IRS Forms

Form 8857 Instructions: How to Request Innocent Spouse Relief (2026)

The short answer: Form 8857, Request for Innocent Spouse Relief, asks the IRS to remove your responsibility for tax your spouse or ex-spouse caused on a joint return. You generally have 2 years from the IRS's first collection activity against you to file it, one form can cover multiple years, and review typically takes up to six months.

You signed the return because your spouse handed it to you finished, and now a bill for income you never saw has your name on it. That's the exact problem Congress built this form to fix — and these Form 8857 instructions walk through who qualifies, what to attach, and the three deadlines that decide most cases.

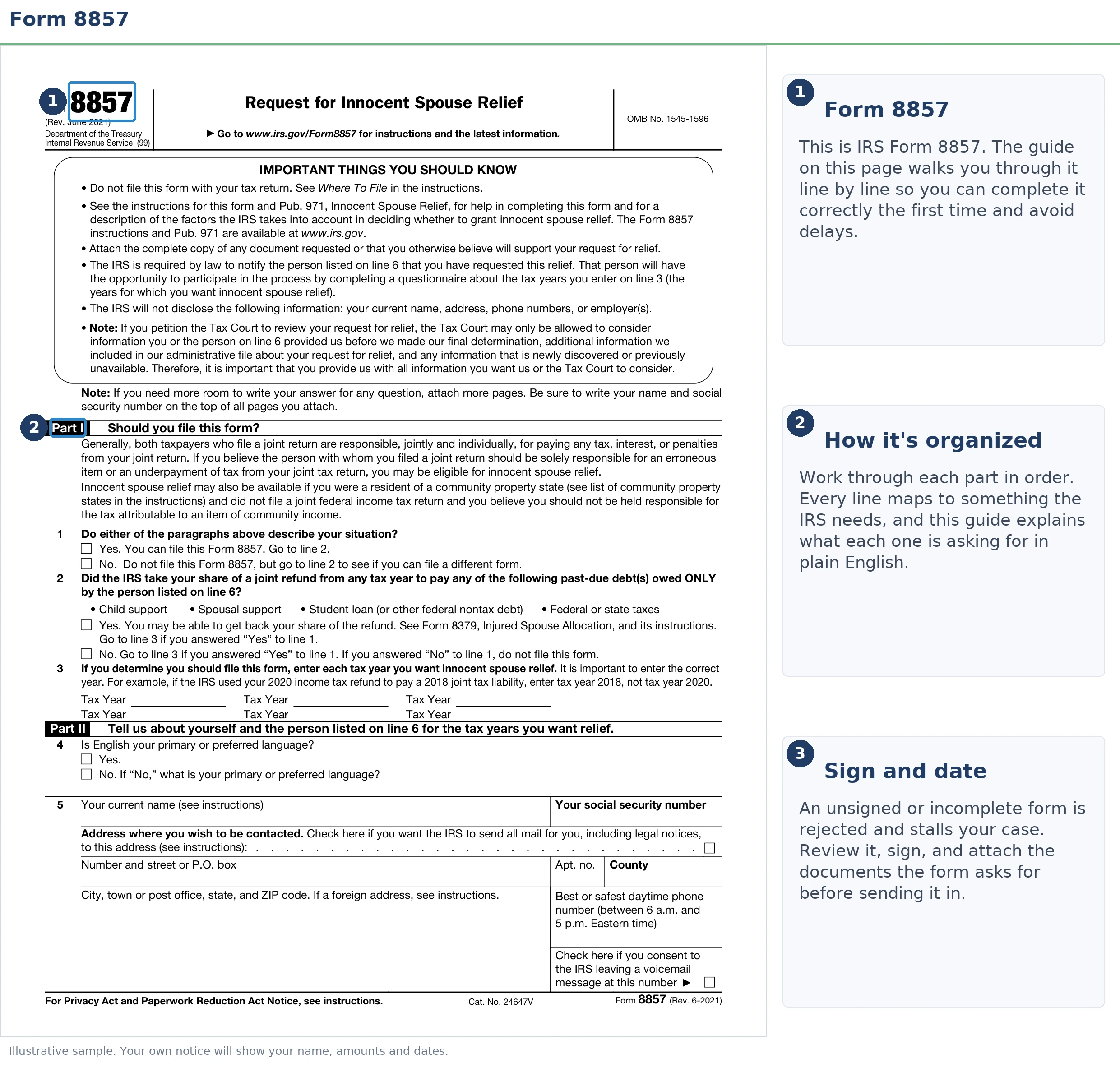

The form itself runs about seven pages of personal questions, not tax math. The image below shows exactly what Form 8857 looks like and where to focus — a handful of questions about what you knew and how the money was handled carry most of the weight.

⏱ Your deadline: you have 2 years from the date of the IRS's first collection activity against you — a refund offset, a levy notice — to request innocent spouse relief or separation of liability on Form 8857. Equitable relief has no 2-year cutoff: it stays available as long as the IRS can still collect, or within the refund window if you're asking for money back.

Why you'd file Form 8857

Form 8857 exists because a joint tax return creates joint and several liability — each spouse legally owes 100% of the bill, no matter whose income or mistake caused it. If your spouse left freelance income off the return, inflated deductions, or simply never paid what the return showed due, the IRS can collect the entire amount from you alone. Form 8857 is the only application that asks the IRS to break that link.

You can file as soon as you become aware of a joint liability you believe only your spouse should pay — you don't have to wait for collection letters to start. Awareness usually arrives as an audit result, a letter from the IRS like a CP2000, or a seized refund after a divorce.

Two things Form 8857 is not for. It can't erase tax on your own income — the item has to be attributable to the other spouse. And it's not the form for a refund the IRS grabbed to pay your spouse's separate debt (their child support, their pre-marriage back taxes); that's injured spouse Form 8379, a completely different request with a different unit and timeline.

What happens if you never file it

If you never file Form 8857, the IRS collects the joint balance from whichever spouse is easier to reach — usually the one with steady wages or a refund to intercept. The collection machine doesn't know or care who caused the debt:

- The balance posts to the joint account — both names, both fully liable, interest and the monthly failure-to-pay penalty running against both of you.

- Your refunds start disappearing — every year's refund, including refunds on a new joint return with a new spouse, gets applied to the old balance.

- The notice sequence escalates against you personally — reminder bills give way to a CP504 (the IRS can take your state refund), then an LT11 final notice that opens a 30-day window before wage and bank levies.

- Liens and levies land on the reachable spouse — a federal tax lien attaches to your property, and a wage levy runs continuously until released, even though the income behind the debt was never yours.

- Your best relief options expire — once 2 years pass from that first collection action, innocent spouse relief and separation of liability are off the table. Only equitable relief remains, and it's the hardest of the three to win.

One more thing that surprises almost everyone: a divorce decree assigning the tax debt to your ex does not bind the IRS. The decree is a contract between the two of you; the IRS's claim against you survives it, and only relief granted through Form 8857 actually removes your name from the debt.

Staring at a joint tax bill that isn't yours?

The 2-year window on innocent spouse and separation-of-liability relief started the day the IRS first moved to collect from you. Get your Form 8857 case reviewed free before that window closes — an experienced tax professional will tell you which relief type fits and what evidence you'll need.

The three types of relief Form 8857 requests

Form 8857 is one form, but it applies for up to four different kinds of relief, each with its own legal test — and you don't have to choose. Check the boxes, answer the questions honestly, and the IRS is required to consider every type you could qualify for.

| Relief type | Core requirement | What it covers | Filing deadline |

|---|---|---|---|

| Innocent spouse relief — §6015(b) | You didn't know, and had no reason to know, about the understatement your spouse caused | Extra tax added later (audit, CP2000) on a joint return | 2 years from the IRS's first collection activity against you |

| Separation of liability — §6015(c) | You're divorced, legally separated, widowed, or lived apart the past 12 months | Splits an understatement between spouses based on whose items caused it | 2 years from the IRS's first collection activity against you |

| Equitable relief — §6015(f) | Holding you liable would be unfair given all facts: hardship, abuse, knowledge, who benefited | Understated tax or tax reported correctly but never paid | As long as the IRS can still collect — or the refund window if claiming money back |

| Community property relief — §66(c) | You filed separately in a community property state and were taxed on your spouse's community income | Tax attributed to you under community property rules on a separate return | Follows the windows of the matching relief type above |

The pattern to notice: equitable relief is the only type that covers tax that was reported correctly but never paid. If your spouse filed an accurate return and then spent the money instead of sending the check, §6015(b) and (c) can't help you — your entire case rides on the equitable-relief factors.

A worked example: the $6,200 bill

Say you and your husband filed jointly, and a CP2000 later assessed $6,200 in extra tax from consulting income he earned and never mentioned. The IRS adds the 20% accuracy-related penalty — $6,200 × 0.20 = $1,240 — so the account shows $7,440 before interest, all collectible from either of you.

If you win innocent spouse relief, every dollar attributable to his income comes off your account: your share of the $7,440 drops to $0, and the IRS pursues only him. If you're divorced and elect separation of liability instead, the $6,200 allocates by whose items caused it — his unreported income, his liability, same result for you.

Now change one fact: you knew about roughly $2,000 of that consulting income because the checks hit the joint account you managed. Relief can then be partial — you'd stay liable for the tax and penalty tied to the $2,000 you knew about, while the portion tied to the hidden $4,200 is removed. This is a hypothetical, but it shows why the knowledge questions on the form matter more than any other page. If your spouse actively concealed income from you, documenting that concealment is the heart of the case — our guide on what to do when a spouse hid income covers how to build that record.

Form 8857 instructions, section by section

Form 8857 is about seven pages long, and almost all of it asks about your marriage and money rather than tax computations. Here's what each stretch of the form is really testing:

- The screening questions (start of the form). These confirm you filed a joint return (or live in a community property state) and ask which tax years you want covered. A single Form 8857 can cover multiple tax years — list every year in dispute, because a year you leave off isn't protected.

- You and your spouse. Current contact information, marital status, and dates. Your new address, phone, and employer are kept confidential from the other spouse, even though the IRS must tell them a request was filed.

- Your involvement with the finances and the return. Your education, your health when you signed, who handled the household money, whether you saw the return before signing, and whether anything about your lifestyle should have tipped you off. This is where cases are won or lost — the IRS is measuring what you knew and what you had reason to know. Answer specifically: "he prepared the return the night it was due and I signed at the kitchen table without reviewing it" beats "I wasn't involved."

- Abuse and financial control. The form asks directly about domestic abuse, fear, and whether you were prevented from questioning the finances. Abuse changes how the knowledge factor is weighed — a spouse who knew about income but couldn't safely challenge it can still win relief. Attach whatever exists: protective orders, police reports, medical records, letters from counselors or shelters.

- Your current financial situation. Monthly income and expenses. This feeds the economic-hardship factor for equitable relief — if paying the tax would leave you unable to cover basic living costs, say so with numbers.

- Signature and statement. You sign under penalty of perjury. If the boxes don't fit your story, attach a written statement — a clear two-page narrative, in order, with dates, is often the most persuasive document in the file.

One filing habit that prevents delays: never leave a question blank. Write "I don't know" or "does not apply" — blank answers generate correspondence, and every letter cycle adds weeks in a year when IRS staffing is down roughly 27%.

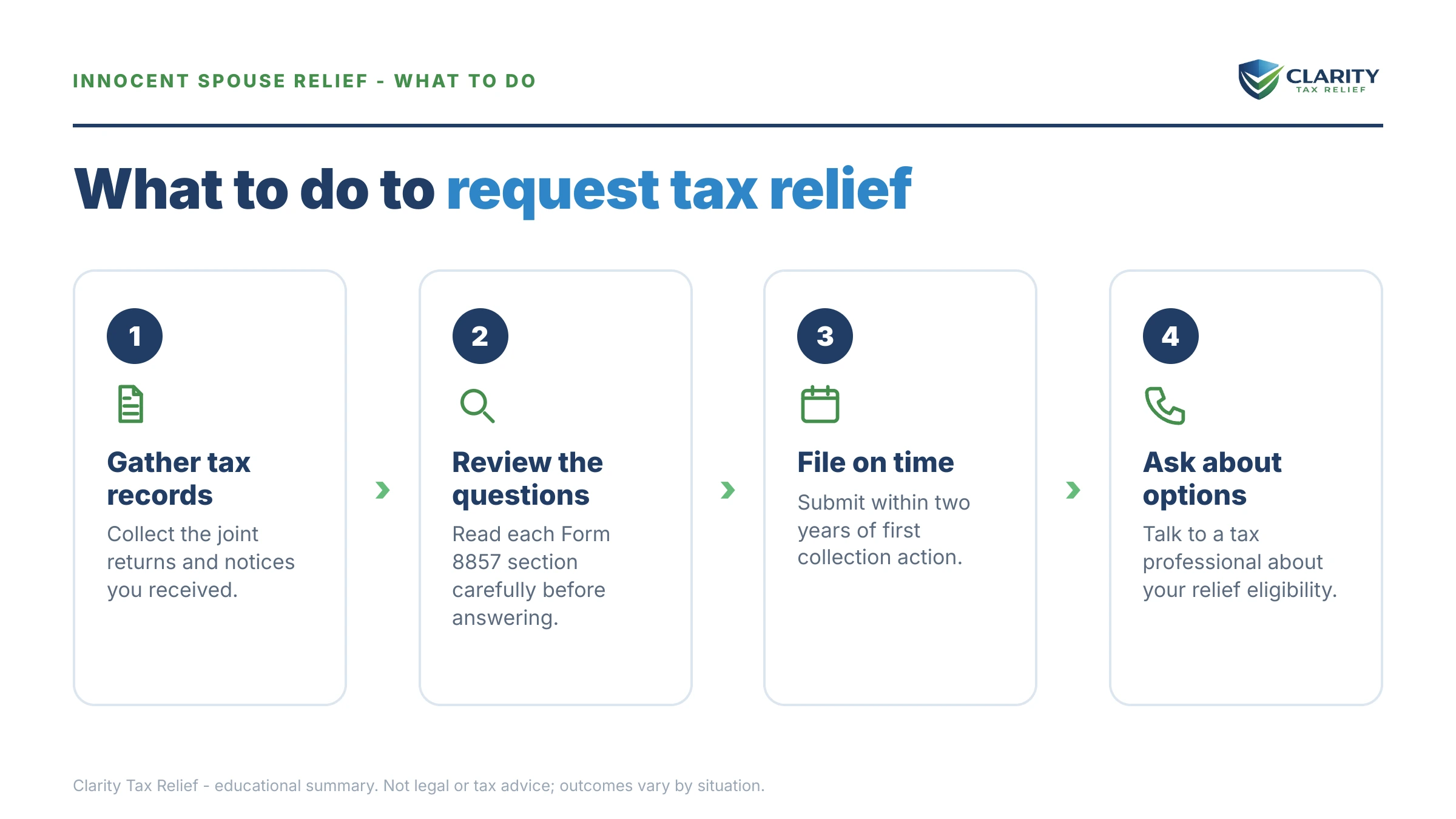

How to file Form 8857, step by step

You file Form 8857 by mail or fax directly to the IRS's innocent spouse unit — never attached to a tax return. Download the current form and its official instructions from the IRS's About Form 8857 page, then work through these steps:

- Gather your paperwork. Pull the IRS notices, the joint returns for each year involved, any divorce or separation documents, and records of your own income and household finances.

- Confirm this is the right form. Answer the screening questions at the start of Form 8857 — they verify you filed jointly (or live in a community property state) and list every tax year you want covered.

- Answer every question, even the hard ones. The form asks about your marriage, your education, your role in the household finances, and how the return was prepared — write "I don't know" rather than leaving a blank.

- Attach proof, not just statements. Include bank records, the divorce decree, medical or police records if abuse applies, and anything showing the income or deductions belonged to your spouse.

- Mail or fax it to the IRS innocent spouse unit. Use the mailing address or fax number in the current IRS instructions for Form 8857 — never attach the form to a tax return.

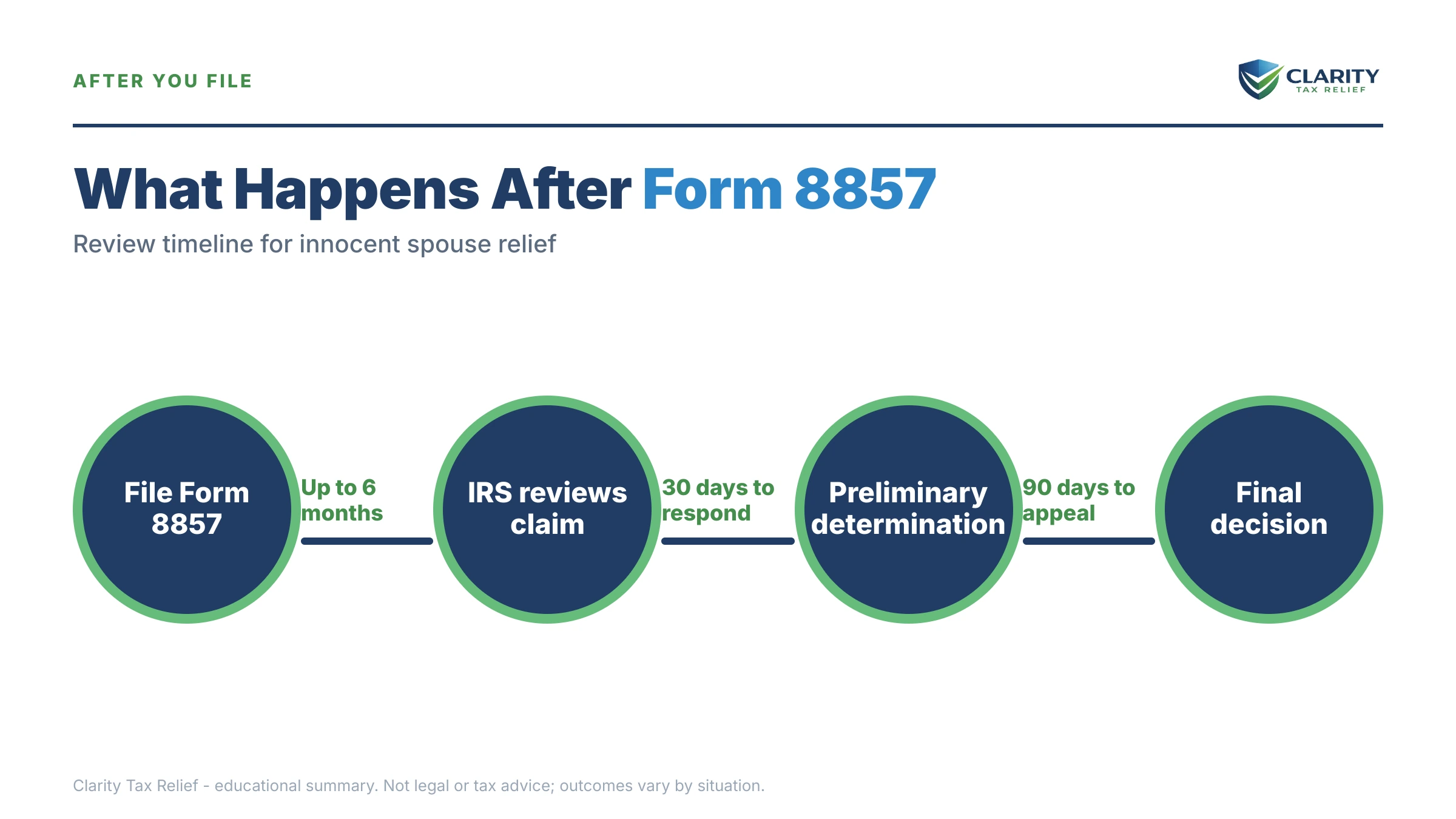

- Calendar the response windows. The IRS will write to you and to the other spouse; you typically get 30 days to dispute a preliminary denial and 90 days to petition the Tax Court after a final one.

Deadlines, appeals, and the rights you keep

Three separate clocks control an innocent spouse case: 2 years to request §6015(b) or (c) relief, roughly 30 days to fight a preliminary denial, and 90 days to take a final denial to Tax Court. Miss one and you don't just lose time — you lose a specific right:

| Event | Your window | What you lose if it passes |

|---|---|---|

| IRS's first collection activity against you (refund offset, levy notice, collection suit) | 2 years to file Form 8857 for §6015(b) or (c) relief | Both of those relief types — only equitable relief remains |

| IRS preliminary determination letter | Typically 30 days to disagree using Form 12509 | Review by the IRS Independent Office of Appeals before the decision goes final |

| IRS final determination letter | 90 days to petition the U.S. Tax Court | Independent court review of the denial |

| LT11 / Letter 1058 final notice of intent to levy | 30 days to request a CDP hearing on Form 12153, where innocent spouse relief can be raised | The pre-levy hearing and the Tax Court path attached to it |

| Payments you already made on the joint debt | Generally 3 years from the return or 2 years from the payment to claim them back | Any refund of amounts you personally paid on your spouse's tax |

While your request is pending, the IRS generally suspends collection against you for those years — but the meter doesn't stop. Interest keeps accruing, and the 10-year collection statute is extended by the time the case is open plus 60 days, giving the IRS longer to collect whatever survives. You can estimate where your own 10-year clock stands with our CSED Calculator.

If the IRS denies relief, don't restart — appeal. The innocent spouse denial appeal process runs through Form 12509 to Appeals and then, if needed, to Tax Court, where the judge looks at the case fresh rather than deferring to the IRS's decision. Cases genuinely turn around at both stages.

When you can handle Form 8857 yourself

You can file Form 8857 on your own — the form is free, there's no application fee, and nobody knows your marriage better than you do. DIY makes sense when the facts are clean: one tax year, the income or deduction is clearly and provably your spouse's, you're within the 2-year window, you have documents (the CP2000, the divorce decree, bank statements), and there's no abuse or safety issue complicating the story.

Experienced help changes outcomes in the messier cases: partial knowledge that needs careful framing, abuse or financial control that must be documented and argued under the equitable-relief factors, unpaid-tax cases where everything hinges on factor-weighing, a levy already in motion that requires coordinating the CDP route with the 8857, or an appeal after a denial. A representative also handles all IRS contact — you'd authorize that with Form 2848, power of attorney — which matters when reliving the marriage on paper is the hardest part of the filing. If cost is a barrier, the Taxpayer Advocate Service and low-income taxpayer clinics take innocent spouse cases at no charge for those who qualify.

Terms on Form 8857, decoded

- Joint and several liability — the rule that makes each spouse on a joint return individually responsible for the entire tax bill, not half of it.

- Understatement vs. underpayment — an understatement is tax the return should have shown but didn't (hidden income, fake deductions); an underpayment is tax the return showed correctly but nobody paid. Only equitable relief covers underpayments.

- Non-requesting spouse — the other person on the joint return. The IRS must notify them, let them participate, and let them appeal a decision granting you relief.

- Preliminary and final determination — the IRS's two-stage answer. The preliminary letter is contestable within about 30 days via Form 12509; the final letter starts the 90-day Tax Court clock.

- Attribution — whose income, deduction, or credit caused the tax. Relief only reaches items attributable to the other spouse.

- CSED — the Collection Statute Expiration Date, the 10-year deadline on IRS collection. Filing Form 8857 pauses collection against you and extends this date by the pending time plus 60 days.

For the IRS's own plain-language overview of the program, see Innocent Spouse Relief at IRS.gov.

Form 8857 questions, answered

Will my spouse or ex-spouse find out I filed Form 8857?

Yes — the law requires the IRS to notify the other person on the joint return and give them a chance to participate in the review. The IRS will not share your current address, phone number, employer, or other new personal details with them. If you are in an abusive situation, say so on the form; the IRS weighs abuse heavily and handles those cases with extra care.

How long does Form 8857 take to process?

The IRS says a Form 8857 review can take up to six months, and 2026 staffing shortages can stretch it longer. During that time the IRS gathers your information, contacts the other spouse, and issues a preliminary determination. Collection against you for those years is generally paused while the request is pending, though interest keeps accruing on any balance that survives.

What is the deadline to file Form 8857?

For innocent spouse relief and separation of liability, you generally have 2 years from the date of the IRS's first collection activity against you — such as a refund offset or a levy notice. Equitable relief is different: you can request it for as long as the IRS can still collect the balance, or within the refund window if you are asking for money back.

What's the difference between Form 8857 and Form 8379?

Form 8857 (innocent spouse) asks the IRS to remove your responsibility for tax caused by your spouse on a joint return. Form 8379 (injured spouse) asks for your share of a joint refund back when it was seized for your spouse's separate debt, like child support or their old taxes. If the debt itself is joint tax your spouse caused, you want 8857; if a taken refund is the only problem, you want 8379.

Does filing Form 8857 stop the IRS from collecting?

Generally, yes — the IRS pauses most collection against you for the years in your request while it decides, though it can still collect from the other spouse. Two trade-offs: interest continues to build on any amount you ultimately owe, and the pause extends the IRS's 10-year collection deadline by the time the request is pending plus 60 days.

Can I get back money the IRS already took from me?

Sometimes. Innocent spouse relief and equitable relief can include refunds of payments you made, but only within the refund window — generally three years from when the return was filed or two years from the payment, whichever is later. Separation of liability relief cannot produce a refund; it only removes what you have not yet paid.

What happens if the IRS denies my Form 8857?

You are not done. First you receive a preliminary determination — you typically have 30 days to disagree using Form 12509, which sends the case to the IRS Independent Office of Appeals. If the final determination still denies relief, you have 90 days to petition the U.S. Tax Court, which reviews the case fresh rather than just checking the IRS's work.

Do I qualify for relief if we're still married and living together?

You can — innocent spouse relief and equitable relief have no divorce requirement. Only separation of liability requires that you be divorced, legally separated, widowed, or living apart for the 12 months before you file. Being married does affect the equitable-relief factors, since the IRS looks at whether you benefited from the unpaid tax and whether paying it would cause your household hardship.

Your next 24 hours

- Find your trigger date. Pull the notice that started collection against you — a refund-offset notice or a levy notice — and write down its date. Your 2-year window for innocent spouse and separation-of-liability relief runs from there.

- Gather three things. The joint returns for the years involved, every IRS letter you've received, and any divorce, separation, bank, or abuse-related records showing whose income caused the debt and what you knew.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will tell you which of the four relief types fits your facts and whether your window is still open.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.