Innocent Spouse Relief

IRS Equitable Relief in 2026: Section 6015(f) When You Don't Qualify for Other Innocent Spouse Relief

The short answer: IRS equitable relief under Section 6015(f) removes your responsibility for a joint tax debt that fairly belongs to your spouse or ex-spouse. It's the only innocent spouse category that covers tax that was reported correctly but never paid, and you can request it on Form 8857 any time the IRS can still collect.

The return you signed was accurate. The problem is the balance on it was never paid — and because both names are on that return, the IRS is now collecting from you, the one with the visible 1099 income and the reachable bank account. Equitable relief exists for exactly this gap: the joint debt that the other two innocent spouse programs can't touch because there was no error on the return, only a broken promise to pay it.

Two facts set IRS equitable relief apart from every sibling program. First, it's the only Section 6015 category that covers underpayments — tax shown on the return but never paid — not just extra tax from an audit. Second, it has no two-year deadline: you can request it for as long as the IRS can legally collect the debt. Farther down the page, an image shows exactly what Form 8857 looks like and where the questions that drive an equitable-relief decision sit — worth seeing before you start writing your own answers.

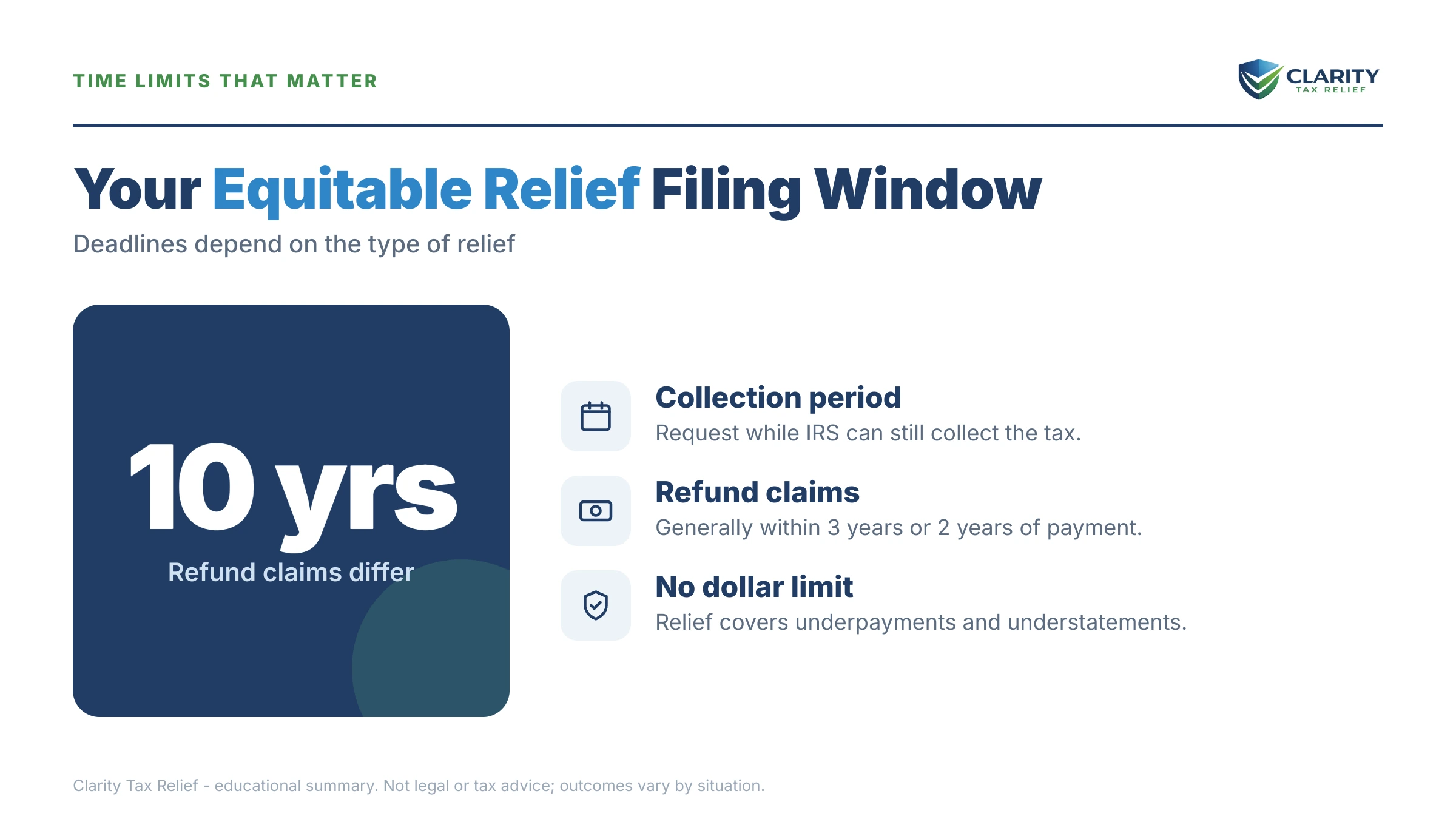

⏱ Your real clocks: for an unpaid balance, you can request equitable relief any time before the 10-year collection statute (CSED) on that debt expires. To get back money you already paid or had offset, you must file within the refund window — generally 3 years from when the return was filed or 2 years from the payment. Every month you wait, interest and the monthly late-payment penalty keep growing the joint balance the IRS is chasing you for.

Why the IRS can bill you for your ex's share of the tax

Signing a joint return makes each spouse legally responsible for 100% of the tax on it — not half. The IRS calls this joint and several liability, and it survives divorce, separation, and even a divorce decree that assigns the debt to your ex. The government's collection computers don't read family-court orders; they read the two names and Social Security numbers on the return.

In practice, the IRS collects from whichever spouse is easier to reach. If your ex is unemployed, self-dealing, or gone, and you're a contractor with 1099s reporting your income to the IRS every January, the notices come to you. That's not the system judging you — it's automation following the money it can see.

Section 6015 is Congress's fix. It contains three separate relief programs, and equitable relief under subsection (f) is the safety net beneath the other two: it exists precisely for people who fail the strict tests of innocent spouse relief and separation of liability but who, on the whole facts, shouldn't be stuck with the bill.

What happens if you never request relief

A joint tax debt follows both spouses through the full IRS collection sequence, no matter what a divorce decree says. If you do nothing, the debt is treated as fully yours, and the machine escalates in a predictable order:

- Refund offsets, every year. Any federal refund you're owed — including one built on your own quarterly estimated payments — is seized and applied to the joint balance until it's gone.

- The balance-due notice sequence. Bills escalate from a first notice through CP504 (intent to levy your state refund) to LT11, the final notice that opens the door to levies after its 30-day window.

- A federal tax lien. The lien attaches to everything you own — including property you acquired after the divorce — and complicates selling or refinancing a home.

- Levies on your income. For a 1099 contractor this is especially painful: the IRS can garnish 1099 income by levying a client, which can capture an entire invoice at once rather than a slice of a paycheck.

- Compounding growth. The failure-to-pay penalty adds 0.5% per month while interest compounds daily — a debt your ex created keeps getting bigger under your name.

None of this waits for a human to review the fairness of your situation. In 2026, with IRS staffing down sharply, the people are harder to reach — but the automated offsets, liens, and levies never stopped. Fairness only enters the picture when you formally ask for it on Form 8857.

Being collected on for a tax debt that isn't fairly yours?

Get your equitable relief case reviewed free before another refund is offset or a levy reaches your contractor pay. An experienced tax professional will map your facts against the Section 6015(f) factors and tell you honestly whether Form 8857 is worth filing — (888) 825-7779 or the 2-minute form.

Your options under Section 6015 — and why equitable relief is often the only open door

Section 6015 contains three distinct relief programs, and equitable relief is the only one that reaches a tax bill that was reported correctly but never paid. The other two apply only to understatements — extra tax the IRS added after finding an error on the return — and both carry a hard two-year deadline that starts with the IRS's first collection activity against you. If your situation is an unpaid balance, or your two years have run, subsection (f) is the door that's still open.

| Relief type | Covers | Core requirement | Deadline |

|---|---|---|---|

| Innocent spouse relief — §6015(b) | Understatements only (errors on the return) | You didn't know and had no reason to know of the error | 2 years from first IRS collection activity |

| Separation of liability — §6015(c) | Understatements only; splits the deficiency | Divorced, widowed, legally separated, or living apart 12+ months; no actual knowledge of the item | 2 years from first IRS collection activity |

| Equitable relief — §6015(f) | Understatements and unpaid balances | Unfair to hold you liable, weighed under the Rev. Proc. 2013-34 factors | Any time the CSED is open (refunds: 3-year/2-year window) |

| Injured spouse — Form 8379 (not §6015) | Your refund taken for your spouse's separate debt | The debt was never yours to begin with | Refund statute on the offset year |

That last row trips people up constantly: if the debt was never yours at all — your refund was grabbed for your spouse's old, separate liability — you want injured spouse allocation, a different form and a much simpler fight. Our comparison of injured spouse vs. innocent spouse sorts you into the right lane in two minutes.

Do you qualify? The seven threshold conditions for IRS equitable relief

Before the IRS weighs any fairness factors, your request must clear seven gate conditions — miss one and the analysis stops. Under Revenue Procedure 2013-34, you must show:

- A joint return was filed for the year at issue (or you're seeking parallel relief under IRC §66(c) for community income — see community property tax relief if you live in a community property state and didn't file jointly).

- Relief isn't available under §6015(b) or (c) — which is automatic for underpayment cases, since those programs can't touch them.

- The request is timely — CSED still open for balance relief; refund statute open for money back.

- No fraudulent asset transfers between you and your spouse designed to cheat the IRS or another third party.

- No disqualified assets were transferred to you by your spouse (with exceptions, including where abuse or financial control was involved).

- You didn't knowingly participate in filing a fraudulent return.

- The tax is attributable to your spouse — their income, their withdrawal, their business. Exceptions exist where the item was nominally yours, where your spouse misappropriated money meant for the tax, where abuse prevented you from challenging the return, or where community property law created the attribution.

That last condition is the one that most often shapes a real case, and it's why the worked example below splits a single balance into a relieved share and a kept share.

How the IRS decides: the seven Rev. Proc. 2013-34 factors

Once past the gates, equitable relief is decided by weighing seven factors — no single factor controls, and the IRS is instructed to look at the whole picture rather than count votes. This is where cases are won or lost, because each factor is only as strong as the evidence behind it.

| Factor | Weighs toward relief when… | Weighs against when… |

|---|---|---|

| Marital status | You're divorced, widowed, legally separated, or living apart 12+ months | Neutral if still together — never counted against you |

| Economic hardship | Paying would leave you unable to meet basic living expenses | Neutral if you can pay without hardship |

| Knowledge / reason to know | You reasonably believed your spouse would pay the reported tax (underpayment) or didn't know of the error (understatement) | You knew the tax wouldn't be paid or knew of the error — unless abuse or financial control neutralizes it |

| Legal obligation | The divorce decree makes your ex responsible for the debt | The decree puts it on you |

| Significant benefit | You got no benefit beyond normal support from the unpaid tax | The unpaid money funded a lifestyle upgrade you shared in |

| Tax compliance | You've filed and paid properly in the years since | You have your own unfiled years or new balances |

| Mental / physical health | Illness at signing or at the time of the request impaired you | Neutral if health wasn't a factor |

Abuse changes the math on everything. Rev. Proc. 2013-34 explicitly instructs the IRS to weigh abuse — physical, psychological, or financial control — heavily, and it can flip the knowledge factor entirely: even if you knew the tax wouldn't be paid, knowing wasn't the same as being able to do anything about it. If your spouse hid money or controlled every account, document it; our guide on what to do when your spouse hid income from me walks through building that record. And note the compliance factor: filing and paying cleanly now, as a contractor making quarterly estimates, actively strengthens the request you file later.

One more point on the legal-obligation factor: the decree helps your case, but it doesn't replace it. The IRS is not a party to your divorce, which is why a decree alone never stops collection — the full explanation is in divorce decree IRS debt.

The streamlined determination: equitable relief's fast lane

The IRS grants equitable relief without full factor-balancing when three conditions are all met. Under the streamlined determination in Rev. Proc. 2013-34, you qualify directly if:

- you're no longer married to the other spouse (divorced, widowed, legally separated, or living apart at least 12 months), and

- you'd suffer economic hardship if forced to pay, measured against the IRS's allowable living expense standards, and

- you didn't know of the understatement — or, for an unpaid balance, reasonably expected your spouse to pay when you signed.

Hit all three and the analysis ends in your favor. Miss any one — say, your income comfortably exceeds allowable expenses — and the request isn't dead; it simply drops into the seven-factor weighing above, where a strong overall story can still win.

Worked example: a $27,500 joint balance, line by line

Say you're a 1099 graphic-design contractor, divorced last year. Two years ago you filed a joint return that was completely accurate — but it showed $27,500 due, and your ex, who handled all the money, promised to pay it from a year-end distribution. They didn't. Here's how the equitable-relief math actually plays out:

- Attribution first. Of the $27,500, say $22,600 traces to your ex's early 401(k) cash-out (the income tax plus the 10% early-withdrawal addition), and $4,900 is the income and self-employment tax on your own contracting income. Equitable relief can only reach the $22,600 attributable to your ex — the $4,900 from your 1099 work stays yours regardless of the outcome ($22,600 + $4,900 = $27,500).

- Streamlined check. Divorced? Yes. Hardship? Your net self-employment income runs about $4,100/month against roughly $4,300 in IRS-allowable living expenses — paying the debt would break basic expenses, so hardship holds. Knowledge? You have texts where your ex confirms they'll pay "when the distribution hits," and the decree assigns the debt to them. All three prongs land — a streamlined grant is realistic.

- The result if granted. The $22,600 plus its share of penalties and interest comes off your account. You resolve the remaining ~$4,900 yourself — at that size, a short-term IRS payment plan (up to 180 days, $0 setup fee) usually closes it out.

- The refund angle. If the IRS already offset, say, a $1,800 refund of yours against the joint balance within the last two years, the Form 8857 can ask for that money back too — a request separation of liability could never make.

This is a hypothetical, and the IRS decides each case on its full facts — but the structure is the structure: split the balance by attribution, test the streamlined prongs, then weigh factors on whatever's left in dispute.

Deadlines, rights, and what filing Form 8857 pauses

Equitable relief has no two-year deadline — the window for an unpaid balance stays open as long as the 10-year collection statute does. That statute is the CSED, ten years from assessment, though appeals, offers, bankruptcy, and the innocent spouse claim itself can pause and extend it — the mechanics are in our guide to how long the IRS can collect back taxes, and you can estimate your own expiration dates with our CSED Calculator.

| Window | The clock | If it passes |

|---|---|---|

| Relief from an unpaid balance | Open until the debt's CSED expires (10 years from assessment, pausable) | The IRS can no longer grant relief — but it also can no longer collect |

| Refund of amounts paid or offset | Generally 3 years from filing or 2 years from the payment | Money already taken stays gone, even if relief is granted going forward |

| Appeal of a preliminary denial | The window printed on your preliminary determination letter | You lose the IRS Appeals review and move straight to a final determination |

| Tax Court petition | 90 days from the final determination | You lose independent court review of the denial |

| While your request is pending | Levies against you generally paused; CSED suspended | — (note: refunds can still be offset, and the debt's expiration date moves later) |

Two practical warnings hide in that table. First, waiting costs refund money: every year the offset machine takes another refund, and offsets older than the refund window are unrecoverable. Second, filing pauses the CSED — if your claim fails, the IRS gets that pending time added back to collect. Neither is a reason not to file a strong case; both are reasons not to file a weak one carelessly.

How to request equitable relief, step by step

- Confirm your category — verify the debt comes from a joint return, and identify whether it is an unpaid balance (equitable relief is your only door) or an audit adjustment (compare all three Section 6015 programs first).

- Check both clocks — relief from an unpaid balance is available while the 10-year collection statute is open; a refund of money already paid must be claimed within roughly three years of filing or two years of the payment.

- Gather your evidence — collect the joint return, divorce or separation decree, records showing whose income created the tax, proof your spouse controlled the money or promised to pay, and any abuse or health documentation.

- Complete Form 8857 — one form covers all years at issue. Answer every question that maps to a Rev. Proc. 2013-34 factor, and attach a written statement telling your story factor by factor.

- File it and respond fast — send the form per its instructions, keep copies, and answer every IRS letter promptly — expect the IRS to contact your ex and expect the review to take six months or more.

- Appeal a denial — request an appeal within the window printed on your preliminary determination letter, and if the final determination goes against you, petition the U.S. Tax Court within 90 days.

The form itself is longer than people expect — a line-by-line companion is in our Form 8857 walkthrough. The image below shows exactly what the form looks like and where to focus your attention, so you know what you're building toward before the blank pages arrive. And if the answer comes back no, a denial is the middle of the process, not the end — the appeal path is mapped in innocent spouse denied.

When you can handle this yourself — and when help changes the outcome

Plenty of equitable relief requests are genuinely DIY-able. If your facts are streamlined-clean — you're divorced, the debt traces entirely to your ex's income, your budget clearly fails the hardship test, and you have the decree and payment-promise messages in hand — a carefully completed Form 8857 with organized attachments is something you can do on your own. The same goes for the leftover balance that stays yours: a small amount you can pay within 180 days doesn't need professional help, and the DIY playbook in how to settle tax debt yourself covers those mechanics.

Experienced help tends to change outcomes in four situations. Abuse or financial-control cases, where the evidence must be assembled carefully to flip the knowledge factor without retraumatizing you in the process. Mixed-attribution years — multiple years, business income tangled between spouses, or community property rules in play — where the split itself is the fight. Active collection, where a levy is already reaching your contractor invoices and the relief request has to be coordinated with a levy release. And appeals or Tax Court, where the record you build determines what a judge ever sees. If any of those describe you, a free review before you file — not after a denial — is the cheap move: get your situation assessed here.

Terms on Form 8857 and your notices, decoded

- Understatement — extra tax the IRS added because the return itself was wrong (unreported income, bad deductions).

- Underpayment — the return was right, but the tax shown on it was never paid; only equitable relief covers this.

- Joint and several liability — each signer of a joint return owes 100% of the tax, and the IRS can collect all of it from either one.

- Nonrequesting spouse — the IRS's term for your spouse or ex; the law requires the IRS to notify them of your request and let them respond.

- CSED — the Collection Statute Expiration Date, 10 years from assessment (pausable), after which the IRS can't collect and can't grant balance relief.

- Streamlined determination — the fast-lane grant for requesters who are no longer married, face economic hardship, and lacked knowledge or reasonably expected the tax to be paid.

- Economic hardship — being unable to pay reasonable basic living expenses, measured against the IRS's published allowable-expense standards, not your actual lifestyle.

IRS equitable relief questions, answered

What is equitable relief from the IRS?

Equitable relief is the IRS's catch-all innocent spouse program under Section 6015(f): it removes your responsibility for a joint tax debt when holding you liable would be unfair, even though you miss the strict tests of the other two categories. It is the only category that covers tax that was reported correctly on the return but never paid. You request it on Form 8857.

How long do I have to request equitable relief?

For an unpaid balance, you can request equitable relief any time before the 10-year collection statute on that debt expires — there is no two-year deadline. To get back money you already paid or had offset, you must file within the refund window, generally three years from when the return was filed or two years from the payment. Older articles still cite a two-year rule for equitable relief; the IRS scrapped it in 2011.

Will the IRS contact my ex if I file Form 8857?

Yes. The law requires the IRS to notify your spouse or ex-spouse and give them a chance to participate, and there is no exception to that rule. The IRS will not share your current address, phone number, or employer information with them. If there is a history of abuse, say so on the form — abuse weighs heavily in your favor and shapes how the IRS handles the case.

What is the difference between innocent spouse relief and equitable relief?

Traditional innocent spouse relief under Section 6015(b) applies only to understatements — extra tax from errors on the return — and carries a strict two-year deadline after collection starts. Equitable relief under Section 6015(f) is broader: it covers both understatements and balances that were reported but never paid, and it can be requested any time the IRS can still collect. The trade-off is that equitable relief is discretionary, decided by weighing factors rather than meeting a bright-line test.

Can I get equitable relief if I knew about the tax debt?

Possibly. For an unpaid balance, the question is not whether you knew tax was owed but whether you reasonably believed your spouse would pay it when you signed the return. Documented promises to pay, a spouse who controlled all the finances, or abuse that made it unsafe to question them can all support relief even when you knew the balance existed. For understatement cases, knowledge weighs against you, but abuse can neutralize it.

Does the IRS stop collecting while my equitable relief request is pending?

Generally yes — new levies against you for the years in your request are paused while the IRS reviews it, which commonly takes six months or more. The IRS can still keep tax refunds you become owed and apply them to the joint debt during that time. Be aware the 10-year collection clock is suspended while the claim is pending, so if you lose, the debt's expiration date moves later.

My divorce decree says my ex pays the taxes — doesn't that settle it?

No. A divorce decree binds you and your ex, not the IRS — a joint return makes both signers fully liable no matter what the decree says. The decree still matters, though: a legal obligation placed on your ex to pay the tax is one of the seven factors that weighs toward granting you equitable relief. Bring a complete copy of the decree with your Form 8857.

What is a streamlined determination for equitable relief?

It is a fast lane in Revenue Procedure 2013-34 that grants relief without full factor-balancing when three things are all true: you are divorced, legally separated, widowed, or have lived apart from your spouse for at least 12 months; you would suffer economic hardship if forced to pay; and you did not know about the understatement — or, for an unpaid balance, reasonably expected your spouse to pay it. Miss any one of the three and the IRS moves to weighing all seven factors instead.

Can equitable relief refund money the IRS already took from me?

Yes — equitable relief can produce a refund of payments and offsets, which is one of its advantages over separation of liability relief, which never can. The catch is timing: refunds are limited by the refund statute, generally three years from when the return was filed or two years from the payment you want back. Refunds offset years ago may be gone for good even if relief is granted going forward.

What happens if my equitable relief request is denied?

You can appeal within the IRS, and after a final determination you can petition the U.S. Tax Court within 90 days. Tax Court review of equitable relief is genuine — the court takes a fresh look at the case rather than rubber-stamping the IRS. Many denials happen because the factor story was thin or poorly documented the first time, which is often fixable at the appeal stage.

Your next 24 hours

- Pull the paperwork that defines the debt. Find the tax year and balance on your most recent IRS notice — or log into your IRS online account — and note whether the debt comes from the return as filed (underpayment) or an IRS adjustment (understatement). That one distinction decides which relief program you're in.

- Gather your factor evidence. The joint return, your divorce or separation decree, proof of whose income created the tax, and any texts, emails, or records showing your ex controlled the money or promised to pay.

- Get a free case review. Send us what you have at the 2-minute form or call (888) 825-7779. An experienced tax professional will map your facts against the Section 6015(f) factors before another refund is offset or more interest piles onto a balance that isn't fairly yours.

Primary sources: the IRS's overview of innocent spouse relief, the official About Form 8857 page, and the independent Taxpayer Advocate Service, which can intervene when a pending claim isn't stopping harmful collection.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.