Offer in Compromise

Will the IRS Keep My Refund After an Offer in Compromise? (2026)

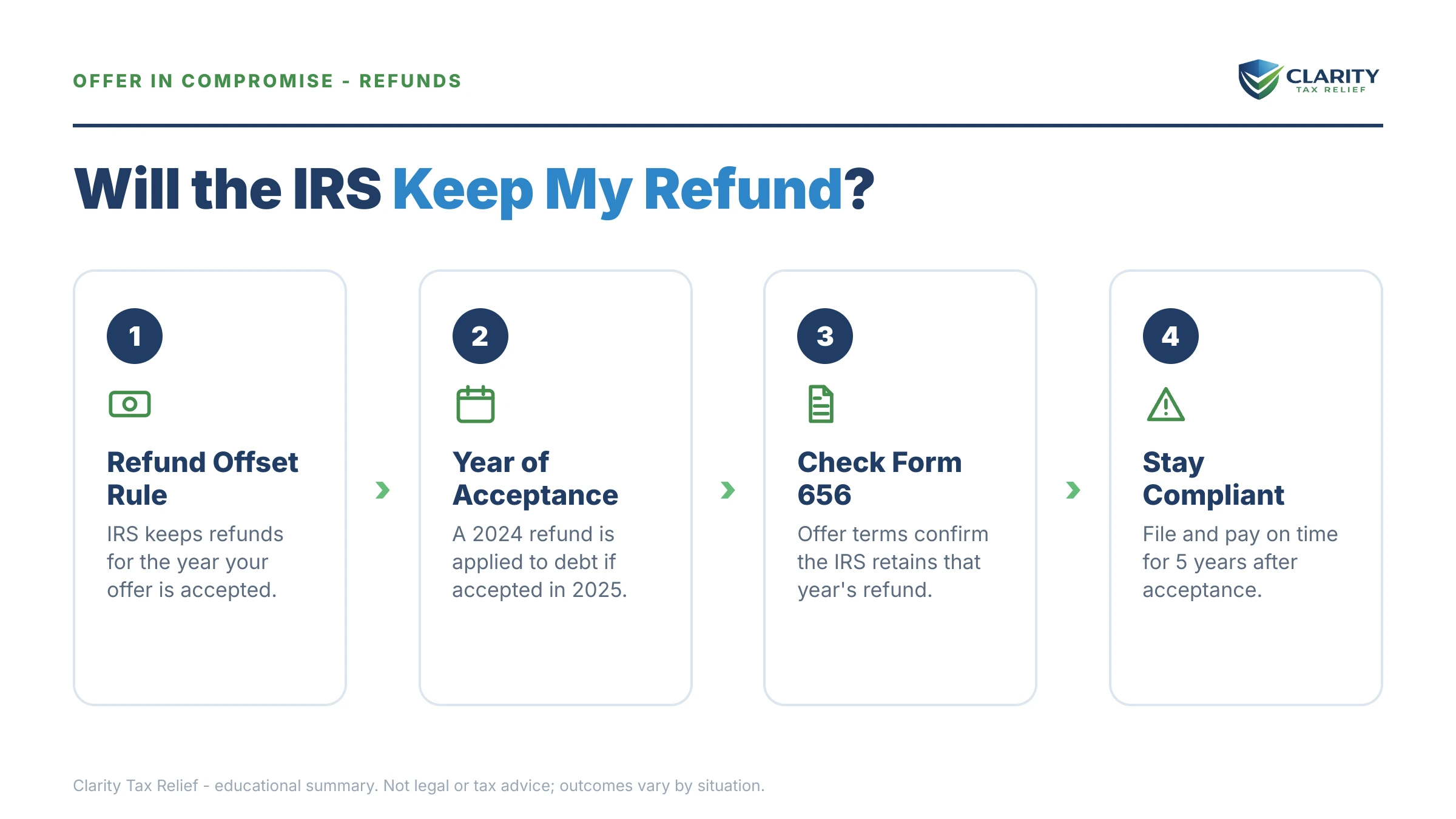

The short answer: no — for offers accepted on or after November 1, 2021, the IRS no longer keeps your tax refund for the calendar year your offer in compromise is accepted. But a refund that comes due while your offer is still pending can be taken and applied to your old debt — and it won't count toward your offer amount.

You fought for months to get an offer through — or it's sitting in the review queue right now — and this filing season your return shows a refund you were planning to put straight back into the business. Whether that money ever reaches your account comes down to one date: the day the IRS signs your acceptance letter. Here's the good news up front: the rule changed in your favor a few years ago, and most people asking this question keep more than they expect.

The one distinction that decides everything is pending versus accepted. The stage-by-stage table below maps exactly when a refund is at risk, when it's safely yours, and the one five-year trap that can undo the whole settlement.

⏱ The clock that matters: there's no 30-day deadline on this question — the dividing line is your offer's acceptance date. Refunds the IRS receives while your offer is pending can be applied to the old debt. Refunds for the calendar year of acceptance and every year after are yours — as long as you stay fully compliant for five years.

Will the IRS keep my refund after an offer in compromise? What changed in November 2021

For offers accepted on or after November 1, 2021, the IRS no longer keeps the refund for the calendar year in which the offer is accepted. That single policy change is why so much advice on this question is out of date.

Under the old rule, the fine print of Form 656 — the offer contract itself — let the IRS "recoup" your refund for the year your offer was accepted, on top of the offer amount you paid. Get accepted in 2020, file your 2020 return the following spring, watch the refund vanish. It surprised thousands of taxpayers every year, because nobody reads Section 7 of a settlement contract twice.

The IRS dropped that recoupment term for all offers accepted on or after November 1, 2021. In 2026, every newly accepted offer works the same way: the acceptance-year refund is yours, and so is every refund after it — subject to the compliance rules covered below. (If you're still deciding whether an offer fits your situation at all, the mechanics, eligibility math, and costs live in our guide to how an offer in compromise works.)

What did not change: the IRS's treatment of refunds while your offer is still under review. That's where most of the money is actually lost.

Will the IRS take my refund while my offer in compromise is pending?

Yes — while your offer in compromise is pending, the IRS can take any tax refund you're owed and apply it to the original debt. On your account transcript, the pending offer shows as code 480, and a refund pulled into the old balance posts as code 826.

The part that stings: that offset does not count toward your offer amount. If you offered $11,000 and the IRS absorbs a $6,200 refund during review, you still owe the full $11,000 if the offer is accepted. The refund just shrank a balance you were about to settle anyway.

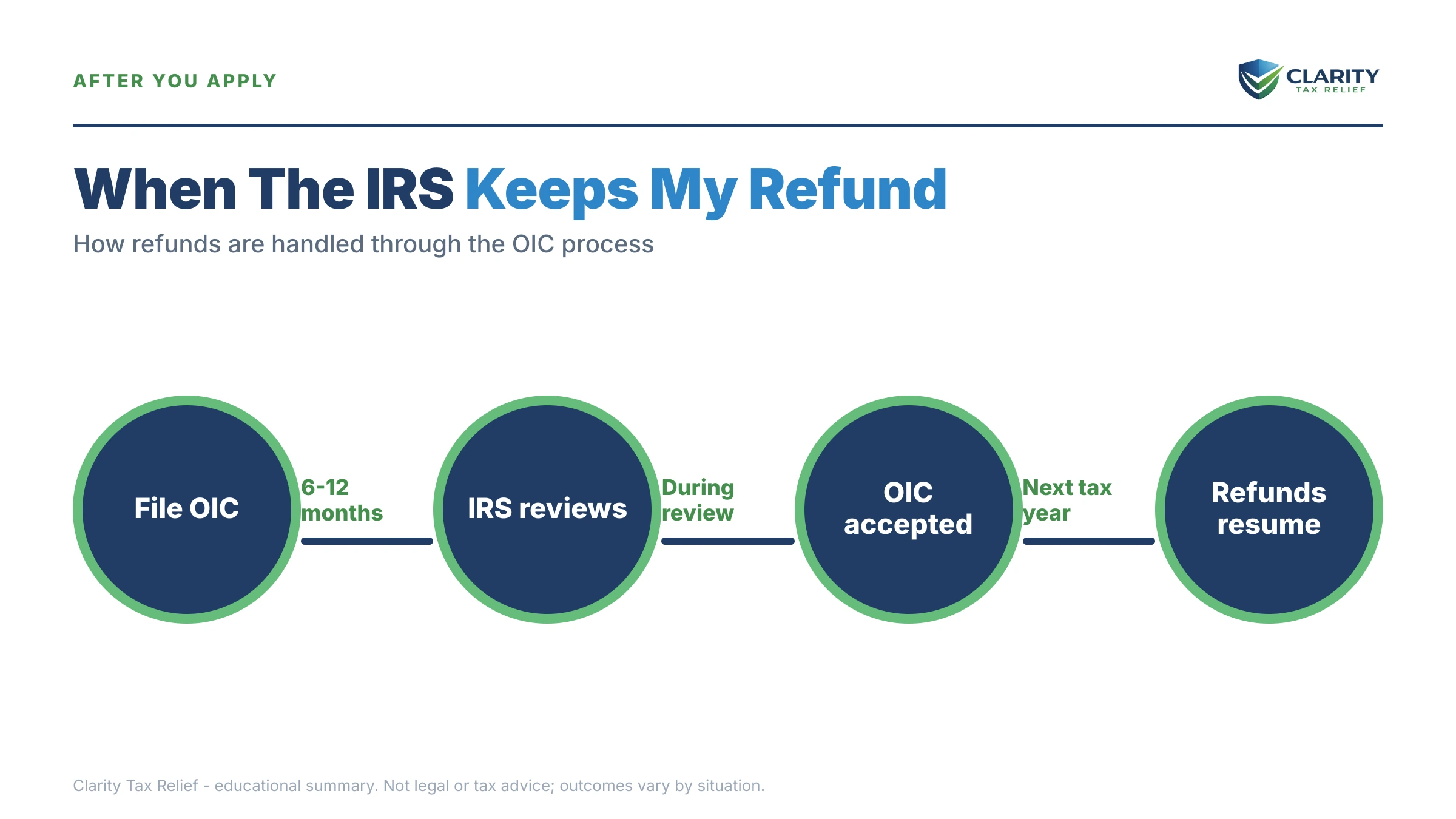

And "pending" is not a short window. Offer review routinely runs the better part of a year — sometimes longer with 2026 staffing levels — which means most people file at least one tax return while their offer is under consideration. (See how long an offer in compromise takes for the full timeline.) One useful backstop: if the IRS doesn't decide within two years, the offer is deemed accepted by law.

There is one narrow exception during the pending period: if losing the refund would cause immediate economic hardship — eviction, utility shutoff, an unpayable medical bill — you may qualify for an offset bypass refund for hardship, requested through the Taxpayer Advocate Service (typically on Form 911) before the refund is applied.

What happens to your refund at each stage of an offer in compromise

Refund treatment flips three times over the life of an offer — before submission, during review, and after acceptance. This is the whole answer in one table:

| Stage | What happens to a refund | Counts toward your offer? |

|---|---|---|

| Before you submit the offer | Automatically offset against your back taxes, like any refund while you owe — see will my refund be taken for back taxes | No — it only reduces the balance |

| While the offer is pending (code 480) | Can be taken and applied to the original debt; a hardship offset bypass refund is the only exception | No — your offer amount is unchanged |

| Calendar year of acceptance | Yours to keep (offers accepted on or after Nov 1, 2021) | N/A — you keep it |

| Years 1–5 after acceptance | Yours — but a refund can still be offset against any new balance you rack up | N/A — you keep it |

| After the five-year compliance period | Normal taxpayer again; refunds are only at risk for new debts | N/A |

Two edge cases worth flagging. First, a joint return filed during a pending offer puts the whole joint refund at risk even if only one spouse owes — the non-liable spouse can recover their share with injured spouse Form 8379. Second, refunds offset during a pending offer aren't wasted if the offer is rejected: the balance you renegotiate from is that much smaller.

A worked example: a $6,200 refund and a pending offer

Say you run an HVAC company with three employees, and two rough years left you owing $52,000 on your personal 1040s. In March 2026 you submit a lump-sum offer of $11,000 — the number your asset equity and future income support. With the paperwork goes the $205 application fee plus a 20% down payment of $2,200, leaving $8,800 payable shortly after acceptance. (If your AGI is at or below 250% of the federal poverty level, low-income certification waives the fee, the down payment, and payments during review.)

In April, while the offer sits in review, you file your 2025 return. Your quarterly estimates overshot by $1,550 per quarter, so the return shows a $6,200 refund. The IRS applies it to the $52,000 debt — code 826 on your transcript. Your offer amount? Still $11,000.

Total cash out if accepted: $11,000 offer + $6,200 absorbed refund + $205 fee = $17,405 — when accurate quarterlies would have kept the settlement at $11,205 and left $6,200 of working capital in the business.

Now run the calendar the other way. The offer is accepted in October 2026, and your 2026 return — filed in February 2027 — shows another $6,200 refund. That one lands in your bank account, because it belongs to the calendar year of acceptance. Same dollar amount, opposite outcome, decided entirely by which side of the acceptance date the refund fell on.

One more note on the $11,000 itself: the IRS accepts an offer only when it meets or beats your Reasonable Collection Potential — the equity in what you own plus a multiple of your monthly disposable income. You can estimate your own offer with our Offer in Compromise Calculator. And keep expectations honest: the IRS accepted roughly 1 in 5 offers in FY2024, so the math has to genuinely work.

State refunds and business debts: two rules people miss

An IRS offer in compromise settles federal debt only — it does nothing for state balances, and states don't honor the IRS's refund rules. While your federal offer is pending, the IRS can even grab your state refund for the federal debt through the State Income Tax Levy Program. And if you owe your state separately, its refund intercepts continue until you resolve that balance under the state's own program — California's runs through the FTB offer in compromise, with different forms, different math, and a 20-year collection statute behind it.

If your debt includes payroll tax, the stakes rise. Offers on trust-fund liabilities are rare and strictly scrutinized — the rules are covered in business offer in compromise payroll — and once an offer of any kind is accepted, an employer's compliance picture includes timely federal tax deposits and 941 filings, not just the April 1040. Overpayments sitting on a business tax account get applied to outstanding business balances the same way personal refunds do.

What happens if you slip during the five-year compliance period

One missed return or unpaid new balance during the five years after acceptance can default your offer and bring the entire original debt back. This is the real "will they take my refund" risk after acceptance — not the refund itself, but the compliance terms attached to it. Here's the sequence when something slips:

- A trigger posts — an unfiled return, an unpaid new balance, or a missed payment on a periodic-payment offer.

- The IRS sends a default warning letter — typically a short window to cure by filing, paying, or catching up. This letter is your last cheap exit.

- The offer defaults — the settlement contract is void.

- The original debt is reinstated — the full pre-offer balance, minus your offer payments and any refund offsets, plus penalties and interest that kept accruing on paper.

- Collection restarts — bills, intent-to-levy notices, then lien and levy authority. And because the 10-year collection statute was paused while your offer was pending, the IRS has more time on the clock than if you'd never applied.

In our HVAC example, defaulting in year two would revive roughly $52,000 minus the $11,000 paid and the $6,200 offset — call it $34,800 plus accumulated additions — in exchange for one missed filing deadline. The compliance terms in plain English:

| Requirement | What breaks it | What happens |

|---|---|---|

| File every required return on time | A late or unfiled 1040 or business return in any of the five years | Warning letter, then default and full reinstatement of the original debt |

| Pay every new balance in full | An April balance due or unpaid quarterly estimates | Same — new unpaid tax is the most common reason accepted offers default |

| Stay current on payroll obligations (if you have employees) | Missed federal tax deposits or late 941 filings | Compliance failure that puts the offer at default risk |

| Finish paying the offer itself | A missed installment on a periodic-payment offer | Warning, then default if not cured |

Offer pending — or accepted — and a refund on the line?

Whether the IRS just absorbed a refund during your pending offer or you're protecting an accepted one through the five-year compliance period, an experienced tax professional can review your transcript and map the timing free — before this filing season locks in the outcome.

Your options if the IRS took a refund you were counting on

Which fix applies depends on when the refund was taken and why — and every option below is free to pursue. The one that's genuinely time-sensitive is the hardship bypass: it only works before the refund posts to your old balance.

| Option | When it applies | Cost & timing |

|---|---|---|

| Offset bypass refund (OBR) | Pending offer plus documented immediate hardship — eviction, shutoff, medical bill | Free; request through the Taxpayer Advocate Service (Form 911) before the refund is applied |

| Dispute a wrongful offset | The IRS took a refund for the acceptance year or later by mistake | Free; call with your acceptance letter in hand — corrections typically take weeks to months |

| Injured spouse allocation (Form 8379) | A joint refund was taken during a pending offer when only one spouse owes | Free to file; processing typically runs a few months |

| Adjust withholding or estimates | Offer still pending — stop building refunds the IRS will absorb | Free; takes effect with your next paycheck or quarterly payment |

| Appeal a rejected offer (Form 13711) | The offer was rejected after your refund was already applied | Free; must be filed within 30 days of the rejection letter — the offset stays as a payment on the smaller balance |

If the offer route ultimately isn't the right fit, refund treatment differs across the alternatives too: on an installment agreement, the IRS keeps offsetting refunds until the balance is paid, and in Currently Not Collectible status refunds are offset even while collection is paused. That trade-off is part of the payment plan vs. offer in compromise decision — an accepted offer is the only resolution that eventually gives you your refunds back.

How to protect your refund during and after an OIC, step by step

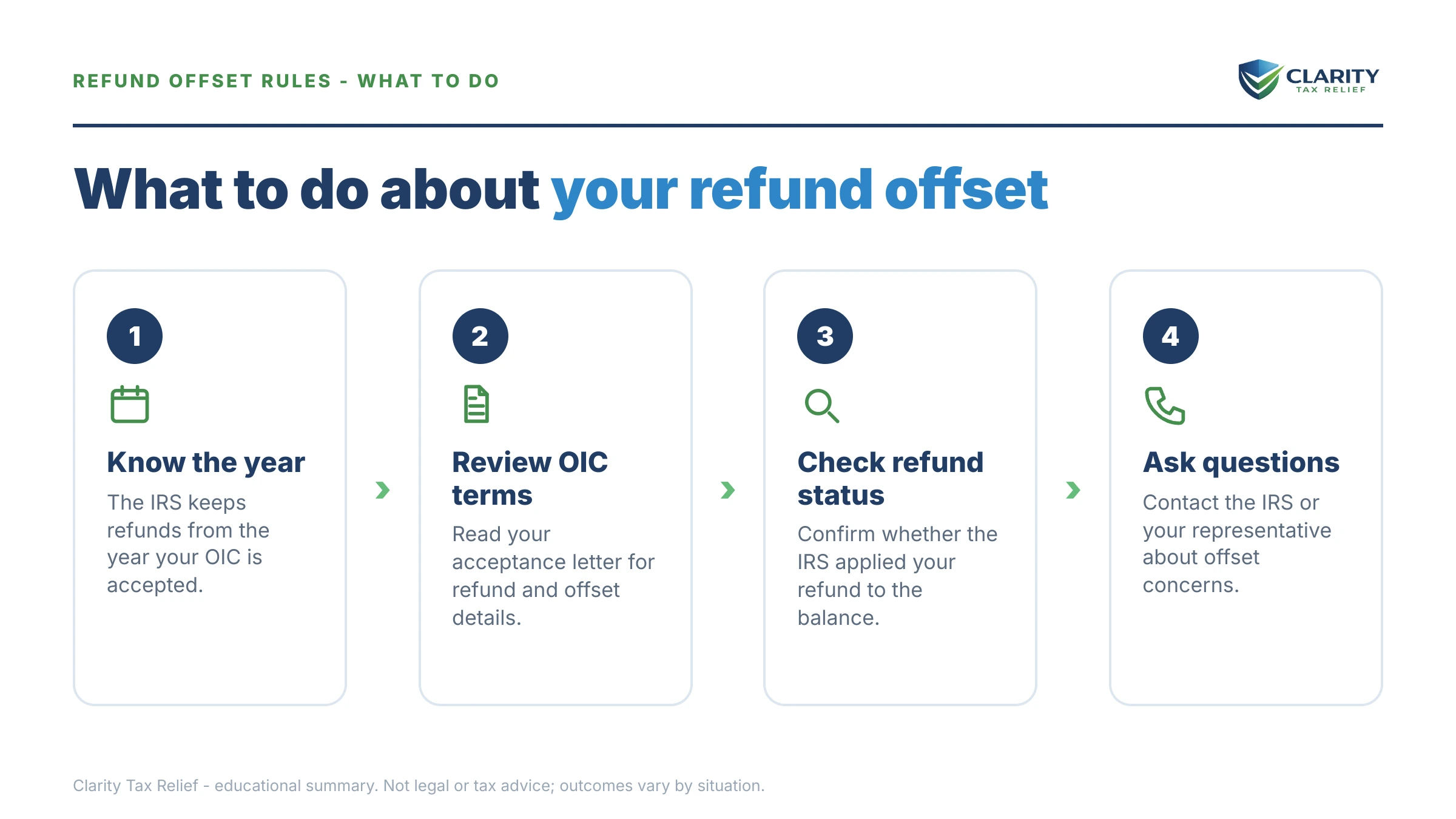

- Pin down your dates — Find your acceptance date on your offer acceptance letter, or pull your account transcript — code 480 means your offer is still pending, which is when refunds are at risk.

- Stop building a refund — Adjust your withholding or quarterly estimates to break even; a refund created while your offer is pending will likely be applied to the old debt without counting toward your offer.

- File every return on time for five years — Calendar every filing deadline, including extensions and business returns — one unfiled return during the compliance period can default your accepted offer.

- Pay every new tax in full — Cover quarterly estimates, payroll deposits, and any April balance as they come due — a new unpaid balance is the most common way accepted offers default.

- Act fast if a refund is taken — Call the IRS with your acceptance letter if a post-acceptance refund is offset by mistake, or request an offset bypass refund through the Taxpayer Advocate before a pending-offer offset posts if it would cause hardship.

When you can handle this yourself — and when help changes the outcome

Most refund questions around an accepted offer are genuinely DIY. If your offer was accepted after November 1, 2021, your returns are filed, and you owe nothing new, no action is required — your refunds are simply yours. If a post-acceptance refund gets offset by mistake, a phone call with your acceptance letter and a copy of your transcript usually resolves it without professional help. Adjusting withholding or quarterlies to break even is a ten-minute fix you can do today.

Experienced help earns its cost in a narrower set of situations: a pending offer with a hardship offset-bypass request, where a missed timing window forfeits the refund permanently; a default warning letter during the five-year period, where the cure has to be exactly right the first time; business or payroll debt in the mix, where compliance spans deposits and 941s and a slip revives personal exposure; or a rejected offer where the taken refund, the appeal deadline, and a possible second offer all need sequencing. In those cases, the order of moves changes the dollars — see the IRS's official Offer in Compromise page for the program terms, and the Taxpayer Advocate Service for the hardship route.

If your offer is pending and a refund is riding on this filing season, get a free review of your OIC and transcript — or call (888) 825-7779 — before you file, while the timing can still be managed.

Terms on your offer paperwork, decoded

- Offset — the IRS taking a refund you're owed and applying it to a tax debt instead of paying it to you.

- Recoupment — the old (pre–November 2021) offer term that let the IRS keep your acceptance-year refund on top of your offer amount; it no longer applies to new offers.

- Pending offer (code 480) — the review window between submitting Form 656 and the IRS's decision, when refunds can still be applied to the old debt.

- Code 826 — the transcript entry showing a refund was moved from one tax year and applied to a balance on another.

- Five-year compliance period — the term in every accepted offer requiring you to file and pay on time for five years, or the settlement defaults.

- Default — the offer contract being voided, which reinstates the full original debt minus what you've paid.

- Offset bypass refund (OBR) — a hardship-only release of a refund that would otherwise be offset, requested through the Taxpayer Advocate before the offset posts.

Offer in compromise refund questions, answered

Does the IRS keep your refund the year your offer in compromise is accepted?

Not anymore. For offers accepted on or after November 1, 2021, the IRS ended its old practice of keeping the refund for the calendar year of acceptance — that refund, and every one after it, is yours. The exception is new debt: if you owe a fresh balance for a later year, a refund can be offset against that new liability, and the unpaid new balance itself can default your offer.

Will the IRS take my refund while my offer in compromise is pending?

Yes, usually. Any refund that comes due while your offer sits in review can be taken and applied to the original tax debt, and review commonly takes many months. That money does not count toward your offer amount — it simply shrinks the old balance. The narrow exception is an offset bypass refund, available only for documented financial hardship and only if you request it before the refund is applied.

Does a refund the IRS keeps count toward my offer amount?

No. A refund offset during a pending offer reduces the underlying liability, but your offer amount stays exactly what you proposed on Form 656. So if you offered $11,000 and the IRS absorbs a $6,200 refund during review, you still owe the full $11,000 offer. The only silver lining: if the offer is later rejected, the balance you go back to negotiating on is $6,200 smaller.

What happens to the refund the IRS took if my offer is rejected?

It stays applied to your tax debt — the IRS does not return it, because you legally owed that balance all along. The offset simply becomes a payment on the liability. If you disagree with the rejection itself, you have 30 days from the date of the rejection letter to appeal on Form 13711, and the reduced balance carries into the appeal or into any second offer you file.

Can I get my refund during a pending offer if I'm in financial hardship?

Possibly, through an offset bypass refund (OBR). You must show immediate economic hardship — a pending eviction, utility shutoff, or unpayable medical bill — and request it through the Taxpayer Advocate Service, typically on Form 911, before the refund is applied to your debt. Timing is everything: once the offset posts to your account, an OBR is generally no longer available for that refund.

What happens if I don't file a return during the five-year compliance period?

Your accepted offer is at risk of default. The IRS typically sends a warning letter first and gives you a short window to file and cure the problem. If you don't, the offer defaults, the entire original debt — minus your offer payments and any offsets — is reinstated with penalties and interest, and collection starts again. One late return can undo a settlement that took a year to win, so calendar every deadline for the full five years.

Will the IRS or my state take my state refund after an offer in compromise?

While your federal offer is pending, the IRS can still take your state refund for the federal debt through the State Income Tax Levy Program. After acceptance, the settled federal debt no longer supports that levy. But an IRS offer does nothing for state back taxes — states run entirely separate programs with their own rules, so a state agency like California's FTB can keep intercepting state refunds until you resolve the state balance directly.

Should I change my withholding while my offer in compromise is pending?

Yes — aim to break even. Any refund you build up during review is likely to be absorbed by the old debt without counting toward your offer, so over-withholding is essentially a donation to a balance you're trying to settle. Just don't swing too far the other way: an underpayment creates a new balance due, and new unpaid tax can sink a pending offer or default an accepted one.

Can the IRS take my spouse's share of our refund for my offer in compromise?

If you file a joint return while your offer is pending, the entire joint refund can be offset for the debt even when only one spouse owes it. The non-liable spouse can file Form 8379, the injured spouse allocation, to recover their share of the refund; processing typically takes a few months. After acceptance, refunds for the acceptance year and later are not taken for the settled debt.

Your next 24 hours

- Find your acceptance date. Pull your offer acceptance letter — or your account transcript — and confirm whether your offer is accepted or still showing code 480 (pending). That one fact decides whether your next refund is safe.

- Gather three things: your Form 656 packet, your most recent tax return (or the one you're about to file), and this year's withholding or quarterly-estimate figures.

- Get the timing reviewed free. Refunds absorbed during a pending offer don't come back, and compliance slips quietly compound — an experienced tax professional can map your filing timing in one call. Start at the 2-minute form or dial (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.