IRS Levies & Garnishment

Can the IRS Garnish SSDI? What the 15% Levy Takes and How to Stop It (2026)

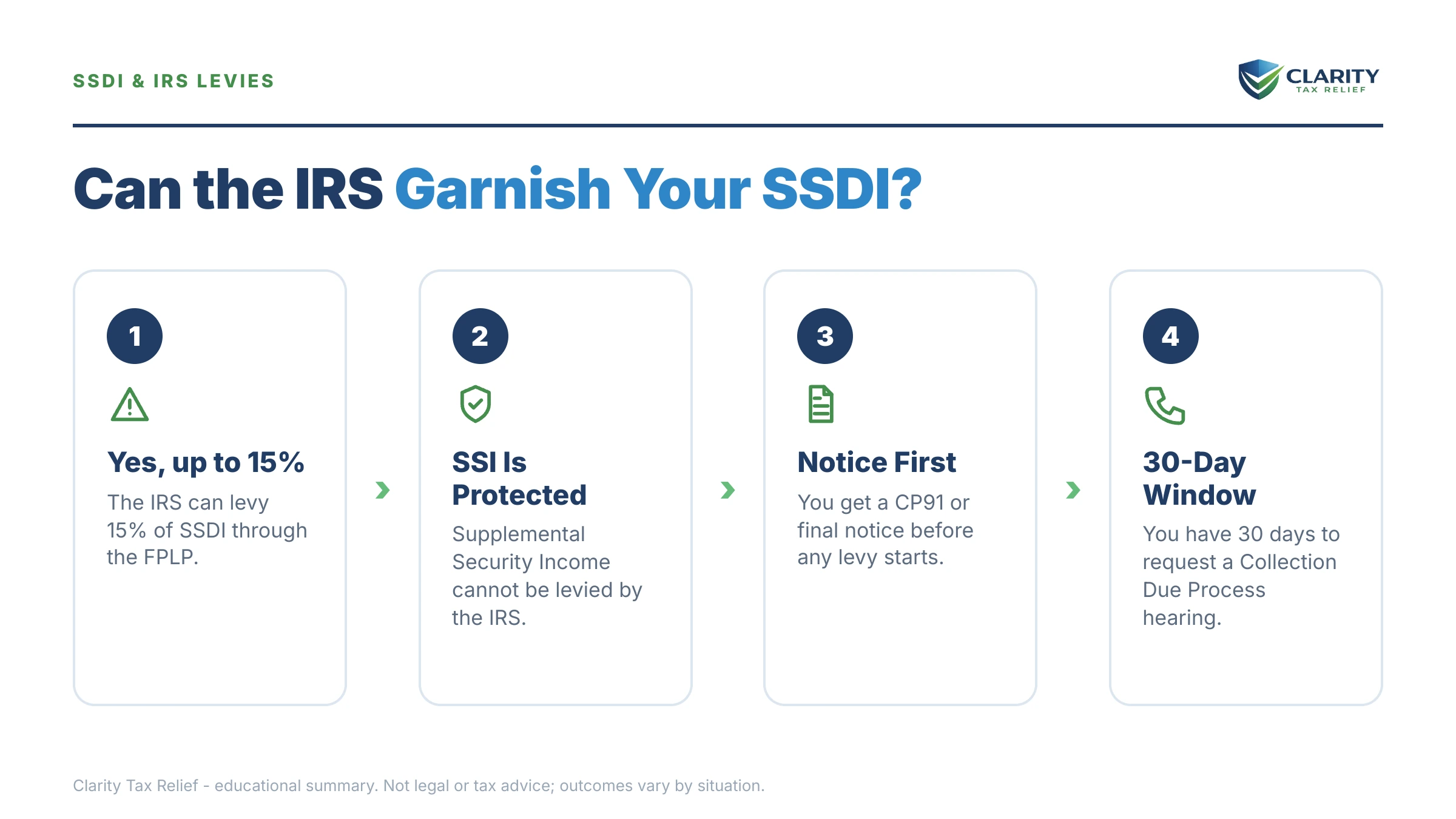

The short answer: yes — the IRS can garnish SSDI. Through the Federal Payment Levy Program, it can take up to 15% of your monthly Social Security Disability check, every month, until the debt is resolved. SSI is exempt. Before the levy starts, the IRS must send a CP91 notice giving you 30 days to respond.

So if you're asking "can the IRS garnish SSDI," the honest answer is yes — but only up to 15%, only after a specific warning notice, and only until you put one of several resolutions in place. On a disability income, you actually have more leverage than most taxpayers, because the same hardship rules that make your budget tight also make you a strong candidate for the IRS's relief programs.

Maybe you ran your own business for years — filed the Schedule C, paid quarterlies when cash allowed — and then your health made the decision for you. The business income stopped, the SSDI checks started, and the old self-employment balance is still sitting on the IRS's books, growing. Now a letter is threatening the only income you have left. That letter is beatable, and this guide maps every path.

If the letter in your hand is a CP91 notice — the specific final warning the IRS sends before touching Social Security benefits — the image below shows exactly what it looks like and where to find the two things that matter most: the notice date and the balance the IRS is collecting on.

⏱ Your deadline: you have 30 days from the date printed on a CP91 before the IRS can start taking 15% of your SSDI. Respond inside that window and the levy never begins. Miss it and the deduction comes out of every monthly check — while penalties and interest keep accruing on the full balance — until the debt is resolved, released, or the collection statute expires.

Why the IRS can garnish SSDI — and why the 15% cap exists

SSDI is a federal payment, and IRC §6331(h) lets the IRS take up to 15% of any federal payment through an automated system called the Federal Payment Levy Program. No judge, no court order, no human review — the Federal Payment Levy Program matches your Social Security number against the IRS's balance-due files and tells Treasury to hold back 15% before your deposit ever reaches your bank.

One technical point that matters: the IRS calls this a levy, not a garnishment. Garnishments are what private creditors get through court — and private creditors generally can't touch SSDI. The IRS doesn't need a court. That's why the "SSDI is protected from garnishment" advice you may have read is true for credit cards and medical bills, and wrong for federal taxes.

The 15% is calculated on your gross monthly benefit, before Medicare premiums come out. Unlike a paycheck levy, there's no exempt living amount under FPLP — if 15% breaks your budget, the fix is requesting a hardship release (covered below), not waiting for the system to notice. The IRS does run a low-income filter that is meant to screen many below-poverty-level Social Security recipients out of FPLP before levies start, but it isn't perfect and it isn't a right you can count on.

One more edge case: a revenue officer can bypass FPLP and issue a manual paper levy on Social Security that is not capped at 15%, leaving you only an exempt amount from IRS tables. These are rare on SSDI-only accounts, but they show up in larger cases — a $68,500 self-employment balance is the kind of file that can eventually get human attention.

SSDI vs. SSI vs. other benefits: what the IRS can and can't touch

The IRS's automated levy reaches SSDI and Social Security retirement, but it cannot touch SSI. The distinction is the program, not the disability: SSDI is an earned insurance benefit based on your work record, so the law treats it like other federal payments. SSI is need-based welfare, and Congress kept it out of the levy program entirely.

| Benefit type | Automated 15% levy (FPLP)? | What to know |

|---|---|---|

| SSDI (disability insurance) | Yes — up to 15% | Continuous every month until released, paid, or the statute expires |

| Social Security retirement | Yes — up to 15% | Same program; see can the IRS garnish Social Security |

| SSI (Supplemental Security Income) | No | Need-based; excluded from FPLP entirely |

| VA disability compensation | Generally no | Service-connected compensation is broadly protected — see can the IRS take VA benefits |

| SSDI lump-sum back pay | Not via FPLP | Reachable by a bank levy once deposited; 21-day bank-levy hold applies — a window to call the IRS and request a release, not a shield; the funds are still remitted on day 22 unless the levy is released |

That last row trips people up. Your monthly check can only lose 15% — but once money sits in your bank account, it's just money to the IRS. A bank levy can freeze the whole balance, and the automatic two-months-of-benefits protection your bank applies against ordinary creditors does not stop a federal tax levy. If a five-figure back-pay award is on its way and you owe, get a resolution in place before it lands.

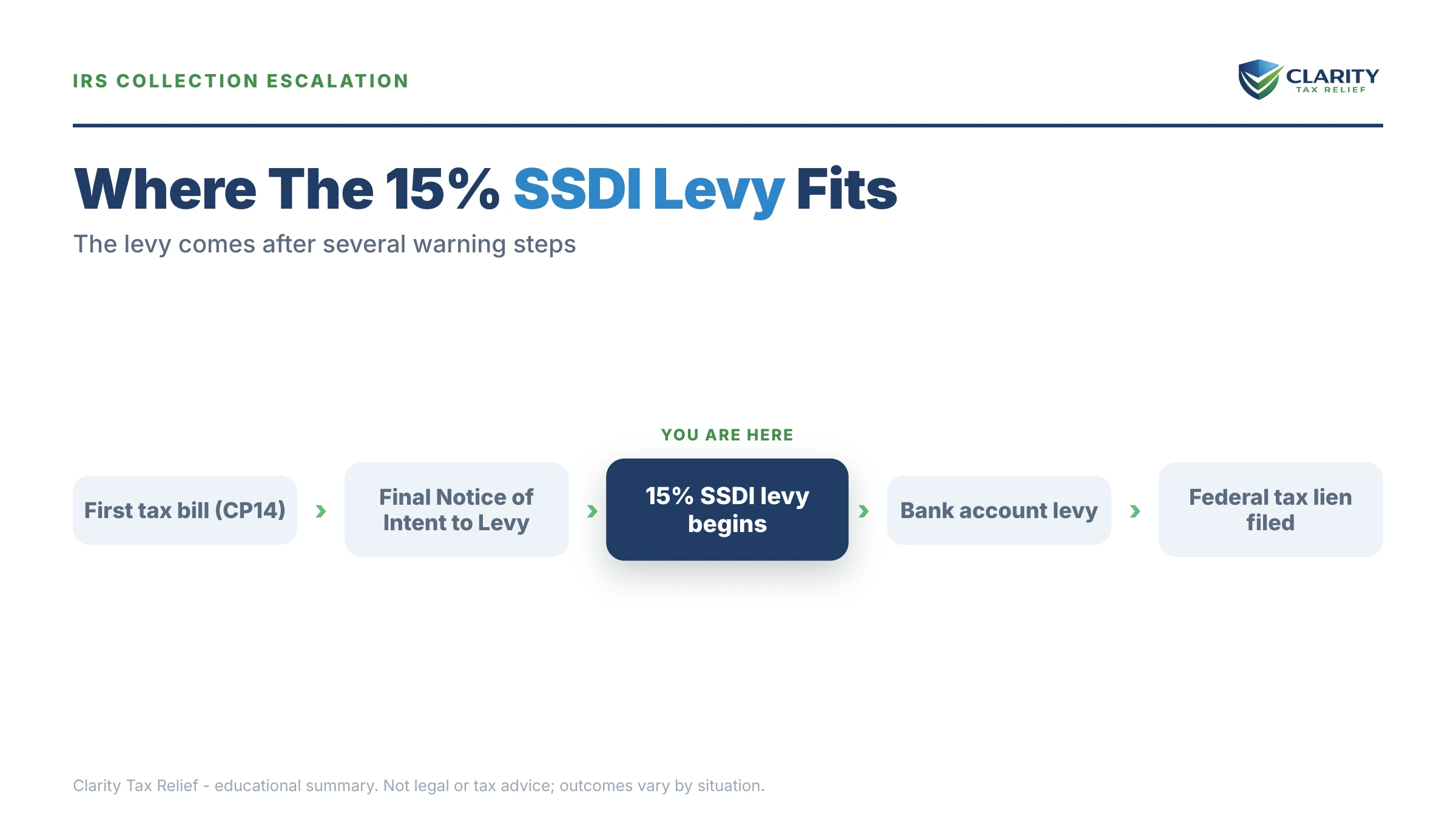

What happens if you ignore it: the road to a Social Security levy

The path from first bill to a levy on your SSDI is fully automated, and it runs on a specific notice sequence. In 2026, with the IRS workforce down roughly 27%, you may never speak to a human along the way — but the computers issuing these notices never stopped:

- CP14 — the first bill. No enforcement yet; the cheapest moment to act.

- CP501 / CP503 — reminders. Still just bills, but penalties and interest are compounding on the balance.

- CP504 — intent to levy your state refund. The IRS can now seize a state tax refund, and a federal tax lien becomes likely on larger balances.

- CP91 / CP298 — final notice before Social Security levy. This is the SSDI-specific warning. Thirty days from its date, the FPLP levy can begin.

- The levy starts. Fifteen percent of your gross benefit is diverted every month — continuously, with no further notices required.

- CP90 or LT11 for everything else. A separate final notice can open your bank accounts and other income to levy; it also triggers formal Collection Due Process appeal rights via Form 12153.

Two things make waiting expensive. First, the levy is continuous — unlike a one-time bank levy, it repeats every month without a new notice. Second, on a fixed income, 15% off the top usually collects slower than penalties and interest accrue, so you can lose the money and still watch the balance grow. The escalation only moves one direction; your options only shrink.

On SSDI and holding an IRS levy notice?

If it's a CP91, the levy can start 30 days from the printed date — and on a disability income, you may qualify for relief that stops it entirely. Get your notice reviewed free before that window closes: call (888) 825-7779 or use the 2-minute form.

Your options on a fixed SSDI income

Every resolution that stops the FPLP levy is available to SSDI recipients, and a fixed disability income makes you a stronger candidate for the hardship-based ones. Which option fits depends mostly on the size of the debt and what your budget shows:

| What you owe | Realistic options on SSDI income | What it takes |

|---|---|---|

| Up to $10,000 | Guaranteed installment agreement (up to 3 years), or short-term plan up to 180 days with $0 setup fee | Filed returns current; no financial disclosure needed |

| $10,001 – $50,000 | Streamlined plan online, up to 72 months — but if the payment squeezes basic living costs, Currently Not Collectible may fit better | Online setup, no detailed financials at streamlined levels |

| Over $50,000 (like $68,500) | Payment plan with financial disclosure, Currently Not Collectible, or an Offer in Compromise — CNC and OIC are common outcomes when SSDI is the only income | Form 433-F income/expense review; OIC requires Form 656 and full financials |

| Any amount, genuine hardship | Currently Not Collectible status pauses all levies; OIC with low-income certification can settle for what the IRS could realistically collect | Proof that paying anything prevents basic living expenses |

Three specifics worth knowing before you pick:

- CNC stops the levy but not the clock. The 10-year collection statute keeps running while you're in hardship status. For many SSDI recipients whose income will never recover, CNC quietly carries the debt to expiration. The trade-off: interest keeps accruing and any tax refunds get offset.

- An OIC on disability income can be genuinely viable — but it's not automatic. The IRS accepted roughly 1 in 5 offers in FY2024. Your offer is driven by what the IRS could actually collect from your assets and income, and if your AGI is at or below 250% of the federal poverty level, low-income certification waives the $205 application fee, the 20% down payment, and payments during review.

- A payment plan works if the number is honest. Approved installment agreements pull your account out of FPLP — but agree only to a payment your real budget supports, because a defaulted plan restarts the whole sequence.

For the general mechanics of getting any IRS levy or garnishment released, our guide on how to stop IRS wage garnishment covers the shared playbook; everything on this page is what's different when the income being levied is SSDI.

A worked example: $68,500 in old self-employment tax on a $1,850 SSDI check

Say you owe $68,500 from your last three self-employed years, and your SSDI benefit is $1,850 a month ($22,200 a year). Here's the math the IRS's computer never shows you:

- The levy: 15% × $1,850 = $277.50 taken every month — $3,330 a year — leaving you $1,572.50 to live on.

- The problem: penalties and interest keep accruing on the full $68,500, and at recent rates that annual accrual can approach or exceed the $3,330 the levy collects. You lose the money and the balance barely moves — or grows.

- The hardship case: on Form 433-F, $1,850 of income against ordinary allowable living expenses typically shows nothing left over. That's the profile of a Currently Not Collectible account — levy released, monthly payment $0, while the 10-year clock keeps running.

- The settlement case: with no meaningful assets and no future income beyond SSDI, the amount the IRS could realistically collect may be a small fraction of $68,500 — and at $22,200 AGI, this taxpayer would likely meet the low-income certification that waives the OIC fee and down payment. Acceptance is never guaranteed, but this is exactly the fact pattern the program exists for.

This example is hypothetical, but the arithmetic is why fighting the levy usually beats enduring it. You can estimate what a levy would take from your own benefit with our IRS Wage Garnishment Calculator.

Two persona-specific wrinkles for former sole proprietors: first, make sure every year is filed — the IRS won't approve CNC, a plan, or an OIC with unfiled returns outstanding, and it may have filed inflated substitute returns for your missing years that a real return can shrink. Second, if any of the debt is 1099 income the IRS is still chasing separately, the levy rules differ — see can the IRS garnish 1099 income.

How to respond to an SSDI levy threat, step by step

- Identify your notice. Find the notice number in the top corner — CP14, CP504, CP91, or CP90 — and the date printed on it; together they tell you exactly how much time you have.

- Verify the balance and assessment dates. Log into your IRS online account or pull an account transcript to confirm what you owe and when the 10-year collection clock started for each year.

- Run your hardship math. List your SSDI income against your monthly living expenses the way Form 433-F does — if nothing is left over, you likely have a Currently Not Collectible case.

- Request a resolution before the 30-day date. Call the number on the notice — or have a representative do it — and ask for CNC status, an installment agreement, or submit an Offer in Compromise; any of these blocks the FPLP levy.

- If the levy already started, push for a release. Document economic hardship under IRC §6343 and request an immediate levy release; if the IRS refuses, appeal through a CDP hearing (Form 12153) or the CAP process.

On that last step: an economic hardship levy release is not a favor — the law requires the IRS to release a levy that prevents you from meeting basic living expenses. The burden is on you to document it, which is why the Form 433-F numbers in step three do double duty.

When you can handle this yourself — and when help changes the outcome

Plenty of SSDI levy situations are genuinely DIY. If your balance is under $10,000 and all your returns are filed, a guaranteed installment agreement takes one phone call or an online session, and the FPLP release follows. If you got a first bill you agree with and can pay within 180 days, a short-term plan costs nothing to set up. If the CP91's numbers are simply wrong — a payment that didn't post, a year you already resolved — a written response with proof handles it.

Experienced help earns its cost in four situations: the levy is already running and every month costs you $200–$300 you can't spare; you have multiple unfiled self-employment years that must be reconstructed before the IRS will approve anything; the balance is large enough (like $68,500) that the IRS demands full financial disclosure and the way your 433-F is presented decides between a payment you can't afford and CNC; or you're pursuing an Offer in Compromise, where the offer math and documentation determine whether you land in the accepted fifth or the rejected four-fifths. If the account is also tangled with bankruptcy questions, start with does bankruptcy stop an IRS levy before assuming either path.

Terms on your notice, decoded

- FPLP (Federal Payment Levy Program): the automated Treasury system that diverts up to 15% of federal payments — including SSDI — to the IRS.

- Continuous levy: a levy that repeats every payment cycle without a new notice, unlike a one-time bank levy.

- CP91 / CP298: the final notice the IRS must send before levying Social Security benefits; it starts the 30-day countdown.

- CNC (Currently Not Collectible): hardship status that pauses levies and payments because collection would prevent basic living expenses; the debt remains and interest accrues.

- CSED (Collection Statute Expiration Date): the date, generally 10 years after assessment, when the IRS's right to collect — and any FPLP levy — ends; certain events pause the clock.

- Economic hardship release (§6343): the legal requirement that the IRS release a levy that leaves you unable to pay reasonable basic living expenses.

SSDI garnishment questions, answered

Can the IRS garnish SSDI disability payments?

Yes. SSDI is a federal payment, and the Federal Payment Levy Program lets the IRS take up to 15% of your monthly benefit automatically — no court order needed. The IRS must first send a final notice, usually a CP91, giving you 30 days to respond. SSI, which is need-based, is exempt from this program.

How much of my SSDI check can the IRS take?

Up to 15% of your gross monthly benefit through the automated Federal Payment Levy Program. Unlike a wage levy, FPLP applies no exempt living amount — the 15% comes out even if it causes hardship, until you request a release. In rare cases a revenue officer can issue a manual levy that isn't capped at 15%, though part of the benefit is exempt under IRS tables.

Is SSI protected from IRS garnishment?

Yes. Supplemental Security Income is a need-based benefit and is excluded from the Federal Payment Levy Program, so the IRS's automated 15% levy never touches it. If you receive both SSI and SSDI, only the SSDI portion is exposed. The debt itself doesn't go away, though — refund offsets and other collection tools still apply.

What is a CP91 notice?

A CP91 (or CP298 for businesses) is the IRS's final notice before it levies your Social Security benefits. It states the balance and warns that up to 15% of your monthly benefit will be taken if you don't respond within 30 days of the notice date. Responding inside that window — with a payment plan, hardship request, or appeal — is what stops the levy from starting.

Can I get an SSDI levy released after it starts?

Yes. The fastest paths are proving economic hardship under IRC §6343, which requires the IRS to release a levy that prevents you from meeting basic living expenses, or getting into Currently Not Collectible status or an installment agreement. You'll typically need to give the IRS your income and expense numbers, usually on Form 433-F, before it agrees to release.

Can the IRS take my SSDI back pay?

Not through the FPLP levy itself — that program takes 15% of ongoing monthly benefits. But once a lump-sum back-pay award lands in your bank account, it becomes reachable by an ordinary IRS bank levy, and the automatic two-month protection banks apply against most creditors does not stop a federal tax levy. If a large deposit is coming and you owe, resolve the account first.

Does the 15% Social Security levy end when the 10-year collection statute expires?

Yes. The IRS generally has 10 years from the date a tax was assessed to collect (the CSED), and an FPLP levy must stop when that date passes. But the clock pauses for things like Offer in Compromise review, bankruptcy, and Collection Due Process appeals, so your real expiration date may be later than ten calendar years. Pull your account transcript to confirm the assessment dates.

Will a payment plan stop the IRS from garnishing my SSDI?

Generally yes. Once an installment agreement is approved — or your account is placed in Currently Not Collectible status — the IRS releases the account from the Federal Payment Levy Program and the 15% deduction stops. Set it up before the CP91's 30-day window closes and the levy never starts. Note that interest and penalties keep accruing on the balance under a payment plan.

Your next 24 hours

- Find the notice number and date. Check the top right corner of the letter — if it says CP91, count 30 days from the printed date; that's your real deadline. If it says CP14 or CP504, the Social Security levy hasn't been queued yet and you're acting early, which is cheaper.

- Gather three things: the notice itself, your most recent tax return (or a list of unfiled years), and your SSDI award amount plus a rough monthly budget. Those are the inputs for every option on this page.

- Get the notice reviewed free. Send it through the 2-minute form or call (888) 825-7779. An experienced tax professional will tell you whether your numbers point to hardship status, a plan, or an offer — before the 30-day window on a CP91 closes and the 15% starts coming out of your check.

Primary sources: the IRS's payment options are at IRS.gov/payments; if the levy is causing hardship and you can't get traction, the independent Taxpayer Advocate Service can intervene; and your exact benefit amount is in your account at SSA.gov.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.