Levies & Seizures

Can the IRS Take My Business? Levy and Seizure of a Going Concern (2025)

The short answer: can the IRS take my business? Yes — the IRS can levy your business bank accounts and seize and sell business assets to pay a tax debt. But seizing a working business is rare and a true last resort. It happens only after years of unpaid taxes, ignored notices, and a deliberate decision by IRS managers.

Worried the IRS is about to take your business?

Send us a photo of your notice. An experienced tax professional will tell you exactly where you stand, what your deadline really is, and which options can stop a levy — free, confidential, and no pressure.

⏱ Your deadline: if you've received a Final Notice of Intent to Levy (LT11 or Letter 1058), you have 30 days to act before the IRS can legally levy accounts and seize assets. Filing a Collection Due Process appeal within those 30 days pauses enforcement. After a bank levy, the bank holds the funds for 21 days — another window to get a release.

Why the IRS is coming after your business

The IRS doesn't seize a business because someone is angry. It happens because an automated collection system kept escalating an unpaid debt while no one responded. The most common reasons a business ends up on the IRS's radar:

- Unpaid payroll taxes. This is the number-one trigger. When you withhold income tax, Social Security, and Medicare from employee paychecks, that money is held "in trust" for the government — it was never yours. Falling behind on these 941 back taxes is treated far more seriously than any other business debt.

- Unfiled returns. Missing payroll (Form 941), income, or excise returns make the IRS assume the worst and assess what it thinks you owe.

- A large income tax balance the business never paid down.

Withholding taxes from a paycheck and keeping the money is the line the IRS treats most harshly. The agency views it as spending the government's money to fund your operations — and it acts accordingly.

What the IRS can actually take

"Take my business" can mean several different things. Here's what's really on the table, from most common to most extreme:

- Business bank accounts — the most common business levy. The bank freezes the balance and, after 21 days, sends it to the IRS.

- Accounts receivable — the IRS can levy money your customers owe you, instructing them to pay the IRS directly. This can be devastating because it cuts off your incoming cash.

- Equipment, vehicles, and inventory — tangible assets the IRS can seize and sell at auction.

- The business itself as a "going concern" — in rare cases, the IRS seizes an operating business to sell it intact. This requires high-level approval and almost never happens to a cooperative taxpayer who is communicating.

Before any of this, the IRS usually files a federal tax lien — a public claim against business property. A lien is not a seizure; it's a warning. To understand the difference, see our guide on lien vs. levy.

What happens if you ignore the notices

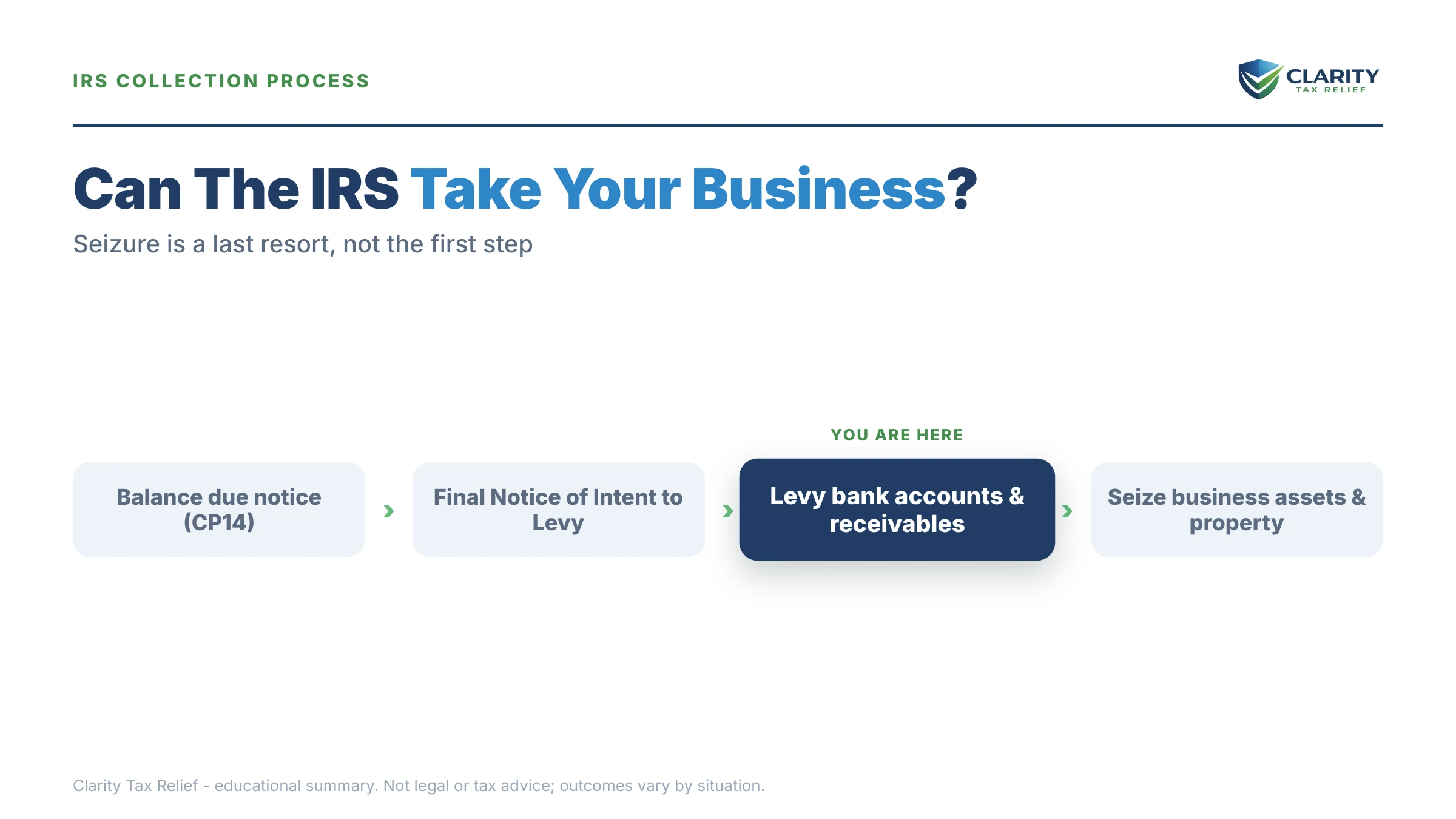

The path to seizure is a sequence, not a surprise. Each notice arrives weeks apart, with more enforcement power behind it. Ignore them and the system keeps moving:

- Balance-due notices (CP14, then reminders) — the first bills. No enforcement yet, but penalties and interest grow monthly.

- CP504 — Notice of Intent to Levy — the IRS can now grab state tax refunds and a lien becomes likely.

- LT11 / Letter 1058 — Final Notice of Intent to Levy — after 30 days with no response, the IRS can levy bank accounts and receivables. You have formal appeal rights here. Read our LT11 notice guide for the exact steps.

- Revenue officer assignment — for payroll cases and larger balances, a person is now handling your file. A visit often starts with Letter 725-B. This is when seizure of equipment or the business itself becomes a real conversation.

The takeaway: seizure follows silence. The single biggest factor in whether a business survives a tax debt is whether the owner responds before the deadlines pass.

The payroll tax trap: the Trust Fund Recovery Penalty

If your business owes payroll taxes, there's a personal danger most owners don't see coming. The IRS can assess the Trust Fund Recovery Penalty (TFRP) against any "responsible person" who willfully failed to pay over the trust fund portion of payroll taxes. That can mean the owner, an officer, a bookkeeper, or anyone with check-signing authority.

Here's why it matters: even if your business is an LLC or corporation that normally shields you, the TFRP reaches your personal assets — your home, your personal bank account, your wages. So "can the IRS take my business?" quietly becomes "can the IRS take my personal property too?" For trust fund debts, the answer can be yes. The IRS usually proposes this with Letter 1153, which gives you 60 days to respond.

How to stop the IRS from taking your business

The notice gives you two options — pay or else. In reality, the IRS has several programs, and a working business almost always has more room to negotiate than the letters suggest:

- File every missing return first. The IRS will not approve any agreement while returns are unfiled. This is step one, always.

- Installment agreement. A monthly IRS payment plan stops enforcement while you pay the debt down over time. In-business payroll cases have their own plan rules, but plans exist.

- Currently Not Collectible status. If paying anything would shut you down, collection can be paused while your situation recovers.

- Offer in Compromise. Settling for less than the full balance is real, but only when the IRS's own math shows you genuinely can't pay it all. Anyone promising to settle your debt for "pennies on the dollar" before reviewing your finances is selling you something — not telling you the truth.

- Collection Due Process appeal. Filing Form 12153 within 30 days of a Final Notice pauses levies and gets your case in front of an independent appeals officer.

How to respond, step by step

- Read the notice and find the deadline. A Final Notice of Intent to Levy starts a 30-day clock — that's your most urgent number.

- Confirm what you owe by logging into your IRS online account and pulling your business transcripts. Levies are sometimes based on unfiled returns the IRS estimated.

- File all missing returns. Nothing else moves forward until this is done.

- Choose your resolution path — payment plan, hardship status, or an offer — and set it up or file your appeal before the deadline.

- If a levy already hit your bank, act fast: the bank holds the money for 21 days. See how to request an emergency levy release for hardship.

- If payroll taxes or a revenue officer are involved, get an experienced tax professional in the conversation. These cases carry personal liability and move quickly.

Can the IRS take my business? Your questions, answered

Can the IRS actually shut down my business?

Yes, the IRS has the legal power to seize and sell business assets to satisfy a tax debt, which can effectively shut a business down. But seizing a working business is rare and treated as a last resort. It generally only happens after years of unpaid taxes, ignored notices, and a deliberate decision by a revenue officer and IRS managers.

What business taxes most often trigger an IRS seizure?

Unpaid payroll taxes are the biggest trigger. When you withhold income tax, Social Security, and Medicare from employee paychecks but don't send it to the IRS, that money is held in trust for the government. The IRS treats falling behind on these trust fund taxes far more aggressively than other debts, and the people responsible can be held personally liable.

Can the IRS levy my business bank account?

Yes. After a Final Notice of Intent to Levy and a 30-day window with no response, the IRS can levy your business bank account. The bank freezes the balance and holds it for 21 days before sending it to the IRS. That 21-day hold is your window to act and request a release for hardship or to set up an agreement.

Can the IRS take my business if it is an LLC or corporation?

If the tax debt belongs to the LLC or corporation, the IRS can levy that entity's accounts and seize its assets. An owner usually isn't personally liable for the entity's income tax. But unpaid payroll trust fund taxes are different: the IRS can assess the Trust Fund Recovery Penalty against owners, officers, or anyone responsible for paying them, reaching personal assets.

How do I stop the IRS from taking my business?

Respond before the deadline on your notice. File any missing returns, then set up an installment agreement, request Currently Not Collectible status, or apply for an Offer in Compromise if you qualify. Filing a timely Collection Due Process appeal with Form 12153 also pauses enforcement. The worst move is ignoring the notices, because seizure follows silence, not negotiation.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. For the agency's own rules, see the IRS pages on IRS levies and the Taxpayer Advocate Service.