Marriage & Tax Debt

Prenup and IRS Debt: Does a Prenup Shield You? (2025)

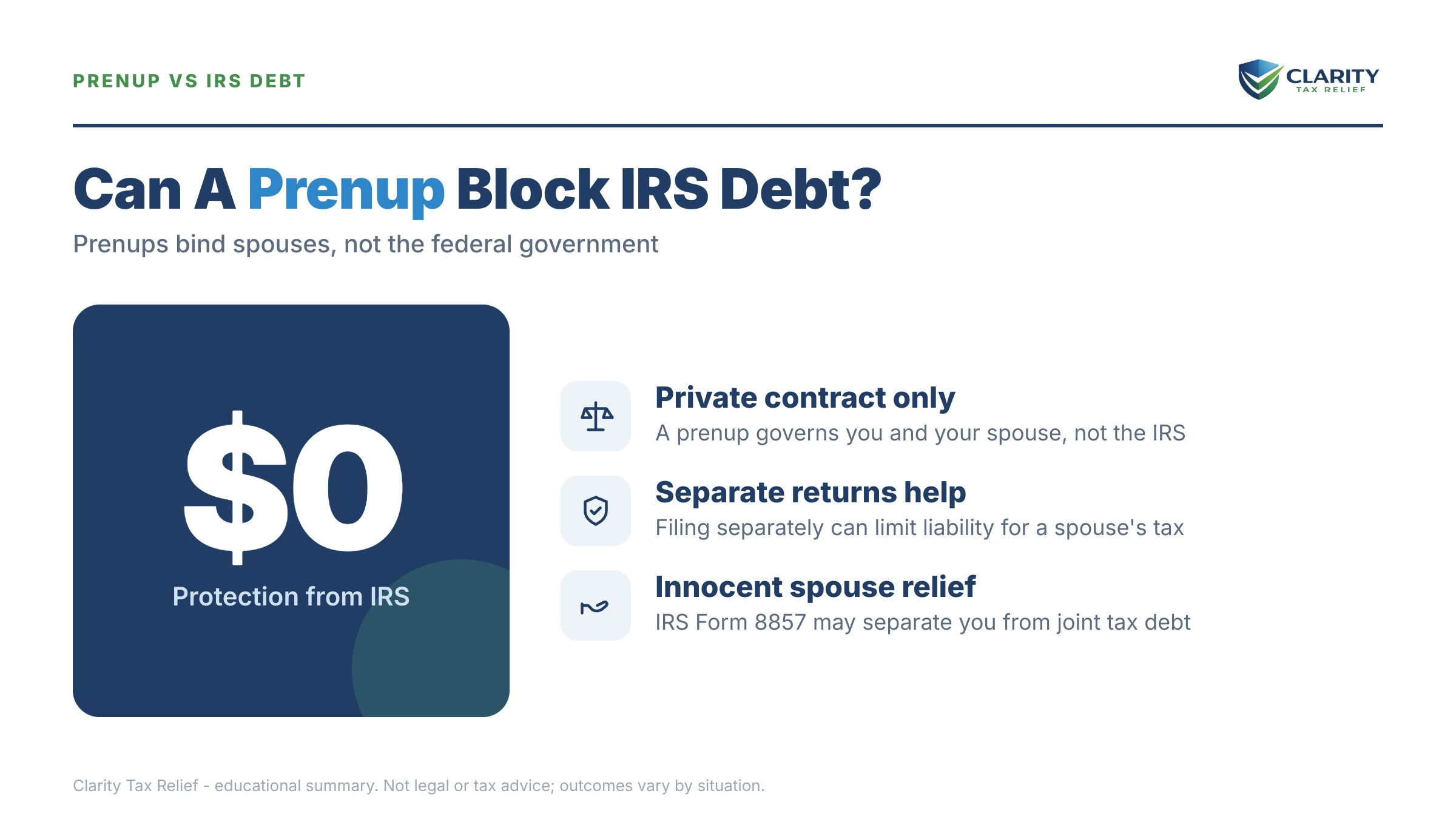

The short answer: a prenup does not shield you from IRS debt. A prenup (prenuptial agreement) is a private contract between you and your spouse — the IRS was never a party to it. It can decide who owes what between the two of you, but it can't stop the IRS from collecting a joint tax debt from either spouse.

Worried a spouse's tax debt could reach you?

An experienced tax professional can review your situation and tell you which protection actually fits — filing status, an injured spouse claim, or innocent spouse relief. The consultation is free, confidential, and no-pressure.

⏱ Time-sensitive: if your share of a joint refund was taken for a spouse's debt, you can file an injured spouse claim (Form 8379) — generally within 3 years of the return's due date or 2 years of the offset, whichever is later. File it as soon as you know the offset happened.

Why people think a prenup stops the IRS

It's an easy assumption. You signed a legal document saying "your debts are yours, my debts are mine." So if your spouse owes back taxes, that's their problem, right? The "prenup IRS debt" question comes up constantly — usually from someone about to marry a partner with a tax balance, or someone who just learned their spouse has years of unpaid returns.

Here's the hard truth: a prenup only binds the two people who signed it. The IRS didn't sign your prenup. A federal tax debt is owed to the United States Treasury, and your private agreement can't rewrite federal law that says who is liable for a tax. The prenup may matter between you and your spouse — for example, if you pay a debt that the prenup says was theirs, you may have a claim against them. But that's a family-law issue, not a shield against the IRS.

What actually decides if you're on the hook

Two things drive your liability for a spouse's tax debt, and a prenup is neither of them:

- Your filing status. When you sign a joint return, both spouses become "jointly and severally liable" for the entire balance — interest and penalties included. That means the IRS can collect 100% of the debt from either one of you. The prenup doesn't undo that. Filing separately is what keeps each spouse's liability legally separate.

- When the debt arose. A tax debt your spouse rang up before you married, on their own separate return, stays their personal debt. You aren't personally liable for it. But a shared joint refund is fair game for the IRS to grab.

So the real protection isn't a paragraph in a prenup — it's how you file and which IRS relief you claim. If you're weighing this before the wedding, our guide to marrying someone who owes the IRS walks through the practical steps.

What happens if you ignore the issue

The danger is assuming the prenup has you covered and doing nothing. The IRS collection system is automated and moves on its own timeline. Here's how a spouse's debt can reach you:

- Refund offset. File a joint return and the IRS can take the entire refund — including your share — to cover your spouse's back taxes through the Treasury Offset Program.

- Joint liability locks in. If the debt comes from a joint return, the IRS can pursue your wages, your bank account, and your assets for the full balance.

- Levies and liens. Left unresolved, a joint tax debt can lead to wage garnishment, a bank levy, and a federal tax lien — none of which a prenup prevents.

- Community property exposure. In community property states, income earned during the marriage is often shared, which can pull your half into the picture even on separate returns.

Pre-marriage debt: a worked example

Say your future spouse owes $18,000 from returns filed before you met. You marry and file jointly. Your withholding and credits generate a $6,000 refund. Because you filed jointly, the IRS applies the entire $6,000 to that old $18,000 debt — even though none of it was yours.

The fix isn't the prenup. It's Form 8379, Injured Spouse Allocation, which tells the IRS to carve out and return your share of the refund. Filed correctly, you could get back the portion tied to your income and credits. To understand which relief fits, compare injured spouse versus innocent spouse — they sound alike but solve very different problems.

What actually protects you (when a prenup can't)

- Filing separately. Married filing separately keeps each spouse responsible only for their own tax. You give up some tax benefits, but you don't inherit your spouse's balance. See filing separately when a spouse owes the IRS.

- Injured spouse claim (Form 8379). Protects your share of a joint refund when it's taken for your spouse's separate debt — back taxes, defaulted student loans, or child support.

- Innocent spouse relief (Form 8857). May erase your responsibility for a joint debt that came from your spouse's errors or unreported income — when you genuinely didn't know and it would be unfair to hold you liable.

- Knowing your state's rules. Community property states (like California, Texas, and Arizona) treat marital income differently. The IRS applies its own community property rules, so the right move depends on your facts.

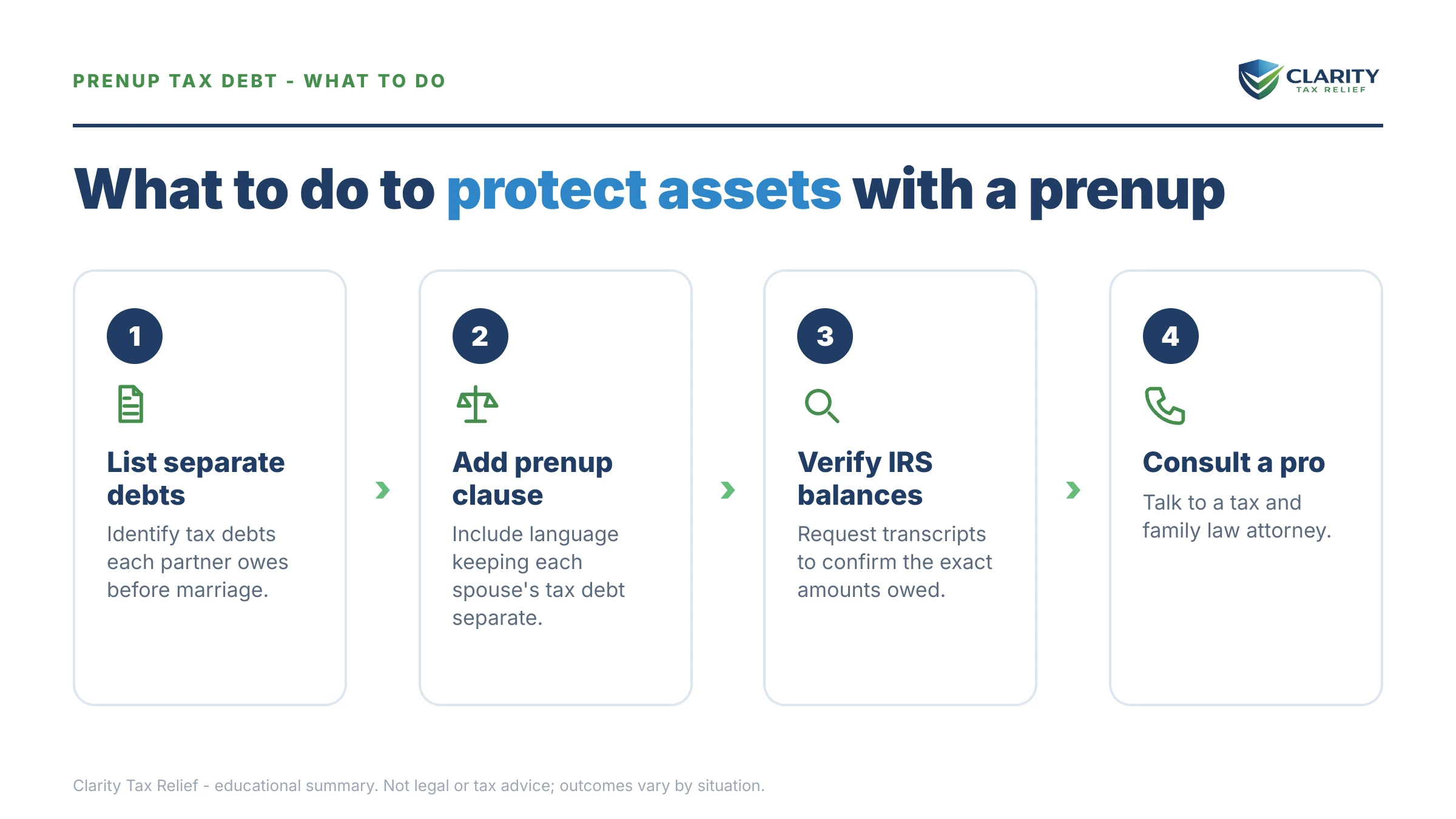

How to protect yourself, step by step

- Stop relying on the prenup for tax purposes. Treat it as a contract between you and your spouse, not a defense against the IRS.

- Find out exactly what's owed. Pull both spouses' IRS account transcripts so you know the years, the amounts, and whether the debt is separate or joint.

- Choose filing status with eyes open. Run the numbers on joint versus separate. Sometimes the tax savings of filing jointly are worth more than the risk; sometimes they aren't.

- If a joint refund was taken, file Form 8379, Injured Spouse Allocation to recover your share.

- If you're stuck with a joint debt you shouldn't owe, look at innocent spouse relief on Form 8857.

- Get a professional review if the balance is large, there are unfiled years, or you live in a community property state — the order you fix things in changes the outcome.

For background on how the IRS treats shared income, the IRS publishes Publication 555, Community Property, and the Taxpayer Advocate Service can help if a refund offset causes hardship.

Prenup and IRS debt: your questions, answered

Does a prenup protect me from my spouse's IRS debt?

Not against the IRS. A prenup is a private contract between you and your spouse, and the IRS was never a party to it. The agreement can decide who owes what between the two of you, but it cannot stop the IRS from collecting a joint tax debt from either spouse.

Am I responsible for tax debt my spouse had before we married?

Generally no — a separate, pre-marriage tax debt belongs to the spouse who incurred it, and the IRS can't hold you personally liable for it. The risk is your shared refund: if you file jointly, the IRS can take the whole refund to cover that old debt unless you file an injured spouse claim to protect your share.

Can I use a prenup instead of filing separately?

No. The choice that actually controls liability is your filing status, not your prenup. When you sign a joint return, both spouses become jointly and severally liable for the whole balance no matter what the prenup says. Filing separately is what keeps each spouse's tax liability legally separate.

Does a prenup help in community property states?

It can matter, but it's complicated. Community property states treat most income earned during marriage as shared, which can expose your half to a spouse's tax debt. A valid prenup may reclassify some property as separate, but the IRS applies its own rules, so don't assume the agreement settles it — get the facts reviewed.

If a prenup won't stop the IRS, what actually protects me?

Your real tools are filing status and specific IRS relief: filing separately, an injured spouse claim (Form 8379) to protect your share of a joint refund, and innocent spouse relief (Form 8857) when your spouse's errors created a debt you didn't know about. Which one fits depends on your facts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.