Refund Offsets

Tax Refund Offset for Student Loans: How to Stop It and Get Out of Default (2026)

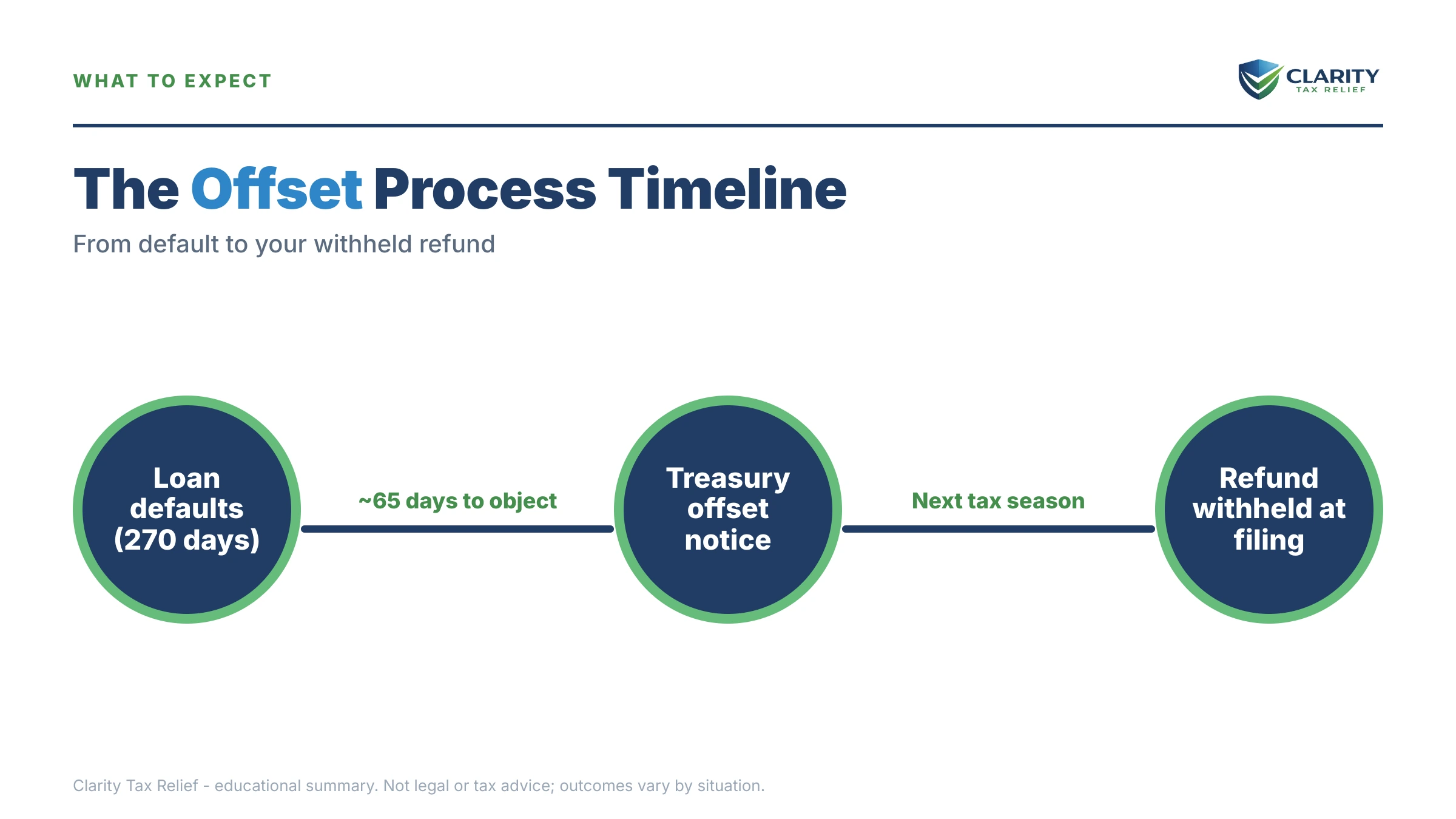

The short answer: a tax refund offset for student loans happens only when federal loans are in default — typically 270+ days past due — and the Department of Education refers them to the Treasury Offset Program. Offsets resumed in 2025 after the pandemic pause. Loan rehabilitation or consolidation stops future offsets.

"Where's My Refund" said your refund was approved. Then, instead of a deposit, a letter from the Bureau of the Fiscal Service arrived saying the money went to the Department of Education for defaulted student loans. It stings — but this is one of the most reversible problems in the collection world, because federal law gives you two clear exits from default that shut the offset machine off.

This matters more in 2026 than it has in years. Student loan offsets were paused for roughly five years during the pandemic; the Department of Education restarted them in 2025, and this filing season is the first full year many defaulted borrowers are losing refunds again. The image below shows what the offset paperwork looks like and where to find the two facts that matter most — the agency that took the money and the exact amount.

⏱ Your window: before your refund can be taken, you should receive a Notice of Intent to Offset — and it typically gives you 65 days from its date to request a review, dispute the debt, or start getting out of default. Check the date printed on your notice; requesting review inside that window generally pauses the offset until it's decided. If your refund was already taken, there's no reversal deadline — but every future refund stays at risk until the default ends.

Why your tax refund was offset for student loans

Federal student loans in default can take 100% of your federal tax refund through the Treasury Offset Program. The IRS doesn't make this decision — the Department of Education certifies your defaulted loan to the Treasury Offset Program (TOP), and the Bureau of the Fiscal Service intercepts the refund before it ever reaches your bank account.

Only defaulted federal loans qualify. A Direct or FFEL loan generally enters default after about 270 days of missed payments. Loans in an income-driven plan, deferment, or forbearance — even if you're struggling — are not certified for offset. Private student loans can never use TOP at all.

Offsets also follow a fixed pecking order. Federal tax debts get paid first (the IRS keeps the refund itself), then past-due child support, then federal non-tax debts like defaulted student loans, then state income tax debts. So if you owe both the IRS and a defaulted loan, the IRS is satisfied before a dime goes to the Department of Education.

How to find out who took your refund — and how much

The TOP call center at 800-304-3107 will tell you which debts are certified against your Social Security number before you ever file. Our guide to the offset hotline walks through exactly what the automated line asks and what it can and can't tell you.

After an offset happens, three paper trails confirm it. The Bureau of the Fiscal Service mails a letter showing the amount taken, the agency that received it, and that agency's contact information. Your IRS account transcript shows code 898 — "refund applied to non-IRS debt" — usually right after the 846 refund issued date. That's why "Where's My Refund" can say your refund was sent while your bank account stays empty: the IRS did send it, just not to you.

One thing that trips people up: the IRS cannot return money taken for a student loan offset. Once the funds transfer, disputes go to the Department of Education's Default Resolution Group or your loan holder — calling the IRS about it wastes weeks you could spend fixing the default.

What happens if you stay in default

A defaulted federal student loan never expires — unlike IRS debt, there is no 10-year collection statute for federal student loans. If you do nothing, collection escalates through a sequence that gets harder to unwind at each stage:

- Default — generally after about 270 days of missed payments. The full balance accelerates, collection costs are added on top, the default hits your credit, and you lose access to new federal aid and normal deferment options.

- TOP certification — once the intent-to-offset notice window passes, your loan sits in the Treasury's database. Your federal refund can be offset every year until the debt is resolved — there's no annual limit and no cap.

- Administrative wage garnishment — the Department of Education can order your employer to withhold up to 15% of your disposable pay with no court order, after a 30-day notice with hearing rights.

- Federal benefit offset — a portion of Social Security retirement or disability benefits can be offset for defaulted loans, though federal law protects a monthly floor of roughly $750.

- The long tail — the government can sue, and because there's no statute of limitations, a loan from decades ago can still take this year's refund. Waiting it out is not a strategy that exists here.

The offset itself isn't wasted money — it does pay down the loan (after collection costs). But as the worked example below shows, offsets alone barely dent a large balance, while the default keeps costing you everywhere else.

Refund taken — or afraid this year's will be?

If defaulted loans took your refund and you also have unfiled returns or IRS debt in the mix, the order you fix things in changes what you keep. Get a free, confidential review of your whole picture — an experienced tax professional will map the fastest path out.

How to stop a tax refund offset for student loans

Loan rehabilitation and loan consolidation are the two exits from default that permanently end refund offsets. Everything else — disputes, injured spouse claims, hardship reviews — addresses one offset without fixing the underlying default. Here's how the options compare:

| Option | Who it's for | What it does | Typical timeline |

|---|---|---|---|

| Loan rehabilitation | Any defaulted federal borrower (one time per loan) | Ends offsets once complete; removes the default from your credit history | 9 on-time payments in 10 months |

| Direct Consolidation Loan | Borrowers who need out of default faster | Ends offsets once the new loan is made; default stays on credit history | Often 1–3 months |

| Request review / dispute | Debt isn't yours, was paid, discharged, or is tied to a closed school or pending discharge | Pauses or cancels the offset if the debt isn't enforceable | Inside the window on your notice |

| Injured spouse (Form 8379) | Joint filers whose spouse — not them — owes the loan | Recovers your share of the joint refund | A couple of months or more |

| Hardship review with ED | Offset would cause serious financial harm | May reduce, pause, or in narrow cases refund an offset — discretionary and limited | Case by case |

| Pay the loan in full | Small balances only | Ends certification immediately | Immediate |

Rehabilitation is usually the stronger play if you can wait: nine on-time monthly payments within ten months, with the amount based on your income — payments can be as low as $5 a month for low earners. When you finish, the loan leaves default, offsets stop, and the default notation comes off your credit history. The catch: offsets can still happen during the rehabilitation months, so start early enough that you finish before you file a return with a big refund on it.

Consolidation is faster — you fold the defaulted loan into a new Direct Consolidation Loan, usually by agreeing to an income-driven repayment plan or making three voluntary payments first. It ends offset certification sooner, but the historical default stays on your credit record, and you can generally only use it if you haven't already consolidated your way out of default once.

Which path is realistic depends partly on how big the defaulted balance is:

| Defaulted balance | Most realistic path | Why |

|---|---|---|

| Under $5,000 | Pay in full or quick rehabilitation | One or two refund offsets may nearly clear it anyway — paying it off ends certification immediately and stops collection costs |

| $5,000–$25,000 | Rehabilitation, then an income-driven plan | Income-based rehab payments are affordable, and the credit-repair benefit matters at this size |

| $25,000–$100,000 | Rehabilitation or consolidation into income-driven repayment | Offsets barely dent the balance while fees compound — exiting default and letting the IDR formula set the payment is the only math that works |

| Over $100,000 | Consolidation + IDR, plus discharge screening | At this size, check disability discharge, closed-school, and borrower-defense eligibility before committing to a repayment path |

Two boundaries worth knowing. The IRS's offset bypass refund for hardship applies only when your refund would offset an IRS tax debt — the IRS has no power to bypass a Treasury offset for student loans. And if your real problem is a balance owed to the IRS itself rather than a loan, that's a different playbook entirely — start with our guide on how to settle tax debt yourself.

Married filing jointly? Your spouse's share is recoverable

A joint refund can be taken in full for one spouse's defaulted student loans — but the other spouse can claim their share back. The tool is Form 8379, Injured Spouse Allocation, which splits the refund based on each spouse's income, withholding, and credits. Our injured spouse Form 8379 walkthrough covers the allocation line by line; the official form is at IRS.gov's About Form 8379 page.

You can attach Form 8379 to your return before filing — smart if you know the offset is coming — or file it alone after the money is taken. Either way, expect processing to take a couple of months or more, and know that it protects only the injured spouse's portion, not the borrower's.

If the debt that grabbed your refund belongs to a former spouse, the fix looks different — see ex-spouse's tax debt took my refund for how liability actually splits after divorce.

Worked example: $68,500 in default, three years unfiled

Say you're a gig worker with $68,500 in defaulted federal student loans and three years of unfiled tax returns. You've avoided filing partly because you figured any refund would be seized anyway. Here's the actual math — hypothetical, but realistic.

Suppose those three returns, once filed, would produce refunds of $2,100, $1,750, and $2,650 from Earned Income Tax Credit and overpaid estimated taxes — $6,500 total. If the loans stay in default, TOP intercepts all $6,500. After the collection costs the government adds to defaulted loans, only a portion reaches principal — against $68,500, the balance barely moves, and next year's refund gets taken too.

Now run the alternative. You start loan rehabilitation; with modest gig income, the income-based formula might set your payment at a low two-digit monthly amount. Nine payments over ten months — call it under $500 total — pulls the entire $68,500 out of default, decertifies it from TOP, removes the default from your credit history, and rolls you into an income-driven plan going forward. You keep every future refund.

The unfiled years carry their own clock: refunds die three years after the return's due date. If the oldest of your three returns is approaching that line, filing it means the refund at least pays down your loan through the offset — waiting past the deadline means it vanishes entirely and pays nothing. See the 3-year refund deadline for old returns and our guide for people who haven't filed in 3 years — filing also heads off the IRS filing a substitute return that manufactures a tax debt on top of the loan problem.

How to respond, step by step

- Call the offset hotline: 800-304-3107 tells you which debts are certified against your Social Security number and for how much — check before you file, or confirm after an offset.

- Confirm your loan status: log in at StudentAid.gov to verify which loans are in default, who holds them now, and the current balance with collection costs.

- Pick your exit from default: start loan rehabilitation (nine income-based monthly payments) or a Direct Consolidation Loan — either one ends future refund offsets once complete.

- File Form 8379 if you filed jointly: recover your share of a joint refund that was taken for your spouse's defaulted loans — you can file it with your return or after the offset.

- File any missing tax returns: unfiled years risk losing refunds forever to the 3-year deadline and create IRS problems far bigger than the offset itself.

When you can handle this yourself

Most single-debt student loan offsets are fixable without paying anyone. If your only issue is a defaulted federal loan, you can call the hotline, verify the debt on StudentAid.gov, and set up rehabilitation or consolidation directly with the Default Resolution Group — those programs cost nothing to enter, and no company can get you terms the income-based formula doesn't already provide. A straightforward Form 8379 is also a reasonable DIY project.

Experienced help changes outcomes in the messier combinations: multiple unfiled years alongside the default (the filing order and refund-statute timing matter), an IRS balance competing with the loan for your refund, a wage garnishment already running against gig or W-2 income, or a debt you believe isn't enforceable — wrong person, paid, discharged, or tied to a school that closed. In those cases, an experienced tax professional coordinating the tax side while you work the loan side prevents one fix from stepping on the other.

Terms on your offset notice, decoded

- Treasury Offset Program (TOP): the Treasury system, run by the Bureau of the Fiscal Service, that intercepts federal payments — including tax refunds — to pay debts owed to government agencies.

- Default: the status a federal student loan reaches after roughly 270 days of missed payments, which triggers acceleration, collection costs, and offset eligibility.

- Certification: the Department of Education's formal referral of your defaulted loan into TOP — the switch that makes your refund interceptable.

- Loan rehabilitation: nine on-time, income-based monthly payments within ten months that pull a loan out of default and erase the default from your credit history.

- Administrative wage garnishment (AWG): the government's power to take up to 15% of your disposable pay for a defaulted loan without a court order.

- Injured spouse: a joint filer whose refund share was taken for a debt that belongs only to their spouse — recoverable with Form 8379.

Student loan refund offset questions, answered

Will the IRS take my tax refund for student loans in 2026?

Yes — if your federal student loans are in default, your refund can be offset in 2026. The Department of Education resumed referring defaulted loans to the Treasury Offset Program in 2025 after a five-year pandemic pause, so many borrowers are seeing offsets again for the first time since 2020. Loans in good standing, deferment, or forbearance are not offset.

How do I know if my tax refund will be offset for student loans?

Call the Treasury Offset Program hotline at 800-304-3107 before you file. The automated line tells you whether any debt is certified against your Social Security number and which agency submitted it. You should also receive a Notice of Intent to Offset from the Department of Education — typically 65 days before your refund can be taken.

Can I get my refund back after a student loan offset?

Only in limited situations. Money already offset can be returned if the debt was paid, isn't yours, was discharged in bankruptcy, or the offset was made in error — and the Department of Education has granted hardship refunds in narrow circumstances. If you filed jointly, your spouse's share can be recovered with Form 8379. Requests go to the loan holder, not the IRS.

Does loan rehabilitation stop the tax refund offset?

Yes, once you complete it. Rehabilitation takes nine on-time monthly payments within ten months, and payments are income-based — they can be as low as $5 a month. Offsets can still happen during those months, so time your rehabilitation to finish before you file if a large refund is coming. Completing rehabilitation also removes the default from your credit history.

Can private student loans take my federal tax refund?

No. The Treasury Offset Program only collects debts owed to federal and state government agencies, and private lenders can't use it. A private lender must sue you, win a judgment, and then use state remedies like wage garnishment or bank levies. If a private collector threatens your tax refund, that's a pressure tactic, not a real power.

Will a student loan offset take my Earned Income Tax Credit?

Yes. Your entire federal refund — including refundable credits like the EITC and the Additional Child Tax Credit — can be offset for defaulted federal student loans. The temporary protections some borrowers saw during the pandemic pause have ended. That makes checking the offset hotline before filing especially important for gig workers and families whose refunds are mostly credits.

My spouse's student loans took our joint refund — can I get my share back?

Usually, yes. File Form 8379, Injured Spouse Allocation, to recover the portion of the joint refund attributable to your income, withholding, and credits. You can attach it to your return before filing or send it after the offset — expect processing to take a couple of months or more. This is different from innocent spouse relief, which deals with tax debts, not loans.

Do student loans on an income-driven repayment plan get offset?

No. Only defaulted loans that the Department of Education certifies to the Treasury Offset Program can take your refund. Loans in an income-driven plan, standard repayment, deferment, or forbearance are in good standing and aren't referred. That's why getting out of default through rehabilitation or consolidation — and then staying in an affordable plan — protects every future refund.

Your next 24 hours

- Find the source. Call 800-304-3107 and note which agency certified the debt and the amount — or, if you're holding a Notice of Intent to Offset, find its date and count your review window from there.

- Gather your file. Log in at StudentAid.gov for your loan list and default status, and pull together your last filed return, income records (1099s if you're a gig worker), and any offset letters.

- Get the plan reviewed free. If unfiled years, IRS debt, or a garnishment are tangled up with the offset, call (888) 825-7779 or use the 2-minute form at the free consultation page — every default month means added collection costs, and every filing season in default means another refund gone.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.