Offer in Compromise

OIC Future Income: How the IRS Calculates What You Can Pay (2026)

The short answer: the IRS calculates OIC future income by subtracting your allowable living expenses from your average gross monthly income, then multiplying what's left by 12 (lump-sum offer) or 24 (periodic-payment offer). That number, added to your net asset equity, sets the minimum offer the IRS will accept.

A levy warning is on your counter, you rent, you own almost nothing worth seizing — and you keep reading that the IRS settles for "what it can collect." For a renter, what it can collect is almost entirely one number: your future income. This page shows exactly how the IRS computes that number, line by line.

Every figure in the calculation comes off one worksheet — Form 433-A(OIC) — and the image below shows you exactly what that document looks like and where your future income number lands, so you can follow the same math the offer examiner will run.

⏱ Your real clock: there's no filing deadline for an offer — but interest and the 0.5% monthly failure-to-pay penalty keep growing your balance until it's resolved. If you've received an LT11 or Letter 1058 final levy notice, you have 30 days from its date to request a Collection Due Process hearing (Form 12153) — and once a processable offer is pending, the IRS generally may not start new levy action.

Why OIC future income decides most of your offer

Future income is usually the largest component of Reasonable Collection Potential — the figure the IRS compares your offer against. Your Reasonable Collection Potential (RCP) has two parts: the quick-sale value of your assets, plus what the IRS believes it could collect from your paychecks going forward. Homeowners fight the battle on equity. Renters fight it almost entirely on the income side.

That's actually the opportunity in your situation. With no house and little equity, your offer amount rises or falls almost dollar-for-dollar with your monthly disposable income — so every legitimate expense you document, and every income assumption you correct, changes the bottom line directly.

The IRS doesn't take your word for the expense side. It measures your spending against its published Collection Financial Standards — the IRS allowable living expenses standards — which cap what counts for housing, food, transportation, and other categories. If the whole OIC framework is new to you, the hub guide on how an offer in compromise works covers the program end to end; this page stays on the income math. You can also estimate your own numbers in a few minutes with our Offer in Compromise Calculator — it estimates, it doesn't decide, but it tells you whether the math is even in the neighborhood.

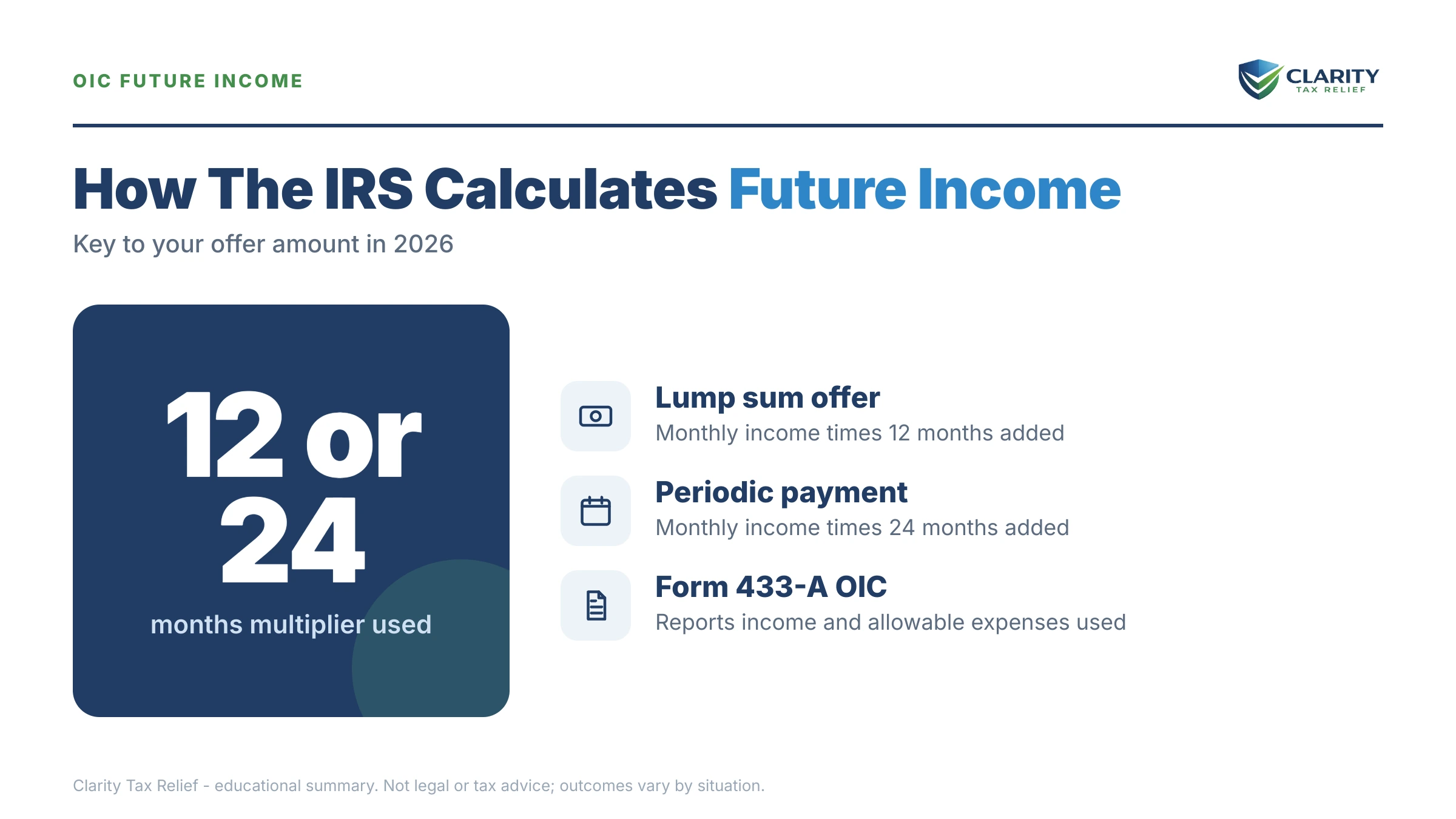

The multiplier: 12 months vs. 24 months of future income

A lump-sum offer counts 12 months of your disposable income; a periodic-payment offer counts 24. That single choice on Form 656 can double the future-income side of your offer, which is why most people who can scrape together a lump sum choose it. (Older articles cite 48 or 60 months — those multipliers died with the 2012 Fresh Start changes.)

| Offer type | Future income counted | Cost at filing | Payment timeline |

|---|---|---|---|

| Lump-sum (Form 656) | 12 × monthly disposable income | $205 application fee + 20% of the offer (both waived with low-income certification) | Balance in 5 or fewer payments within 5 months of acceptance |

| Periodic-payment (Form 656) | 24 × monthly disposable income | $205 fee + first monthly payment; payments must continue through review (waived with low-income certification) | 6–24 monthly payments, finished within 24 months of acceptance |

Two cost notes before you pick. First, the 20% down payment and the monthly payments during review are not refundable — if the offer fails, they're applied to your balance, as covered in oic down payment refundable. Second, if your AGI is at or below 250% of the federal poverty guidelines, oic low income certification waives the fee, the down payment, and payments during review — for a renter on a tight budget, that can be the difference between filing and not filing.

What counts as income — and which expenses the IRS allows

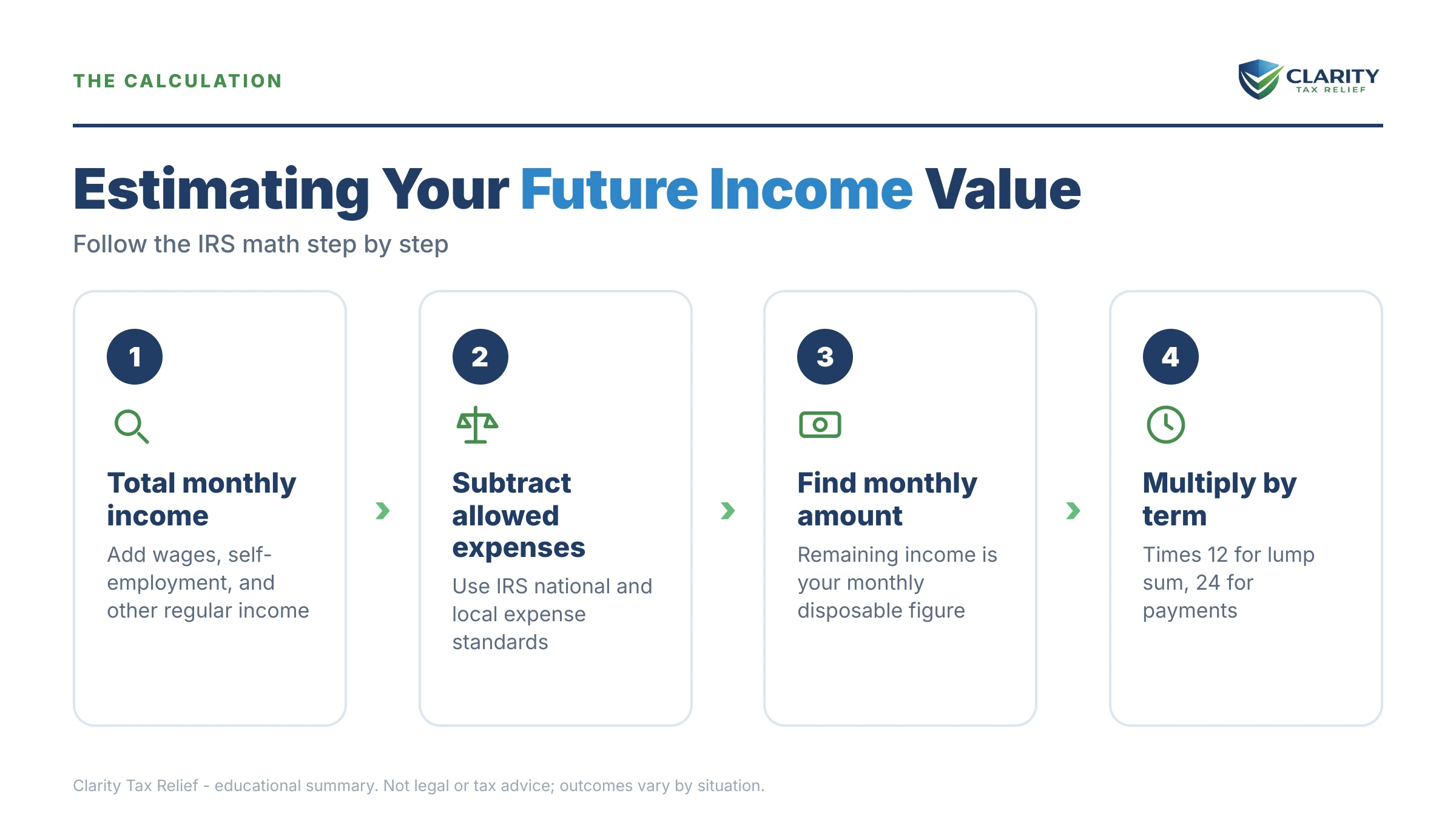

The IRS starts from gross monthly income, averaged over your recent pay history, not your take-home pay. On Form 433-A(OIC) that includes wages, self-employment net profit, rental income, pensions, Social Security, alimony and child support received, and regular side income. The examiner will cross-check your bank statements, so "forgetting" a Venmo side gig doesn't work — it just costs credibility. (The Form 433-A walkthrough covers the form box by box.)

On the expense side, three different rules apply depending on the category:

- National standards, no receipts needed: food, clothing, housekeeping supplies, and miscellaneous get a fixed allowance by household size — you can claim the full standard even if you spend less.

- Local standards, capped: housing/utilities and transportation are limited to your county's published cap. Rent above the local standard generally gets cut down to the cap — a common, painful surprise for renters in expensive metros.

- Actual amounts, documented: current tax withholding, health insurance, out-of-pocket medical costs, court-ordered payments (child support, restitution), and term life insurance count at what you actually pay — with proof.

What generally does not count: credit card minimums, private school tuition, voluntary 401(k) contributions, and payments on unsecured personal loans. The examiner strips those out, which is how people who "have nothing left each month" end up with disposable income on paper.

Worked example: $27,500 owed, renting, levy warning in hand

Say you owe $27,500 across two tax years, you rent, and an LT11 just arrived. This is hypothetical, but the arithmetic is exactly what an examiner runs:

- Gross monthly income: $4,600 (averaged from three months of pay stubs).

- Allowable expenses: $1,750 rent + utilities (at the local cap), $800 national standard for food/clothing/misc, $900 vehicle ownership and operating costs, $250 health insurance, $580 current tax withholding = $4,280.

- Monthly disposable income: $4,600 − $4,280 = $320.

- Future income, lump-sum: $320 × 12 = $3,840. Periodic: $320 × 24 = $7,680.

- Asset side: $1,400 in checking minus the $1,000 exclusion = $400; car worth $8,000 at quick-sale value (~$6,400) minus a $6,500 loan = $0 equity.

- RCP, lump-sum offer: $3,840 + $400 = $4,240 — versus $8,080 on a periodic offer.

On these facts, a $4,240 lump-sum offer against a $27,500 debt is what the formula produces. Filing it costs the $205 fee plus 20% down ($848) — or nothing up front with low-income certification. None of this makes acceptance automatic: the examiner verifies every line, and the IRS accepted roughly one in five offers in FY2024 (current numbers in offer in compromise acceptance rate 2026). But it shows why the future-income lines are where the case is won or lost — shift disposable income from $320 to $600 and the lump-sum offer jumps from $4,240 to $7,600.

What happens if your future income numbers don't hold up

An offer built on numbers the IRS can't verify doesn't get negotiated — it gets returned or rejected, and collection resumes with months of extra interest attached. The sequence runs in stages:

- Returned offer. If your offer isn't "processable" — unfiled returns, missing documentation, a skipped periodic payment — the IRS sends it back with no appeal rights. Your fee and any payments made are kept and applied to the balance.

- Rejected offer. If the examiner's math says you can pay more, you get a rejection letter showing the IRS's own income calculation, and transcript code 481 posts to your account.

- 30-day appeal window. You have 30 days from the rejection letter to appeal — see form 13711 oic appeal. Appeals officers regularly correct examiner errors on income averaging and expense caps.

- Collection resumes. No appeal, and the case goes back to collections where it paused — for you, that means the levy path picks up again, now with the interest that accrued during review added on.

- A longer collection runway. The 10-year collection statute was paused while your offer was pending, plus 30 days — so a failed offer leaves the IRS with more time to collect, not less.

Levy notice in hand and running the OIC math?

Before the 30-day window on a final levy notice closes, have an experienced tax professional check your future-income numbers — a free review tells you what the formula says your offer would be, and whether an offer is even your best move.

Legitimate ways to lower the future-income side of your offer

You can't invent expenses, but the formula has real levers most first-time filers miss:

- Choose lump-sum when possible. Cutting the multiplier from 24 to 12 halves the future-income component — in the example above, a $3,440 difference.

- Claim every actual-expense category. Out-of-pocket medical, court-ordered payments, and current-year estimated taxes are routinely left off Form 433-A(OIC) by DIY filers.

- Average income honestly but favorably. If your hours were just cut permanently, document it — otherwise the examiner may project future income from your old, higher pay.

- Time the filing. An offer submitted one month after a genuine, documented income drop reads very differently from one submitted the month before a scheduled raise.

- Don't burn assets first. Emptying savings on non-essentials before filing can be added back as dissipated assets oic — raising your RCP instead of lowering it.

And be honest about fit: if your disposable income times 12 already exceeds what you owe, the formula says you can full-pay, and an offer will be rejected. In that case a payment plan — or a partial-pay arrangement or hardship status if the budget genuinely doesn't stretch — beats spending months on an offer the math dooms. Self-employed readers have an extra layer of income-averaging rules covered in oic self employed.

Tracking your offer on your IRS transcript

Once the IRS accepts your offer as processable, a transaction code posts to your account transcript — and the codes that follow tell you the outcome before any letter arrives.

| Transcript code | What it means | What to do |

|---|---|---|

| Code 480 | Your offer is pending review; new levy action is generally suspended and the collection statute is paused. | Keep filing and paying current-year taxes on time, keep periodic payments going, and respond fast to examiner requests. |

| Code 481 | The offer was rejected — usually because the IRS's RCP calculation came in above your offer amount. | Compare the rejection letter's income figures to yours; appeal within 30 days with Form 13711 if they're wrong. |

| Code 482 | The offer was withdrawn — by you, or treated as withdrawn after a missed requirement. | Collection resumes; decide quickly between refiling a corrected offer and moving to a payment plan or hardship status. |

Timelines vary case by case, but reviews commonly run many months — how long does an offer in compromise take maps the full path from submission to decision.

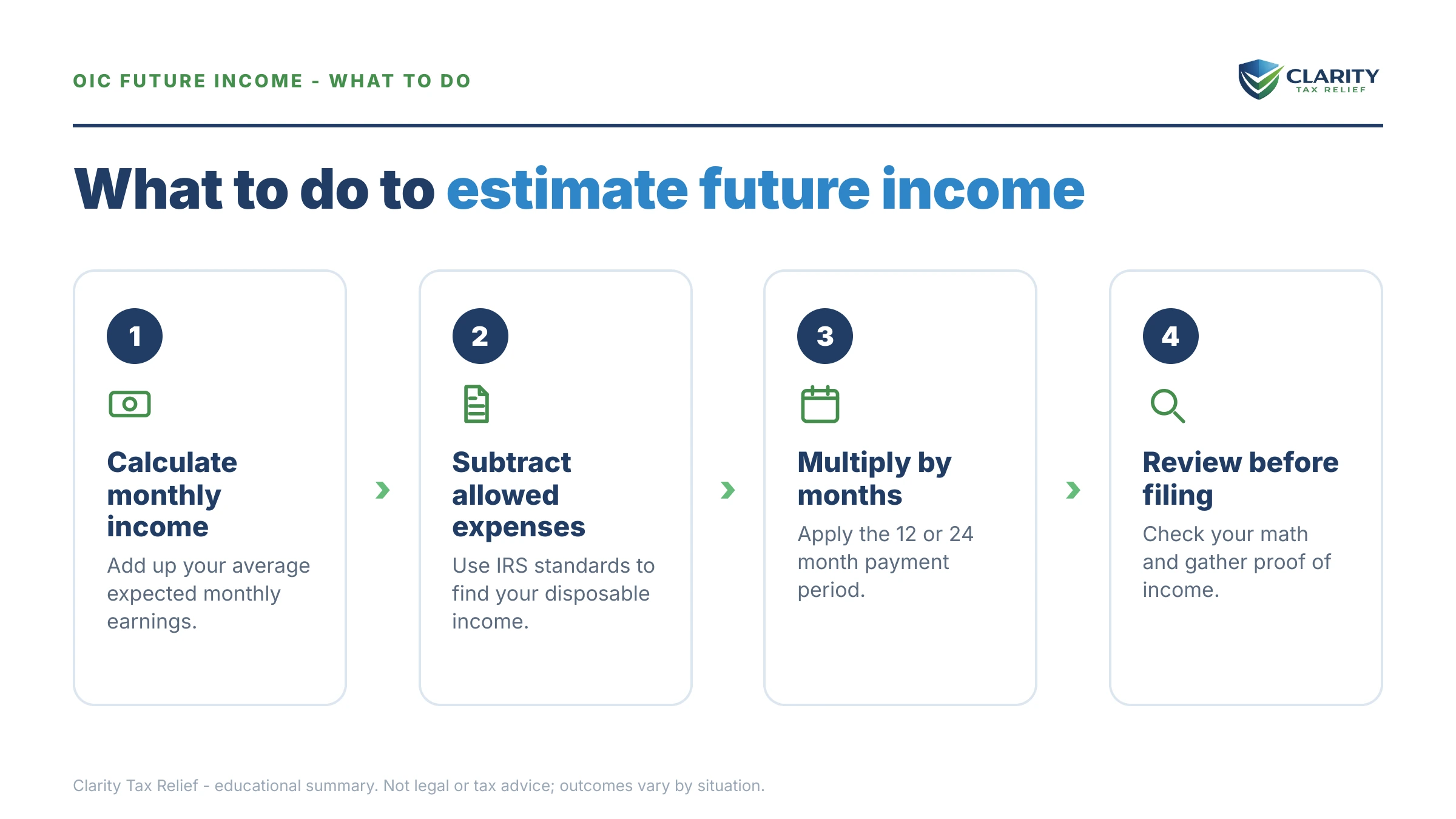

How to calculate your OIC future income, step by step

- Gather three months of income proof. Collect pay stubs, bank statements, and — if you're self-employed — a profit-and-loss statement covering the most recent three months.

- Average your gross monthly income. Total the three months and divide by three. Include wages, side income, rental income, and regular support payments — the IRS will find them on your bank statements anyway.

- List your monthly expenses against the IRS standards. Use the national standards for food, clothing, and miscellaneous; the local standards for housing, utilities, and transportation; and your actual amounts for health care, current taxes, and court-ordered payments.

- Subtract expenses from income. Gross monthly income minus total allowable expenses equals your monthly disposable income — the single number the multiplier applies to.

- Multiply by 12 or 24. Use 12 if you can pay the offer within five months of acceptance (lump sum); use 24 if you need up to two years of monthly payments (periodic).

- Add your net asset equity. Future income plus the quick-sale value of your assets equals your Reasonable Collection Potential — the minimum offer the IRS will accept.

When you can run this math yourself — and when help changes the outcome

If you have one W-2 job, steady pay, simple expenses, and no levy in motion, you can genuinely work Form 433-A(OIC) yourself — the standards are published, and the arithmetic on this page is the whole formula. The official program page at IRS.gov: Offer in Compromise includes a pre-qualifier tool worth running first, and if money is tight, the Taxpayer Advocate Service can point you to free clinic help.

Experienced help earns its cost in narrower situations: a levy already served or a final notice clock running, self-employment or commission income that needs careful averaging, a spouse who doesn't owe but shares the household budget, a prior rejection you're appealing, or income the IRS is likely to project from old, higher earnings. Those are exactly the cases where the examiner's version of your future income and your version diverge by thousands of dollars — and where the difference is argued with documentation, not hope.

Terms on Form 433-A(OIC), decoded

- Reasonable Collection Potential (RCP): net asset equity plus future income — the IRS's floor for an acceptable offer.

- Future remaining income: the formal name for the multiplied disposable-income figure on the offer worksheet.

- Monthly disposable income: gross monthly income minus allowable living expenses; the number the 12/24 multiplier applies to.

- Allowable living expenses: spending the IRS permits, capped by its national and local Collection Financial Standards.

- Quick-sale value: what an asset would fetch in a fast sale — typically about 80% of market value — used on the asset side of RCP.

- Collateral agreement: a side agreement letting the IRS collect extra if your income rises sharply after acceptance.

OIC future income questions, answered

How many months of future income does the IRS count for an OIC?

Twelve months for a lump-sum offer (paid in five or fewer payments within five months of acceptance) and 24 months for a periodic-payment offer (paid in six to 24 monthly payments). Before the 2012 Fresh Start changes it was 48 and 60 months, which is why older articles show much bigger numbers. If the IRS expects your income to jump — a degree finishing, a business recovering — it can ask for a collateral agreement that captures part of that future increase.

Does the IRS use gross or net income for an OIC?

The calculation starts with gross monthly income, not take-home pay. Your tax withholding isn't ignored, though — current federal, state, and FICA taxes are an allowable expense line, so they come out on the expense side of Form 433-A(OIC). If you're self-employed, you start with net business income after ordinary and necessary business expenses, then subtract personal allowable expenses from there.

Does my spouse's income count in my OIC future income calculation?

If only you owe the debt, the IRS still asks for household income and expenses — not to take your spouse's pay, but to prorate shared expenses like rent so you only claim your fair share. That proration can raise your disposable income even when your spouse's paycheck is untouchable. In community-property states the rules are tighter and a spouse's income can factor in more directly.

What if my income changes after I submit my offer?

The offer examiner verifies your income during review, which often runs many months — so they may work from newer pay stubs than the ones you filed. A significant raise can push your Reasonable Collection Potential above your offer and lead to a rejection or a counteroffer. If your income drops, send updated documentation to the examiner; a lower verified income supports a lower offer.

Can the IRS use a higher income than I actually earn right now?

Yes. If your current income looks temporarily low — a recent layoff, a slow season, reduced hours — the examiner can base future income on your earning capacity, often your recent earnings history. If your lower income is the new normal, document why: age, health, an industry change, or a permanent move to lower-paid work. Without that proof, expect the IRS to run the math on what you used to make.

Does a pending offer in compromise stop a levy?

Generally yes — while a processable offer is pending, the IRS generally may not start new levy action, and your transcript will show code 480. A levy already in place isn't automatically released, though; you or your representative must ask the IRS to release it. If your offer is returned as not processable, that protection ends and collection resumes.

What happens if the IRS doesn't decide my offer within two years?

By law, an offer the IRS fails to decide within two years of submission is deemed accepted — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. In practice this is rare — most offers are decided well inside that window — so don't build a strategy around running out the clock. The two-year rule matters mainly as a backstop that keeps your case from sitting in limbo forever.

Do I have to keep paying while the IRS reviews a periodic offer?

Yes — with a periodic-payment offer, you must keep making the proposed monthly payments during the entire review, and missing one can get the offer returned without appeal rights. Those payments are not refundable; they're applied to your tax balance either way. The exception is low-income certification (AGI at or below 250% of the federal poverty guidelines), which waives payments during review along with the fee.

Your next 24 hours

- Find your date. If a final levy notice (LT11 / Letter 1058) is in the stack, locate the notice date — your 30-day hearing window runs from that day, not from when you opened it.

- Gather the income file. Three months of pay stubs, three months of bank statements, your last filed return, and your monthly bills — that's everything the future-income calculation needs.

- Get the math checked free. Send it through the 2-minute form at claritytaxrelief.com/#consult or call (888) 825-7779 — an experienced tax professional will run your disposable-income numbers and tell you what the formula says before you spend a dollar filing.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.