Spouse & Family Tax Debt

Married Filing Separately When Your Spouse Owes the IRS: 2026 Guide

The short answer: filing married filing separately when your spouse owes the IRS keeps your refund and income legally walled off from their debt — you are not liable for a spouse's separate tax bill. But MFS often costs more in tax, so compare it against filing jointly with Form 8379, Injured Spouse Allocation, first.

You're sitting down to file, and the person you married owes the IRS money from before you ever shared a return. If you searched "married filing separately spouse owes IRS," you're really asking two questions: can their debt reach me, and does filing separately actually stop it? The answers are mostly no and mostly yes — with a handful of exceptions that matter enormously if you share a bank account, a house title, or a community property state.

Here's the map: what you are and aren't liable for, the real cost of filing separately, the injured spouse alternative that often beats it, and — because a growing balance eventually produces a lien — what your spouse's debt means for the refinance you're planning.

⏱ The running clock: there's no notice deadline on this decision, but there is a meter. Your spouse's failure-to-pay penalty accrues at 0.5% per month, interest compounds daily on top, and once a balance passes $66,000 (the 2026 threshold), the IRS can certify it for passport denial. Every return you file wrong risks that year's refund.

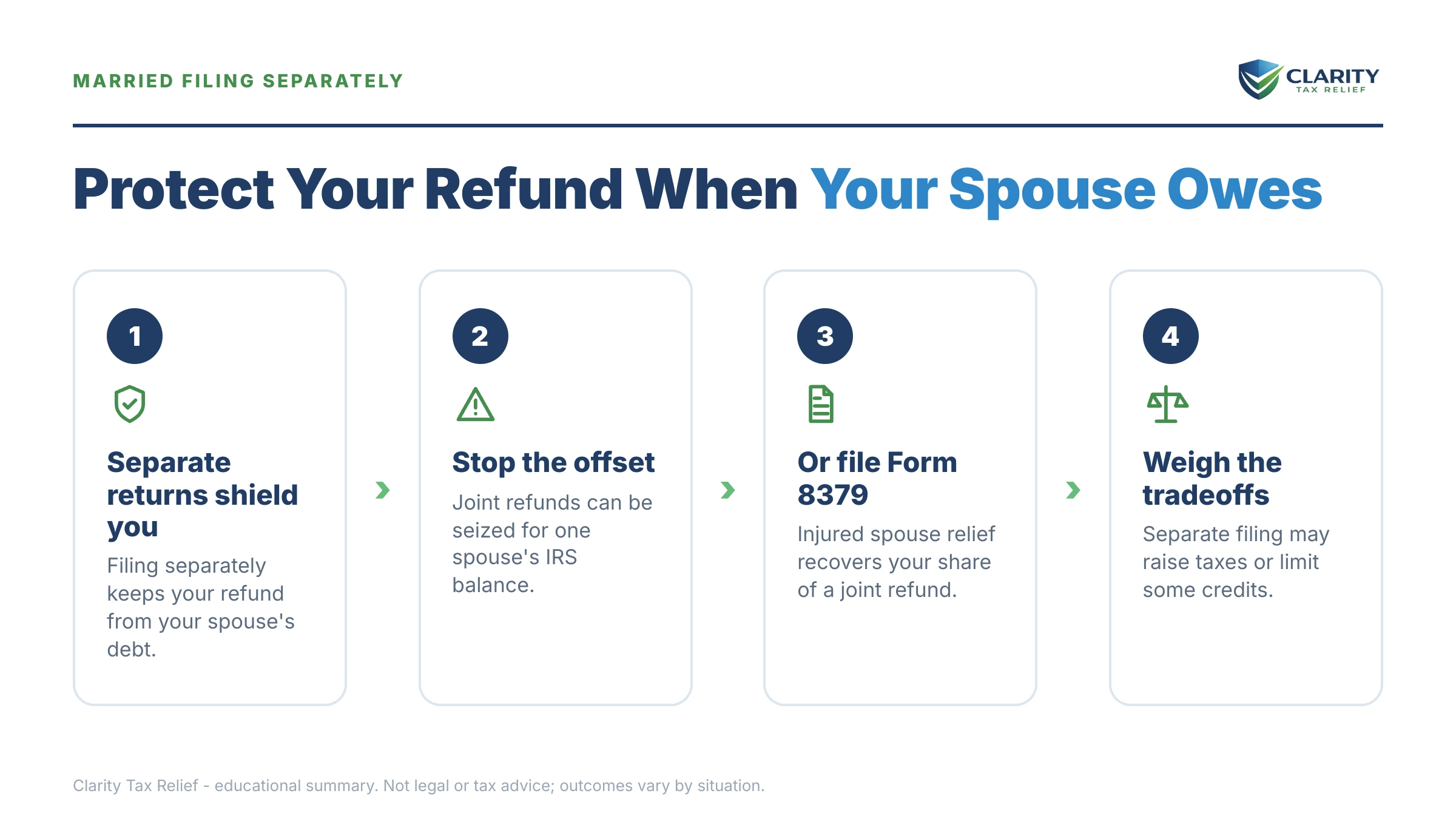

Why married filing separately protects you when your spouse owes the IRS

You are never liable for tax debt your spouse created on a separate return — including every return they filed before you married. IRS debt belongs to the person (or people) whose signature is on the return that generated it. Marriage alone transfers nothing.

The trap is the joint return. Signing a Form 1040 jointly creates joint and several liability: the IRS can collect 100% of that year's tax from either of you, forever, regardless of who earned the income or what a divorce decree later says. Filing separately means each spouse signs only for their own income — so a new MFS return can't add you to the old debt, and your separate refund can't be swept into it.

Here's how liability actually breaks down by scenario:

| Where the debt comes from | Are you liable? | What protects you |

|---|---|---|

| Their returns filed before your marriage | No | MFS filing, or joint filing with Form 8379 |

| Their MFS returns during the marriage | No | Same — keep filing separately or attach Form 8379 |

| A joint return you both signed | Yes — jointly and severally | Innocent spouse relief (Form 8857), if you qualify |

| Their separate debt in a community property state | Not liable, but community assets may be reachable | Section 66 relief; careful income and account separation |

Two boundary notes. If the debt comes from a joint year where your spouse understated income without your knowledge, that's a different problem with a different fix — see innocent spouse relief: how to qualify and, if you're just discovering the numbers, spouse hid income from me. And if you're reading this before the wedding, marrying someone who owes the IRS covers the protective setup from day one.

What happens if your spouse's IRS debt goes unresolved

Filing separately protects your return, but it does nothing to stop collection against your spouse — and collection against your spouse can still bruise a shared life. The IRS's automated system escalates in a fixed sequence:

- Balance-due notices (CP14, then CP501/CP503 reminders) — bills, with penalties and interest compounding each cycle.

- CP504 — Notice of Intent to Levy — the IRS can seize your spouse's state tax refund, and a Notice of Federal Tax Lien becomes a live possibility.

- Lien filing — a recorded federal tax lien attaches to everything your spouse owns, including their half of a jointly titled home. This is the step that stalls refinances.

- LT11 / Letter 1058 — Final Notice of Intent to Levy — after a 30-day window (with Collection Due Process appeal rights), the IRS can levy your spouse's wages and bank accounts, including joint accounts, since it can reach any funds your spouse has the right to withdraw. See can the IRS take my spouse's bank account for exactly how far that reach goes.

- Passport certification — once the balance exceeds $66,000 in 2026, the IRS can certify the debt to the State Department, which can deny or revoke your spouse's passport. Details in passport revoked for tax debt.

- Annual refund offsets — every future joint refund gets intercepted until the debt is resolved. MFS or Form 8379 protects your share; nothing protects theirs.

None of this requires a human at the IRS to review the file. In 2026, with the workforce cut roughly 27%, the people are harder to reach — but the notices, liens, and levies are generated by automation that never stopped. You can estimate how fast a balance like this grows with our Penalty & Interest Calculator.

Married to someone with an IRS balance — and worried it will touch your refund, your accounts, or your refinance?

An experienced tax professional will review both spouses' IRS records, tell you exactly what's exposed and what isn't, and map the cheapest way through — free and confidential. Penalties and interest are accruing on the balance either way; the review costs nothing.

Your filing options: separately, jointly with Form 8379, or bare joint

Married filing separately is not the only way to keep your refund — and it's frequently not the cheapest. Filing jointly with Form 8379, Injured Spouse Allocation, keeps the lower joint tax rates and credits while asking the IRS to carve out and release your share of the refund instead of applying it to your spouse's debt.

What MFS actually costs you: as a separate filer you generally lose the earned income credit, both education credits, and the student loan interest deduction; Roth IRA contribution limits phase out almost immediately; the capital-loss deduction is cut to $1,500; and if one spouse itemizes, the other cannot take the standard deduction. For many couples that adds up to more than the refund they were trying to protect.

| Filing approach | Your refund | Tax cost | Best when |

|---|---|---|---|

| Married filing separately | Fully protected — your refund is yours, immediately | Usually highest: credits lost, worse brackets for many couples | You want zero entanglement, doubt your spouse's numbers, or the joint numbers barely beat MFS anyway |

| Joint return + Form 8379 | Your allocated share is released; expect months of extra processing | Lowest for most couples — full joint rates and credits | The joint tax savings exceed the hassle and delay, and the debt is clearly your spouse's alone |

| Joint return, no Form 8379 | Entire refund offsets to the debt automatically | Lowest tax — but you donate your refund | Almost never — only if you've deliberately set withholding so there's no refund to take |

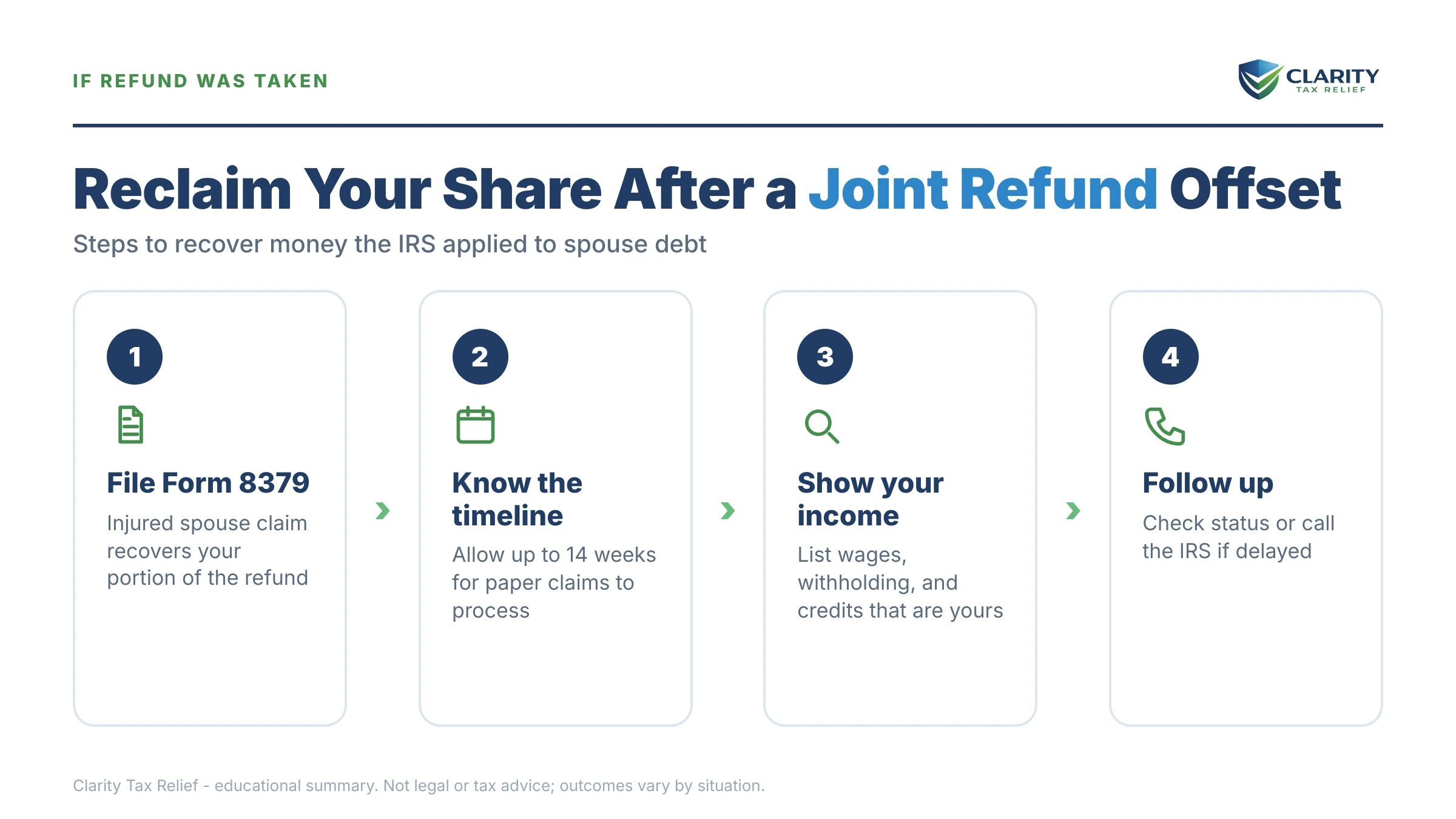

One distinction worth 30 seconds: injured spouse (Form 8379) protects your share of a refund from your spouse's debt; innocent spouse (Form 8857) removes your liability for a joint year's debt. People mix these up constantly — injured spouse vs. innocent spouse sorts them out.

And note what Form 8379 does not do: it doesn't shrink the debt, stop the lien, or end the annual interception. It's a shield for one refund at a time. The debt itself still needs a plan.

Resolving the debt itself: what your spouse's balance qualifies for

The permanent fix is getting the balance into an IRS resolution — and the options depend heavily on the amount. Because the debt is your spouse's alone, they apply in their name only; your income generally stays out of the IRS's collection math for a separate liability (community property states aside). The full DIY playbook lives in our guide to how to settle tax debt yourself; here's how the options break by balance:

| Balance owed | Realistic options | What it takes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement; 180-day short-term plan ($0 setup) | Filed returns and staying current — approval is essentially automatic |

| $10,000–$25,000 | Streamlined installment agreement, up to 72 months | No financial disclosure; set up online in minutes |

| $25,000–$50,000 | Streamlined agreement with direct debit; online setup still available | Direct debit generally required in this band |

| Over $50,000 (your spouse's tier) | Full-financials installment agreement, pay-down to $50,000, Currently Not Collectible, or Offer in Compromise if the math supports it | Form 433 financial disclosure — and above $66,000, passport certification is in play until a plan is active |

Interest and penalties keep accruing on any installment agreement, so the fastest affordable payoff is usually the cheapest — our comparison of the best ways to pay the IRS runs the real cost of each method. An Offer in Compromise is real but means-tested and hard: the IRS accepted roughly 1 in 5 offers in FY2024, and it only works when your spouse's assets and income genuinely can't cover the debt.

A worked example: your spouse owes $68,500 and you're planning to refinance

Say your spouse owes the IRS $68,500 from self-employment years before you married, you own your home together, and you want to refinance this year. This is hypothetical, but the math is the math:

- The refund decision. Filed jointly with no protection, suppose your refund would be $5,200 — the Treasury applies all of it to the $68,500 the moment it's approved. With Form 8379, the IRS allocates the refund by each spouse's income and withholding; if your withholding generated $4,100 of it, that's roughly the share released to you. If MFS would cost you $1,900 more in tax than joint, the 8379 route keeps both the $1,900 and your refund share — at the price of a few months' wait.

- The accrual meter. At 0.5% per month, the failure-to-pay penalty alone adds about $342 a month to a $68,500 balance — over $4,100 a year before interest. Doing nothing is the most expensive option on the table.

- The passport problem. $68,500 is above the $66,000 certification threshold for 2026, so the IRS can flag your spouse's passport. A debt being paid on time under an installment agreement is generally excluded from certification — one more reason to get a plan active.

- The refinance problem. Above $50,000, no online streamlined plan exists. One path: pay the balance down by $18,600 to $49,900, then set up a 72-month streamlined agreement online — roughly $693 a month before accruals ($49,900 ÷ 72). The IRS typically doesn't file a lien on streamlined agreements, which matters enormously here: once a Notice of Federal Tax Lien hits the county records against your spouse, it attaches to their interest in your home, surfaces in the title search, and most lenders won't close until it's paid, in a qualifying plan, or subordinated via Form 14134. See can I refinance with an IRS lien and tax lien subordination for the escape hatches — but the cheapest escape is resolving the debt before the lien exists.

The sequence for this couple: file with protection now, get the debt into an agreement before a lien filing, then refinance. Reversing that order can cost months and thousands in a worse rate lock.

Community property states change the math

In the nine community property states, filing separately does not fully wall off your income from your spouse's IRS debt. Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin treat most income earned during the marriage as owned half-and-half — so an MFS return there generally requires reporting half of the combined community income, and the IRS can often collect one spouse's separate debt from community assets, potentially including part of your paycheck.

Section 66 relief can decouple your income from your spouse's in some community property situations, but the rules are technical and state-law dependent. If you live in one of these nine states, read community property tax relief before choosing a filing status — and treat this as the scenario where a professional review pays for itself fastest.

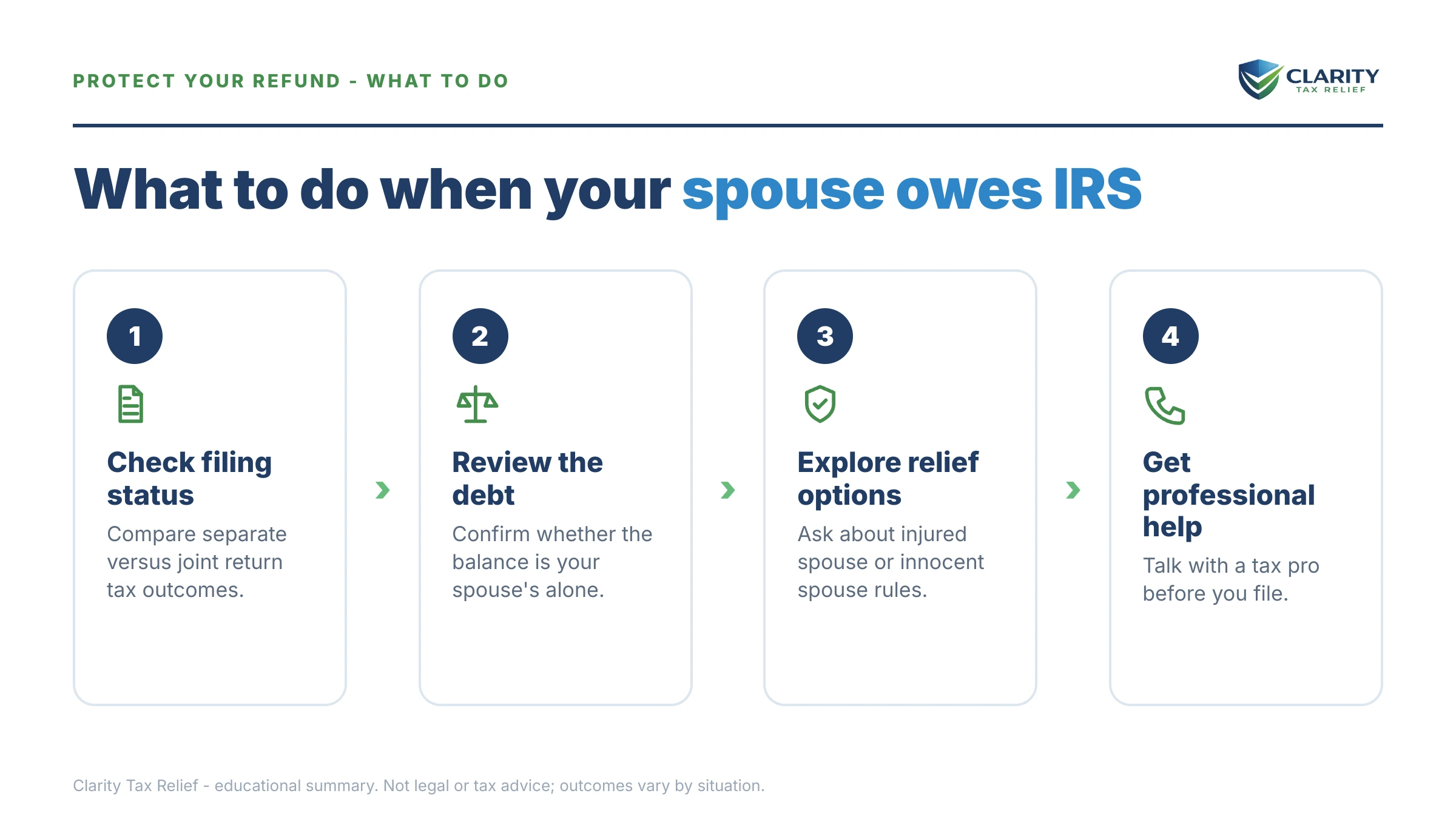

How to respond, step by step

- Confirm whose debt it is — pull your spouse's IRS online account or transcripts and note the balance, the tax years, and whether any year was filed jointly with you.

- Run your return both ways — prepare it as married filing separately and as married filing jointly with Form 8379, then compare total tax and how much refund each version actually leaves in your pocket.

- File the protective version — attach Form 8379 to a joint return, or file separately — but never file a bare joint return while your spouse has an unresolved balance.

- Separate your day-to-day finances — move your pay into an individual account and trim your withholding so you are not building a large refund the IRS can intercept.

- Put the debt itself on a resolution track — get your spouse into a payment plan, hardship status, or an Offer in Compromise review before a lien filing complicates your refinance or sale plans.

When you can handle this yourself

Much of this is genuinely DIY territory. If the debt is clearly your spouse's alone, you don't live in a community property state, and the balance is under $50,000, you can file Form 8379 with your return (or file MFS), have your spouse set up a streamlined installment agreement online, and be done — no professional needed.

Experienced help changes the outcome in four situations: a balance over $50,000 where Form 433 financials determine what the IRS demands (and where presenting them wrong costs real money every month); a lien already filed or a refinance on a tight timeline, where subordination paperwork has to be sequenced with the lender; a community property state, where filing status, income splitting, and Section 66 interact; and any joint-year debt where innocent spouse relief is on the table, because those claims are argued, not just filed. If you're weighing it, a free review that tells you "you don't need us" is a perfectly good outcome.

Terms in this situation, decoded

- Joint and several liability — when you sign a joint return, the IRS can collect that year's entire tax from either spouse, regardless of who earned what.

- Injured spouse — a spouse whose share of a joint refund was (or would be) taken for the other spouse's debt; Form 8379 gets that share back.

- Innocent spouse — a spouse seeking removal of liability for a joint year's understated tax caused by the other spouse; requested on Form 8857.

- Notice of Federal Tax Lien (NFTL) — the public recording that attaches the IRS's claim to everything the debtor owns, including their share of jointly titled property.

- Treasury Offset Program — the automated system that intercepts federal payments, including tax refunds, to cover past-due debts.

- Community property — state-law rules in nine states treating most income earned during marriage as owned equally by both spouses, which can expose your income to your spouse's separate debt.

Spouse-owes-IRS questions, answered

Am I responsible for my spouse's IRS debt if we file separately?

No. Tax debt from your spouse's separate returns — filed before your marriage or as married filing separately — is legally theirs alone. You become responsible only when you sign a joint return, which creates joint and several liability for that year's tax. The exception is community property states, where the IRS may reach community assets, including part of your income, even for a spouse's separate debt.

Will the IRS take my refund if my spouse owes back taxes and we file jointly?

Yes — a joint refund is automatically applied to either spouse's past-due federal tax debt unless you file Form 8379, Injured Spouse Allocation. Form 8379 asks the IRS to calculate your share of the refund based on your income, withholding, and payments, and release that portion to you. You can attach it to the return or file it on its own after an offset; expect the allocation to add a few months of processing time.

Is it better to file jointly with injured spouse or married filing separately?

Run the return both ways before deciding. Filing jointly with Form 8379 usually produces lower total tax, because MFS disqualifies you from the earned income credit, education credits, and the student loan interest deduction. MFS wins when you want zero entanglement — no waiting on an allocation, no shared paperwork — when you doubt the accuracy of your spouse's numbers, or when community property rules would expose your income anyway.

Can the IRS garnish my wages or bank account for my spouse's tax debt?

Not for a debt that is only your spouse's — with two caveats. Money in a joint bank account can be levied, because the IRS can reach funds your spouse has the right to withdraw. And in community property states, the IRS may claim a share of your wages as community property. Keeping separate accounts and understanding your state's rules closes most of the gap.

Does my spouse's tax debt affect a mortgage refinance?

It can. If the IRS files a Notice of Federal Tax Lien and your spouse is on the title, the lien attaches to their interest in the home and appears in the title search. Most lenders then require the debt to be paid, placed in a qualifying payment plan, or subordinated with Form 14134 before closing. Debt with no lien filed generally will not surface in a title search, but applications may still ask about federal payment plans.

What if we live in a community property state?

The rules shift against you. In Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin, filing separately generally requires reporting half of the combined community income, and the IRS can often collect one spouse's debt from community property — potentially including part of your paycheck. Section 66 relief can decouple your income in some cases; this is the scenario where professional review earns its cost fastest.

Can the IRS put a lien on our house if only my spouse owes?

Yes — on your spouse's interest in it. A federal tax lien attaches to all property and property rights of the person who owes, including their share of a jointly owned home. The IRS rarely forces the sale of a jointly owned primary residence, but the lien clouds the title and complicates any sale or refinance until it is paid, released, or subordinated.

Does my spouse's IRS debt show up on my credit report?

No. The credit bureaus removed tax liens from credit reports in 2018, and IRS balances themselves were never reported to the bureaus. But invisibility on a credit report is not invisibility to a lender: a filed lien is a public record that surfaces in title searches, and mortgage applications ask directly about delinquent federal debt and payment plans. Answer honestly — the fix is resolving the debt, not hiding it.

Your next 24 hours

- Find the real number. Have your spouse log into their IRS online account and write down the exact balance, the tax years behind it, and whether any lien has been filed. Everything else depends on those three facts.

- Gather the paperwork. Last year's returns for both of you, both sets of W-2s/1099s, any IRS letters your spouse has received, and — if you're refinancing — your loan officer's timeline.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will run your return both ways, check the community property angle, and map how to get the debt resolved before a lien complicates the refinance — while the balance is still growing at 0.5% a month plus interest.

Primary sources: the IRS's page on Form 8379, Injured Spouse Allocation, its overview of payment plans and installment agreements, and the Taxpayer Advocate Service for cases stuck in processing.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.