Spouse Tax Relief

Ex-Husband's Tax Debt Took My Refund: How to Get It Back in 2026

The short answer: if your refund was taken for your ex-husband's tax debt, the fix depends on whose debt it legally is. Debt from a joint return you signed calls for innocent spouse relief (Form 8857). If the debt is legally only his, injured spouse Form 8379 recovers your share — and both can reclaim money already taken.

You checked "Where's My Refund" expecting a deposit date and found the money gone — applied to a tax bill from a marriage that ended years ago. If you're searching "ex husband's tax debt, my refund taken," you're standing exactly where the divorce was supposed to protect you, and it didn't. That's infuriating — and it's also fixable, because the IRS has two formal relief paths built for this exact situation, each with its own form and its own clock.

⏱ Your deadline: you generally have 2 years from the IRS's first collection activity against you to request innocent spouse relief under sections 6015(b) and 6015(c) — and a refund offset counts as collection activity. This offset may have started that clock. Equitable relief and injured spouse claims have longer windows, but the strongest relief types expire first.

Why the IRS took your refund for your ex-husband's tax debt

The IRS took your refund because, in its records, the debt is yours too — a joint return you signed during the marriage created joint and several liability, meaning the IRS can collect 100% of the balance from either spouse, forever, regardless of who earned the income or what the divorce decree says.

This wasn't a person deciding to punish you. Before the IRS releases any refund, its system automatically checks every Social Security number on the return against open balances. If your SSN appears on an old joint liability with your ex, the refund is applied to it before you ever see a dime. You'll get a CP49 notice — refund applied to back taxes confirming what happened; if you've remarried and the offset hit a debt tied to only one spouse on the new return, a CP42 notice arrives instead.

One important distinction up front: this is an IRS-internal offset for a federal tax debt. It's different from a Treasury Offset Program seizure for child support or student loans, and different again from a state refund taken for IRS debt — each has its own dispute path, so identifying which one hit you is step one.

Injured spouse vs. innocent spouse: which fix matches your situation

Injured spouse relief recovers your share of a seized refund; innocent spouse relief removes you from the debt itself — and picking the wrong one wastes months. The full comparison lives in our injured spouse vs. innocent spouse guide, but here's the fast sort:

- The debt is from a joint return you signed with your ex (an audit, a CP2000 he ignored, or a balance he promised to pay). Legally it's your debt too, so "injured spouse" doesn't apply — you need innocent spouse relief on Form 8857 to be removed from the liability.

- You've remarried and this year's joint refund with your new husband was seized for your old joint debt with your ex. Your new husband is the injured spouse — his share comes back on Form 8379. (This is its own scenario; see our guide to a new spouse's refund taken for old debt.)

- The debt is legally only his — his separate-filing years, his business payroll taxes, or years before you married — and your own refund was still taken. That shouldn't happen. Pull your notice and transcript and dispute the offset; if your SSN was attached to his debt in error, the IRS must correct it.

Many divorced readers end up needing both forms in the same year: Form 8379 to rescue the new household's share of this refund, and Form 8857 to attack the underlying joint debt so next year's refund isn't taken too.

What happens if you do nothing

A refund offset is not a one-time event — it repeats every filing season until the joint balance is gone or you are removed from it. Here's the sequence if you let it ride:

- This year's refund is applied and the CP49 or CP42 confirms it. The balance shrinks by your money, not his.

- Interest and the monthly failure-to-pay penalty keep accruing on whatever remains, so part of what the offset "paid" grows back.

- Next year's refund is taken automatically — no new notice of intent, no warning. Offsets continue year after year until the debt is paid or the collection statute expires.

- Collection can escalate beyond refunds. Because you're jointly liable, the IRS can file a lien against your property or levy your wages and bank account — not just his — if the automated notice sequence runs its course.

- Your two-year window quietly closes. Relief under sections 6015(b) and 6015(c) — the two strongest innocent spouse paths — must generally be requested within two years of the first collection action against you. Wait, and you may be left with only equitable relief, which is harder to win.

The bitter irony of waiting: every offset collects the debt from the spouse who didn't create it, while your ex feels no pressure at all.

Your refund is gone — and the clock may already be running

A refund offset can start the two-year innocent spouse deadline. Send us your CP49 or CP42 and a quick summary of the debt's history — an experienced tax professional will tell you which relief path fits and whether money already taken can come back. Free, confidential, no pressure.

How to get your refund back: every option compared

Four distinct relief paths exist, and eligibility turns on how the debt arose, when you divorced, and what you knew. This table sorts them:

| Relief path | When it fits | Key eligibility requirement | Form & deadline |

|---|---|---|---|

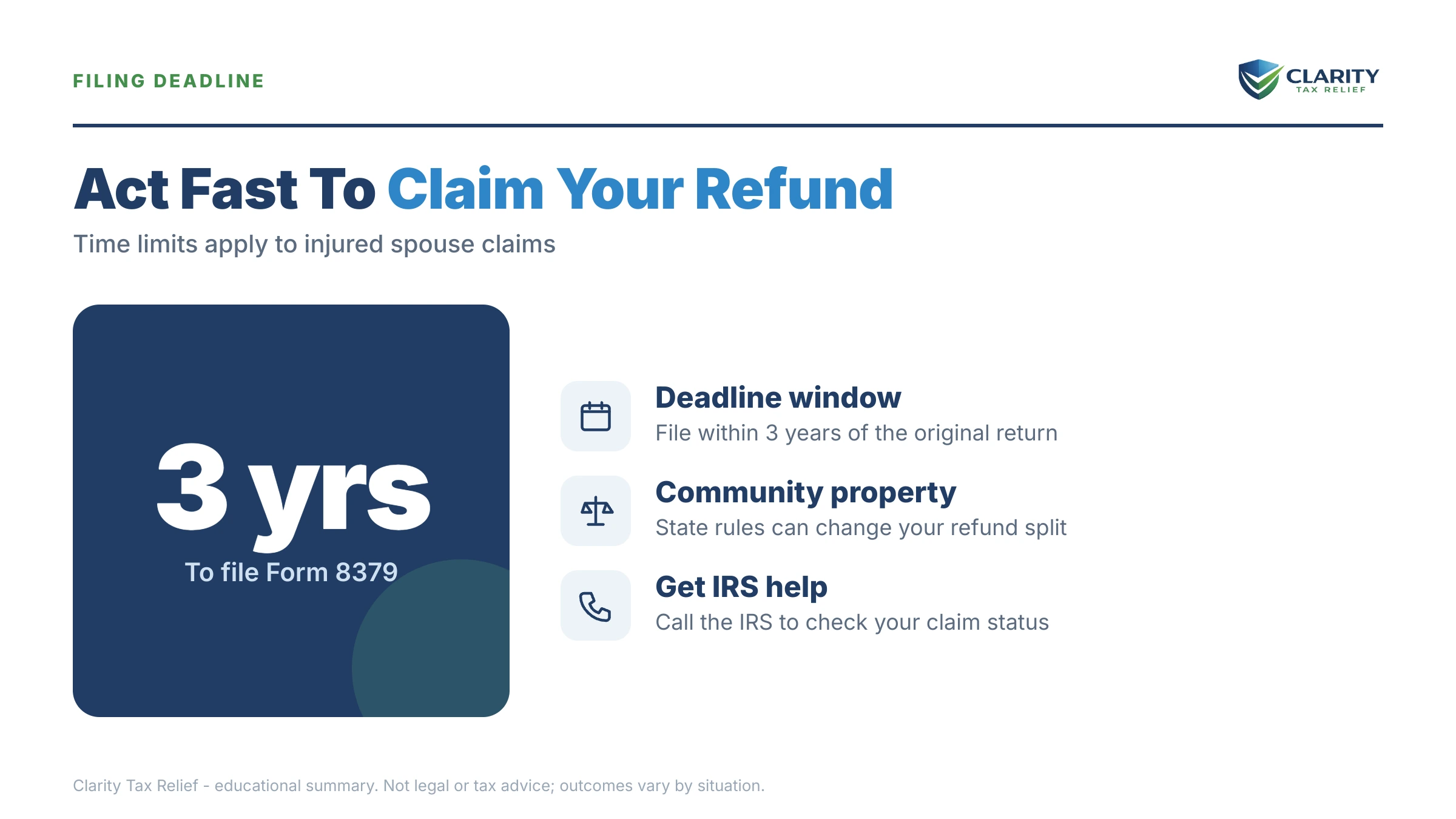

| Injured spouse allocation | The debt is legally only one spouse's; part of a joint refund belonged to the other (e.g., a new husband's share) | The injured spouse must have their own income, withholding, or refundable credits on the offset return | Form 8379 — generally within 3 years of the return's due date |

| Innocent spouse relief — §6015(b) | Extra tax came from your ex's unreported income or false deductions on a joint return | You didn't know and had no reason to know about the understatement, and holding you liable would be unfair | Form 8857 — within 2 years of first collection activity |

| Separation of liability — §6015(c) | You're divorced, legally separated, or have lived apart 12+ months | The understatement is split by who earned the income; no actual knowledge of the item when you signed | Form 8857 — within 2 years of first collection activity |

| Equitable relief — §6015(f) | The debt was reported but never paid (an underpayment), or (b) and (c) don't fit | Fairness factors: economic hardship, abuse, financial control by your ex, who benefited from the money | Form 8857 — any time before the 10-year collection statute ends |

Two details in that table decide most cases. First, sections 6015(b) and (c) only cover understatements — extra tax the IRS added after the return was filed, like an audit or CP2000 assessment. If your ex simply reported the tax and never paid it, your only door is equitable relief under section 6015(f). Second, being divorced is a genuine advantage: it's the entry ticket to separation of liability relief, which splits the debt by who earned the income — often the cleanest win for an ex-wife whose husband's side business created the bill.

Two honest caveats. Filing Form 8857 pauses IRS collection against you while it's reviewed, but it also pauses the 10-year collection statute — you can estimate where your debt stands on that clock with our CSED Calculator. And if every relief path fails, you remain jointly liable; at that point the question becomes resolving the balance itself through a payment plan, hardship status, or an offer — our guide on how to settle tax debt yourself walks through those options.

What it costs and how long it takes

Every relief request in this fight is free to file — the real cost is time, and in 2026 the IRS workforce is roughly 27% smaller, so build patience into your plan:

| Option | IRS cost | Typical timeline | If it succeeds |

|---|---|---|---|

| Form 8379 injured spouse claim | $0 | Typically 2–3 months; longer amid 2026 processing delays | The injured spouse's share of the refund is returned |

| Form 8857 innocent spouse request | $0 | Commonly 6 months or more | You're removed from your ex's share of the debt; amounts collected from you may be refunded |

| Appeal of a denied 8857 | $0 | Several additional months | IRS Appeals re-reviews with fresh eyes and better documentation |

| Tax Court petition after final determination | $60 filing fee | Often a year or more | An independent judge decides your relief claim |

| Payment plan on any balance that stays yours | $0 setup for short-term plans; a modest fee for longer agreements | Can be set up online the same day | Enforced collection stops while you pay; interest continues |

A worked example: $27,500 of his debt, $6,400 of your refund

Say your 2021 joint return with your ex-husband drew a CP2000 for 1099 income he never told you about. He ignored it, the IRS assessed the tax plus an accuracy penalty, and with interest the balance now sits at $27,500. You divorced in 2023; the decree says he pays it. This spring you filed jointly with your new husband and your $6,400 refund vanished — applied to that balance, with a CP49 in the mailbox.

Break the refund down. Your withholding on $38,000 of wages contributed roughly $2,300 of it; your new husband's withholding on $71,000 contributed roughly $4,100. Here's how the two forms work together:

- Form 8379 allocates the refund between the new spouses by income, withholding, and credits. Your new husband's share — roughly $4,100 in this example — comes back to him, because the 2021 debt was never his. (In a community property state, the allocation follows state law and his recovery may be smaller.)

- Form 8857 attacks the $27,500 itself. If you can show you didn't know and had no reason to know about the hidden 1099 income — separate bank accounts, no lifestyle change, he handled the filings — section 6015(b) can remove you from the entire liability and refund your $2,300 share too. Since you're divorced, section 6015(c) is a backstop: the understatement came from his income, so it allocates to him.

- If relief is granted, the $27,500 becomes his problem alone, and your future refunds stop being seized. If only the 8379 succeeds, the IRS keeps your $2,300 — and takes your share again next year until the underlying liability is resolved.

This is a hypothetical, and real allocations depend on the exact numbers — but the structure holds for almost every remarried reader in this situation: 8379 rescues this year, 8857 ends the cycle.

How to respond, step by step

- Confirm which debt took your refund. Read the notice — a CP49 means the refund paid a tax debt on an account with your name on it; a CP42 means it paid your current spouse's debt. Match the tax year on the notice to the years you filed jointly with your ex.

- Pull the account transcript for the debt year. It shows whether the balance came from an audit, a CP2000 underreporter notice, or simply an unpaid return — which determines whether section 6015(b), (c), or (f) fits your facts.

- Choose the right form. File Form 8857 if the debt is from a joint return you signed with your ex. File Form 8379 if the debt is legally only one spouse's and part of the seized refund belonged to the other.

- File with documentation. Attach your divorce decree, proof of who earned the income, and anything showing you did not know about it — thin paperwork is the top reason innocent spouse requests fail.

- Protect next year's refund. File Form 8379 with every joint return while the debt is open, or adjust withholding so you are not handing the IRS a large refund to seize.

- Get experienced help for a large or denied claim. Innocent spouse cases are fact-intensive. An experienced tax professional can frame the knowledge, hardship, and abuse factors correctly before the IRS decides — not after a denial.

Our line-by-line walkthroughs of both forms — the injured spouse Form 8379 walkthrough and the Form 8857 walkthrough — cover the allocation math and the questionnaire the IRS actually scores. The official form pages are at IRS.gov: About Form 8379 and IRS.gov: About Form 8857.

The divorce decree says he pays — why the IRS doesn't care

A divorce decree binds you and your ex-husband; it does not bind the IRS, which was never a party to your divorce. The agency will collect from whichever spouse has a refund to seize or wages to levy — usually the one who stayed compliant. The decree still matters in two places: a state family court can hold your ex in contempt and order him to reimburse you, and the decree is supporting evidence for a section 6015(c) request. The full explanation — and what a decree can and can't do — is in our guide to the divorce decree vs. IRS debt.

When you can handle this yourself — and when help changes the outcome

A straightforward injured spouse claim is genuinely DIY territory. If you've remarried, the debt is clearly from your old marriage, and the allocation is simple wage withholding, Form 8379 is arithmetic plus patience — no professional needed. The same goes for calling to dispute an offset that hit a debt that was never legally yours.

Innocent spouse relief is a different animal. The IRS denies many first-time 8857 requests, usually because the "knowledge" and fairness factors weren't documented — not because the taxpayer didn't deserve relief. Experienced help tends to change outcomes when: the balance is large (like our $27,500 example); the debt spans multiple joint years; your ex hid income or controlled the finances (see how to qualify for innocent spouse relief); there was abuse or financial coercion; you live in a community property state; or you've already been denied once and are heading to Appeals or Tax Court — the playbook for that is in our guide to innocent spouse relief denied. If money is tight, a Low Income Taxpayer Clinic or the Taxpayer Advocate Service can also assist at no cost.

Terms on your notice, decoded

- Refund offset: the IRS applying your refund to an existing balance before paying you — automatic, and repeated every year the debt stays open.

- Joint and several liability: the rule that each spouse on a joint return owes 100% of the tax, so the IRS can collect the whole debt from either one.

- CP49 / CP42: the notices confirming an offset — CP49 for a debt on your own account, CP42 for a debt belonging to your spouse on the return.

- Understatement vs. underpayment: an understatement is tax the IRS added later (audit, CP2000); an underpayment is tax reported but never paid. The distinction decides which relief section applies.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, after which the IRS can no longer collect, though relief requests and appeals pause the clock.

Ex-husband tax debt refund questions, answered

Can the IRS take my refund for my ex-husband's taxes after we're divorced?

Yes, if the debt comes from a return you filed jointly with him. Signing a joint return makes you jointly and severally liable, meaning the IRS can collect the entire balance from either person regardless of what the divorce decree says. If the debt is from his separate returns or his business, your own refund should not be taken for it — and if it was, dispute the offset right away.

Does my divorce decree protect me if it says he pays the tax debt?

No. The IRS was not a party to your divorce, so the decree does not bind it — the agency collects from whichever spouse is easier to reach. The decree is still useful: a state court can enforce it against your ex, and it supports a separation-of-liability request under section 6015(c). But the only way to stop IRS collection against you is relief granted by the IRS itself.

How long do I have to request innocent spouse relief?

Generally two years from the IRS's first collection activity against you for relief under sections 6015(b) and 6015(c) — and a refund offset counts as collection activity, so this year's seized refund may have started that clock. Equitable relief under section 6015(f) is more forgiving: you can request it any time before the 10-year collection statute runs out, or within the refund window if you are asking for money back.

What's the difference between Form 8379 and Form 8857?

Form 8379 (injured spouse) recovers your share of a refund taken for a debt that is legally only your spouse's — you are not disputing the debt, just the seizure of your portion. Form 8857 (innocent spouse) asks the IRS to remove you from liability for a joint debt itself. If the offset paid a balance from a joint return with your ex, you need Form 8857; if your new spouse's refund share was taken for your old debt, that is Form 8379.

Will the IRS keep taking my refund every year until his debt is paid?

Yes. Refund offsets repeat automatically every filing season until the balance is paid, the 10-year collection statute expires, or you are removed from the liability. Filing Form 8379 with each joint return protects a new spouse's share going forward, and winning innocent spouse relief ends the offsets entirely. Some people also reduce their withholding so there is no large refund to seize.

Can I get back a refund the IRS already took?

Often, yes. An injured spouse allocation can generally be filed up to three years from the return's original due date, even after the money is gone. If you win innocent spouse relief under section 6015(b) or 6015(f), the IRS can refund amounts it collected from you — including offset refunds — while you are within the refund statute. Separation of liability under 6015(c) stops future collection but does not generate refunds.

Does injured spouse relief work differently in community property states?

Yes. In community property states such as California, Texas, and Arizona, the IRS allocates a joint refund under state law, which can treat half of each spouse's income and withholding as belonging to the other. That often shrinks what an injured spouse recovers. Community property states also have a separate relief rule, section 66(c), for income your ex controlled — worth raising if you live in one of these states.

What if my innocent spouse request is denied?

You can appeal inside the IRS, and after a final determination you have 90 days to petition the U.S. Tax Court, where a judge reviews your case independently. Many first requests fail on thin documentation — proof you did not know about the income, or evidence of hardship or abuse, often changes the result. Read our guide to what to do when innocent spouse relief is denied before giving up.

Your next 24 hours

- Find the notice. Locate the CP49 or CP42 and note the tax year and the exact amount applied — that year tells you instantly whether the debt is from a joint return with your ex.

- Gather your proof. Pull your divorce decree, this year's return, the joint returns from the marriage, and anything showing whose income created the debt and what you knew about it.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form — the two-year window for the strongest innocent spouse relief may already be running from this offset, and the right form filed now can bring seized money back.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.