IRS Collections

Can the IRS Take My IRA? The Real Rules and How to Stop a Levy (2026)

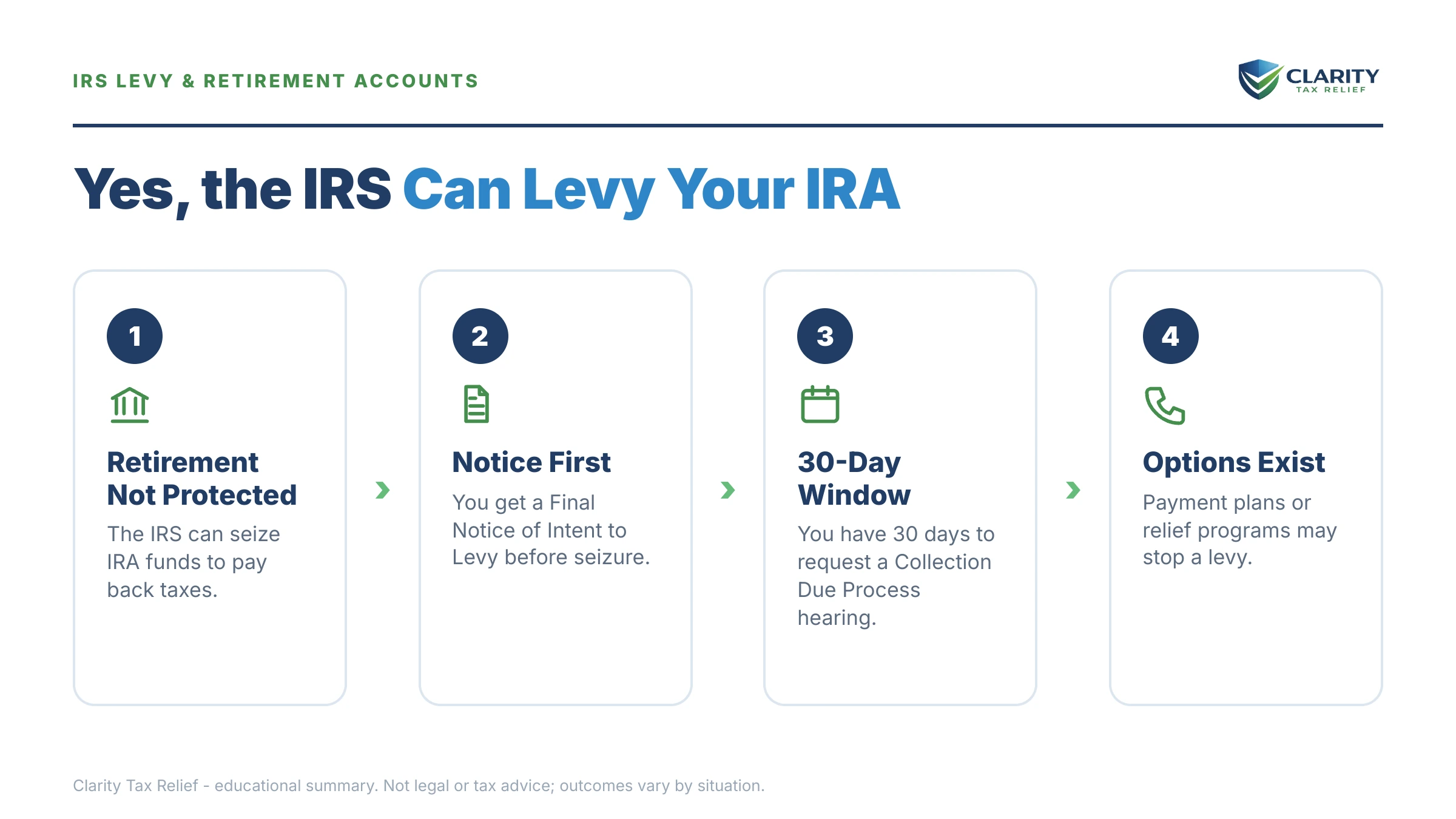

Can the IRS take my IRA? Yes. Traditional, Roth, SEP, and SIMPLE IRAs are not exempt from a federal tax levy, and state creditor protections don't stop the IRS. In practice, an IRA levy is a last resort requiring a manager's approval — and it's almost always preventable if you act before the final notice.

Maybe the divorce is final, the house and the debts are divided — and now the IRS says a balance from your married years is still yours to pay, while the IRA you spent two decades funding is the biggest asset left with only your name on it. That fear is rational, but the situation is far from hopeless: the law that lets the IRS reach an IRA also builds in warnings, hearings, and off-ramps at every stage.

This guide covers what almost every other page on this question skips: why your IRA is more exposed than a 401(k), the internal hurdle the IRS must clear before touching retirement money, and the exact math on why cashing out your own IRA to pay the debt is usually the most expensive move available.

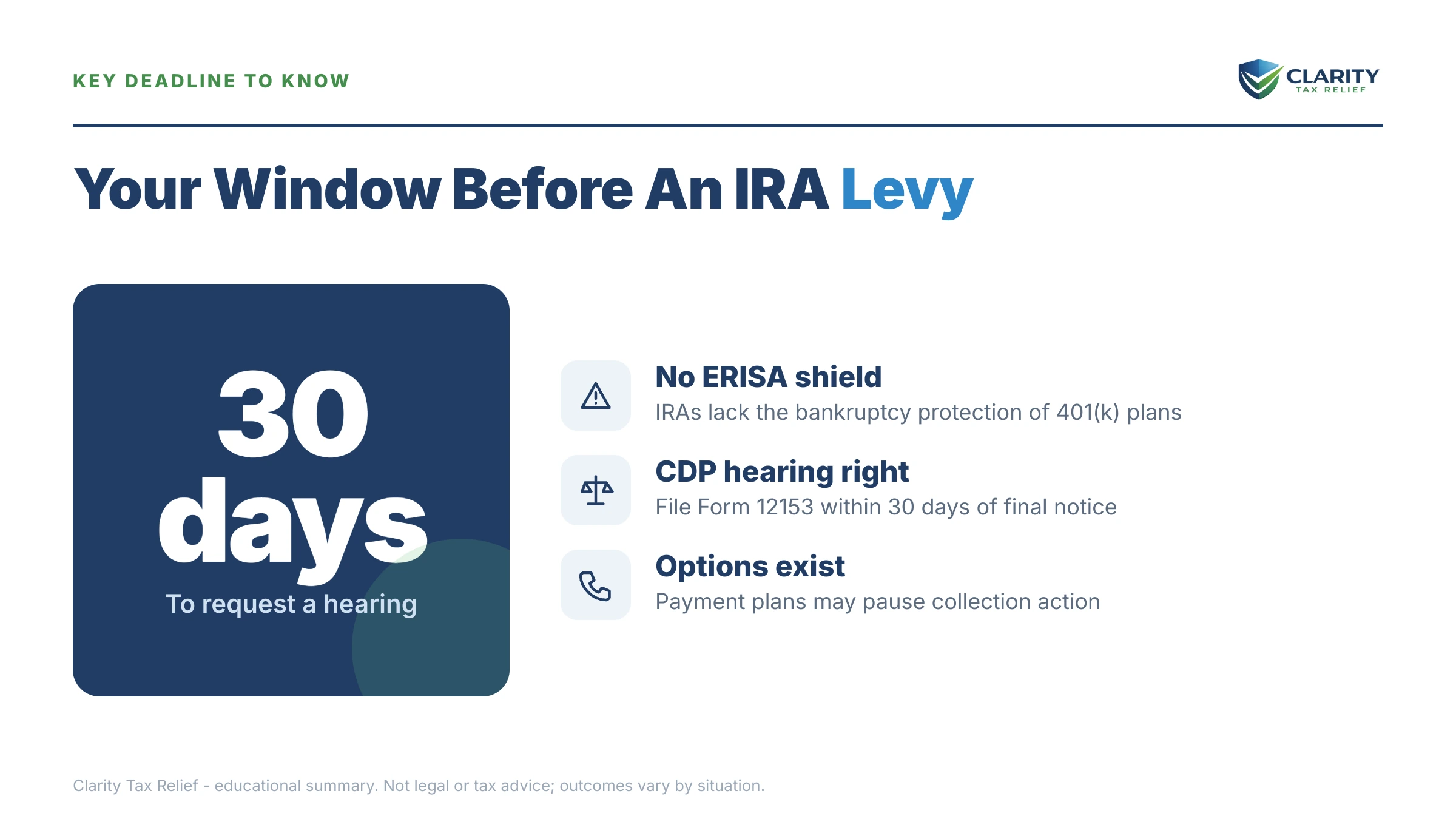

⏱ The one hard deadline: if you've received an LT11 or Letter 1058 — the final notice of intent to levy — you have 30 days from the date printed on it to request a Collection Due Process hearing with Form 12153. A timely request is the single strongest tool for keeping a levy away from your IRA. No fixed deadline applies before that notice, but interest and penalties accrue monthly while you wait.

Can the IRS take my IRA when other creditors can't? Yes — here's why

A federal tax levy overrides the creditor protections that make IRAs nearly untouchable in every other context. The tax code lists the property exempt from levy — items like workers' compensation, unemployment benefits, and certain minimal wages — and retirement accounts are not on that list. State exemption statutes and the shields IRAs enjoy in bankruptcy do not bind the federal government.

There's a second reason your IRA is exposed, and it's the key difference from an employer plan: the IRS can levy any right to property you have. Because an IRA owner can withdraw funds at any time (paying tax to do so), you have a present right to the full balance — so the IRS does too. A current-employer 401(k) you can't yet withdraw from is harder to reach, which is why the answer on our can the IRS take my 401(k) page reads differently than this one.

And if your balance traces to a jointly filed return, divorce didn't split it. Joint filers are each liable for 100% of the debt, and the IRS can collect the whole amount from whichever ex-spouse has reachable assets — often the one with the IRA. Your decree can order your ex to pay, but the IRS isn't a party to it; our guide on why the IRS ignores your divorce decree explains that gap, and separation of liability relief is the tool that can actually reassign the debt.

The one thing standing between the IRS and your IRA: the "flagrant conduct" hurdle

IRS procedures treat retirement accounts as a last-resort levy source, not a first target. Before an IRA levy is approved, internal rules require three things: other collection sources have been considered or exhausted, your conduct has been determined flagrant — think ignoring every notice, hiding assets, or repeatedly building new balances — and a manager signs off. The IRS is also supposed to weigh whether you depend on the account for necessary living expenses in retirement.

That hurdle is real protection, but it protects the people who engage — not the people who go silent. Someone who answers notices and gets on a plan almost never sees an IRA levy. Someone who lets the automated system run to the end is exactly who the exception exists for. Meanwhile, the federal tax lien attaches to your IRA automatically once tax is assessed and the demand for payment goes unpaid, even if no levy ever happens — the same lien reach we cover in can the IRS take my house.

Which retirement accounts can the IRS levy?

The IRS can reach nearly every kind of retirement account, but how easily — and how much — varies by account type. The image below shows how this comparison looks at a glance and where your account fits.

| Account type | Can the IRS levy it? | What determines exposure |

|---|---|---|

| Traditional IRA | Yes — full vested balance | You can withdraw at any time, so the IRS can too; income tax applies to a levied distribution |

| Roth IRA | Yes | Same reach; contributions come out tax-free, non-qualified earnings may be taxed |

| SEP / SIMPLE IRA | Yes | Treated like other IRAs — common exposure for self-employed filers with SE-tax debt |

| 401(k) — current employer | Only your present right to withdraw | If plan rules block withdrawal, the IRS generally waits — see the 401(k) rules |

| Pension in pay status | Yes — payments can be levied | Covered in can the IRS take my pension |

| Inherited IRA | Yes — it's your asset once inherited | Inherited money broadly is reachable — see can the IRS take an inheritance |

What happens if you ignore the debt: the road to an IRA levy

No IRA levy happens without a written sequence of warnings first — the IRS must send a final notice and give you 30 days to respond before levying any asset. Here is the order the escalation runs in, from first bill to retirement account:

- CP14 — the first bill. No enforcement power yet; the cheapest moment to fix everything.

- CP501 / CP503 — reminder notices while penalties and interest compound monthly.

- CP504 — Notice of Intent to Levy. The IRS can seize your state tax refund, and the federal tax lien — which already attaches to your IRA — may be publicly filed.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts on your Collection Due Process rights (Form 12153). Miss it and the IRS may levy without further warning — see our LT11 guide.

- Levy on ordinary sources first — bank accounts (with a 21-day hold before funds leave), wages (continuous until released), and state refunds. These are the routine targets.

- Retirement accounts — only after other sources are considered, a flagrant-conduct determination is made, and a manager approves. Rare, but it happens to taxpayers who ignore everything above.

One 2026-specific note: IRS staffing fell roughly 27% in 2025, so reaching a human is harder than ever — but these notices and levies come from automated systems that never stopped running. Silence from the IRS is not the same as safety. For the full picture of every stage, see the IRS collection process, step by step.

Worried the IRS is getting close to your retirement savings?

Send us your latest notice. An experienced tax professional will tell you exactly where you sit in the levy sequence and which option protects your IRA — free and confidential. If an LT11 has arrived, the 30-day hearing window is already running, so don't sit on it.

Should you cash out your IRA to pay the IRS? Run this math first

Voluntarily cashing out an IRA to pay tax debt usually costs far more than the debt itself. Here's the trap: money the IRS levies from an IRA is exempt from the 10% early-withdrawal penalty — but money you withdraw to pay the IRS is not. Under 59½, a voluntary withdrawal gets hit with ordinary income tax plus the full 10% penalty.

Say you owe $19,700 after a divorce, you're 45, and you're in the 22% bracket, with $60,000 sitting in a traditional IRA. Compare three paths:

- Cash out voluntarily. To net $19,700 after 22% income tax and the 10% penalty (32% combined), you'd need to withdraw roughly $19,700 ÷ 0.68 ≈ $28,970. Nearly half your retirement account gone to clear a $19,700 debt — and the extra income could even push you into a higher bracket.

- Let a levy happen. The 10% penalty is waived on levied amounts, but 22% income tax on $19,700 still creates a new bill of about $4,334 the following April — a fresh debt starting the cycle over, with your savings gone.

- Set up a payment plan. At $19,700 you're under the $25,000 streamlined threshold: an online 72-month agreement runs roughly $19,700 ÷ 72 ≈ $274 a month before interest and the 0.5% monthly late-payment penalty (expect a somewhat higher actual payment to cover accruals). Your IRA stays invested and untouched.

This is hypothetical, but the shape holds at almost any balance: the payment plan preserves the retirement money, and the voluntary cash-out is the worst of the three. Pay off the plan early and you cut the interest further.

Your options to keep the IRS out of your IRA

An account in an active resolution is not a levy target — the "flagrant conduct" standard exists precisely to separate people who engage from people who don't. These are the real programs, with their thresholds (the shared background on each lives in our guide to how to settle tax debt yourself):

| Option | Who qualifies | What it does for your IRA |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days; $0 setup fee | Halts the escalation sequence immediately; interest still accrues |

| Guaranteed installment agreement | Individuals only who owe $10,000 or less in income tax (excluding penalties and interest), with all returns filed, timely filing and payment for the past 5 years with no installment agreement in that period, and full payment within 3 years | The IRS must accept it — enforcement stops while you pay |

| Streamlined installment agreement | ≤ $25,000 online (≤ $50,000 with direct debit), up to 72 months | No financial disclosure of your IRA required; no levy while current |

| Currently Not Collectible | Paying anything would prevent basic living expenses (financial statement required) | Collection pauses; the debt and lien remain, but no levy while in CNC |

| Offer in Compromise | Assets + future income genuinely can't cover the debt; $205 fee, 20% down on lump-sum offers (both waived with low-income certification) | Settles the debt for what the IRS could realistically collect — but your IRA counts as an asset in that math |

One honest caution on the Offer in Compromise: the IRS accepted roughly 1 in 5 offers in FY2024, and your IRA counts toward your "reasonable collection potential." If your IRA balance alone could pay the debt — like the $60,000 account against a $19,700 balance above — a collectibility-based offer will almost certainly be rejected. A payment plan or, in true hardship, CNC is usually the realistic path for IRA owners. Also worth knowing: the IRS generally has 10 years from assessment to collect (paused by appeals, offers, or bankruptcy) — you can estimate your own expiration dates with our CSED Calculator.

How to respond, step by step

- Find your place in the notice sequence. Pull your most recent IRS letter and check its number — a CP14 or CP503 means you have time; a CP504 or LT11 means the clock is short. Confirm the balance in your IRS online account.

- File Form 12153 if you're holding an LT11 or Letter 1058. Request a Collection Due Process hearing within 30 days of the date on the final notice — a timely request generally pauses levy action while your case is heard.

- Get into an agreement before enforcement starts. Set up a payment plan, request hardship status, or submit an offer — a balance under $50,000 can usually go on a plan online, and an account in an active agreement is not a levy target.

- Leave the IRA alone until you've run the math. Do not voluntarily cash out to pay the IRS before comparing the withdrawal's tax and penalty cost against a monthly plan — a voluntary early withdrawal usually costs far more.

- Sort out joint liability if the debt is from your marriage. If the balance comes from jointly filed years, evaluate separation of liability or innocent spouse relief so you aren't defending your IRA against a debt your ex created.

When you can handle this yourself — and when help changes the outcome

Most people asking this question can protect their IRA without hiring anyone. If your balance is under $25,000, your returns are filed, and you're still in the CP14-through-CP504 stage, setting up a streamlined plan online takes about 20 minutes and ends the levy risk. If you can pay in full within 180 days, the short-term plan costs nothing to set up.

Experienced help earns its cost in a narrower set of situations: an LT11 has arrived and the 30-day CDP window is running; a levy notice has already reached your IRA custodian; the debt comes from joint years and you're building a separation-of-liability or innocent spouse case against an ex who won't cooperate; or you have multiple unfiled years that must be resolved before the IRS will approve any agreement. In those cases, sequencing — returns first, penalty relief second, resolution third — materially changes what you pay and what you keep.

Terms you'll see, decoded

- Levy — the actual seizure of your property (money, wages, accounts) to pay tax debt.

- Lien — the government's legal claim against everything you own, including your IRA; it attaches automatically when an assessed balance goes unpaid, even with no levy.

- Flagrant conduct — the IRS's internal standard for levying retirement accounts: behavior like ignoring all notices, hiding assets, or repeatedly running up new balances.

- Collection Due Process (CDP) — your right, after a final levy notice, to a hearing before enforcement; requested on Form 12153 within 30 days.

- CSED — the Collection Statute Expiration Date; the IRS generally gets 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

Can the IRS take my IRA — your questions answered

Can the IRS take my entire IRA?

Legally, yes — there is no dollar-amount exemption protecting retirement accounts from a federal tax levy, so a levy can reach your full vested balance. In practice, IRS procedures treat retirement accounts as a last resort: a manager must approve the levy and determine your conduct was flagrant. If the levy would leave you unable to cover basic living expenses in retirement, that is an argument for releasing or limiting it — raise it immediately, in writing.

Do I pay the 10% early-withdrawal penalty if the IRS levies my IRA?

No. The tax code specifically exempts amounts distributed because of an IRS levy from the 10% early-withdrawal penalty, even if you are under 59½. You still owe ordinary income tax on a levied traditional IRA distribution, which creates a new balance the following April. If you voluntarily withdraw money to pay the IRS, the exemption does not apply — a voluntary withdrawal before 59½ generally triggers the full 10% penalty on top of income tax.

Can the IRS take a Roth IRA?

Yes — Roth IRAs have no special protection from a federal tax levy. The tax hit is smaller, though: your original Roth contributions come out tax-free, and only earnings may be taxable if the distribution isn't qualified. That makes a Roth marginally less painful to lose, but the retirement money is still gone — the same prevention steps apply.

Will the IRS seize my IRA without warning?

Almost never. Before levying any asset, the IRS must send a final notice of intent to levy — an LT11 or Letter 1058 — and give you 30 days to request a Collection Due Process hearing. The rare exception is a jeopardy levy, used when the IRS believes collection is at immediate risk; for an ordinary back-tax balance, you will see multiple notices first.

Can the IRS take my IRA for my ex-spouse's tax debt?

If the debt comes from a jointly filed return, it isn't just your ex's debt — you are each fully liable for the whole amount, and the IRS can collect from either of you regardless of what the divorce decree says. Your IRA is exposed for joint-year balances. Separation of liability and innocent spouse relief can shift the debt to the spouse who caused it, but you must apply — it doesn't happen automatically.

How often does the IRS actually levy IRAs?

Rarely. IRA levies sit at the very end of the collection playbook — internal procedures require exhausting other collection sources, a determination of flagrant conduct, and managerial sign-off. But rare doesn't mean protected: the federal tax lien attaches to your IRA automatically once a balance is assessed and a demand goes unpaid, and taxpayers who ignore every notice are exactly who the exception is used on.

Can I protect my IRA by moving or rolling over the money?

No — and trying can make things worse. The federal tax lien follows the funds, and moving assets to dodge collection can be treated as a dissipated asset if you later apply for an Offer in Compromise, inflating what the IRS expects you to pay. A rollover to another custodian changes nothing about the IRS's reach. The only real protection is resolving the balance.

Does state law or bankruptcy protection stop an IRS levy on my IRA?

No. State creditor-exemption statutes and the protections IRAs enjoy in bankruptcy do not bind the federal government — a federal tax levy overrides them. This surprises many people, because IRAs are famously hard for private creditors to touch. Against the IRS, the account's only practical defenses are the notice-and-hearing process and getting into a resolution before a levy is approved.

Your next 24 hours

- Find your most recent IRS notice and check the letter number in the top corner. If it's an LT11 or Letter 1058, circle the date — your 30-day hearing window runs from that date, not from when you opened it.

- Gather three things: your last filed return, your latest IRA statement, and — if the debt is from married years — your divorce decree and the joint returns involved.

- Get a free case review at the 2-minute form or by calling (888) 825-7779. We'll map your place in the levy sequence and the specific option that keeps the IRS out of your retirement account — before interest and penalties add another month to the balance.

Primary sources: the IRS explains payment options at IRS.gov/payments and plan thresholds at the IRS payment plans page. If a levy is causing immediate hardship and you can't get traction with the IRS, the independent Taxpayer Advocate Service can intervene.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.