Refund Offsets & Hardship Relief

Offset Bypass Refund for Hardship: How to Keep Your Refund From the IRS Offset (2026)

The short answer: an offset bypass refund (OBR) lets the IRS release some or all of a tax refund that would otherwise be applied to your federal tax debt, when the offset would cause economic hardship. There is no form — you must request it by phone or through the Taxpayer Advocate Service before your refund posts.

You owe the IRS back taxes, you finally have a refund coming, and you already know what happens next: the IRS keeps it — while the rent notice on your counter says you have days, not months. An offset bypass refund hardship request is the one narrow exception built into the system, and almost nobody at the IRS will volunteer that it exists.

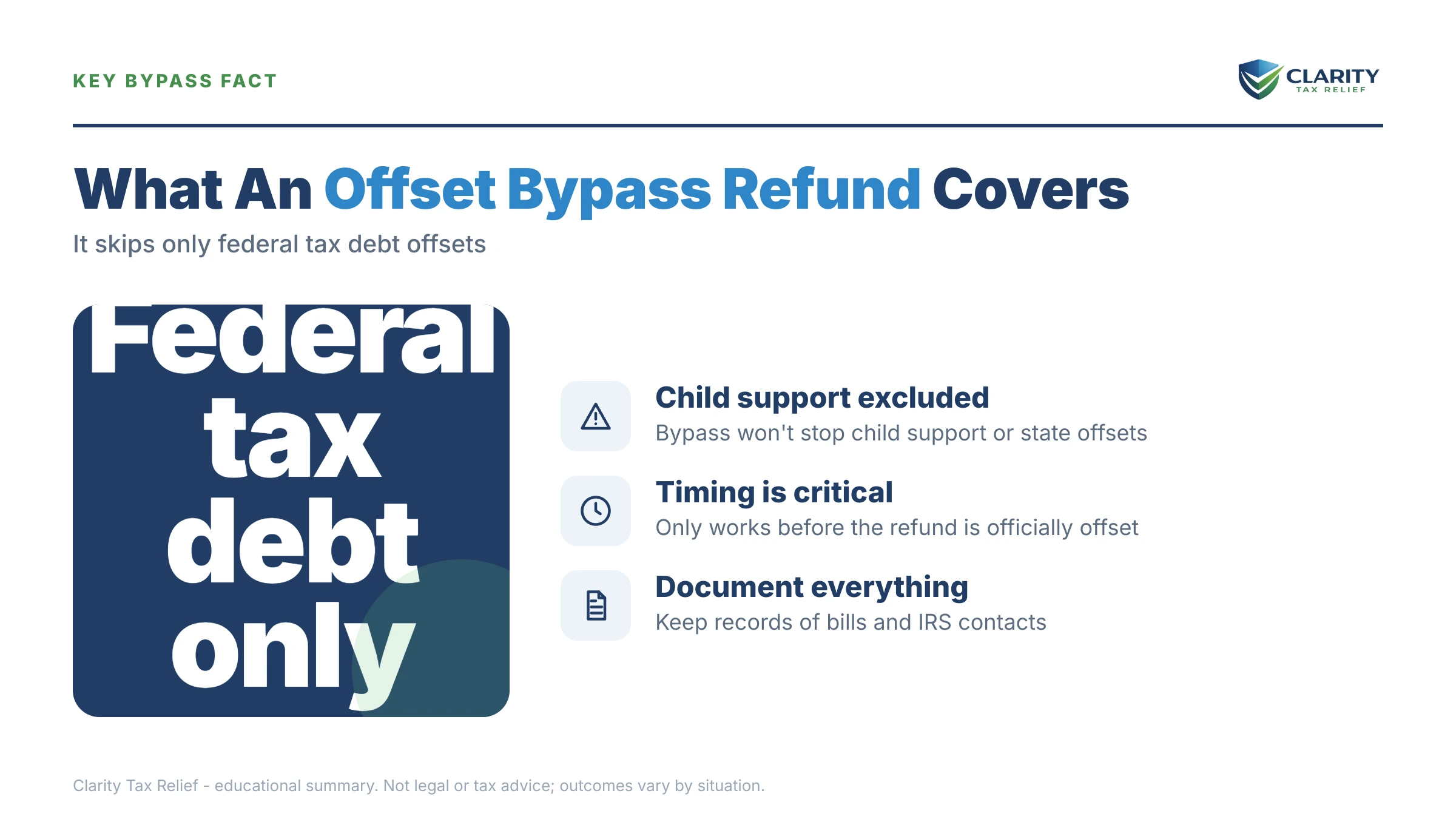

Three facts define this remedy. It has no form. It only works against your own federal tax debt — never child support or student loans. And it dies the moment your refund posts, which makes it one of the most time-sensitive requests in all of tax resolution. The image below shows what an offset actually looks like on an IRS account, so you can tell at a glance whether your window is still open.

⏱ Your real deadline: the moment your refund is applied to your balance. Most e-filed refunds process in about 21 days, and the offset happens inside that same window with no advance warning. If you're going to request an OBR, the safest time is before you file — or the same week you do.

Why the IRS is about to take your refund

Your federal refund is applied to your back taxes automatically under IRC §6402(a) — the IRS does not have to warn you before it happens. If your account shows any assessed federal tax balance, the computer intercepts the overpayment during processing and applies it to the oldest year first.

This internal IRS offset is different from the Treasury Offset Program, which takes refunds for child support, defaulted student loans and other non-tax debts. That distinction is the whole ballgame: §6402(a) offsets are discretionary — the statute says the IRS "may" apply your refund — and that discretion is exactly what an OBR asks the IRS to exercise in your favor. TOP offsets under §6402(c)–(f) are mandatory, and no one at the IRS has authority to bypass them.

The hardship standard the IRS applies mirrors the economic-hardship test used for releasing a levy that causes hardship: the offset must leave you unable to pay a basic, necessary living expense. A pending eviction qualifies. Wanting your refund for ordinary bills does not.

What happens if you do nothing

If you do nothing, the IRS applies your entire refund to your oldest balance and tells you about it only after the money is gone. There is no pre-offset notice for a federal tax offset, so the sequence runs silently:

- You file your return showing an overpayment. The IRS processes it normally — "Where's My Refund" may even show progress.

- The offset posts internally. Transcript code 826 appears on your account, meaning the overpayment moved to another tax year. (An offset to a non-tax debt posts as code 898 instead — a signal an OBR was never possible.)

- A CP49 notice arrives by mail confirming the refund was applied to back taxes. By the time you're reading it, the OBR window has closed — see our CP49 refund applied guide for what that notice means.

- The hardship goes unfunded. The eviction, shutoff, or medical bill you needed the refund for is still due, and the applied refund can't be clawed back except in rare IRS-error cases.

- It repeats every filing season until the underlying balance is resolved — offset is annual and automatic, even for accounts in hardship status.

One 2026 wrinkle makes timing harder, not easier: the IRS workforce shrank roughly 27% in 2025, so reaching a human to process an OBR takes longer — while the automated offset itself runs at full speed. The machine that takes your refund never got slower. The path that saves it did.

Refund about to be offset — and you need that money to keep the lights on?

An offset bypass refund only works before your refund posts, and most e-filed refunds move in about 21 days. Get your situation reviewed free today so the request lands while the window is still open — call (888) 825-7779 or use the 2-minute form.

Your options when a refund offset would cause hardship

An offset bypass refund is the only remedy that releases refund money the IRS would otherwise keep for your own tax debt — but it is not the right tool for every offset. Which remedy applies depends entirely on whose debt is taking the refund and what kind of debt it is:

| Your situation | The right remedy | Key eligibility rule |

|---|---|---|

| Refund going to your own federal tax debt, and you face an immediate hardship | Offset bypass refund (OBR) | No form; request by phone or via TAS before the refund posts; release capped at the documented hardship amount |

| Joint refund taken for your spouse's separate debt | Injured spouse — Form 8379 | You must have your own income, withholding, or credits on the joint return; recovers only your share |

| Refund taken for child support, student loans, or state debt | Dispute with the agency that certified the debt | OBR cannot bypass Treasury Offset Program debts — the IRS has no discretion over them |

| Ongoing inability to pay basic living expenses, beyond this one refund | Currently Not Collectible status | Financial-statement test on Form 433-F; note that offsets continue even in CNC |

| IRS levy (wages or bank account) causing hardship — not a refund offset | §6343 hardship levy release | Applies to active levies only; a refund offset is not a levy and follows the OBR path instead |

If your deeper problem is that you can't pay the IRS at all — not just this one offset — the durable fix runs through hardship status. Our guide on how to qualify for CNC covers the full 433-F financial test, and the IRS hardship program overview explains honestly what that status does and doesn't protect. The one-sentence version for this page: CNC stops levies, but it does not stop refund offsets — which is why the OBR exists as a separate remedy.

Cost and speed differ sharply across these paths, and speed is usually what decides it:

| Option | Cost | Typical timeline |

|---|---|---|

| Offset bypass refund | Free | Must be requested and worked before the refund posts — days, not months; the released portion is then paid to you |

| Injured spouse (Form 8379) | Free | Roughly 2–3 months of IRS processing; can be filed with the return or after the offset |

| TAS case (Form 911) | Free | Varies; hardship cases are prioritized, and TAS can move an OBR faster than the general IRS line in 2026 |

| Currently Not Collectible | Free (financial disclosure required) | Weeks to set up; protects wages and bank accounts going forward but never the refund |

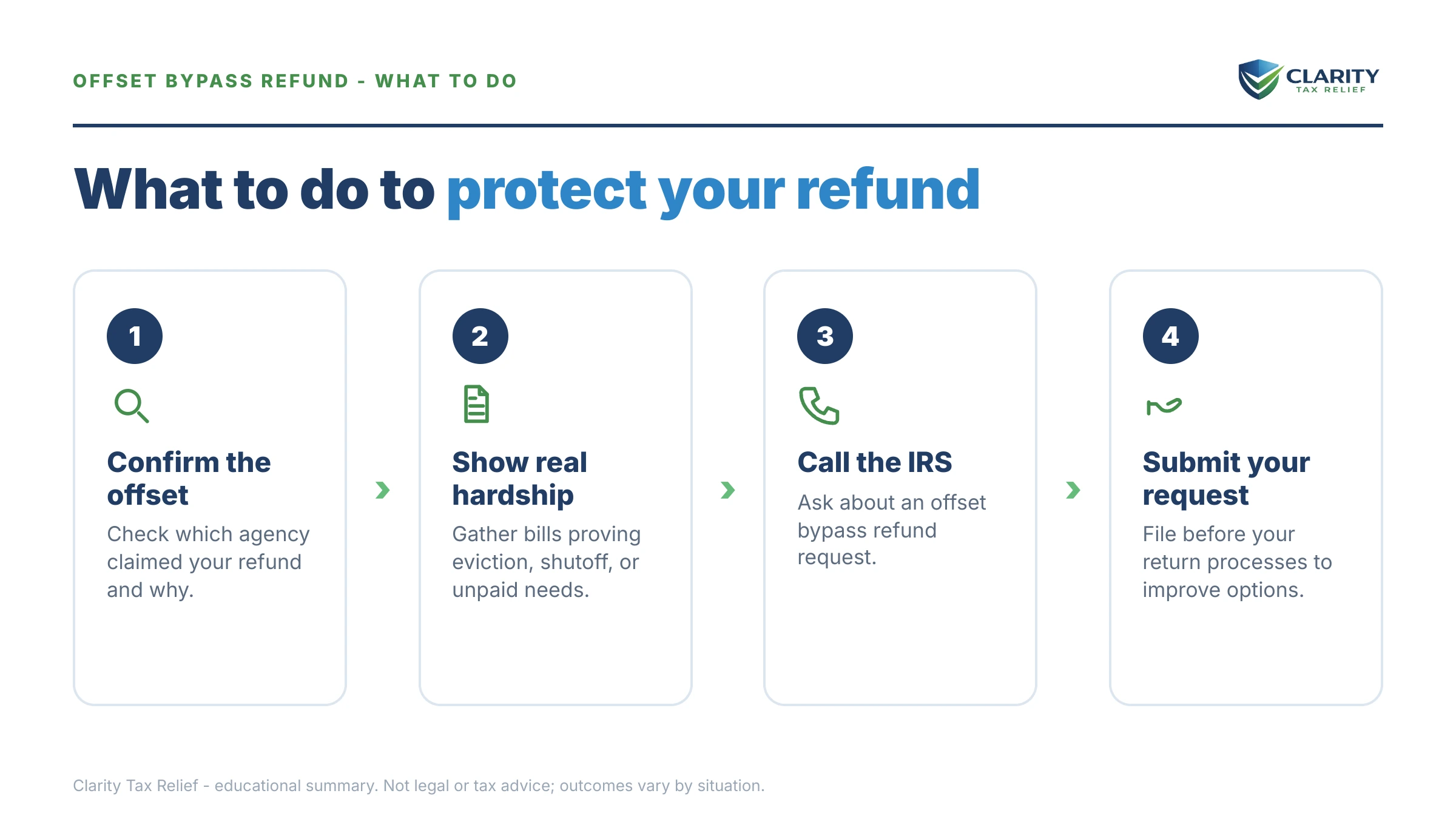

How to request an offset bypass refund for hardship, step by step

There is no IRS form for an offset bypass refund — the request is made by phone or through the Taxpayer Advocate Service, and it must land before your refund posts. Here is the sequence that works:

- Confirm what kind of debt is set to take your refund. Call the Treasury Offset Program hotline at 800-304-3107 and check your IRS account transcript. An OBR only works if the offset is for your own federal tax debt — child support, student loans, and state debts follow a different path.

- Gather proof of the hardship with exact dollar amounts. An eviction or foreclosure notice, utility disconnection notice, or medical bill — plus the precise amount you need and its due date. The IRS releases only what the paperwork supports.

- Request the OBR before your refund posts — ideally when you file. Call the IRS at 800-829-1040, say you are requesting an offset bypass refund for economic hardship, and be ready to fax or upload your documentation the same day.

- Open a Taxpayer Advocate Service case if you can't get through. File Form 911 or call TAS directly. Advocates handle OBR requests routinely and can push a manual refund through before the offset applies — often the faster route in 2026.

- Follow up until the release is confirmed. Ask for the approved amount and how the released portion will be paid, and watch your transcript so the request doesn't die in processing while the refund clock runs.

- Deal with the underlying balance so next year's refund survives. Set up an installment agreement, request CNC status, or explore settlement — offsets repeat every year until the debt itself is resolved.

The TAS route deserves emphasis this year. With IRS phone service degraded, many successful OBRs run through an advocate rather than the main line — our Form 911 walkthrough shows exactly how to open the case and what to put in the hardship description. Two practical notes: the IRS will expect your required returns to be filed before it exercises discretion in your favor, and a denied OBR carries no formal appeal rights — which is one more reason to get the documentation right the first time.

What hardship proof the IRS actually accepts

The OBR release is capped at the documented hardship amount, so your evidence sets your ceiling. Vague statements about being broke get nothing released; a dated notice with a dollar figure on it gets that dollar figure considered:

| Hardship type | Documentation to gather | What it establishes |

|---|---|---|

| Eviction or foreclosure | Landlord's pay-or-quit notice, foreclosure letter, past-due amount and deadline | The exact dollar amount needed to keep your housing, and by when |

| Utility shutoff | Disconnection notice with account number, balance, and cutoff date | An essential service ends on a specific date without a specific payment |

| Medical necessity | Bills, prescription costs, or a provider letter tying treatment to payment | Care you or a dependent will lose access to without the funds |

| Vehicle needed for work | Repair estimate plus proof the vehicle produces your income (common for 1099 drivers and contractors) | The offset would cut off your ability to earn at all |

A worked example: $76,400 owed, a $4,900 refund, and a pay-or-quit notice

Say you're a 1099 contractor who owes the IRS $76,400 across three years of unpaid self-employment tax. This year you finally overpaid — your fourth-quarter estimated payment plus a refundable credit produced a $4,900 overpayment on your return. Then your landlord posted a pay-or-quit notice: $2,300 past due, ten days to cure.

Without an OBR, the math is brutal and automatic: the full $4,900 offsets, your balance drops from $76,400 to $71,500, and you're facing eviction with nothing in hand. The IRS considers the offset a payment; the eviction isn't its problem.

With a timely OBR request backed by the pay-or-quit notice, the math changes: the IRS can release up to $2,300 — the documented hardship amount — as an actual refund to you. The remaining $2,600 still offsets, so the balance falls from $76,400 to $73,800. You don't keep the whole refund; you keep the roof.

Two side notes for this contractor. First, at $76,400 the debt sits above the $66,000 passport-certification threshold for 2026, so this account has bigger exposure than a lost refund. Second, hardship status is genuinely available to the self-employed, but the financial test works differently when your income is business income — our guide to currently not collectible self employed walks through that math.

When you can handle this yourself — and when help changes the outcome

You can request an offset bypass refund yourself — the IRS requires no representative, and the request costs nothing. If your situation is a single tax year owed, a clean filing record, one clear hardship document, and time before you file, a patient morning on the phone (or a Form 911 to TAS) is a reasonable DIY plan.

Experienced help earns its keep when the clock or the file is against you: the return is already filed and the refund could post any day; you have unfiled years the IRS will raise before exercising discretion; the hardship spans several categories and needs to be packaged to support a larger release; or the real problem is the $76,400 behind the offset — where sequencing an OBR now with an installment agreement, CNC request, or settlement analysis afterward determines what the next several years cost. In those cases an experienced tax professional isn't filing a form for you; they're making sure a one-shot, no-appeal request lands right the first time.

Terms in the offset process, decoded

- Offset: the IRS or Treasury applying your refund to a debt during processing — administrative, automatic, and not a levy.

- Offset bypass refund (OBR): the IRS's discretionary release of the hardship portion of a refund that would otherwise offset to your federal tax debt.

- IRC §6402(a): the statute saying the IRS may apply overpayments to your tax debts — the word "may" is where OBR discretion lives.

- Treasury Offset Program (TOP): the separate, mandatory system that takes refunds for child support, student loans, and state debts; no bypass exists for it.

- Code 826 / Code 898: transcript codes showing your refund moved to another tax year (826) or to a non-tax agency debt (898).

- Economic hardship: the inability to pay basic, necessary living expenses — the same standard used for hardship levy releases.

Offset bypass refund questions, answered

Is there an IRS form for an offset bypass refund?

No. Unlike almost every other IRS remedy, there is no form for an OBR. You request one by calling the IRS at 800-829-1040 or by opening a case with the Taxpayer Advocate Service using Form 911. Because the OBR is discretionary and handled manually, a specific, documented hardship amount matters more than anything a form could capture.

Can an offset bypass refund stop a child support or student loan offset?

No. An OBR only bypasses offsets against your own federal tax debt under IRC §6402(a). Offsets for child support, federal student loans, state income tax, and unemployment overpayments run through the Treasury Offset Program and are mandatory — the IRS has no discretion to release them. Your dispute goes to the agency that certified the debt, not the IRS.

When do I have to request an offset bypass refund?

Before your refund is applied to your tax debt — as a practical matter, when you file or within days afterward. Most e-filed refunds process in about 21 days, and once transcript code 826 posts, the money has been applied and an OBR is generally no longer possible. If you know an offset is coming, start the request before you file.

How much of my refund can an OBR release?

Only the amount of your documented hardship, not your whole refund. If your refund is $4,900 and you need $2,300 to stop an eviction, the IRS releases up to $2,300 and offsets the rest. That is why the exact figures on your eviction notice, shutoff notice, or medical bill matter so much.

Can I get an offset bypass refund if I'm in currently not collectible status?

Yes — and you may need one, because CNC pauses levies and garnishments but does not stop refund offsets. The IRS keeps taking refunds while you're in hardship status. An OBR is the separate, year-by-year remedy for a tax season when the offset itself would leave you unable to cover a basic necessity.

What counts as economic hardship for an OBR?

An immediate inability to pay basic, necessary living expenses — a pending eviction or foreclosure, a utility disconnection, essential medical care, or a car repair you need to keep working. The standard mirrors the economic-hardship test the IRS uses for levy releases. Vague financial stress isn't enough; you need a specific expense, a specific amount, and paper proving both.

What if my refund was already offset — can I get it back?

Generally no. An OBR is a bypass, not a reversal of an offset that already happened; once the overpayment is applied, the IRS treats your debt as paid down. In rare cases the Taxpayer Advocate Service can help if the IRS made an error or ignored a timely request, but the realistic answer is to act before the offset, not after.

Will the IRS take my refund again next year?

Yes, until the balance is resolved. Refund offset is automatic every year you have a federal tax debt, even in CNC status or on many payment plans. Each year's OBR request stands alone, so the durable fix is addressing the underlying balance through an installment agreement, an Offer in Compromise, or hardship status.

Your next 24 hours

- Find out where your refund stands. Call the Treasury offset hotline at 800-304-3107 and pull your IRS account transcript. No code 826 or 898 yet means your OBR window is still open.

- Gather the hardship paper. The eviction, shutoff, or medical notice with its exact dollar amount and due date, plus a copy of this year's return (or the draft, if you haven't filed).

- Get a free case review before the refund posts. Call (888) 825-7779 or use the 2-minute form — an OBR is a one-shot, no-appeal request, and once the offset applies, the money is gone for the year.

For the IRS's own resources: payment options for the underlying balance are at IRS.gov/payments, the Taxpayer Advocate Service is at taxpayeradvocate.irs.gov, and the Treasury Offset Program is run by the Bureau of the Fiscal Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.