IRS Collections

Can the IRS Take VA Disability? What the Law Protects — and What It Doesn't (2026)

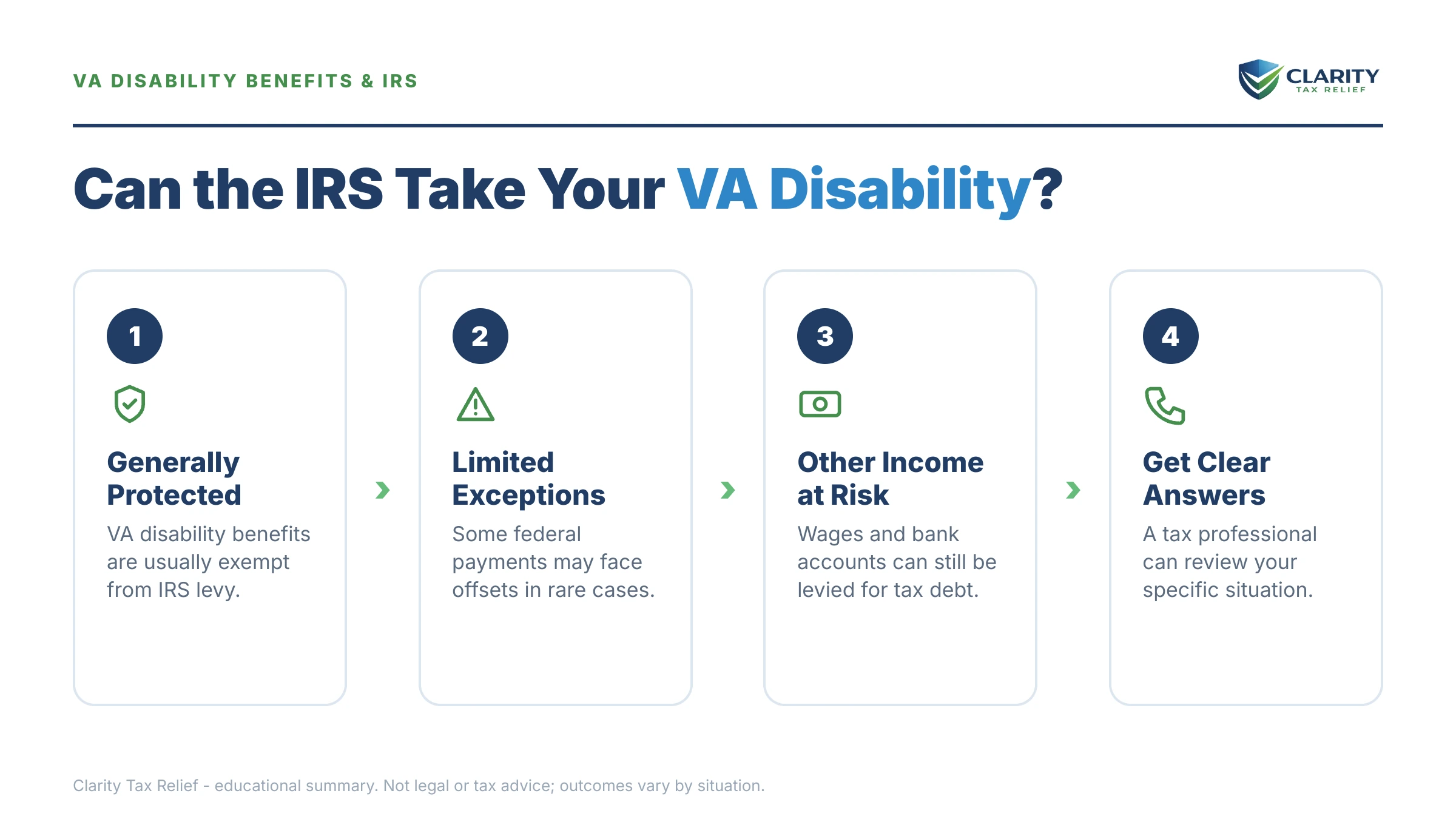

The short answer: no — the IRS cannot take VA disability at the source. IRC §6334(a)(10) exempts service-connected VA disability compensation from levy, so your monthly check keeps arriving in full. But the protection stops there: once the money hits your bank account, a levy can reach it, and your other income and refunds stay exposed.

You earned that rating, and the compensation attached to it is one of the very few income streams federal law puts beyond the IRS's collection power. If you're looking at a back-tax balance right now, that protection is real — but it's narrower than most veterans assume, and the debt keeps growing whether or not the IRS can touch your check. Here's exactly where the line sits, and what to do about the balance itself.

⏱ The clocks that actually run: there's no deadline printed on this question, but two timers never stop. The failure-to-pay penalty adds 0.5% of your balance every month (plus daily interest), and if an IRS bank levy ever hits your account, the bank holds the frozen funds just 21 days before sending them to the Treasury.

Why the IRS can't take VA disability at the source

The IRS cannot levy service-connected VA disability compensation — IRC §6334(a)(10) exempts those payments from levy entirely. On top of that, 38 U.S.C. §5301 broadly shields VA benefits from attachment and seizure. The exemption is automatic: you don't apply for it, claim it on a form, or prove hardship to get it.

In practice, that means the IRS never sends the VA a levy against your service-connected compensation, and your deposit arrives in full every month no matter how large your tax balance grows. Even the IRS's automated Federal Payment Levy Program — the system that takes a continuous 15% of other federal payments — does not reach service-connected VA disability compensation.

Don't confuse this with other benefits that only sound similar:

- SSDI is not VA disability. Social Security Disability Insurance can be levied at up to 15% through the FPLP — see can the IRS garnish SSDI.

- Military retirement is not VA disability. Retirement pay from DFAS carries no exemption and is fully levyable.

- Concurrent receipt splits the difference. If you draw both, the retirement portion is exposed while the service-connected disability portion stays protected.

The bank account gap: where VA disability money loses its protection

The §6334(a)(10) exemption protects the payment on its way to you — not the money after it lands in your account. Once deposited, VA funds become ordinary bank balances in the IRS's eyes, and a bank levy attaches to everything in the account on the day the levy hits, whatever its source.

Veterans are often surprised here because a different federal rule forces banks to automatically protect two months of directly deposited VA and Social Security benefits. That rule applies to garnishment orders from private creditors and states — it does not bind a federal tax levy. Against the IRS, deposited benefit money has no automatic shield.

You do get a window. Under the IRS bank levy 21-day rule, your bank freezes the funds but holds them for 21 days before remitting. During that hold you can contact the IRS, document that the frozen money is VA disability you need for rent, food, utilities, and medical costs, and request a hardship release under IRC §6343. Releases happen — but they require you to act inside the window, with proof in hand. That's why keeping your award letter and statements showing the VA deposit trail matters before any levy ever arrives.

What the IRS can take from a veteran who owes back taxes

The exemption covers one payment stream — everything else you earn or own follows normal collection rules. If you run a business or have other income, that's where enforcement actually lands. Self-employed veterans face a specific exposure: the IRS can send levies straight to your clients and payment processors, a one-shot grab covered in can the IRS garnish 1099 income. And if part of your income is W-2 wages, you can estimate what a wage levy would leave you with using our IRS wage garnishment calculator.

| Income or asset | Can the IRS take it? | How it happens |

|---|---|---|

| Service-connected VA disability payment | No — exempt at the source | IRC §6334(a)(10); no levy is served on the VA |

| Bank account funds (including deposited VA money) | Yes | Bank levy freezes the balance; 21-day hold, then funds go to the IRS |

| Self-employment income / accounts receivable | Yes | One-time levies served on clients and payment processors |

| Military retirement pay (DFAS) | Yes | Regular levy, or a continuous 15% FPLP cut |

| Social Security / SSDI | Yes, up to 15% | Federal Payment Levy Program |

| Federal and state tax refunds | Yes | Automatic offset; state refunds after a CP504 |

| Home, vehicles, other property | Lien: yes. Seizure: rare | Federal tax lien attaches to everything; home seizure requires court approval |

Two of those rows deserve their own reading if they apply to you: the lien question is covered in depth in can the IRS take my house, and retirement-account reach — which follows different rules than VA benefits — in can the IRS take my 401(k).

What happens if you ignore the debt — VA check or not

An exempt check does not stall the collection machine; the notice sequence runs on your balance, not your income source. Each stage arrives with more enforcement power than the last:

- CP14 — the first bill, with roughly 21 days to pay or arrange something before escalation.

- CP501 / CP503 — reminders. Still just bills, but penalties and interest compound the whole time.

- CP504 — intent to levy your state tax refund. A federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — final notice of intent to levy. A 30-day clock starts on your Collection Due Process rights; after it runs, bank levies and levies on your business receivables can begin.

- Enforcement — bank accounts, client payments, retirement pay, and refunds are all fair game. Your VA check keeps arriving untouched while everything around it gets squeezed.

- Passport certification — once your assessed balance passes $66,000 (the 2026 threshold), the IRS can certify the debt to the State Department, which can deny or revoke your passport. Details in passport revoked for tax debt.

One 2026 reality worth knowing: the IRS workforce shrank about 27% in 2025, so reaching a human is harder than ever — but these notices, liens, and levies are generated by automated systems that never went anywhere. Nobody has to look at your file for the machine to escalate it.

Owe back taxes on top of your VA disability?

An experienced tax professional will map exactly what's protected, what's exposed, and which resolution fits your numbers — free and confidential, before another month of penalties and interest stacks on.

Your options when you owe the IRS and receive VA disability

Every IRS resolution program is open to veterans — the exemption changes what the IRS can seize, not what you owe or how you can settle it. One rule surprises almost everyone: VA disability counts as household income on Form 433-F and in offer calculations, even though it's nontaxable and levy-exempt. A large benefit can raise your required monthly payment; a modest one paired with real expenses can support hardship status. The full do-it-yourself playbook lives in our guide on how to settle tax debt yourself — here's how the options line up:

| Option | Who qualifies | What it costs |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and 0.5%/month penalty continue |

| Streamlined installment agreement | Balance $50,000 or less (if you owe more, pay it down to $50,000 or below before applying) | No financial statement required; up to 72 months |

| Non-streamlined installment agreement | Balances over $50,000; Form 433-F financial disclosure | Payment set by ability to pay, VA income included |

| Currently Not Collectible | Allowable living expenses equal or exceed income | $0; collection pauses, interest accrues, refunds still offset |

| Offer in Compromise | Assets + future income can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) |

| Penalty abatement (FTA / AEP) | Clean compliance in the prior 3 years | Free; removes penalties, not the tax itself |

A worked example — clearly hypothetical. Say you're a sole proprietor drawing $2,400 a month in VA disability, and three years of unpaid self-employment tax left you owing $68,500. The failure-to-pay penalty alone is running $68,500 × 0.5% = about $342 a month until it caps at 25%, interest compounds daily on top, and — because $68,500 exceeds the $66,000 passport threshold — certification is already on the table. Your realistic paths:

- Pay down to streamlined. Put $18,501 toward the balance to reach $49,999, and a streamlined plan of up to 72 months becomes available: roughly $695 a month ($49,999 ÷ 72), with no detailed financial disclosure. See IRS payment plans over $50,000 for how the two tiers differ.

- Negotiate a non-streamlined plan. File Form 433-F showing all income — the $2,400 VA benefit included — against IRS allowable expenses. If the math leaves $800 a month of ability to pay, that's roughly where your payment lands, even though none of it can be forcibly taken from the VA check.

- Hardship or settlement. If your business income has collapsed and the VA benefit barely covers essentials, Currently Not Collectible status can pause enforcement — or, if the IRS's own math shows it could never collect $68,500 from you, an Offer in Compromise may resolve the debt for what it can collect. The IRS accepted roughly 1 in 5 offers in FY2024, so eligibility is genuinely means-tested, not marketing.

If your debt traces to a deployment period, one more door exists: combat-zone service suspends many IRS deadlines and collection actions — see combat zone IRS collection relief.

How to respond, step by step

- Confirm the balance — log into your IRS online account and pull transcripts to see exactly what you owe, for which years, and whether any returns are missing.

- Document your VA deposits — keep your award letter and bank statements showing which deposits are VA disability; if a bank levy ever hits, that proof supports a fast hardship release.

- File anything unfiled — the IRS won't approve a payment plan, hardship status, or an offer while returns are missing, and the failure-to-file penalty is ten times the late-payment penalty (though in months where both penalties apply, the failure-to-file portion drops to 4.5% — 5% combined).

- Pick your resolution — match your numbers to a payment plan, Currently Not Collectible status, or an Offer in Compromise using the options table above.

- Act on any final notice immediately — if an LT11 or Letter 1058 arrives, file Form 12153 within 30 days to pause levies while an appeals officer reviews your case.

When you can handle this yourself — and when help changes the outcome

Plenty of veterans resolve IRS debt without paying anyone. You can confidently go it alone if the balance is one you can clear within 180 days, if you agree with the amount and just need a simple online payment plan, or if your only fix is requesting first-time penalty abatement on an otherwise clean record. The IRS's own payment plans page handles those setups in one sitting, and the Taxpayer Advocate Service exists for cases where IRS processes themselves are causing you harm.

Experienced help earns its cost in specific situations: a bank levy already freezing VA funds with the 21-day clock running, multiple years of unfiled Schedule C returns behind the balance, offer-in-compromise math that mixes exempt VA income with fluctuating business income, or a revenue officer assigned to your account. In those cases, the order you fix things — returns first, penalties second, balance last — and how your 433-F presents the VA benefit can swing the outcome by thousands.

Terms you'll run into, decoded

- Levy vs. lien: a levy takes property (a bank balance, a client payment); a lien is a recorded legal claim against everything you own until the debt is resolved.

- IRC §6334(a)(10): the tax-code section listing property exempt from IRS levy — service-connected VA disability compensation is on the list.

- FPLP: the Federal Payment Levy Program, an automated continuous levy of up to 15% on federal payments like Social Security and military retirement — not service-connected VA disability.

- CDP rights: Collection Due Process — your right, after a final notice, to a 30-day window to demand an independent appeals hearing (Form 12153) before levies begin.

- CNC: Currently Not Collectible — hardship status that pauses collection when paying would leave you unable to cover basic living expenses.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause that clock.

VA disability and IRS debt: your questions, answered

Can the IRS garnish my VA disability payments?

No. Service-connected VA disability compensation is exempt from IRS levy under IRC §6334(a)(10), so the IRS cannot order the VA to withhold any part of your monthly check. The exemption applies automatically — you don't have to request it. It protects the payment stream only, though: money already deposited in a bank account, other income, and tax refunds can still be reached.

Can the IRS take VA disability money out of my bank account?

Yes, it can. Once your VA payment is deposited, it becomes ordinary bank funds, and an IRS bank levy attaches to the full balance. The bank holds levied funds for 21 days before sending them, which is your window to call the IRS, prove the money is VA disability you need for basic living expenses, and request a hardship release under IRC §6343.

Does the IRS count VA disability as income for a payment plan or Offer in Compromise?

Yes. Even though VA disability is nontaxable and exempt from levy, the IRS counts it as household income on Form 433-F and in the Offer in Compromise ability-to-pay calculation. That means a large VA benefit can raise your required monthly payment or your minimum offer amount, while a modest one paired with high allowable expenses can support hardship status instead.

Can the IRS take my military retirement pay?

Yes. Military retirement paid by DFAS is not covered by the VA disability exemption, and the IRS can levy it — including a continuous 15% cut through the Federal Payment Levy Program. Many veterans receive both retirement and VA disability; in that case the retirement portion is exposed while the service-connected disability portion stays protected at the source.

Do I have to pay taxes on VA disability benefits?

No. Service-connected VA disability compensation is excluded from gross income, so you don't report it on your tax return and it can't create a tax debt by itself. Back-tax balances for veterans almost always come from other income — self-employment earnings, retirement pay, investment or gig income — not from the VA benefit.

Will the IRS take my tax refund if I'm a disabled veteran?

Yes, if you owe back taxes. Any federal refund you generate from other income is offset against your balance automatically, and the IRS can also grab your state refund after a CP504 notice. Your disability rating doesn't prevent the offset; refunds are applied until the debt, penalties, and interest are paid.

Does a 100% permanent and total rating wipe out IRS debt?

No. There is no VA-rating-based forgiveness program; a 100% P&T rating changes nothing about the balance itself. What it often does change is collectibility: if VA compensation is most of your income, the IRS may agree you can't pay and place the account in Currently Not Collectible status, which pauses enforcement while interest continues to accrue.

Can the IRS put a lien on my house if my only income is VA disability?

Yes. A federal tax lien attaches to everything you own — including your home — regardless of where your income comes from, because a lien is a claim, not a seizure. Actually taking a primary residence requires court approval and is rare. If VA disability is your only income, hardship status can stop levies, but the lien can still be filed until the debt is resolved.

Your next 24 hours

- Find your real balance. Pull the most recent IRS letter you received, or log into your account at IRS.gov, and note the total owed and which tax years it covers — especially whether it's above or below the $50,000 and $66,000 lines.

- Gather three things. Your last filed tax return, your VA award letter with recent bank statements showing the deposits, and a rough picture of your business or other income.

- Get the free review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will confirm what's protected, what's exposed, and which option stops the monthly penalty-and-interest growth fastest.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.