Levies & Garnishment

Can the IRS Garnish 1099 Income? The One-Time Levy on Contractor Pay (2025)

The short answer: yes, the IRS can garnish 1099 income — but a contractor levy is usually a one-time levy. It only takes what your client owes you at the exact moment the levy is served. It does not automatically grab your future invoices the way a paycheck garnishment grabs every paycheck.

Worried a 1099 levy is coming — or already hit a client?

Send us a photo of your notice. An experienced tax professional will tell you exactly where you stand, whether a levy is imminent, and what your fastest options are — free, confidential, no pressure.

⏱ Your deadline: before levying, the IRS must send a Final Notice of Intent to Levy (an LT11 or Letter 1058) and wait 30 days. Those 30 days are also your window to request a Collection Due Process hearing, which pauses collection. Once the window closes, a levy can be served without further warning.

Yes — the IRS can reach your 1099 income

If you're an independent contractor, freelancer, or gig worker and you owe back taxes, the IRS can garnish your 1099 income. It does this by sending a Notice of Levy (Form 668-A) to whoever pays you — a client, a platform, or a company you invoice. That payer is legally required to turn over money it owes you and send it to the IRS instead.

This power comes straight from the tax code, and the IRS explains the basics on its official levy page. But here's the part most people don't know — and it matters a lot for contractors: a 1099 levy works very differently from a paycheck garnishment.

Why a 1099 levy is "one-time," not continuous

When the IRS garnishes an employee's wages, it uses a continuous levy. That means it keeps taking part of every paycheck, automatically, until the debt is paid or the levy is released.

A levy on independent-contractor pay is different. Because you aren't an employee, your client doesn't "owe" you ongoing wages — they owe you only for work you've already invoiced. So a 1099 levy is generally a one-time grab: it captures whatever your client owes you at the precise moment the levy lands, and nothing more.

Want to picture it? Here's a simple example.

- You owe the IRS $18,000. The IRS serves a one-time levy on a client who owes you $4,000 for a finished project.

- The client must send that $4,000 to the IRS. Your balance drops to $14,000.

- Next month you invoice that same client another $4,000 for new work. The old levy does not touch it. To reach that payment, the IRS would have to serve a brand-new levy.

That's the contractor's small advantage: each future payment requires a fresh levy. It is not a free pass — the IRS can keep sending new levies — but it does mean a single levy won't drain everything you'll ever earn. And it means acting quickly can protect the income that hasn't been invoiced yet.

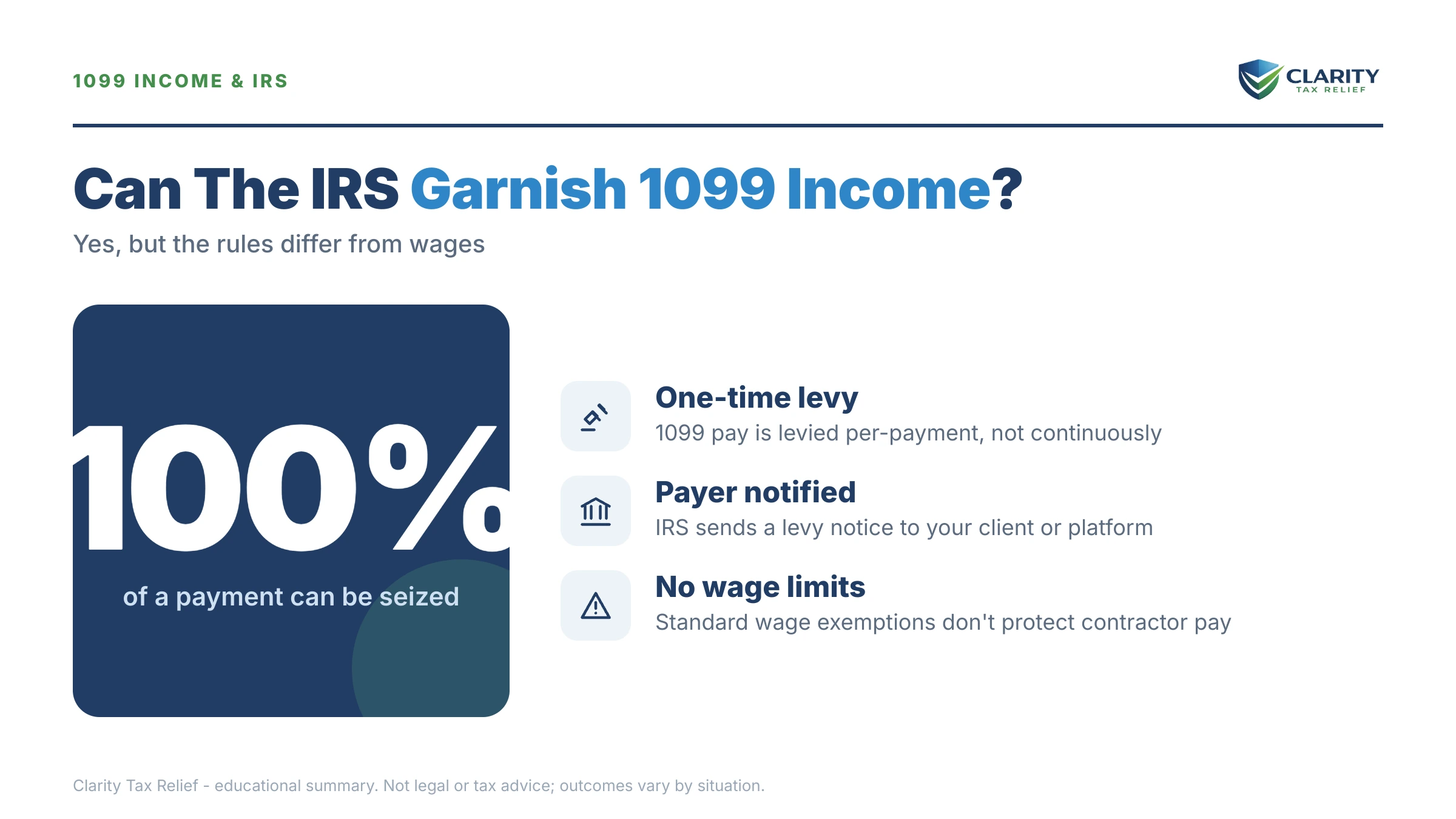

How much of your contractor pay can the IRS take?

This is where 1099 workers are actually more exposed than employees. For wages, the law protects a portion of each paycheck from garnishment (the exempt amount depends on your filing status and dependents). You can read how that works in our guide to how much the IRS can garnish from a paycheck.

For 1099 income, there is no automatic exempt amount. A one-time levy can take up to the entire amount your client owes you, up to your tax debt. Nothing is set aside for rent, groceries, or your own self-employment taxes. That's why, for contractors, the goal isn't usually to "negotiate the percentage" — it's to get the levy released and replaced with an arrangement you can live on.

What happens if you ignore the notices

The IRS doesn't levy out of nowhere. A levy is the end of an automated sequence of letters. Each step gives you a chance to act — and each one you ignore brings the levy closer:

- CP14 — the first bill for the unpaid tax. No enforcement yet.

- CP501 / CP503 — reminder notices. The balance keeps growing with penalties and interest.

- CP504 — Notice of Intent to Levy. The IRS can now take your state tax refund and a federal tax lien becomes likely.

- LT11 / Letter 1058 — the Final Notice of Intent to Levy. After 30 days, the IRS can serve a levy on your bank account or your 1099 clients.

The LT11 notice (or Letter 1058) is the one that matters most. It's the IRS's legal last warning, and it carries your right to a Collection Due Process hearing. Miss that 30-day window and you lose your easiest path to stopping the levy before it starts.

Your options to stop or release the levy

A levy on contractor pay isn't permanent. Several routes can stop one before it happens — or release one already in place:

- Installment agreement — a monthly payment plan. Once an agreement is in place, the IRS generally won't levy. For balances under about $50,000, a streamlined installment agreement can often be set up without detailed financial disclosure.

- Currently Not Collectible status — if a levy would leave you unable to cover basic living expenses, the IRS can pause collection. The debt remains, but levies stop while your finances recover.

- Collection Due Process appeal — filed within 30 days of your LT11 or Letter 1058. This pauses collection and puts your case in front of the IRS Independent Office of Appeals.

- Hardship levy release — if a levy is already taking money you need to live on, you can request an emergency release. See how an emergency levy release for hardship works.

- Offer in Compromise — settling for less than the full balance. It's real, but only when your income and assets genuinely can't cover the debt. Anyone promising to settle your taxes for "pennies on the dollar" before reviewing your finances is selling you something — the IRS runs the math, not the marketing.

How to respond, step by step

- Read the notice and find your deadline. If you're holding an LT11 or Letter 1058, the 30-day clock is running. Note the date.

- Confirm what you actually owe. Log into your IRS online account and compare the balance with your records. Make sure all your returns are filed — the IRS won't approve most arrangements until they are.

- Pick the option that fits. If you can pay over time, set up a plan. If paying anything is a hardship, gather your income and expense figures for a Currently Not Collectible or Offer review.

- If a levy already hit a client, act immediately — a hardship release or a quickly arranged payment plan can free up money, and the one-time nature of the levy means your next invoice may still be safe.

- Get a professional review if you owe more than $10,000, have unfiled years, or have a revenue officer assigned. The order you fix things in — returns, then arrangement, then penalties — changes what you end up paying.

You can verify any deadline or appeal right yourself with the Taxpayer Advocate Service, an independent IRS office that helps when collection causes hardship — start at the Taxpayer Advocate Service.

1099 levy questions, answered

Can the IRS garnish 1099 income?

Yes. The IRS can levy money a client owes an independent contractor. But a 1099 levy is usually a one-time levy — it only grabs what the payer owes you at the exact moment the levy is served. It does not automatically capture your future invoices the way a wage garnishment captures every paycheck.

Is a 1099 levy the same as a wage garnishment?

No. A wage garnishment is continuous — it keeps taking part of every paycheck until the debt is paid or released. A levy on independent-contractor pay is generally one-time. To reach a future payment, the IRS has to serve a brand-new levy each time. That difference is why acting fast can protect upcoming income.

How much of my 1099 income can the IRS take?

There is no fixed exempt amount for contractor pay the way there is for wages. A one-time 1099 levy can capture up to the full amount the client owes you at the moment it is served, up to your tax debt. Because nothing is automatically protected, a hardship release or payment plan is often the fastest way to free up money you need to live on.

Will the IRS notify me before levying my 1099 income?

Almost always, yes. Before levying, the IRS must send a Final Notice of Intent to Levy (an LT11 or Letter 1058) and give you 30 days to respond. That notice also gives you the right to a Collection Due Process hearing, which pauses collection while your case is reviewed.

How do I stop the IRS from levying my contractor pay?

Respond before the deadline on your notice. Setting up an installment agreement, requesting Currently Not Collectible status for hardship, filing a Collection Due Process appeal, or paying the balance can all stop or release a levy. An experienced tax professional can pick the fastest route for your situation.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.