Offer in Compromise

Can I Apply for an OIC While on a Payment Plan? (2026 Rules)

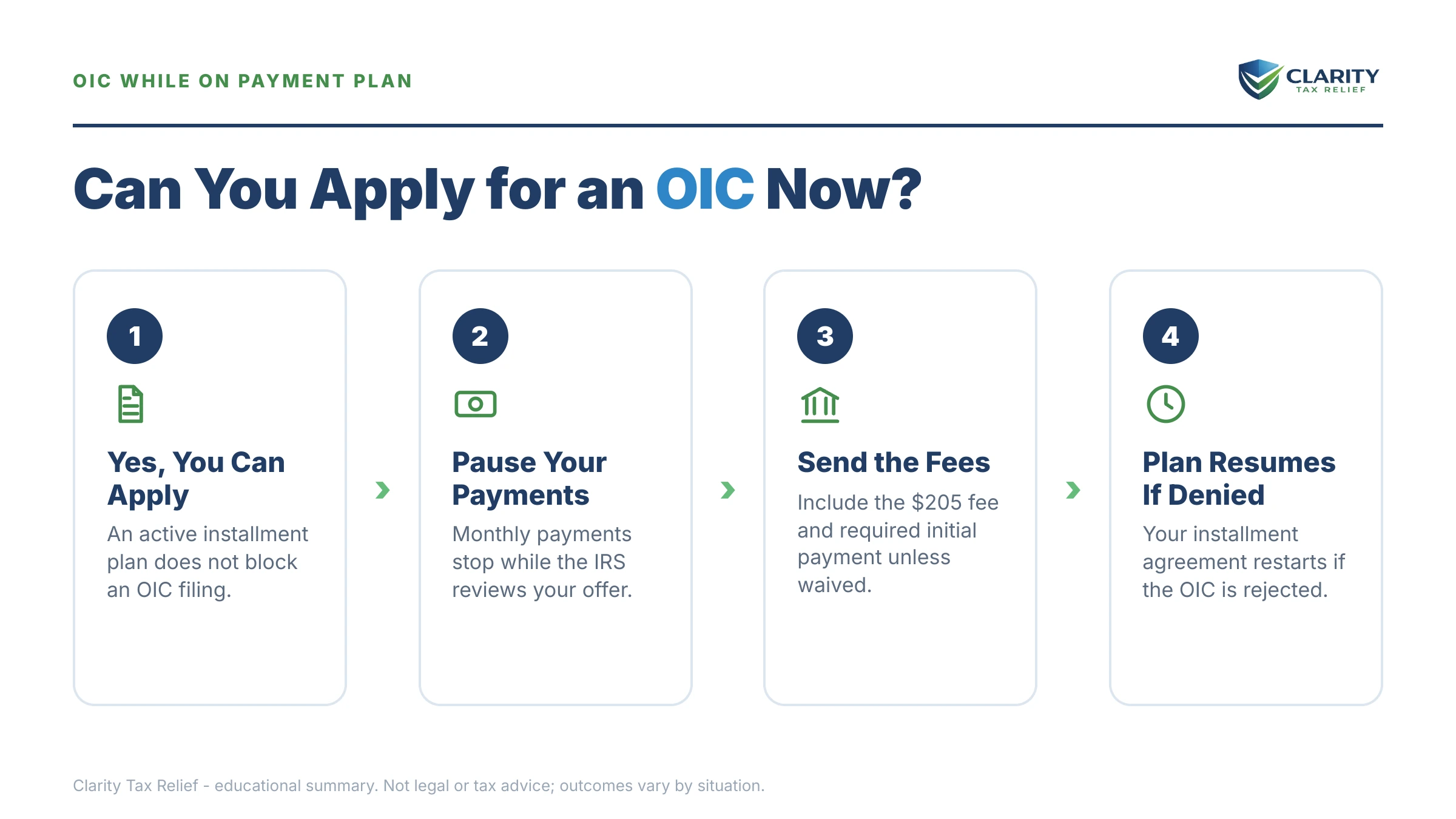

The short answer: yes — you can apply for an Offer in Compromise while on an IRS payment plan. Once the IRS accepts your offer for processing, your installment agreement payments are suspended during review. If the offer is rejected, returned, or withdrawn, the plan is generally reinstated and payments resume.

You've been sending the IRS the same payment every month, and each new balance statement seems to move less than the check you mailed. Somewhere along the way you heard the debt can sometimes be settled for less — and now you're wondering whether applying would blow up the plan you already fought to get. It won't, and the rules here actually favor you more than most people expect.

So, can I apply for an OIC while on a payment plan? Yes — and three facts should frame your decision before anything else. Your monthly plan payments pause once the offer is deemed processable; the payments you've already made count toward your balance but never toward your offer; and your own payment history becomes evidence the IRS uses to judge whether it could collect in full. The stage-by-stage table below shows exactly what happens to your agreement at each point in the offer process.

⏱ The clock that's actually running: there is no deadline to apply for an Offer in Compromise. But your plan has a meter — interest compounds daily on the unpaid balance, and the failure-to-pay penalty continues at a reduced 0.25% per month while an installment agreement is in effect. Part of every payment you send is absorbed by those charges before it touches the debt.

Can you apply for an OIC while on a payment plan? How the IRS handles it

The IRS accepts Offer in Compromise applications from taxpayers with active installment agreements, and it suspends the agreement's payments once the offer is accepted for processing. Form 656 — the offer application itself — asks directly whether you have an existing installment agreement, because the situation is routine, not a conflict.

Here's the part the notice stuffers never explain: the plan is suspended, not terminated. You don't lose the agreement by applying. If the offer fails, the IRS generally puts the plan back in force at its prior terms, so applying doesn't burn the bridge you're standing on.

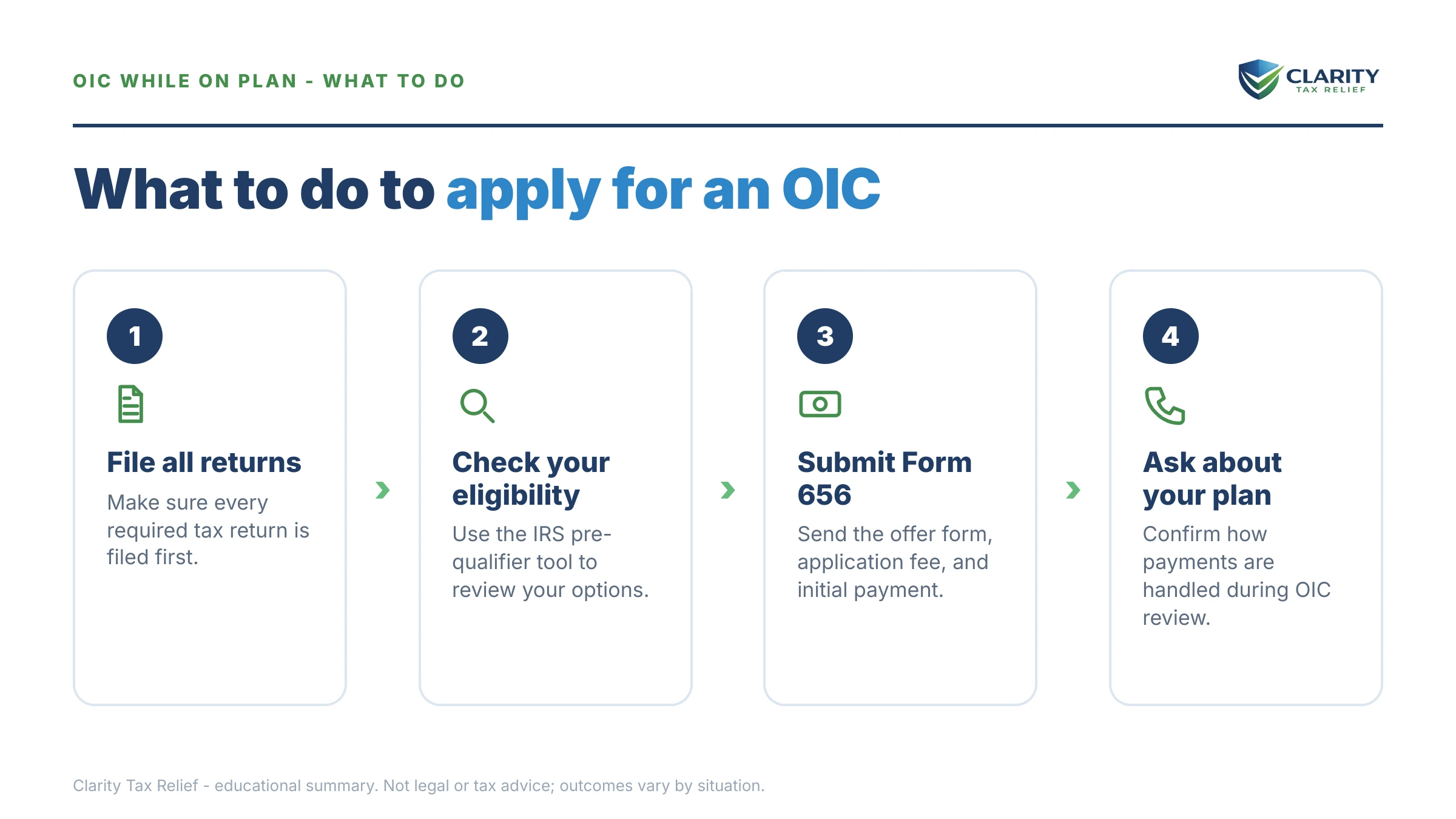

Two conditions still apply, plan or no plan. Every required return must be filed, and your current-year withholding or estimated payments must be on track. An offer from a non-compliant taxpayer gets returned unreviewed — with the fee kept. For the full mechanics of eligibility, the offer formula, and the two payment structures, see our guide to how an offer in compromise works; this page stays focused on what's different when you're already on a plan.

Why people on payment plans switch to an offer — and when they shouldn't

An installment agreement pays the whole debt over time; an Offer in Compromise pays only what the IRS could realistically collect — and being on a plan is often the moment people discover the gap between those two numbers. The common triggers are real: your income dropped after the plan was set, the balance barely moves because interest eats each payment, or the plan's term stretches past what your finances can sustain.

But your plan cuts both ways as evidence. If your current monthly payment would fully pay the debt before the 10-year collection statute expires, the IRS will usually conclude it can collect in full — and reject the offer. A comfortable, on-time payment history on a plan that retires the balance is close to a self-disqualification for a doubt-as-to-collectibility offer.

Keep the odds honest, too: the IRS accepted roughly 1 in 5 offers in FY2024, mostly because applicants' own numbers showed they could pay. Our breakdown of the offer in compromise acceptance rate 2026 shows who actually gets through. And if you're still weighing the two paths at a higher level, start with payment plan vs. offer in compromise — the decision framework is different when you haven't set up either one yet.

What happens to your installment agreement when you submit an offer

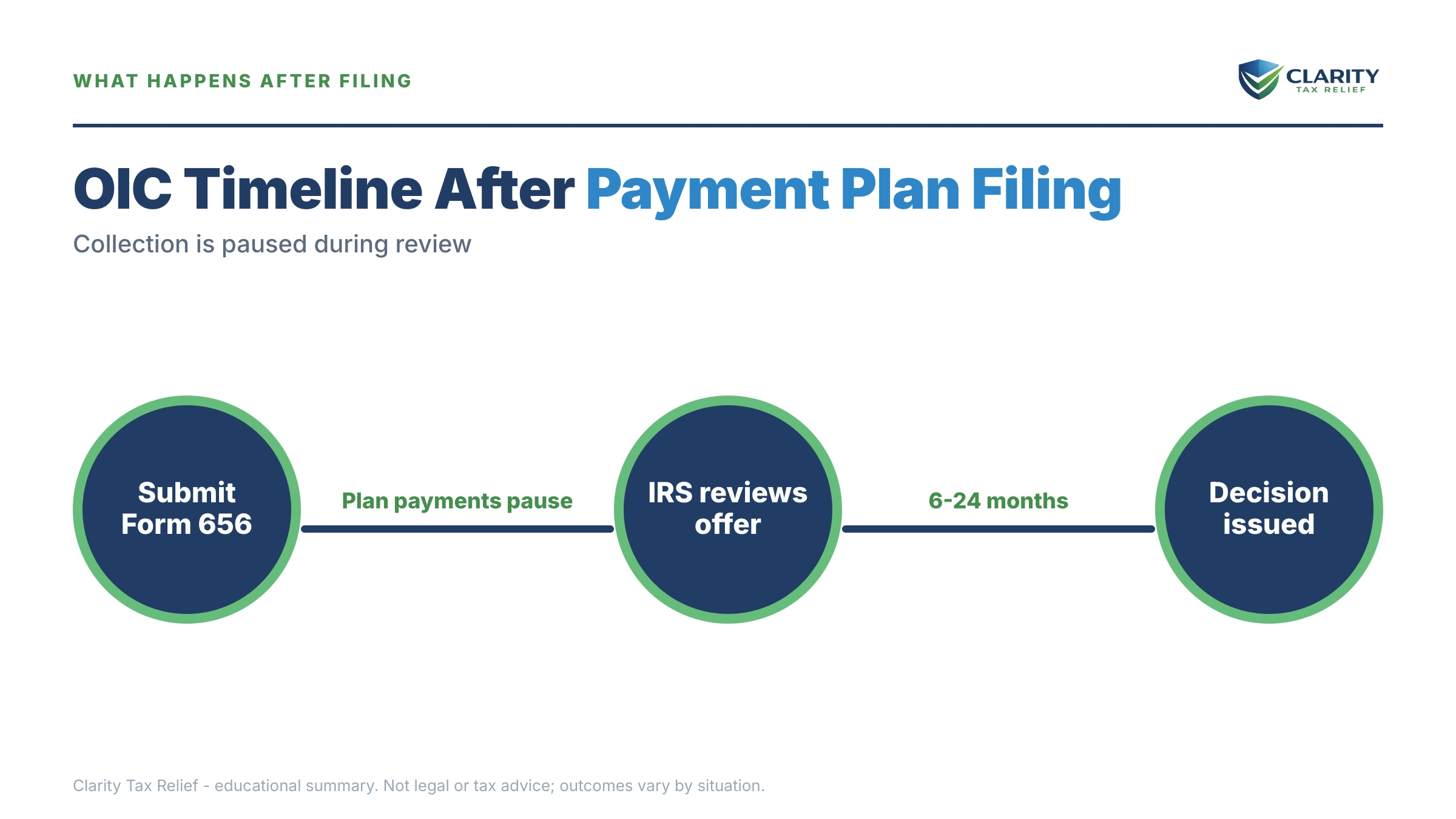

Your installment agreement moves through four distinct stages once an offer is filed, and the biggest mistakes happen at stage one. The sequence runs like this:

- Offer received — processability screening. The IRS checks that all returns are filed, the fee and initial payment (or low-income certification) are included, and you're current on this year's taxes. Keep making your plan payments through this stage. An offer returned as non-processable never suspended anything — and missed plan payments during the gap can push your agreement toward default.

- Offer deemed processable. Transaction code 480 posts to your account transcript, your installment agreement payments are suspended, and the 10-year collection statute stops running. You can confirm the posting yourself — our guide to code 480 transcript shows what it looks like.

- Investigation. An offer examiner works through your Form 433-A (OIC), compares it to bank statements and pay stubs, and may request documents on short turnaround. No plan payments are required, though interest keeps accruing on the full balance. If you chose a periodic-payment offer, you must make those monthly offer payments during review unless you're low-income certified.

- Decision. Accepted: the installment agreement ends and you pay the offer terms instead — then stay filing- and payment-compliant for five years, or the compromised debt comes back. Rejected: you have 30 days to appeal, and the plan is generally reinstated. Returned or withdrawn: no appeal rights, plan reinstated, payments resume. One backstop works in your favor — if the IRS doesn't decide within 2 years, the offer is deemed accepted automatically.

The statute suspension in stage two deserves its own warning. The CSED pauses while the offer is pending, plus 30 days after rejection, plus any appeal time. If your debt is old, a failed offer can gift the IRS a year of collection time it was about to lose — see what extends the IRS collection statute before filing on aging balances.

| Offer stage | Your installment agreement | Your rights / what to watch |

|---|---|---|

| Before submitting | Active — keep paying on schedule | A missed plan payment now can trigger default proceedings before the offer even lands |

| Processability screening | Still active — payments still due | Non-processable offers are returned with no appeal; the $205 fee is kept |

| Processable (TC 480 posts) | Payments suspended | CSED stops running from this point; confirm via transcript or letter before you stop paying |

| Under investigation | Suspended; interest still accrues | Periodic-offer payments required (unless low-income certified); answer document requests by their dates |

| Offer accepted | Terminated — offer terms replace it | Five years of filing and payment compliance required, or the full debt is reinstated |

| Offer rejected | Generally reinstated at prior terms | 30 days to appeal with Form 13711; CSED stays paused during appeal |

| Returned or withdrawn | Reinstated; payments resume | No appeal rights on a returned offer — fix the defect and refile instead |

On a payment plan and wondering if an offer would work?

The answer lives in your numbers — your income, allowable expenses, assets, and how much collection time the IRS has left. An experienced tax professional can run that math with you in one free call and tell you honestly whether an offer is worth the fee, or whether your plan (or a lower payment) is the smarter move. Interest is accruing either way — get the answer before another payment cycle goes by.

Your options side by side: stay on the plan, switch, or pause

Filing an offer is one of five realistic moves for someone already on an installment agreement, and each carries a different price tag. Note the fee structure of the offer itself before comparing: the $205 application fee, the 20% lump-sum down payment, and periodic offer payments are all non-refundable — even if the offer is rejected, they're applied to your balance, not returned. Our guide on whether the OIC down payment is refundable covers the fine print.

| Option | Upfront cost | While it runs | Typical timeline |

|---|---|---|---|

| Stay on the installment agreement | $0 (already set up) | Current monthly payment; interest + 0.25%/mo penalty accrue | Until paid — up to 72 months on plans under $50,000 |

| Pay the plan off early | Remaining balance | Nothing further | Immediate; stops all future interest and penalties |

| Lump-sum OIC | $205 fee + 20% of the offer | Plan payments suspended during review | Review often takes months; deemed accepted if no decision in 2 years; balance of offer due within 5 months of acceptance |

| Periodic-payment OIC | $205 fee + first offer installment | Monthly offer payments continue through review | Offer paid in monthly installments over up to 24 months |

| Currently Not Collectible | $0 | $0 owed monthly; interest still accrues | Until finances improve; IRS re-reviews periodically |

Two footnotes for smaller balances. If you owe $10,000 or less, you're in guaranteed installment agreement territory — the IRS must generally grant the plan, which is exactly why it will look hard at whether an offer is really necessary at that level. And if the plan itself is the problem rather than the total debt, choosing between lump-sum and periodic structures matters more than most applicants realize — compare them in OIC payment options: lump sum vs. periodic.

The math that decides it: Reasonable Collection Potential

The IRS accepts an offer only when it equals or exceeds your Reasonable Collection Potential — your net asset equity plus your monthly disposable income times 12 (lump-sum) or 24 (periodic). Your existing plan payment is the IRS's first data point for that disposable-income figure, which is why the full reasonable collection potential calculation deserves a careful read before you file. You can estimate your own number in a few minutes with our Offer in Compromise Calculator.

Here's how it plays out — this is a hypothetical, with the arithmetic shown. Say you owe $8,900 as a single W-2 employee, paying $150 a month on a streamlined plan (the minimum on $8,900 over 72 months is about $124, so you're paying slightly ahead).

Scenario one — the offer likely fails. Your gross monthly income is $4,300 and IRS allowable living expenses come to $4,150, leaving $150 of disposable income. Lump-sum offer math: $150 × 12 = $1,800, plus say $500 of countable asset equity = a $2,300 offer. Tempting against $8,900 — but the examiner sees that $150 a month over the years remaining on your collection statute collects far more than $8,900. Conclusion: the IRS can full-pay from your plan, so the offer is rejected, and you've spent $205 plus a $460 non-refundable down payment (20% of $2,300) to learn it.

Scenario two — the offer becomes viable. Your hours get cut and disposable income falls to $40 a month. Now the math reads $40 × 12 = $480, plus $500 of equity = a $980 offer — and $40 a month can't retire $8,900 before the statute runs. That's a genuine doubt-as-to-collectibility case. Better still, if the income drop puts your AGI at or below 250% of the federal poverty level, OIC low income certification waives the $205 fee, the down payment, and payments during review — so a failed offer costs you nothing but time.

Same debt, same person, opposite outcomes. The variable is never the balance — it's what your finances show the IRS could collect.

How to apply for an OIC while on a payment plan, step by step

- Confirm you're compliance-clean. Every required return must be filed and your current-year withholding or estimated payments must be on track. The IRS returns offers from non-compliant taxpayers without reviewing them — and keeps the fee.

- Run the offer math before you spend a dollar. Add your net asset equity to your monthly disposable income times 12 (lump sum) or 24 (periodic). If that number reaches your balance — or your plan full-pays before the collection statute expires — an offer is likely to fail.

- Complete Form 433-A (OIC) and Form 656. Disclose the existing installment agreement where Form 656 asks about it, and make sure the financial figures match your bank statements and pay stubs — mismatches are a top cause of returned offers.

- Submit the $205 fee and initial payment — or the low-income certification. Lump-sum offers require 20% of the offer amount up front; periodic offers require the first monthly payment. If your AGI is at or below 250% of the federal poverty level, check the low-income certification box and skip all three.

- Keep paying your plan until the offer is confirmed processable. Watch for transaction code 480 on your account transcript or a written processability letter, then stop installment payments. Respond to every examiner document request by its stated date — silence gets an offer returned, not rejected, with no appeal rights.

The IRS's own overview, pre-qualifier tool, and current Form 656 booklet are at IRS.gov's Offer in Compromise page — always pull the current booklet, since fee and certification figures adjust over time.

When you can handle this yourself — and when help changes the outcome

Plenty of people on payment plans don't need anyone's help, because the honest answer is that they don't need an offer. If your plan payment is affordable, your income is stable, and the balance will be gone within the term, staying put — or simply paying extra to cut interest — beats spending $665 up front on an offer the math says will fail. Even a payment that's grown too heavy is often fixed by lowering your IRS monthly payment rather than settling. And if you do qualify cleanly — low income, no meaningful assets, obvious hardship — the forms are tedious but doable on your own, with free help available through the Taxpayer Advocate Service or a Low Income Taxpayer Clinic.

Experienced help changes outcomes in the close calls: when disposable income sits near the line between "can full-pay" and "can't," when asset valuations are arguable, when you're deciding whether tolling the CSED on an old debt costs more than an offer saves, when multiple tax years or self-employment income complicate the 433-A (OIC), or when a prior offer already came back rejected and an appeal on Form 13711 is the next move. Those are judgment calls where the fee-versus-savings math genuinely favors representation. Details on plan mechanics themselves live at the IRS payment plans page.

Terms in the offer process, decoded

- Processable offer: an application that clears the IRS's intake screen — all returns filed, fee and initial payment included, current-year taxes on track — so it can actually be investigated.

- TC 480: the transcript transaction code confirming your offer is pending; it's your green light that installment payments are suspended.

- Reasonable Collection Potential (RCP): the IRS's calculation of the most it could ever collect from you — asset equity plus future income — and the floor for any acceptable offer.

- CSED: the Collection Statute Expiration Date, 10 years from assessment; a pending offer pauses this clock.

- Doubt as to collectibility: the legal basis for most offers — a showing that your assets and income can't cover the debt before the statute runs.

- Offer default: breaking the five-year post-acceptance compliance requirement, which reinstates the original debt minus what you paid.

Applying for an OIC while on a payment plan: your questions, answered

Do I have to keep making installment agreement payments while my OIC is pending?

No — once the IRS deems your offer processable, payments on an existing installment agreement are suspended while the offer is under review. Keep paying until you have written confirmation or transaction code 480 posts to your transcript, because an offer returned as non-processable never suspends anything. If you submitted a periodic-payment offer, you must make those offer payments during review unless you qualify for low-income certification.

Will applying for an Offer in Compromise cancel my payment plan?

No. The IRS suspends the agreement rather than terminating it. If your offer is rejected, returned, or withdrawn, the installment agreement is generally reinstated and your monthly payments resume. Acceptance is the only outcome that ends the plan — at that point you pay the offer terms instead of the old balance.

Does being on a payment plan hurt my chances of getting an OIC accepted?

The offer formula is the same, but your plan is evidence. If your current payment would full-pay the debt before the 10-year collection statute expires, the IRS will usually conclude it can collect in full and reject the offer. A plan you're visibly struggling to afford — or one that can't retire the balance before the statute runs — supports doubt as to collectibility.

Do the payments I already made on my plan count toward my offer?

No. Installment agreement payments reduce your outstanding balance, but they don't count as offer payments. Your offer amount is calculated fresh from your assets and future income, and the application fee, any 20% down payment, and periodic offer payments are all separate, non-refundable amounts on top of what you've already paid.

What happens to my payment plan if my offer is rejected?

Your installment agreement is generally reinstated and payments resume at the prior terms. You also get 30 days from the rejection letter to appeal using Form 13711, and the collection statute stays paused during the appeal. Interest that accrued during the review is added to the balance, so the plan may run slightly longer than before.

Does applying for an OIC extend the 10-year collection statute?

Yes. The CSED is suspended while your offer is pending, plus 30 days after a rejection, plus any time an appeal is under consideration. If your debt is old and the statute is close to expiring, a pending offer can hand the IRS extra collection time it would otherwise have lost — sometimes waiting out the clock beats settling.

Can I set up a payment plan first and then apply for an OIC later?

Yes, and it's often the smart order. The plan stops enforced collection immediately while you gather the financial documentation an offer requires, which can take weeks. Just remember the trade-off: every month on the plan chips away at the balance, and payments you make never count toward the offer itself.

How much does it cost to apply for an OIC if I'm already on a payment plan?

A $205 application fee, plus 20% of your offer amount up front if you choose a lump-sum offer, or the first monthly offer payment if you choose periodic payments. Low-income certification — AGI at or below 250% of the federal poverty level — waives the fee, the 20% down payment, and payments during review.

Your next 24 hours

- Pull your numbers. Log into your IRS online account (or grab your latest CP521 payment reminder) and write down three figures: your current balance, your monthly payment, and the tax year(s) assessed — the assessment date drives how much collection time the IRS has left.

- Gather the offer inputs. Your last filed return, two to three months of pay stubs and bank statements, and your real monthly bills. These feed both the RCP math and the Form 433-A (OIC) if you proceed.

- Get the math checked free. Send those numbers through the 2-minute form at claritytaxrelief.com/#consult or call (888) 825-7779. An experienced tax professional will tell you whether an offer beats your plan before you risk a non-refundable fee — and interest is accruing on the balance while you decide.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.