Offer in Compromise

Dissipated Assets OIC: When the IRS Adds Back Spent Assets (2025)

The short answer: a dissipated asset in an OIC (Offer in Compromise) is money or property you once had but spent, gave away, or transferred for less than it was worth — instead of paying the IRS. The IRS may add that value back into your offer as if you still owned it. You can fight an add-back by proving the money went to necessary living expenses or was spent before the tax was owed.

Worried an asset you spent could sink your offer?

Send us your situation. An experienced tax professional will look at the timeline, flag what the IRS might add back, and tell you honestly whether an Offer in Compromise is realistic — free, confidential, no pressure.

⏱ Timing matters: the IRS typically reviews the 3 years before you file your offer, plus the time after your tax was assessed. The longer ago an asset was spent — and the more clearly it went to rent, food, or medical care — the harder it is for the IRS to add it back. Build your records before you submit.

What "dissipated assets" actually means

When you apply for an Offer in Compromise, the IRS calculates what it could collect from you if it tried hard — your reasonable collection potential, or RCP. That number is the value of your assets plus a slice of your future income. Your offer has to roughly match it.

Here's the catch. The IRS doesn't only count what you own today. If you had an asset — a savings account, a retirement account, a piece of real estate, an inheritance — while you owed back taxes, and you spent it on something other than the debt, the IRS may treat it as a dissipated asset and add its value back into your RCP. In plain terms: they count money you no longer have.

The logic, from the IRS's point of view, is fairness. They don't want someone to cash out a 401(k), take a cruise, gift money to relatives, and then ask to settle a tax debt "pennies on the dollar." (Anyone promising you that outcome before reviewing your finances is selling you something — it's not how the program works.) The dissipated asset rule exists to stop people from emptying their pockets right before pleading poverty.

Why the IRS adds spent assets back to your offer

An examiner reviewing your Form 656 and financial statement is trained to look for money that "disappeared." The Internal Revenue Manual instructs them to question large or unusual transactions during the period you owed taxes. Common triggers include:

- Cashing out retirement accounts — a 401(k) or IRA withdrawal that didn't go toward the tax debt.

- Selling property or a vehicle for cash that then vanished from your accounts.

- Large transfers to family — gifts, "loans," or moving money into a relative's name.

- Big-ticket spending — a new boat, luxury travel, or paying off a non-essential loan while ignoring the IRS.

- Receiving an inheritance or settlement that was spent down before the offer.

If the examiner decides one of these counts, they add the value to your RCP. Your offer amount has to rise to match — sometimes by tens of thousands of dollars.

A worked example

Say you owe the IRS $60,000. You have $2,000 in the bank, an old car worth $4,000, and modest income. On paper, your reasonable collection potential might be around $8,000 — and an offer near that figure could make sense.

But two years ago, while you already owed the tax, you withdrew $30,000 from a retirement account. You spent $18,000 of it on a kitchen remodel and a vacation, and $12,000 on overdue rent and a hospital bill.

The examiner may treat the $18,000 in non-essential spending as a dissipated asset and add it to your RCP — pushing the number the IRS expects from around $8,000 to roughly $26,000. The $12,000 you spent on rent and medical care should not be added back, because those are allowable living expenses. The difference between a workable offer and a rejected one often comes down to which dollars you can document.

What is not a dissipated asset

This is where people panic unnecessarily. The IRS is not supposed to punish you for surviving. Money spent on ordinary, necessary costs is not dissipation. That generally includes:

- Rent or mortgage, utilities, and food

- Medical care and health insurance

- Reasonable transportation to work

- Court-ordered payments like child support

- Other costs that fall within the IRS allowable living expenses standards

Money you spent before the tax was assessed also shouldn't count — you can't dissipate an asset to avoid a debt that didn't exist yet. And funds used to pay the IRS itself obviously aren't dissipation.

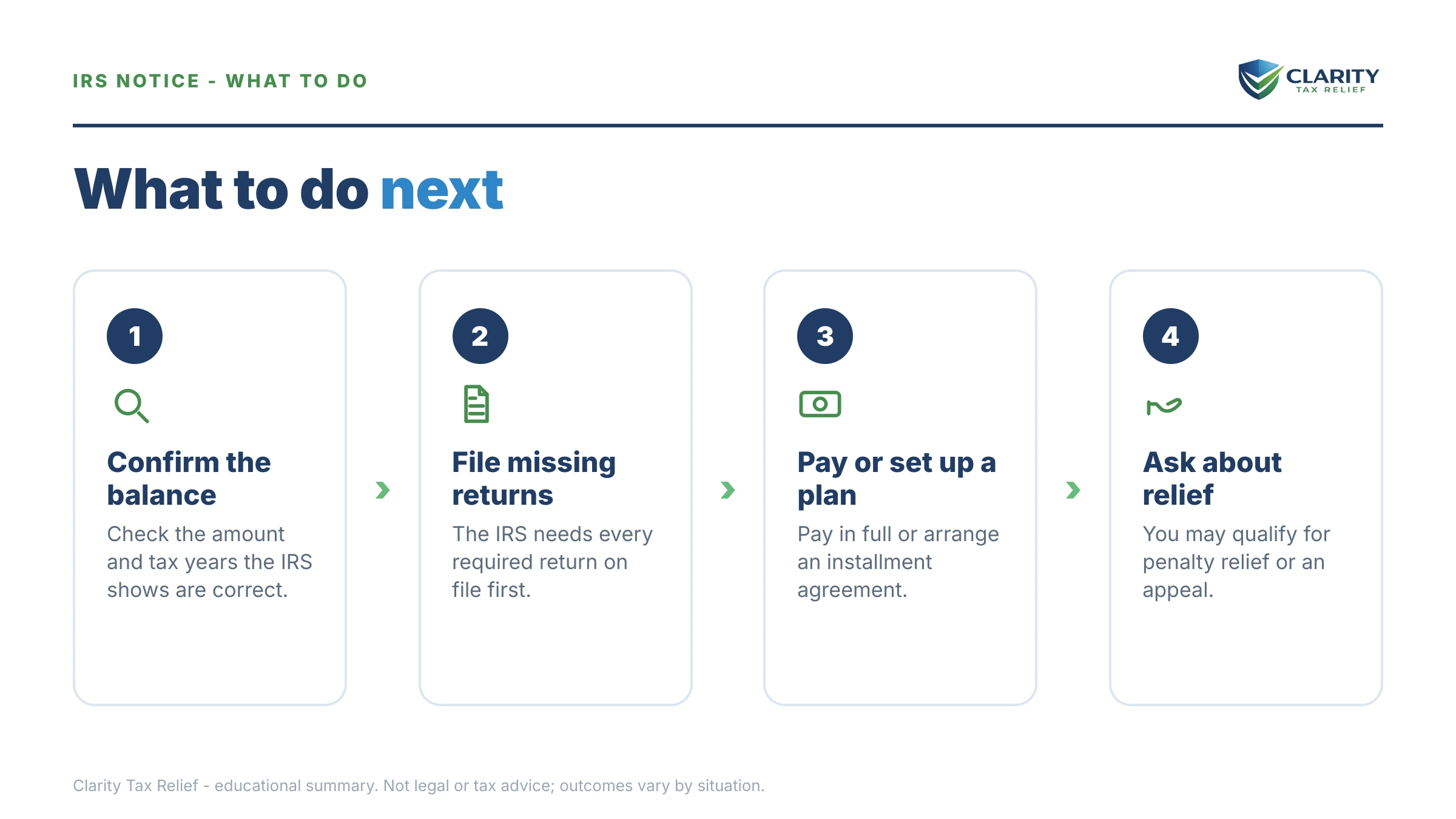

What happens if you ignore the issue

You can't make a dissipated asset disappear by not mentioning it. Bank records, 1099s, and prior transactions are visible to the IRS. Here's how the problem tends to escalate when it's left unaddressed:

- Add-back on the calculation. The examiner quietly raises your RCP, so your offer looks far too low.

- Offer rejected. Because the offer no longer matches the IRS's number, it's returned or rejected — and your application fee and any deposit are generally not refunded.

- Lost time. Months pass while penalties and interest keep growing on the underlying debt.

- Harder second attempt. You can try again or appeal, but you've now shown your hand and have less leverage.

The better path is to get ahead of it: identify any spending the IRS might question, gather proof, and explain it in the offer itself rather than waiting to be challenged.

See your likely offer amount in about 2 minutes

Before you decide anything, our free Offer in Compromise Calculator runs your income, expenses, and assets through the same Reasonable Collection Potential formula the IRS uses to estimate the lowest amount the IRS may accept to settle your debt. No sign-up, instant result.

Estimate my offer →How to respond, step by step

- Map your last three years of money. Pull bank and account statements going back at least three years before you plan to file, and note any large deposits, withdrawals, sales, or transfers.

- Sort each big item into "necessary" or "questionable." Rent, food, medical, and other allowable expenses are defensible. Travel, gifts, and luxury purchases are the items the IRS will flag.

- Gather proof for the necessary spending. Receipts, invoices, lease agreements, and hospital bills turn a suspicious withdrawal into a documented, allowable expense.

- Pin down the assessment dates. If you spent an asset before the tax for that year was assessed, the IRS shouldn't add it back. Your account transcript shows when each balance was assessed.

- Explain it inside the offer. Don't wait to be asked. Attach a short statement and your documents with the Form 656 package so the examiner sees the full story up front.

- Appeal an unfair add-back. If an examiner still counts money you can prove was spent on essentials, you have the right to appeal the determination before the offer is finalized.

How this fits the bigger OIC picture

A dissipated asset add-back is one of several ways an offer can fall apart. It pairs closely with the rules on doubt as to collectibility and the math behind how an Offer in Compromise actually works. The common thread: the IRS settles for less only when its own numbers say it can't collect more — and spent assets are one of the first things it tests. You can read the program rules straight from the source on the IRS's Offer in Compromise page and in the Form 656 booklet. If a determination feels wrong and you can't get it fixed, the Taxpayer Advocate Service is an independent option.

Dissipated assets OIC questions, answered

What are dissipated assets in an Offer in Compromise?

Dissipated assets are money or property you owned during a tax year you owed the IRS but spent, gave away, or transferred for less than fair value instead of paying down the debt. When the IRS believes you should have used that money on your taxes, it may add the value back into your offer calculation as if you still had it.

How far back does the IRS look for dissipated assets?

There is no fixed rule, but the IRS generally reviews the three years before you filed your offer, plus the period after the tax was assessed. Examiners focus on large or unusual withdrawals, transfers to family, and money spent on non-essentials while a balance was owed. Normal living expenses are not dissipation.

Can the IRS really count money I already spent?

Yes, in limited situations. If you spent or gave away assets you could have used to pay the IRS — and the spending was not for ordinary living expenses — the IRS may add that value back to your reasonable collection potential. You can challenge an add-back by showing the money went to necessary expenses or was spent before you owed the tax.

How do I fight a dissipated asset add-back on my OIC?

Document where the money went. Bank statements, receipts, and proof that funds covered rent, food, medical care, or other allowable living expenses can defeat an add-back. You can also show the asset was spent before the tax was assessed, or appeal the determination if the examiner refuses to remove it.

Does spending my 401(k) before an OIC count as dissipation?

It can. If you cashed out a retirement account while owing the IRS and spent the proceeds on non-essential items, the examiner may add that value back. If the money went to allowable living expenses, medical bills, or keeping a roof over your head, document it — necessary spending is generally not treated as dissipation.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.