IRS Collections

Can the IRS Take My Pension? What's Actually at Risk in 2026

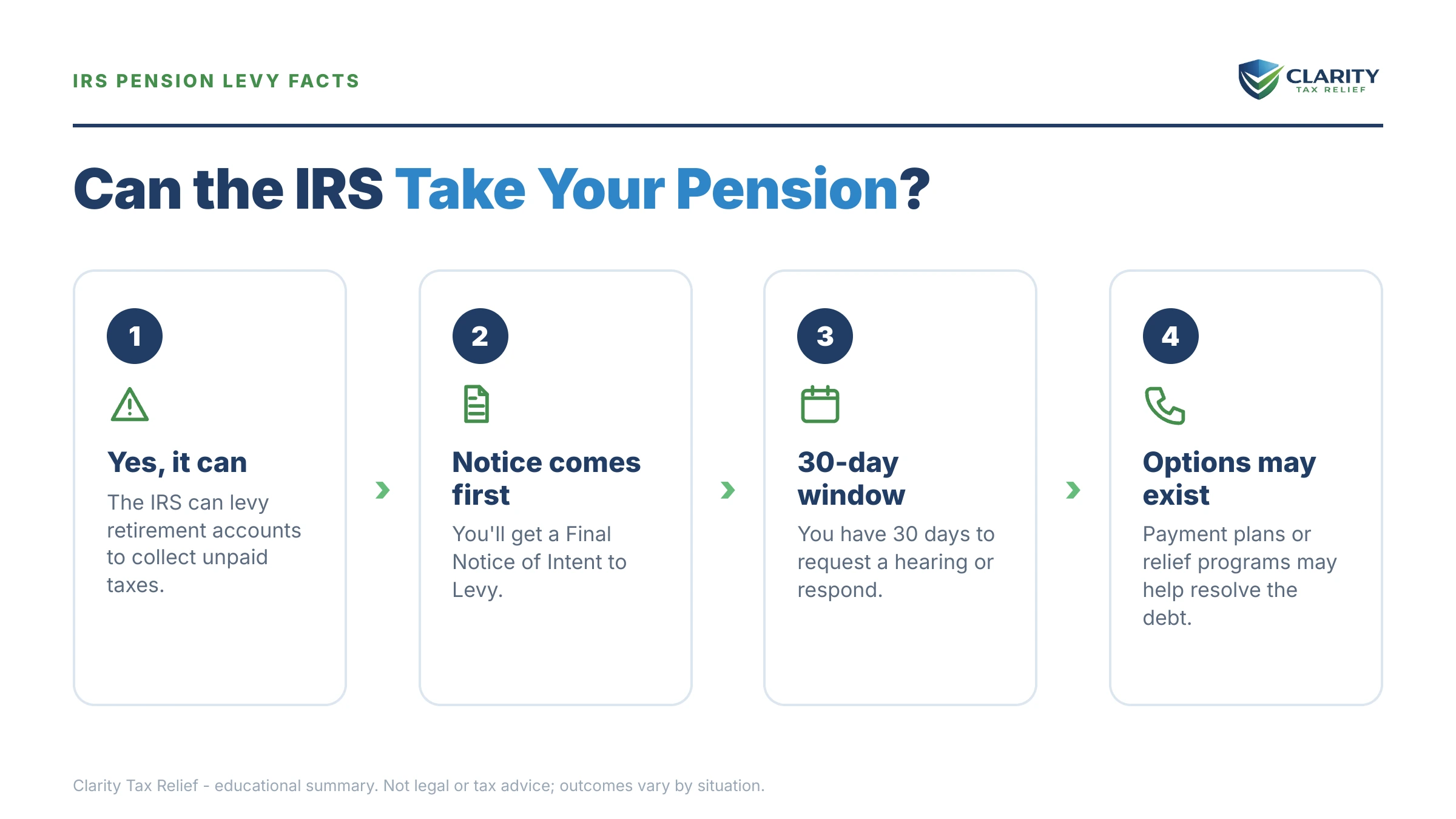

The short answer: yes, the IRS can take your pension. ERISA's creditor protections do not stop a federal tax levy, and monthly pension payments can be levied continuously, like wages. But the IRS must first send a final notice — an LT11 or Letter 1058 — and wait 30 days, and retirement levies are treated internally as a last resort.

You spent decades earning that pension, and now a tax balance from your working years — or from the business you still run — has you wondering whether the check you live on can be intercepted. That fear is reasonable, but the situation has more guardrails than the notices suggest. There is a required warning, a 30-day window, an appeal right, and several ways to take your pension off the table entirely. Here's the map.

⏱ The clock that matters: the IRS cannot levy your pension until it sends a final notice of intent to levy — an LT11 or Letter 1058 — and 30 days pass. If one of those letters is in your stack of mail, the date printed on it controls everything. If you haven't received one, no pension levy is imminent — but penalties and interest are still accruing every month.

Can the IRS take my pension? How far the levy actually reaches

The IRS can levy your pension because federal tax levies are an express exception to ERISA's anti-alienation protection. The rule that makes your pension untouchable to a credit card company or a lawsuit judgment simply does not apply to the U.S. Treasury. What changes the answer is not whether the IRS can reach retirement money — it's which kind of pension money you have.

If your pension is already paying you monthly, the income stream is the exposure. The IRS levies pension payments using the same mechanics as a wage levy (Form 668-W), and the levy is continuous — it attaches once and keeps taking from every future payment until released. A portion of each check is exempt based on your filing status and dependents, using the tables in IRS Publication 1494. You can estimate how much of a monthly payment a continuous levy could reach with our IRS Wage Garnishment Calculator.

If your pension hasn't started paying yet, the IRS "steps into your shoes." It can only reach what you have a present right to take. If your plan won't let you withdraw anything until age 65, the IRS generally has to wait for that date too. If the plan offers you a lump-sum option, the IRS can reach what you could elect — but seizing retirement assets requires extra managerial approval inside the IRS, and internal procedures reserve it for taxpayers whose conduct the agency considers flagrant, such as continuing to fund retirement while deliberately not paying assessed tax.

Federal pensions are the exception to "levies need a human." Civil-service annuities and military retirement pay can be hit automatically through the Federal Payment Levy Program at up to 15% of each payment — the same automated program that reaches Social Security. If you're weighing which retirement assets are exposed, the rules differ enough that each deserves its own read: see can the IRS take my 401k and can the IRS take my IRA, which follow account-seizure rules rather than income-stream rules.

| Pension source | Can the IRS reach it? | How it happens |

|---|---|---|

| Private pension, in pay status | Yes | Continuous levy on monthly payments; a Publication 1494 exempt amount is protected |

| Private pension, not yet payable | Only what you could take today | IRS steps into your shoes; can't force access you don't have; asset seizure needs extra approval |

| Federal civil-service or military retirement | Yes | Automated 15% continuous levy through the Federal Payment Levy Program |

| Social Security retirement | Yes, up to 15% | Same automated program — see can the IRS garnish Social Security |

| 401(k) / IRA balances | Yes, with stricter internal limits | Account-seizure rules, not income-stream rules; last-resort policy applies |

Why the IRS is looking at your retirement income

A pension levy is never the first move — it's the end of an automated sequence that started with an unpaid assessment. For a lot of readers of this page, the debt came from self-employment: quarterly estimates that got skipped in a slow year, self-employment tax that stacked up on top of income tax, or a return filed years late once the business stabilized. The balance got assessed, the first bill went out, and every notice since has been the machine escalating on schedule.

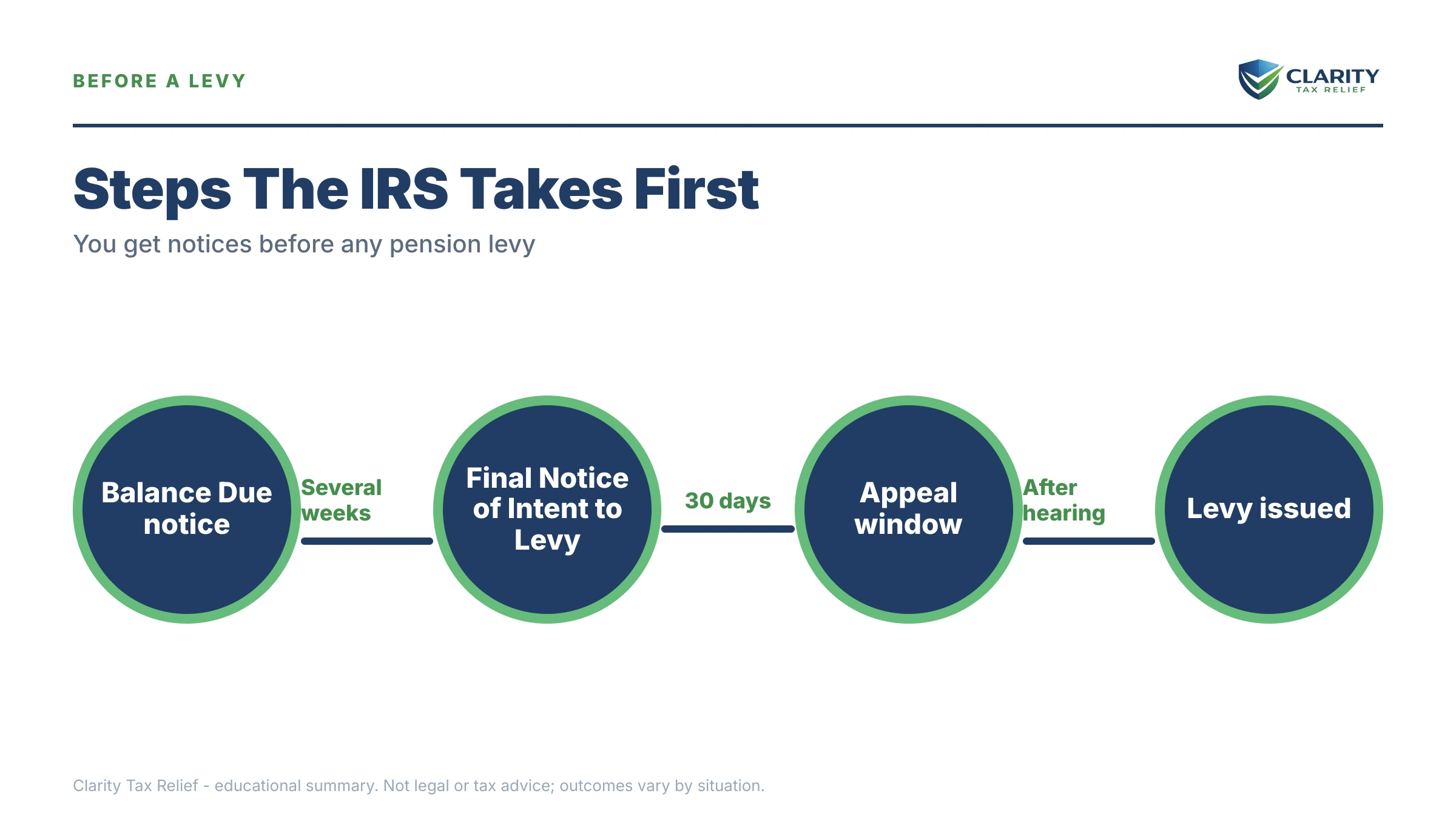

The IRS does not need to sue you, get a judgment, or prove anything in court before levying. The assessment itself is the legal foundation. What it must do is follow the notice sequence and honor your appeal window — which is exactly where your leverage lives.

What happens if you ignore the notices

Ignoring IRS collection notices produces a predictable escalation, and pension income sits near the end of it. The sequence runs in stages, each with more enforcement power than the last:

- CP14, then CP501/CP503 — bills and reminders. No enforcement yet, but failure-to-pay penalties and daily-compounding interest are growing the balance.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now seize your state tax refund. This is serious, but it is not the notice that authorizes a pension levy.

- LT11 or Letter 1058 — the Final Notice of Intent to Levy. This starts the 30-day clock and your Collection Due Process rights. After 30 days with no response, the IRS can levy bank accounts, wages, contractor pay — and pension income.

- Levy stage — a bank levy freezes funds for 21 days before they're sent to the IRS; a pension or wage levy is continuous, taking from every payment until released. Federal pensions can be pulled into the automated 15% program.

One 2026 reality worth naming: per TIGTA reports, the IRS workforce shrank roughly 27% in 2025, so reaching a human to fix things takes longer than ever — but the levy systems are automated and never stopped running. The machine escalates on schedule whether or not anyone answers the phone, which makes acting inside your window more valuable, not less.

| Notice or event | Your window | The right at stake |

|---|---|---|

| CP504 (intent to levy) | Pay-by date on the notice | State refund can be taken after it; last stage before the final notice |

| LT11 / Letter 1058 (final notice) | 30 days from the notice date | File Form 12153 for a CDP hearing; miss it and you lose the path to Tax Court review |

| Bank levy issued | 21-day hold before funds leave | Last chance to negotiate a release before the money is gone |

| Pension or wage levy attached | No hold period — continuous | Only a release (hardship, payment plan, CNC) stops it; it never expires on its own |

Worried a levy is coming for your retirement income?

If an LT11 or Letter 1058 is sitting in your mail, the 30-day window on it is real — and it's the single best moment to protect your pension. An experienced tax professional will review your notices free and tell you exactly where you stand.

Your options for taking your pension off the table

Any active resolution with the IRS stops the path to a pension levy — the levy is a collection tool of last resort, and it goes away when collection has a working plan. The full DIY playbook for each program lives in our guide to how to settle tax debt yourself; here's how each option maps to a pension-levy threat specifically:

| Option | Who qualifies | What it does for your pension |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days; $0 setup fee | Stops enforcement immediately; interest and penalties still accrue |

| Streamlined installment agreement | Balance ≤ $50,000; up to 72 months, set up online | No levy while the agreement is current; no financial disclosure needed at this level |

| Guaranteed installment agreement | Balance ≤ $10,000 plus compliance conditions | IRS must accept if you meet the criteria |

| Currently Not Collectible | Paying would prevent basic living expenses (proven on Form 433-F) | Collection pauses; existing levies can be released for hardship under §6343 |

| Offer in Compromise | Assets + future income genuinely can't cover the debt; $205 fee, 20% down on lump-sum offers (both waived with low-income certification) | Levy action generally holds while a processable offer is pending; per IRS data, roughly 1 in 5 offers were accepted in FY2024 |

| Penalty abatement (FTA / AEP) | Clean compliance for the prior 3 years; a new automatic exemption (AEP) begins rolling out summer 2026 | Shrinks the balance driving the levy; doesn't stop collection by itself |

Two eligibility notes matter for pension-age readers. First, your pension income counts in the IRS's collection math — an Offer in Compromise gets measured against what the IRS could collect from your assets and future income, and steady pension payments raise that number. Second, if your only income is a modest pension or Social Security and your expenses consume it, Currently Not Collectible status is often the realistic fit — the debt remains and the 10-year collection statute keeps running, but levies stop. Retirees weighing these trade-offs will find the fuller picture in our guide for people who are retired and owe back taxes.

What a $19,700 debt looks like next to a pension: the math

Say you owe $19,700 — a self-employed sole proprietor, 63, drawing a $2,600 monthly pension while still running a small Schedule C business. This is a hypothetical, but the arithmetic is real:

The payment-plan path: $19,700 is well under the $50,000 streamlined ceiling for setting up a 72-month agreement online with no financial disclosure — and because it's below $25,000, direct debit isn't even required to avoid a lien filing. The floor payment is $19,700 ÷ 72 ≈ $274 a month — though interest and the 0.5%-per-month failure-to-pay penalty keep accruing, so paying $350–$400 a month retires the debt faster and cheaper. Details on setup are in our walkthrough of the IRS payment plan online.

The do-nothing path: a continuous levy on the $2,600 pension would leave only the Publication 1494 exempt amount — typically far less than $2,600 — and take the rest of every payment until $19,700 plus growing penalties and interest is collected. The same balance ends up paid either way; the levy path just removes your control over the monthly amount and your budget with it.

The OIC question: with $2,600 in monthly pension income plus business income, the IRS's collection-potential math would likely show it can collect the full $19,700 over time, making an offer a poor fit here. An OIC becomes realistic when income barely covers allowable expenses and there are no reachable assets — not simply because paying is painful.

How to respond if your pension is at risk, step by step

- Find the last notice the IRS sent you — if it's an LT11 or Letter 1058, the date printed on it starts your 30-day window to preserve appeal rights.

- Confirm your balance and years owed — log into your IRS online account and match the total against the notice before deciding anything.

- Preserve your appeal rights — if you're inside the 30-day window, file Form 12153 to request a Collection Due Process hearing; levy action generally pauses while it's pending.

- Set up a resolution before a levy attaches — a payment plan, hardship status, or an Offer in Compromise takes levy off the table; balances under $50,000 can usually be resolved online.

- Get help fast if a levy is already running — releases move quickest when complete financials on Form 433-F are presented correctly the first time.

When you can handle this yourself — and when help changes the outcome

Most people who owe under $50,000 and haven't yet received a final notice can protect their pension without hiring anyone. If your balance is accurate, your returns are filed, and you can afford a monthly payment, setting up a streamlined agreement directly at the IRS payment plans page takes under an hour and immediately closes the door on levy action. Same if you can pay in full within 180 days — the short-term plan costs nothing to set up.

Experienced help earns its cost in a narrower set of situations: a levy is already taking your pension and you need a hardship release built on airtight financials; you have multiple unfiled years that must be resolved before the IRS will agree to anything; the debt includes business or payroll tax alongside the personal balance; or you're inside a 30-day CDP window and the hearing is your one shot at Tax Court review. In those cases, the order and packaging of what you present genuinely changes what you pay — and mistakes are expensive to unwind. If you're not sure which side of that line you're on, the free option is the Taxpayer Advocate Service for hardship cases, and our review at (888) 825-7779 for everything else.

Terms on your notices, decoded

- Levy — the actual seizure of money or property to pay a tax debt; a lien is only the legal claim, a levy is the taking.

- ERISA anti-alienation — the federal rule that shields most pensions from private creditors; federal tax levies are an express exception.

- Form 668-W — the levy form the IRS sends to an employer or pension payer to attach wages, salary, or retirement income continuously.

- FPLP — the Federal Payment Levy Program, an automated system that takes up to 15% of federal payments, including federal retirement annuities and Social Security.

- CDP rights — Collection Due Process: your right, after a final notice, to a hearing (requested on Form 12153 within 30 days) before levy action proceeds.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

Can the IRS take my pension: your questions answered

Can the IRS take my entire pension check?

Rarely the whole thing. When the IRS levies pension income, it uses the same mechanics as a wage levy, and a portion of each payment is exempt based on your filing status and dependents (the tables in IRS Publication 1494). Everything above that exempt amount goes to the IRS until the levy is released — and the exempt amount is usually far less than your actual bills. If the levy leaves you unable to cover basic living expenses, you can request a hardship release under IRC §6343.

Can the IRS take my pension if I haven't started collecting it yet?

Only to the extent you could reach it yourself. The IRS steps into your shoes: if your plan gives you no present right to withdraw, the IRS generally has to wait until payments begin. If you have a lump-sum or early-withdrawal option, the IRS can reach what you could take — but seizing retirement assets requires extra internal approval and is generally reserved for cases the IRS considers flagrant.

Does ERISA protect my pension from the IRS?

No. ERISA's anti-alienation clause blocks private creditors — a credit card company or lawsuit judgment usually can't touch your pension. Federal tax levies are an express exception to that protection. That's why the answer for the IRS is different from the answer for every other creditor, and why 'my pension is judgment-proof' is a dangerous assumption in a tax case.

Can the IRS take my federal or military pension?

Yes, and it can happen automatically. Federal retirement payments — including civil-service annuities and military retirement pay — can be levied through the Federal Payment Levy Program at up to 15% of each payment, continuously, without a revenue officer ever touching your file. Social Security retirement benefits are subject to the same 15% program. The levy continues until the debt is resolved or the levy is released.

Will I owe the 10% early-withdrawal penalty if the IRS levies my retirement account?

No. Distributions taken because of an IRS levy are exempt from the 10% additional tax on early withdrawals under IRC §72(t). But the levied amount is still ordinary taxable income in the year it comes out — which can create a brand-new balance due on next year's return if you don't plan for it.

How much warning do I get before the IRS levies my pension?

Several notices, ending with one that matters most. Before levying pension income, the IRS must send a final notice of intent to levy — usually an LT11 or Letter 1058 — and then wait 30 days. Filing Form 12153 within that window requests a Collection Due Process hearing, which generally pauses levy action while your case is heard. Federal payments in the automated 15% program get a CP90 or CP297-series warning first.

Can I stop a pension levy after it has already started?

Yes. A pension levy is continuous, so it never ends on its own — but the IRS releases levies when you enter an installment agreement, when your account is placed in Currently Not Collectible status, or when the levy creates economic hardship under IRC §6343. A pending Offer in Compromise also generally holds off new levy action. The fastest releases come from presenting complete, accurate financials, not from waiting.

Your next 24 hours

- Sort your IRS mail and find the newest letter. Look at the top-right corner for the notice number — if it says LT11 or Letter 1058, circle the date on it; your 30-day window runs from that date, not from when you opened it.

- Gather three things: your most recent tax return, every IRS notice you've received, and a one-page summary of your monthly income (pension, Social Security, business) and basic expenses. Every resolution path starts with these.

- Get your situation reviewed free. Call (888) 825-7779 or use the 2-minute form — if you're inside a 30-day final-notice window, say so first, because preserving that hearing right is the move that protects your pension. No final notice yet? The balance is still growing monthly, and the review costs nothing either way. You can also pay or set up a plan directly at IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.