Refund Offsets

Treasury Offset Program Tax Refund: Why Yours Was Taken and How to Get It Back (2026)

The short answer: a Treasury Offset Program tax refund offset means the Bureau of the Fiscal Service — not the IRS — intercepted some or all of your federal refund to pay a past-due government debt: child support, a defaulted federal student loan, state income tax, or another agency's debt. Call 800-304-3107 to learn which debt took it.

You tracked "Where's My Refund" until it flipped to approved, mentally spent that deposit on rent and the state balance hanging over you — and then the deposit arrived hundreds or thousands of dollars short, or never arrived at all. A letter from the "Bureau of the Fiscal Service" follows, from an agency you've possibly never heard of.

That letter is the key to getting anything back, because it names the agency that actually has your money. The image below shows exactly what an offset notice looks like and where on it to look for the creditor agency's name and phone number. And here's the good news: an offset is a defined, rule-bound process with specific reversal paths — this guide walks through each one.

⏱ The real clocks: before a debt enters the offset database, the creditor agency must mail a notice of intent to offset — typically at least 60 days before referral — giving you a window to dispute or pay. After an offset, there's no fixed federal deadline to dispute with the agency, but an injured spouse claim on Form 8379 generally must be filed within three years of the return. Meanwhile, the underlying debt keeps growing with the agency's own interest and fees.

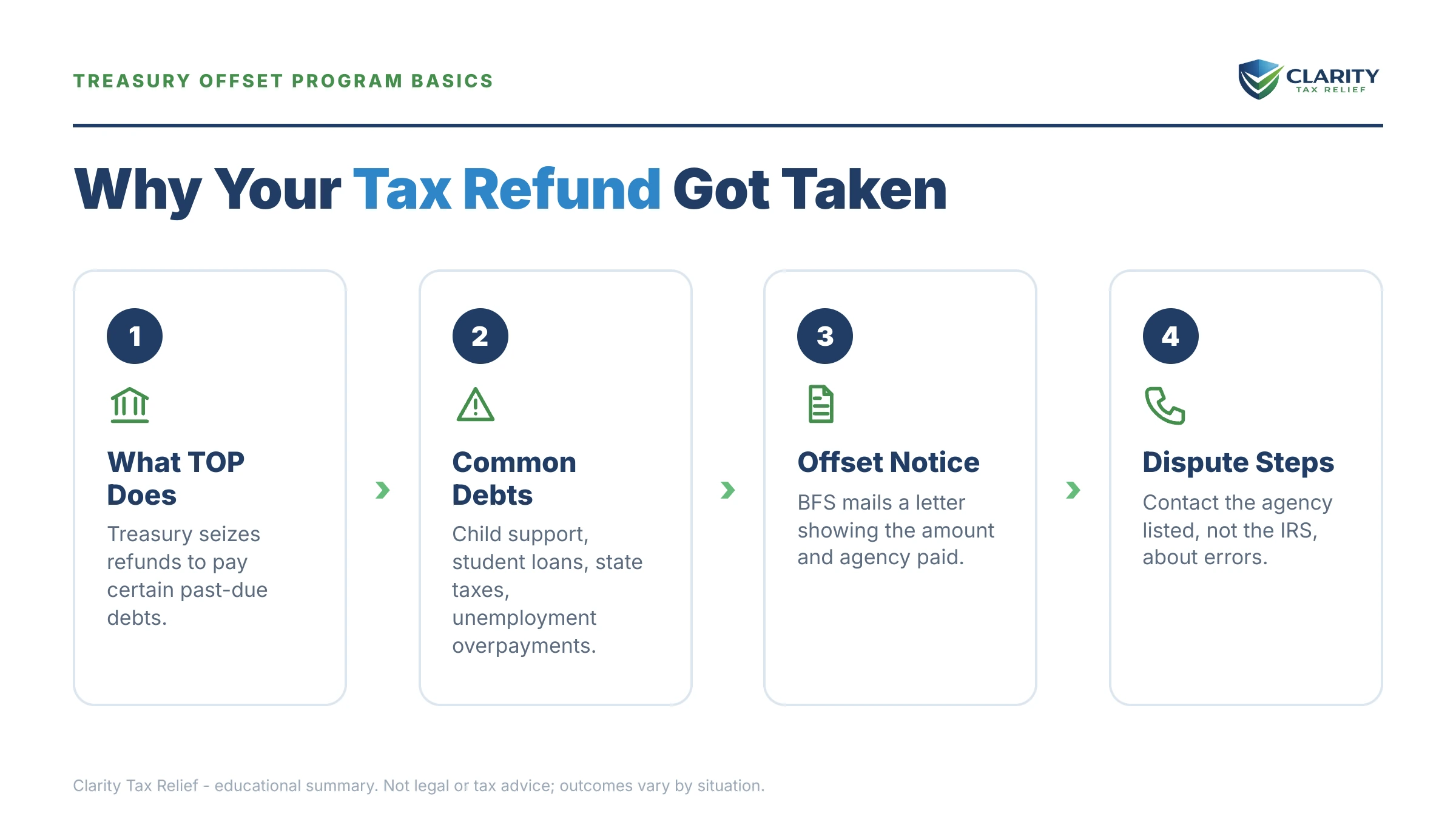

Why the Treasury Offset Program took your tax refund

The Treasury Offset Program (TOP) is a database run by the Bureau of the Fiscal Service that screens every federal tax refund against certified government debts before the money reaches you. If your Social Security number matches a debt in the database, the refund is redirected automatically — no human decides, and no one at the IRS can stop it at that point.

The debts that flow through TOP are, in the order the law pays them:

- Past-due child support, submitted by your state's child support agency.

- Federal agency non-tax debts — most commonly tax refund offsets for defaulted federal student loans, but also VA debts, SBA loans, and federal benefit overpayments.

- State income tax debts, submitted by state revenue departments.

- Unemployment compensation debts owed back to a state.

Notice what's missing: IRS back taxes. The IRS collects its own debts before TOP ever sees your refund — internally, with a CP49 notice and transcript code 826, not through the offset program. If you owe both IRS and TOP debts, the IRS takes its cut first, then whatever remains gets screened against the TOP database. Which agency took your money determines who you dispute with, so sorting this out is step one.

For most people the offset feels sudden because the required warning — the pre-offset notice — went to an old address, sometimes years ago. A defaulted student loan from an apartment you left in 2019 can quietly sit in the database and swallow the refund you filed for in 2026.

How to check for a Treasury Offset Program tax refund hold

You can check the TOP database for free, before or after filing, by calling 800-304-3107. The automated system reads back any debt certified against your Social Security number, the agency that submitted it, and that agency's contact number. Our guide to the treasury offset hotline number covers exactly what to have ready and what each response means.

Two other places tell the story:

- Your IRS account transcript. Code 846 (refund issued) shows the full refund the IRS approved; code 898 posting right after it shows how much TOP redirected to another agency. If you see code 826 instead, the IRS applied your refund to its own back taxes — a different problem with a different fix.

- The offset notice the Bureau of the Fiscal Service mails after the fact. It lists your original refund, the amount offset, and the creditor agency with its phone number. Keep it — every dispute starts from that page.

Here's the full sequence from first warning to money gone, so you can see where you are:

| Stage | Who sends it | Your window |

|---|---|---|

| 1. Pre-offset notice (notice of intent to offset) | The creditor agency — loan holder, state revenue department, or child support agency | Typically at least 60 days to dispute, pay, or arrange payment before the debt is referred |

| 2. Debt certified to TOP | Creditor agency → Bureau of the Fiscal Service | The debt sits in the database until paid, settled, or withdrawn — every federal refund is screened against it |

| 3. You file; refund approved | IRS (code 846 posts to your transcript) | None — TOP screening happens automatically before payment |

| 4. Offset taken | Bureau of the Fiscal Service (code 898 posts) | None — the money moves before it reaches you |

| 5. Offset notice mailed | Bureau of the Fiscal Service | No fixed deadline to dispute with the creditor agency, but Form 8379 claims generally have a 3-year limit |

What happens if you ignore a Treasury offset

An offset that goes unaddressed repeats every filing season until the debt is gone — and the offset is usually only one of the tools the creditor agency is using. The sequence, if you do nothing:

- This year's refund is gone — up to 100% of it, applied to the debt, with the leftover flowing to the next debt in line if you have more than one.

- The debt keeps growing under the creditor agency's own interest and fee rules, so next year's offset may cover less of the balance than you expect.

- Next year's refund gets taken too. The debt stays certified until resolved — see will the IRS take my refund every year for how this loop works on the federal-tax side.

- The agency escalates beyond refunds. Defaulted federal student loans can move to administrative wage garnishment of your paycheck without a court order. States can levy bank accounts and wages under their own statutes — if you're already holding a state intent-to-levy notice, the offset didn't satisfy the state; it only reduced the balance.

- Other federal payments get screened. Certain federal payments beyond refunds run through TOP, including a capped share of Social Security benefits for federal non-tax debts.

The system that runs this is fully automated, and 2026's reduced IRS and agency staffing changed nothing about it — the database doesn't need a human to take next year's refund. The only thing that stops the cycle is resolving the underlying debt or getting it removed.

Refund seized and a levy still hanging over you?

If the offset took your refund and the underlying debt is still collecting — a state levy in motion, a loan in default, next year's refund already exposed — get a free review of exactly which agencies hold what and the fastest path to shut each one down. Call (888) 825-7779 or use the 2-minute form.

Your options after a tax refund offset

An offset can be disputed, partially recovered, or prevented from repeating — but each path runs through a different door, and using the wrong one wastes months. The IRS cannot return money TOP sent to another agency; only the creditor agency can.

| Option | Works when | Key limit or deadline |

|---|---|---|

| Dispute with the creditor agency | The debt isn't yours, was already paid, or the amount is wrong | No fixed federal deadline, but the debt stays certified — and takes next year's refund — until the agency removes it |

| Form 8379, Injured Spouse Allocation | A joint refund was taken for a debt that belongs only to your spouse | Generally within 3 years of the return; processing runs roughly 8–14 weeks |

| Exit student loan default (rehabilitation or consolidation) | The offset is for a defaulted federal student loan | Stops future offsets once you're out of default; money already offset generally stays applied to the loan |

| Agency hardship review | The offset causes documented hardship — eviction, utility shutoff | Agency-by-agency and discretionary; ask the creditor agency directly, and document everything |

| Offset bypass refund (OBR) | Hardship AND the money is being taken for IRS back taxes — not a TOP debt | Must be requested through the Taxpayer Advocate before the refund issues; it cannot bypass child support or other TOP debts |

| Pay or settle the underlying debt | The debt is valid and you can resolve it | Removes the debt from the database going forward — get written confirmation of removal |

| Adjust your W-4 withholding | Offsets will repeat and you need your money during the year | Doesn't fix the debt — it stops you from handing the database a lump sum every spring |

Two of these deserve emphasis. First, Form 8379 is the single most-missed recovery path: if you filed jointly and the debt — a defaulted loan, old child support, a state balance — belongs only to your spouse, your share of the refund was never legally theirs to take. Our injured spouse Form 8379 walkthrough covers the allocation math line by line, and if the debt traces to a former spouse's tax years, see ex-spouse's tax debt took my refund for the injured-spouse-versus-innocent-spouse fork.

Second, the offset bypass refund for hardship is real but narrow: the Taxpayer Advocate can sometimes release a refund that would otherwise go to IRS back taxes when you face immediate hardship — but it must happen before the refund issues, and it does not work against TOP debts like child support or student loans.

A worked example: where an $8,900 refund actually goes

Say you're a renter expecting an $8,900 refund — withholding plus credits — and you're counting on it because your state has already sent an intent-to-levy notice over a $3,400 state income tax balance. What you don't know is that a federal student loan from years back, now at $6,200 in default, was certified to TOP last fall.

Here's the math the database runs, in statutory order. No child support debt, so the federal non-tax debt goes first: $8,900 − $6,200 (student loan) = $2,700 remaining. The state debt is next in line: $2,700 − $3,400 = $0 to you, with $700 still owed to the state. You receive nothing — and because the state balance isn't fully paid, the state's levy threat is still live for the remaining $700.

Now change one fact: you filed jointly, and roughly $3,000 of the withholding came from your spouse's paychecks while both debts are yours alone. A properly allocated Form 8379 could recover your spouse's share of the refund — the offset only legally reaches the debtor's portion. Same refund, same debts, materially different outcome depending on one form.

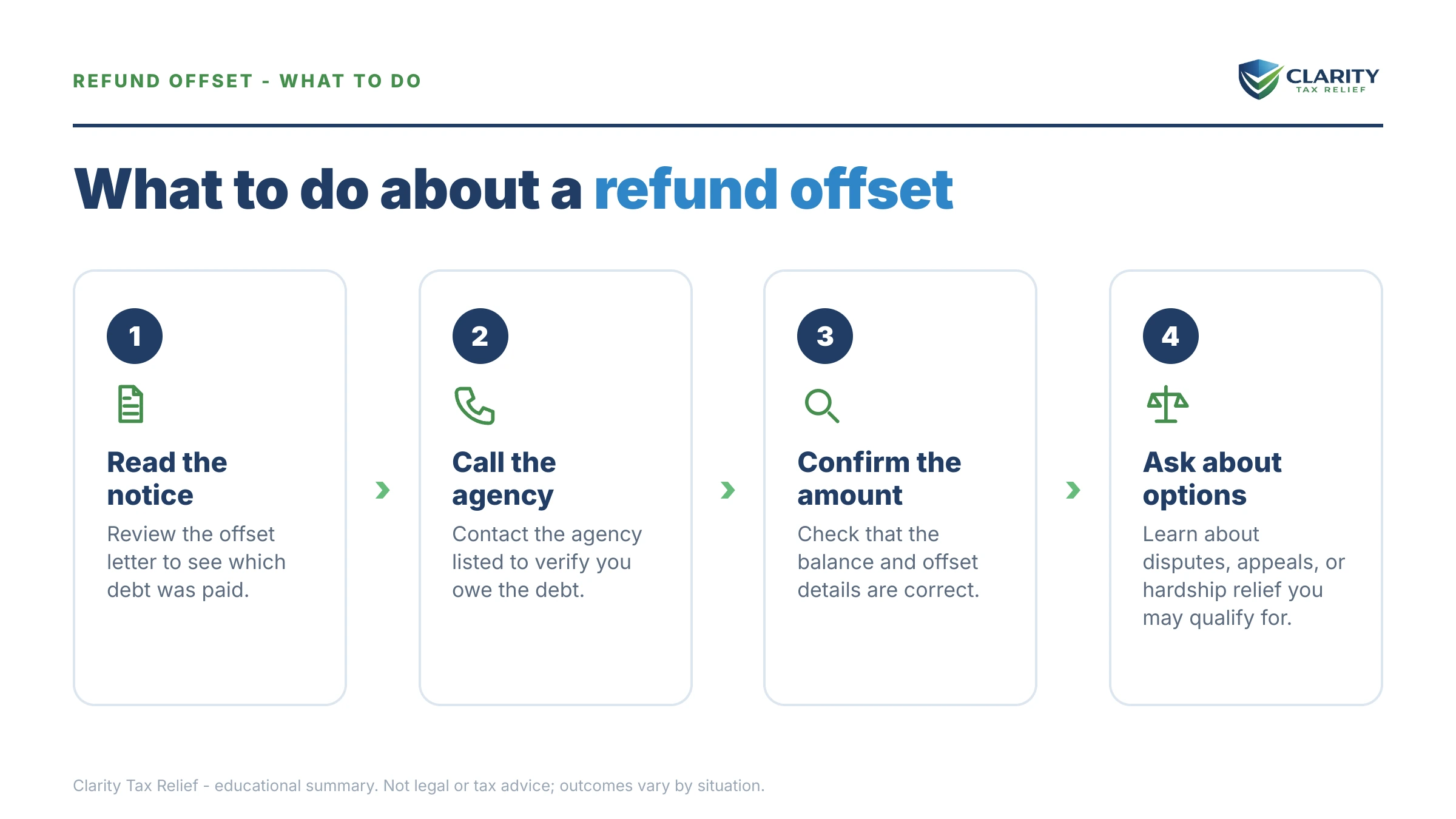

How to respond to a Treasury offset, step by step

- Call the offset line — dial 800-304-3107 and write down every debt, creditor agency, and phone number the automated system reads out.

- Pull your offset notice and transcript — match the Bureau of the Fiscal Service notice against your IRS account transcript; code 898 confirms a TOP offset, while code 826 or a CP49 means the IRS kept the refund itself.

- Contact the creditor agency — dispute in writing if the debt is wrong, paid, or not yours, and ask about that agency's hardship review if the offset leaves you unable to pay rent or utilities.

- File Form 8379 if the debt is your spouse's alone — the Injured Spouse Allocation recovers your share of a joint refund taken for a debt that isn't yours.

- Stop the next offset — resolve or restructure the underlying debt, and adjust your W-4 so next year's money arrives in your paycheck instead of as an offsettable refund.

When you can handle this yourself

Many offsets need no professional help at all. If the debt is valid, clearly yours, and you filed single — a loan you know you defaulted on, a state balance you recognize — your job is simply to work the creditor agency's process: get out of default, set up payments, or pay it off. The how to settle tax debt yourself guide covers the DIY playbook for the tax-debt side.

Experienced help changes the outcome when the pieces stack: a state levy already in motion on a balance the offset only partly paid, a joint refund where the injured-spouse allocation is worth thousands, offsets hitting multiple years at once, or IRS and TOP debts layered so that fixing them in the wrong order costs you money. An experienced tax professional's value here is sequencing — knowing which agency to neutralize first and which recovery claims are actually worth filing.

Terms on your offset notice, decoded

- Bureau of the Fiscal Service (BFS): the Treasury Department bureau that operates TOP and sends the offset notice — it's the toll collector, not the creditor.

- Offset: money taken from a government payment before it reaches you — different from a levy, which seizes money already in your hands or accounts.

- Creditor agency: the agency you actually owe — the only party that can refund an erroneous offset or remove the debt from the database.

- Pre-offset notice: the written warning the creditor agency must mail before certifying your debt, typically at least 60 days ahead — often the letter that went to your old address.

- Injured spouse: a spouse whose share of a joint refund was taken for the other spouse's separate debt — recoverable via Form 8379.

- Code 898: the transcript entry showing your refund (or part of it) was transferred to a non-IRS agency through TOP.

Treasury Offset Program questions, answered

How do I know if my tax refund will be taken by the Treasury Offset Program?

Call the TOP call center at 800-304-3107 before you file — the automated system tells you whether a debt is loaded against your Social Security number and which agency submitted it. You can also watch your IRS account transcript: code 898 posts when a non-IRS debt takes part or all of your refund. The database changes constantly, so check again close to filing.

Can I get my money back after a Treasury offset took my refund?

Sometimes. If the debt was wrong, already paid, or not yours, the creditor agency that received the money — not the IRS — is responsible for refunding it, so dispute directly with the agency listed on your offset notice. If the refund was joint and the debt belongs only to your spouse, Form 8379 can recover your share, generally within three years of the return.

Does the IRS use the Treasury Offset Program for back taxes?

No. The IRS keeps refunds for its own back taxes internally, before TOP ever screens the money, and sends a CP49 notice showing which year the refund was applied to. TOP handles everyone else: past-due child support, defaulted federal student loans, state income tax, and other government agency debts. Different debt, different notice, different dispute path.

Will the Treasury Offset Program take my whole refund?

It can. Tax refund offsets are not capped — TOP takes up to 100% of your refund, up to the balance of the debt, and if the first debt doesn't exhaust the refund, the remainder flows to the next certified debt in line. Only what's left after every debt in the database is paid reaches your bank account.

My spouse's debt took our joint refund — can I get my half back?

Yes, if the debt legally belongs only to your spouse. File Form 8379, Injured Spouse Allocation, to recover the portion of the refund tied to your own income, withholding, and credits. Expect roughly 8 to 14 weeks of processing depending on how you file it. In community property states the split follows state law, so your share may differ from a simple 50/50.

Can the Treasury Offset Program take Social Security or other federal payments?

Some, yes. Certain federal payments beyond tax refunds are screened by TOP, and Social Security benefits can be offset up to 15% for federal non-tax debts, with a protected floor set by federal rules. SSI is exempt. If a benefit offset would leave you unable to cover basic living expenses, ask the creditor agency about a hardship reduction.

How much warning do I get before a Treasury offset?

The agency that holds your debt must send a written notice of intent to offset — typically at least 60 days before referring the debt — to your last known address. Many people never see it because it goes to an old address, which is why offsets feel like they come out of nowhere. Once the debt is certified, the offset itself happens with no additional warning.

Will my refund be offset every year until the debt is paid?

Yes. A debt stays in the TOP database until it is paid, settled, or removed by the creditor agency, and every future federal refund is screened against it. Fixing the underlying debt — or adjusting your withholding so you stop generating large refunds — is the only way off that treadmill.

Your next 24 hours

- Find the creditor agency on your offset notice — the agency name, the amount taken, and the phone number are the three facts every recovery path starts from. No notice yet? Call 800-304-3107 and get the same information from the automated system.

- Gather your paperwork — the offset notice, last year's return, your IRS account transcript, and any proof the debt was paid or isn't yours (payment records, loan statements, a divorce decree).

- Get a free case review — if the offset only dented a debt that's still collecting against you, or a joint refund was taken for a spouse's debt, call (888) 825-7779 or use the form at the top of this page. Interest and fees on the underlying debt accrue either way; the review costs nothing.

Primary sources: the Bureau of the Fiscal Service's official Treasury Offset Program page, the IRS's Tax Topic 203 on reduced refunds and offsets, and the Taxpayer Advocate Service for hardship situations involving IRS-held refunds.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.