Form 12277, and there's no automatic deadline for that.

Why the lien is still there during your OIC

A federal tax lien is the government's legal claim against everything you own once you owe back taxes and don't pay after a demand. It is not the same as a levy — a lien is a claim, a levy is a seizure (we break down the difference in our guide to lien vs. levy). When you file an OIC, you're asking the IRS to settle the debt for less than the full amount. Until that debt is actually satisfied, the IRS has every reason to keep its claim in place.

So even a strong, well-documented offer leaves the lien standing while the IRS reviews it. Submitting Form 656 doesn't lift the lien, and acceptance alone doesn't lift it either. The lien comes off only when you finish paying the agreed amount. You can read the IRS's own rules on the Offer in Compromise page and on understanding a federal tax lien.

Will the IRS file a new lien while my offer is pending?

It can — and on larger balances, it often does. The IRS may file a Notice of Federal Tax Lien (the public document, sent to you on Letter 3172) to protect the government's interest while your offer is under review. Filing an OIC does not block a new lien filing.

Here's the good news that balances that out: while your offer is being processed, the IRS generally pauses levies. So a pending OIC can stop the IRS from grabbing your bank account or wages, even though it doesn't stop a lien from being recorded.

What happens to the lien at each stage

Walking it through in order makes this much less scary. Here is the lien's life cycle around an OIC:

- You submit the OIC. The lien (if one exists) stays. The IRS may still file a new lien, but it generally holds off on levies.

- The OIC is under review. Months can pass. The lien remains a matter of public record the whole time. Nothing about the offer removes it.

- The OIC is accepted. Big step — but the lien is still in place. Acceptance is a promise to pay; the lien protects the IRS until you actually do.

- You finish paying the accepted amount. Now the debt is satisfied. The IRS is required to release the lien within 30 days.

- You request a withdrawal (optional). Release closes the lien; a withdrawal on Form 12277 erases the public filing as if it never happened. You have to ask for this — it is not automatic.

One more thing worth knowing: an accepted OIC includes a five-year compliance term. You must file and pay on time for the next five years. The lien is gone after payment, but a default during those five years can revive the original liability.

Release vs. withdrawal: the distinction that matters most

People searching "does OIC remove tax lien" usually want one real-world outcome: a clean title and a clean record. So understand these two different actions:

- Lien release — the IRS closes out the lien because the debt is satisfied. The public record still shows the lien was filed and then released. This happens automatically within 30 days of full payment. Our guide on how long the IRS takes to release a tax lien walks through what to expect.

- Lien withdrawal — the IRS removes the Notice of Federal Tax Lien as if it had never been filed. This is the cleaner result for property and title searches, but you have to qualify and request it using Form 12277 (IRS instructions are on the About Form 12277 page).

For most people who complete an OIC, the goal is: finish paying, get the release, then file Form 12277 to ask for the withdrawal. That last step is what gives you the cleanest paper trail.

Other lien tools while you're mid-process

If the lien is causing a specific problem before your OIC is done, there are targeted fixes — none of which require you to pay the whole debt first:

- Discharge of property (Form 14135) — removes the lien from one specific piece of property, useful if you're selling a house.

- Subordination (Form 14134) — lets another creditor move ahead of the IRS, which can make refinancing possible.

These don't erase the lien, but they can unstick a sale or refinance while your offer works through the system.

See your likely offer amount in about 2 minutes

Before you decide anything, our free Offer in Compromise Calculator runs your income, expenses, and assets through the same Reasonable Collection Potential formula the IRS uses to estimate the lowest amount the IRS may accept to settle your debt. No sign-up, instant result.

Estimate my offer →How to handle the lien around your OIC, step by step

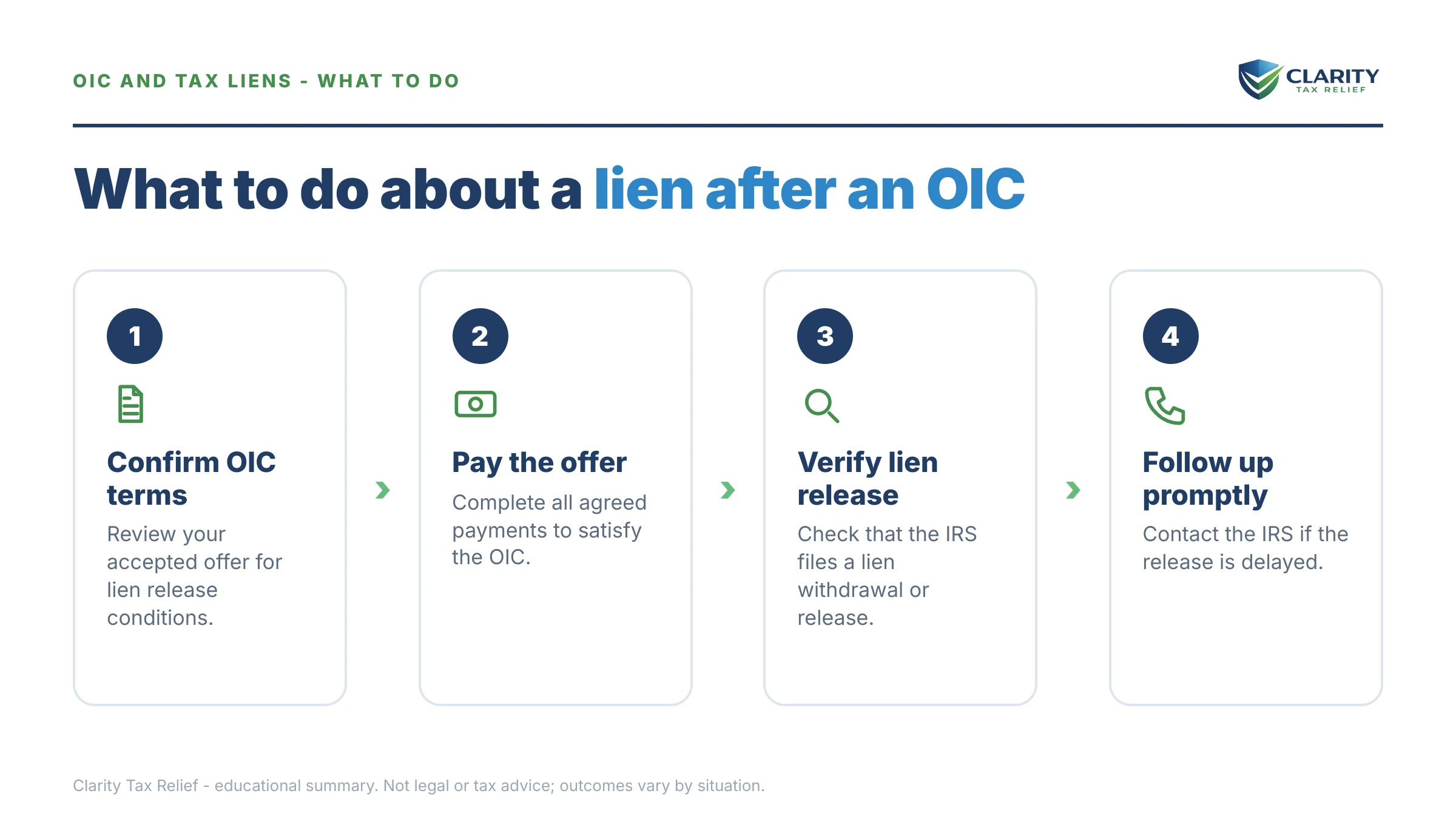

- Confirm the lien exists. Check your IRS online account and look for Letter 3172. Not everyone who owes has a recorded lien.

- Decide whether the OIC is the right path. Read how an offer in compromise actually works and run the math before you spend money pursuing one.

- Submit a complete, well-documented offer. A pending OIC generally pauses levies even though the lien stays.

- Pay the accepted amount in full and on time. Whether lump sum or periodic, finishing payment is what triggers the lien release.

- Confirm the release. The IRS should release the lien within 30 days. If it doesn't show, request it in writing.

- File Form 12277 to request a withdrawal. This is the step that erases the public filing — and the one most people forget.

- Stay compliant for five years. File and pay on time so your settled offer doesn't default and revive the debt.

Does an OIC remove a tax lien? Your questions, answered

Does an offer in compromise remove a tax lien?

Not on its own. While your offer is pending, the federal tax lien stays in place. The IRS only releases the lien after your accepted offer is fully paid and you've met the offer's terms. Acceptance alone doesn't lift it — completion does.

Will the IRS file a lien while my OIC is pending?

It can. The IRS often files a Notice of Federal Tax Lien to protect the government's interest while it reviews your offer, especially on larger balances. Submitting an OIC does not block a lien filing, though it does generally pause levies while the offer is under review.

How long after an accepted OIC is the lien released?

The IRS is required to release a federal tax lien within 30 days after the liability is satisfied. With a lump-sum OIC that's 30 days after your final payment clears; with a periodic-payment OIC it's after your last scheduled payment posts. You can request the lien release if it doesn't appear.

What is the difference between a lien release and a lien withdrawal?

A release closes out the lien once the debt is satisfied, but the public record shows it was filed and then released. A withdrawal, requested on Form 12277, removes the Notice of Federal Tax Lien as if it had never been filed. Withdrawal is better for your credit and title records, but you must qualify and ask for it.

Will the tax lien come off my credit report after the OIC?

The three major credit bureaus stopped including tax liens on consumer credit reports in 2018, so a federal tax lien generally won't show on your score today. It can still appear in public records and title searches, which is why a lien withdrawal matters when you're buying or selling property.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.