Offer in Compromise

Is the OIC Down Payment Refundable? What Happens to Your 20% and Payments (2025)

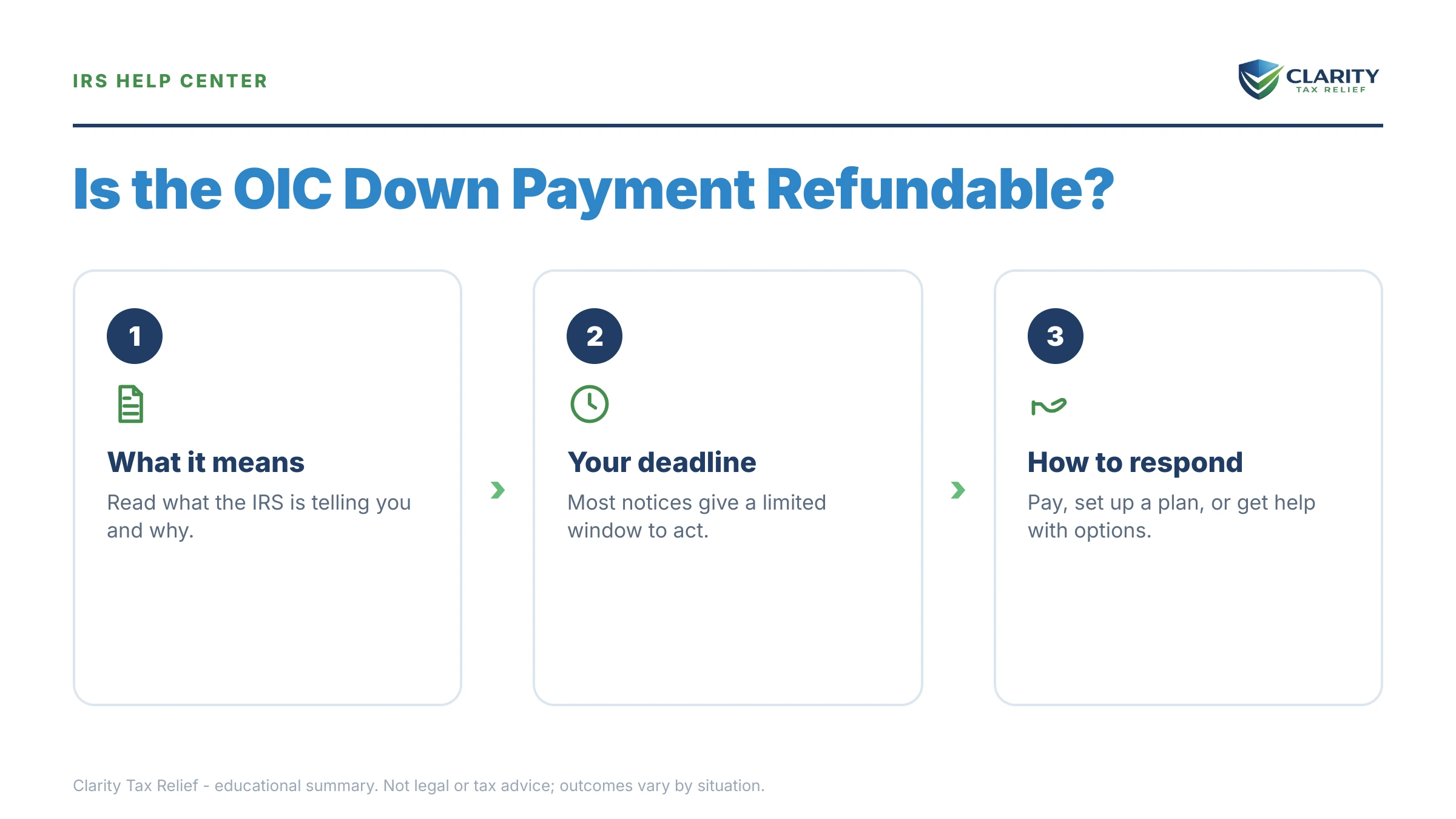

The short answer: the OIC down payment is not refundable. The 20% you send with a lump-sum Offer in Compromise (OIC) — and any monthly payments you make while it's pending — are applied to your tax debt even if the IRS rejects your offer. You don't get them back, but you can choose which year they reduce.

Not sure if your offer will actually be accepted?

Before you send a non-refundable down payment, talk to an experienced tax professional who can run the IRS's own math on your finances — free, confidential, and no pressure.

⏱ Timing that matters: while your offer is under review, periodic-payment offers require you to keep making the monthly payments — miss one and the IRS can return the offer. The IRS also has 24 months from the date it receives your offer to decide; if it doesn't act within that window, the offer is treated as accepted.

What the OIC down payment actually is

An Offer in Compromise lets you settle a tax debt for less than the full amount when you genuinely can't pay it all. To apply, you submit Form 656 and — unless you qualify for the low-income waiver — money up front. There are two payment structures, and they handle the up-front money differently (the IRS lays them out on its Offer in Compromise page):

- Lump-sum cash offer: you send 20% of your total offer amount with the application, then pay the rest in five or fewer payments after acceptance.

- Periodic-payment offer: you send the first monthly payment with the application and keep making the proposed monthly payments while the IRS reviews the offer.

Many people assume this money is a refundable deposit, like earnest money on a house. It is not. That's the single biggest misunderstanding about how an OIC works.

The hard truth: the 20% is non-refundable

Here's the part the marketing rarely mentions. The 20% down payment and every periodic payment you make are not deposits — they are payments toward your tax debt. The IRS keeps them no matter what happens to your offer.

That means if the IRS rejects your offer, returns it, or you withdraw it yourself, that money does not come back. It stays applied to your balance. This is by design, and it's why submitting an offer you don't actually qualify for can be an expensive mistake.

It's also why the "pennies on the dollar" pitch is so dangerous. Anyone promising to settle your debt for pennies on the dollar before reviewing your finances is selling you something — and if they talk you into a long-shot offer, your non-refundable 20% pays for their gamble, not yours.

What happens to your money if the offer is rejected

If your offer is rejected, the IRS applies your down payment and payments to what you owe. By default, the IRS decides which tax period and balance the money reduces. But you have an important right: you can designate where the payment goes when you submit it.

That matters because some tax periods are closer to the end of the 10-year collection statute than others, and some carry penalties you might later get removed. Telling the IRS in writing — clearly, on the payment itself — which year to credit gives you control over money you can't get back.

A worked example

Say you owe $40,000 and submit a lump-sum offer of $10,000. Your down payment is 20% of the offer — $2,000 — sent with Form 656.

- If the offer is accepted: the $2,000 counts toward your $10,000 settlement. You pay the remaining $8,000 in five or fewer payments, and the other $30,000 is forgiven.

- If the offer is rejected: you do not get the $2,000 back. The IRS applies it to your $40,000 debt, leaving roughly $38,000 (plus continuing penalties and interest). You can appeal the rejection, but the $2,000 is gone either way.

Same money, very different outcome. That gap is exactly why you want to know your real odds before you write the check.

The application fee works differently

The OIC application fee is separate from the down payment, and it follows its own rules. If the IRS finds your offer is not "processable" and returns it, the fee is refunded. But if the offer is processed and then rejected, the fee is generally kept and applied to your balance — not returned. You can see the current amount on the Form 656 booklet from the IRS.

Who can skip the down payment entirely

If you qualify as a low-income taxpayer under the IRS guidelines, you don't have to send the 20% down payment, the periodic payments, or the application fee while your offer is pending. You claim this by checking the Low Income Certification box on Form 656. Our guide to the low-income OIC fee waiver walks through who qualifies and how to prove it.

See your likely offer amount in about 2 minutes

Before you decide anything, our free Offer in Compromise Calculator runs your income, expenses, and assets through the same Reasonable Collection Potential formula the IRS uses to estimate the lowest amount the IRS may accept to settle your debt. No sign-up, instant result.

Estimate my offer →How to protect your money, step by step

- Get an honest assessment first. The IRS bases acceptance on your "reasonable collection potential" — your assets plus future income. Learn how an Offer in Compromise actually works and whether your numbers fit before paying anything.

- Pick the right payment structure. Lump-sum and periodic offers calculate the settlement amount differently. Our guide to OIC payment options compares them side by side.

- Check the low-income certification. If you qualify, you keep your money and skip the up-front payments entirely.

- Designate every payment in writing. Note exactly which tax year the down payment should reduce, and keep a copy of your instructions and the check or confirmation.

- If your offer is rejected, appeal fast. You generally have 30 days. See what to do when an OIC is rejected — your appeal rights and your alternatives.

OIC down payment questions, answered

Is the OIC down payment refundable if my offer is rejected?

No. The 20% down payment on a lump-sum Offer in Compromise is non-refundable. If the IRS rejects your offer, that money is not returned — it is applied to your tax debt. You can tell the IRS in writing which tax year and balance to put it toward.

Do I get my 20% back if I withdraw my offer?

No. Whether the IRS rejects your offer, returns it, or you withdraw it yourself, the 20% down payment and any monthly payments you made stay with the IRS and are applied to what you owe. They are never refunded — so withdrawing does not get your money back.

What about the OIC application fee — is that refundable?

The application fee is generally not refunded either, but it is handled differently from the down payment. If the IRS returns your offer because it was not processable, the fee comes back. If the offer is processed and then rejected, the fee is kept and applied to your balance, not refunded.

Can I avoid the 20% down payment?

Yes, if you qualify as a low-income taxpayer. Taxpayers who meet the IRS low-income guidelines do not have to send the 20% down payment, the periodic payments, or the application fee while their offer is pending. You claim this by checking the Low Income Certification box on Form 656.

Where does my down payment go if the offer is rejected?

It is applied to your tax debt. By default the IRS decides which year and balance it reduces, but you have the right to designate where the payment goes when you submit it. Write your instructions clearly on the payment and keep a copy, so it lands on the period you choose.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.