Levies & Asset Seizure

Can the IRS Take My HSA? HSA Levy Exposure Explained (2025)

The short answer: yes — the IRS can take your HSA. A health savings account is property the IRS can levy to collect a tax debt, and it has no special federal protection like an ERISA pension. The good news: an HSA levy only happens after several warning notices, so you have time to act.

Worried the IRS is about to levy your HSA?

Send us a photo of your latest notice. An experienced tax professional will tell you exactly where you stand and what can stop a levy — free, confidential, no pressure.

⏱ Your deadline: the IRS cannot levy your HSA until it sends a Final Notice of Intent to Levy (LT11 or Letter 1058). That notice gives you 30 days to request a Collection Due Process hearing. Miss it, and the levy can be issued — file on time and you can usually stop it.

Why your HSA is exposed in the first place

People assume retirement and health accounts are off-limits. For private creditors — a credit card company, a hospital — that's often true. But the IRS plays by different rules. Under federal law, the IRS can levy almost any property or right to property you own, and your HSA balance counts.

An HSA is not an employer-sponsored ERISA plan. It belongs to you personally, like a savings or brokerage account. That makes it one of the easier targets for an IRS levy. The IRS lists the kinds of property it can reach on its levy overview page, and financial accounts are squarely on that list.

Here's the part that stings: when the IRS pulls money out of your HSA, that distribution is usually treated as a non-medical withdrawal. If you're under 65, that means income tax on the amount plus a 20% additional tax. So a levy can cost you more than just the dollars seized.

What happens if you ignore the warning notices

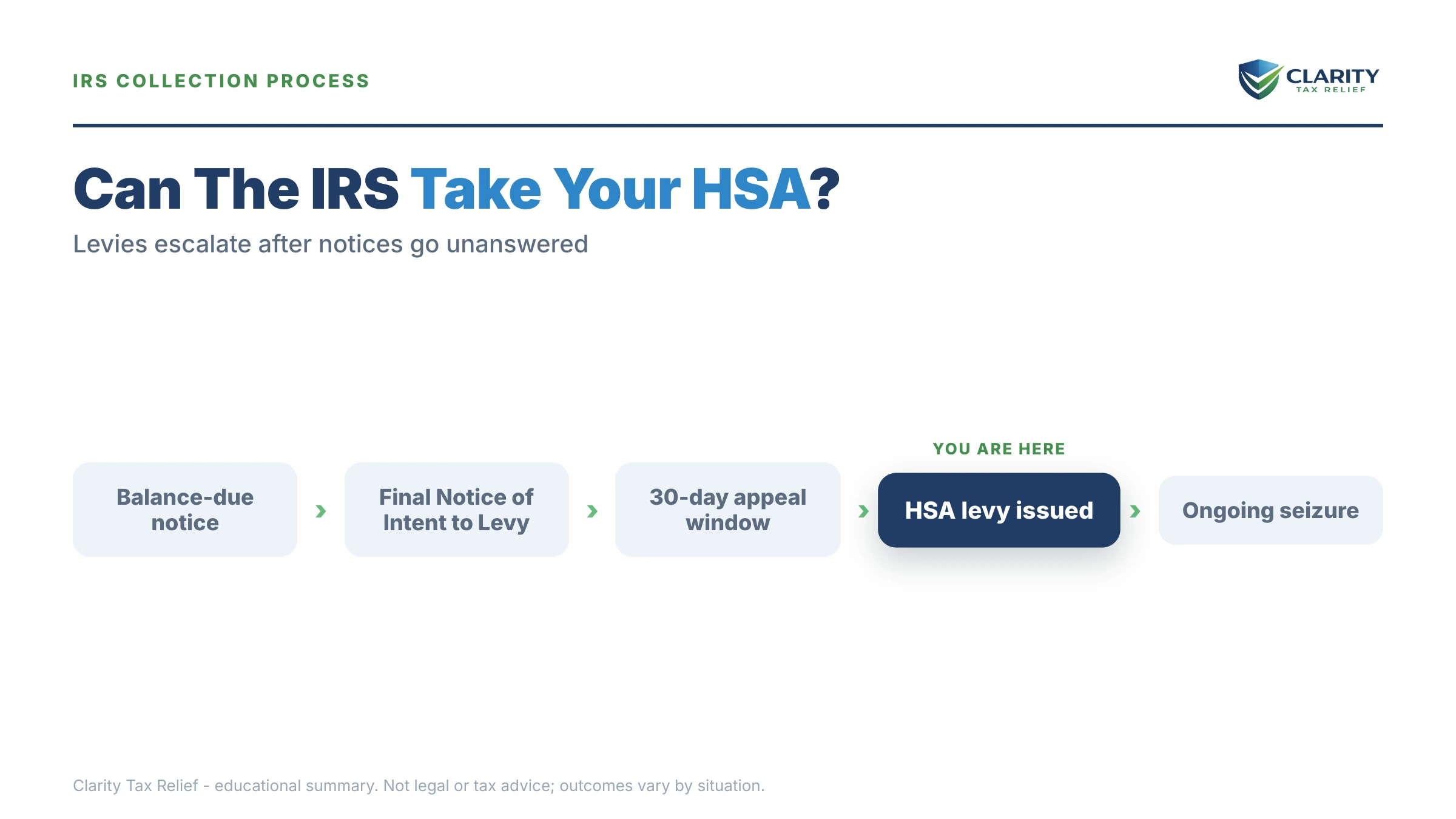

The IRS doesn't empty your HSA out of the blue. Collection is an automated sequence of mailed notices, each one more serious than the last. A levy only comes at the very end:

- CP14 — your first bill. No enforcement yet, just a balance due.

- CP501 / CP503 — reminder notices. The balance grows with penalties and interest.

- CP504 — Notice of Intent to Levy. The IRS can grab your state tax refund and a federal lien becomes likely.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. This is the one that matters. After 30 days, the IRS can levy bank accounts, wages, and your HSA.

The takeaway is simple: a levy is the last step, not the first. If you've been getting IRS mail and tossing it in a drawer, the LT11 notice is the line you do not want to cross without responding. Once that 30-day clock runs out, your appeal options shrink fast.

A worked example: what an HSA levy can really cost

Say you owe $9,000 in back taxes and ignore every notice. You have $6,000 sitting in your HSA. You're 40 years old.

- The IRS levies the full $6,000 and applies it to your balance.

- Because that money came out for a non-medical reason, it's now taxable income — adding roughly $1,320 in tax if you're in the 22% bracket.

- You also owe the 20% additional tax — another $1,200.

So a $6,000 levy created about $2,520 in new tax for next year — and you still owe $3,000 on the original debt. That's why letting it get to a levy is the most expensive path. Acting early is almost always cheaper.

How an HSA compares to other "protected" accounts

If you're worried about the IRS reaching your savings, you're probably wondering about your other accounts too. The honest answer: the IRS can reach nearly all of them, but timing and process differ. We cover the details in our guides on whether the IRS can take your 401(k) and whether the IRS can take your IRA. The short version is that an HSA sits at the more-exposed end of the spectrum, because it isn't an ERISA plan and behaves much like an ordinary bank account in a levy.

Your options to stop or prevent an HSA levy

The notice makes it feel like pay-or-else. In reality you have several ways to take a levy off the table. Which one fits depends on your finances:

- Installment agreement — a monthly payment plan. Once you have an active agreement, the IRS generally won't levy. See the IRS payment plans page; balances under about $50,000 often qualify for a streamlined plan with little paperwork.

- Currently Not Collectible status — if paying anything would create real hardship, the IRS can pause collection. Levies stop while you're in this status.

- Collection Due Process hearing — filing Form 12153 within the 30-day Final Notice window pauses collection and gets your case in front of an Appeals officer. Our Form 12153 CDP hearing guide walks through it.

- Offer in Compromise — settling for less than the full balance. It's real, but only when your assets and income genuinely can't cover the debt. Anyone promising to settle for "pennies on the dollar" before reviewing your finances is selling you something.

- Emergency levy release — if a levy has already hit and it's causing hardship, the IRS can release it. Our levy release for hardship guide explains how.

How to respond, step by step

- Read the notice and find the deadline. If it's an LT11 or Letter 1058, you have 30 days to request a hearing — mark that date.

- Verify the balance by logging into your IRS online account. Make sure the amount and tax years match your records.

- Pick a path before the deadline. A payment plan, hardship status, or a CDP hearing request all stop the levy clock.

- Don't drain the HSA yourself. Pulling the money out to pay the IRS can trigger the same tax and 20% penalty — talk to an experienced tax professional first.

- Get help if you owe over $10,000 or have unfiled years. The order you fix things in changes what you ultimately pay.

HSA levy questions, answered

Can the IRS take money out of my HSA?

Yes. A health savings account is property the IRS can levy to collect a tax debt. Unlike an ERISA pension, an HSA has no special federal shield from collection. If the IRS levies it, you can also owe income tax plus a 20% penalty on the amount pulled out for a non-medical purpose.

Will the IRS levy my HSA without warning?

Almost never. A levy on your HSA only comes after a series of mailed notices, ending with a Final Notice of Intent to Levy (LT11 or Letter 1058) that gives you 30 days to request a hearing. If you respond during that window, you can usually stop the levy before it happens.

Is my HSA protected from the IRS like a 401(k)?

No. A 401(k) is protected from most private creditors by federal ERISA rules, but even those protections don't stop the IRS. An HSA has even less protection — it is not an ERISA plan, so the IRS can reach it just like a regular bank or brokerage account.

Do I owe extra penalties if the IRS levies my HSA?

You can. Money pulled from an HSA for anything other than qualified medical expenses is normally taxable income, and if you're under 65 it also carries a 20% additional tax. An IRS levy can trigger that result, so a levy can cost you more than just the balance taken.

How do I stop the IRS from taking my HSA?

Act before the 30-day Final Notice deadline. Set up a payment plan, request Currently Not Collectible status if paying would cause hardship, file Form 12153 for a Collection Due Process hearing, or apply for an Offer in Compromise if you qualify. Any of these can pause or release a levy.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.