Tax Debt & Marriage

Marrying Someone Who Owes the IRS: What You're Liable For and How to Protect Yourself (2026)

The short answer: marrying someone who owes the IRS does not make you responsible for their pre-marriage tax debt — that liability stays theirs alone. But your joint tax refund, joint bank accounts, and jointly owned property can be exposed, and community property states change the math. Form 8379 and smart filing choices keep your money yours.

Somewhere between the venue deposit and the guest list, your partner told you about the IRS debt — and now you're wondering whether saying "I do" means signing up for their back taxes too. It doesn't. Marrying someone who owes the IRS transfers exactly zero dollars of their old debt onto you.

What marriage does change is how easily the IRS can touch money that's now partly yours: a joint refund, a joint account, a house you buy together. This guide maps exactly where the exposure is — and the handful of moves that close it off.

⏱ The clock that matters: your first joint tax return. File jointly without Form 8379 and the IRS can keep your entire joint refund — including the part generated by your own withholding — and apply it to your spouse's old balance. Meanwhile, interest and the late-payment penalty grow that balance every month it sits unresolved.

Does marrying someone who owes the IRS make you liable for their debt?

Marriage does not transfer tax debt: the IRS can collect a tax bill only from the person who signed the return that created it. If your partner's debt comes from returns they filed alone before you married, it is legally theirs — the IRS cannot garnish your wages, levy an account that holds only your money, or place a lien on property titled solely in your name for that debt.

There are exactly two ways you can become responsible for a spouse's tax problem, and both are avoidable:

- Signing a joint return for a year that owes. Every joint return you sign creates "joint and several" liability for that year — the IRS can collect 100% of that year's balance from either of you. This applies only to years you file together, never retroactively to their old debt.

- Living in a community property state. In Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin, income and property acquired during marriage generally belong to the community — and the IRS can often reach community property to collect one spouse's separate debt. State rules vary; our guide to community property tax relief covers how relief works in these nine states.

One more distinction worth locking in early: the debt someone brings into a marriage is a completely different problem from debt created during one. If you're researching the second kind, start with divorce and IRS debt: who pays — the rules there run through joint returns, not wedding dates.

Where their tax debt can still reach your money

The IRS can take a couple's entire joint refund for one spouse's old debt — that is the single most common way a non-owing spouse feels this problem. It happens automatically through the Treasury Offset Program the first spring you file together, and it repeats every year until the debt is resolved. If it already happened, our guide to a new spouse refund taken for old debt walks through getting your share back.

Here's the full exposure map, asset by asset:

| Asset | Separate-property states (41 states) | Community property states (9 states) |

|---|---|---|

| Your wages | Protected — can't be levied for their pre-marriage debt | Exposed — wages earned during marriage are generally community income |

| Bank account in your name only | Protected, if it holds only your funds | Partially exposed if funded with community income |

| Joint bank account | Exposed — a levy can reach funds in any account your spouse can draw on | Exposed |

| Joint tax refund | Exposed — offset in full unless Form 8379 is filed | Exposed — Form 8379 allocation follows community property rules |

| Home you buy together | A filed lien attaches to your spouse's interest only | A filed lien can attach to the community interest |

| Assets you owned before the wedding | Protected — keep them titled in your name | Generally protected if kept separate and not commingled |

The joint-account row deserves emphasis. When the IRS levies a bank account, it doesn't sort out whose deposits are whose before the freeze — it takes what's there and lets you argue afterward. Details on how that plays out are in can the IRS take my spouse's bank account. Until the debt is resolved, the simple protection is keeping your paycheck in an account with only your name on it.

And a prenup? It documents which property is separately yours — genuinely useful in community property states — but it cannot override federal collection law. The full picture is in does a prenup shield you from IRS debt.

What happens if the debt sits unresolved after the wedding

An unresolved IRS balance never idles — the collection system escalates it automatically, in a fixed sequence, whether or not a human ever reviews the file. In 2026, with IRS staffing down roughly 27% from 2025 cuts, the humans are harder to reach — but the automated notices, offsets, and levies never stopped. Here's the sequence a couple lives through when a pre-marriage balance is ignored:

- The balance compounds. Interest accrues, plus a 0.5%-per-month failure-to-pay penalty. An annual CP71 reminder shows the new, larger total each year.

- Every joint refund disappears. The Treasury Offset Program applies each year's joint refund to the debt — your withholding included — unless Form 8379 accompanies each return.

- CP504 arrives. The IRS states its intent to levy your spouse's state tax refund under IRC §6331(d). It is not the final notice, but enforcement is now in motion.

- A federal tax lien can be filed. A Notice of Federal Tax Lien attaches to your spouse's interest in everything they own — including their half of a home you buy together — and complicates any purchase, refinance, or sale.

- LT11 / Letter 1058 — the final notice. This starts a 30-day clock and Collection Due Process rights. After it runs, the IRS can levy bank accounts (a 21-day hold before funds leave, including joint accounts) and garnish your spouse's wages continuously until released.

- Passport certification. If accruals push the balance past $66,000 — the 2026 threshold — the IRS certifies the debt to the State Department, which can deny or revoke your spouse's passport. Hard news before an anniversary trip abroad; details in passport revoked for tax debt.

None of this is inevitable. Every stage in that sequence stops the moment the debt goes into an approved resolution — which is exactly what the next section covers.

Getting married — or just married — to someone with IRS debt?

Get the debt reviewed free before your first joint return puts your refund on the line. An experienced tax professional will map exactly what's exposed, what isn't, and the fastest way to get the balance resolved — no pressure, no judgment about your partner's past.

Resolving the debt: every option, and what each one means for you

A tax debt in an approved IRS resolution stops escalating — no new liens queued, no levies, no final notices. That protection is the best wedding gift the owing partner can give the marriage, and the right program depends on the balance and their finances. The general playbook lives in our guide to how to settle tax debt yourself; here is how each option looks from the non-owing spouse's side of the table:

| Option | Eligibility | Cost | What it means for the new spouse |

|---|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and penalties continue | Fast, clean; debt gone before it touches joint finances |

| Streamlined installment agreement | Balance ≤ $50,000 with direct debit; up to 72 months, set up online | Setup fee applies; interest and penalties continue | Stops escalation; their payment, not yours — keep it out of joint accounts |

| Offer in Compromise | Assets + future income genuinely can't cover the debt; ~1 in 5 offers accepted in FY2024 | $205 fee; 20% down on lump-sum offers (both waived with low-income certification) | Marriage can raise the offer math — shared household expenses shift the calculation |

| Currently Not Collectible | Paying anything would create genuine hardship, shown on financial disclosure | $0; debt remains and interest accrues | The IRS reviews household expenses — your income appears in the picture even though you owe nothing |

| Penalty relief (FTA / AEP) | Clean compliance the prior 3 years; the new Automatic Exemption from Penalty (AEP) begins applying some relief automatically in summer 2026 | $0 | Shrinks the balance itself — often the cheapest first move |

A worked example: the $48,300 fiancé

Say your fiancé owes $48,300 across three tax years from a self-employed stretch before you met. Because the balance is under $50,000, they can set up a streamlined installment agreement online with direct debit — no financial disclosure, no revenue officer. Spread over the maximum 72 months, that's $48,300 ÷ 72 ≈ $671 a month as a base figure; because interest and the 0.5% monthly failure-to-pay penalty keep accruing during the plan, the real cost of full payoff runs higher, and paying faster than the minimum saves real money.

Could they settle the same $48,300 for less? Only if the Offer in Compromise math works: the IRS calculates their "reasonable collection potential" from assets plus future income, and accepts an offer only when that number falls short of the debt. If your fiancé earns well, the math won't work and the payment plan wins — the IRS accepted roughly 1 in 5 offers in FY2024, and it runs the numbers, not the marketing. One timing point unique to your situation: after the wedding, shared household income and expenses enter the offer calculation, which can raise the minimum acceptable offer. If an OIC is genuinely on the table, have the numbers run before the ceremony, not after.

There's also a quieter fact working in the background: the IRS generally has 10 years from assessment to collect each year's balance. If part of your fiancé's debt was assessed six or seven years ago, some of it may expire before any levy ever lands — though the clock pauses during an OIC, bankruptcy, and certain appeals. Read how the 10-year collection statute (CSED) works, and estimate the expiration dates on their balances with our CSED Calculator.

Filing jointly vs. married filing separately when your spouse owes back taxes

Filing jointly with Form 8379 attached protects your share of the refund while keeping the tax savings of a joint return — for most couples with old, pre-marriage debt, that combination beats filing separately. But it's worth seeing the trade side by side before your first married April:

| Factor | Joint return + Form 8379 | Married filing separately |

|---|---|---|

| Your refund | Your allocated share is protected; expect extra processing time | Fully protected automatically — your return, your refund |

| Liability for the new year | Joint and several — you're both on the hook if the new year owes | Yours alone — their new balance can't attach to you |

| Credits and rates | Full access to joint rates, EITC, education credits, and more | Several credits disallowed or reduced; usually a higher combined tax |

| Effort | One extra form, filed every year until the debt is resolved | Two returns; in community property states, income-splitting rules add complexity |

The mechanics of the allocation form are in our Form 8379 injured spouse walkthrough, and the full case for separate filing is in married filing separately when your spouse owes the IRS. One caution that outranks everything else in this section: never sign a joint return for a year with a balance due you haven't planned for — that signature, not the wedding, is what makes their tax problem legally yours for that year. Injured spouse relief (your refund, their old debt) is also a different remedy from innocent spouse relief (a joint year you signed with errors you didn't know about); make sure you're requesting the right one.

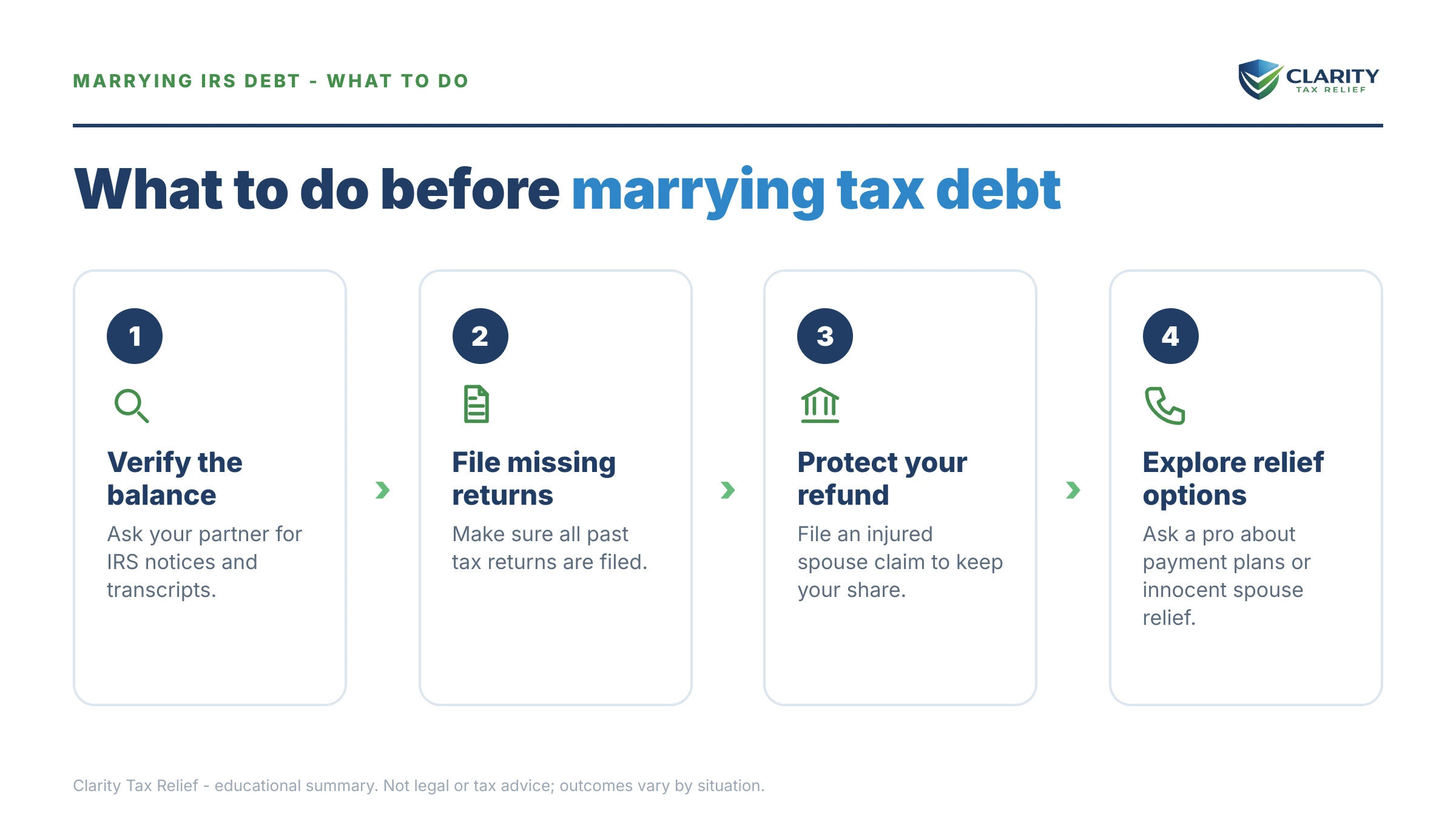

How to protect yourself before and after the wedding, step by step

- Pull the full IRS picture. Have your partner log into their IRS online account and pull account transcripts for every year with a balance. You need the total owed, which years it covers, whether every return is filed, and the assessment dates that start each 10-year collection clock.

- Keep your money separate where it counts. Keep your paycheck in an account in your name only until the debt is resolved — funds in a joint account can be levied for either owner's tax debt. Hold off on retitling savings, vehicles, or a home into joint names.

- Choose your first filing status deliberately. Run your first married return both ways. If filing jointly saves more than the refund at risk, file jointly and attach Form 8379 to protect your share; if not, file separately for that year and revisit annually.

- Get the debt into a resolution. A balance in an approved installment agreement, accepted offer, or hardship status stops the escalation toward liens and levies. For a $48,300 balance, a streamlined direct-debit installment agreement is usually the fastest fix.

- Paper the property decisions. In a community property state, talk to an experienced tax professional about a prenup and how income and accounts are titled — documentation is what keeps your separate property characterized as separate.

When you can handle this yourselves — and when to get help

Plenty of couples in this situation never need professional help. If your partner's balance is accurate, all their returns are filed, and the debt is under $50,000, they can set up a payment plan directly at the IRS payment plans page in an evening, and you can attach Form 8379 to your joint return yourself. If they can pay the whole thing within 180 days, the short-term plan costs nothing to set up and ends the story.

Experienced help changes outcomes in specific situations: your partner has unfiled years (no resolution program is available until returns are in, and the filing order affects the total); a lien is already filed or a final levy notice has arrived; the debt includes business or payroll tax; you live in a community property state and real assets are at stake; or an Offer in Compromise looks plausible and the pre-versus-post-wedding math matters. In those cases, the sequencing decisions made in the first month typically determine what the couple ultimately pays.

Terms you'll run into, decoded

- Joint and several liability — when you sign a joint return, the IRS can collect 100% of that year's balance from either spouse, regardless of who earned the income.

- Injured spouse — the spouse whose refund share was taken for the other's separate debt; Form 8379 gets it back.

- Innocent spouse — a different remedy: relief from a joint year you signed that understated tax because of your spouse's errors.

- Refund offset — the Treasury Offset Program's automatic application of a refund to an outstanding federal debt before you ever see it.

- Notice of Federal Tax Lien — a public filing that attaches the IRS's claim to the debtor's property interests, including their share of jointly owned assets.

- CSED — Collection Statute Expiration Date: the end of the IRS's 10-year window to collect each assessed balance, pausable by offers, bankruptcy, and appeals.

- Community property — the marital-property system in nine states where most income and assets acquired during marriage belong to both spouses — and can be reachable for one spouse's debt.

Marrying someone with IRS debt: your questions answered

Am I responsible for my spouse's tax debt if we get married?

No — marriage alone never makes you liable for tax debt your spouse ran up before the wedding. The IRS can only collect a debt from the person (or people) who signed the return that created it. Your own liability begins only if you sign a joint return for a year with a balance due, or if you live in a community property state, where the IRS can generally reach income and property the two of you acquire during the marriage.

Will the IRS take my tax refund if my spouse owes back taxes?

It will take a joint refund, yes — the Treasury Offset Program applies the entire refund on a joint return to either spouse's federal tax debt. You can recover your share by filing Form 8379, Injured Spouse Allocation, with the return or after the offset happens. Filing it with the return adds processing time but protects the portion of the refund tied to your own income and withholding.

Can the IRS garnish my wages for my spouse's tax debt?

In most states, no — your wages cannot be garnished for a debt that is solely your spouse's. The exception is the nine community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), where the IRS can generally reach community income and property to collect one spouse's separate debt. If you live in one of these states, get advice on how income and accounts are titled before you marry.

Should we file jointly or separately if my spouse owes the IRS?

For old, pre-marriage debt, filing jointly with Form 8379 usually wins — you keep joint-filing rates and credits while protecting your share of the refund. Married filing separately protects your refund automatically but often costs more: it can disqualify credits like the Earned Income Tax Credit and education credits and typically produces a higher combined tax. Run the return both ways before deciding, and never sign a joint return for a year with a balance due without understanding you become fully liable for that year.

Does a prenup protect me from my spouse's IRS debt?

A prenup can't stop the IRS from collecting what your spouse legally owes — federal collection rights aren't bound by private contracts. What it can do is document which assets and income are yours separately, which matters most in community property states and if the marriage ever ends. Think of it as evidence that keeps your property characterized as yours, not as a shield around your spouse's debt.

Can we buy a house together if my spouse owes the IRS?

You can, but plan around the lien risk. If the IRS files a Notice of Federal Tax Lien, it attaches to your spouse's interest in any property they own — including a home you buy together — and most mortgage lenders will want the debt resolved or in a payment plan before approving the loan. Getting the balance into an installment agreement before you house-hunt is usually the cleanest path.

Does my spouse's tax debt affect my credit score?

No — tax debt doesn't appear on either spouse's credit report, and the major bureaus stopped reporting tax liens entirely in 2018. The practical effects show up elsewhere: joint refund offsets, lien attachment to jointly owned property, and extra mortgage underwriting questions when you apply for credit together. Your individual credit score stays untouched by a debt that is solely theirs.

Does my spouse's IRS debt expire after 10 years?

Generally yes — the IRS has 10 years from the date each balance was assessed to collect it, a deadline called the CSED. But the clock pauses during bankruptcy, a pending Offer in Compromise, and certain appeals, so real-world expiration often runs longer than 10 calendar years. Before building a plan around waiting it out, confirm the actual CSED dates on your spouse's account transcripts.

Your next 24 hours

- Find the real number. Have your partner log into their IRS online account or pull their most recent notice — you need the exact balance and which tax years it covers, not a ballpark confession.

- Gather three things: their most recent IRS notice, both of your income figures, and confirmation that every one of their past returns is actually filed.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will map what's exposed and the fastest resolution before your first joint return, while interest and penalties are still growing the balance every month.

If the balance is verified and the plan is simple, you can also handle payment directly through IRS.gov/payments. If the IRS's own process stalls or an offset creates hardship, the independent Taxpayer Advocate Service can intervene at no cost.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.