Tax Debt by Amount

I Owe the IRS $100,000: What Happens Next and Every Real Option (2026)

The short answer: if you owe the IRS $100,000, you're above every streamlined threshold — no online payment plan, over the $66,000 passport-certification line, and in likely lien and revenue-officer territory. Resolution now runs through full financial disclosure on Form 433: an installment agreement, partial-pay plan, Offer in Compromise, or hardship status.

Maybe it's two or three tax years stacked together — a strong self-employment year with no estimated payments, a joint return that came up short, penalties compounding on top — and now the total next to your and your spouse's names has six digits. That number is jarring, and it's supposed to be. But "I owe the IRS $100,000" is a solvable problem with a known playbook, and the people who come out fine are the ones who run it before the automated system runs its own.

This page covers what is specifically different at $100,000. The general mechanics of every IRS program are in our guide to how to settle tax debt yourself — here, we focus on the thresholds you've crossed and the moves that still work above them.

⏱ The clock that's already running: there is no single deadline on a six-figure balance — the cost is continuous. On $100,000, the 0.5% monthly failure-to-pay penalty alone adds roughly $500 every month, interest compounds daily on top of it, and because you're above the $66,000 passport threshold, certification to the State Department can happen at any point once notices go unanswered.

What changes when you owe the IRS $100,000

A $100,000 IRS balance sits above every self-service threshold the IRS offers, including the $50,000 online payment-plan cap and the $66,000 passport-certification line. Below those lines, resolution is largely a formality. Above them, the IRS wants to see your finances before it agrees to anything — and it reserves the right to look at your assets first.

Here is where $100,000 lands on the IRS's own ladder:

| Balance | What the IRS offers | What it means for you |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement | Near-automatic approval, no financial disclosure |

| $10,001–$25,000 | Streamlined agreement | Simple setup, no Form 433 |

| $25,001–$50,000 | Streamlined with direct debit; online plan up to 72 months | Still no financials if you use direct debit |

| $50,001–$99,999 | Non-streamlined agreement — Form 433 required | Payment set by your financials; passport risk above $66,000 |

| $100,000+ | Full financial review; shorter pay windows on notices; possible revenue officer | Lien filing near-standard; the IRS may ask about borrowing against assets first |

Three practical consequences follow. First, you cannot set this up online — an IRS payment plan over 100k goes through a phone call or a revenue officer, supported by a Collection Information Statement. Second, at $100,000 the pay-by window on a first bill shrinks: a CP14 typically allows 21 days, but on balances of $100,000 or more it's typically only 10 business days. Third, you're already more than $30,000 past the passport line, so travel documents are genuinely in play if notices go unanswered.

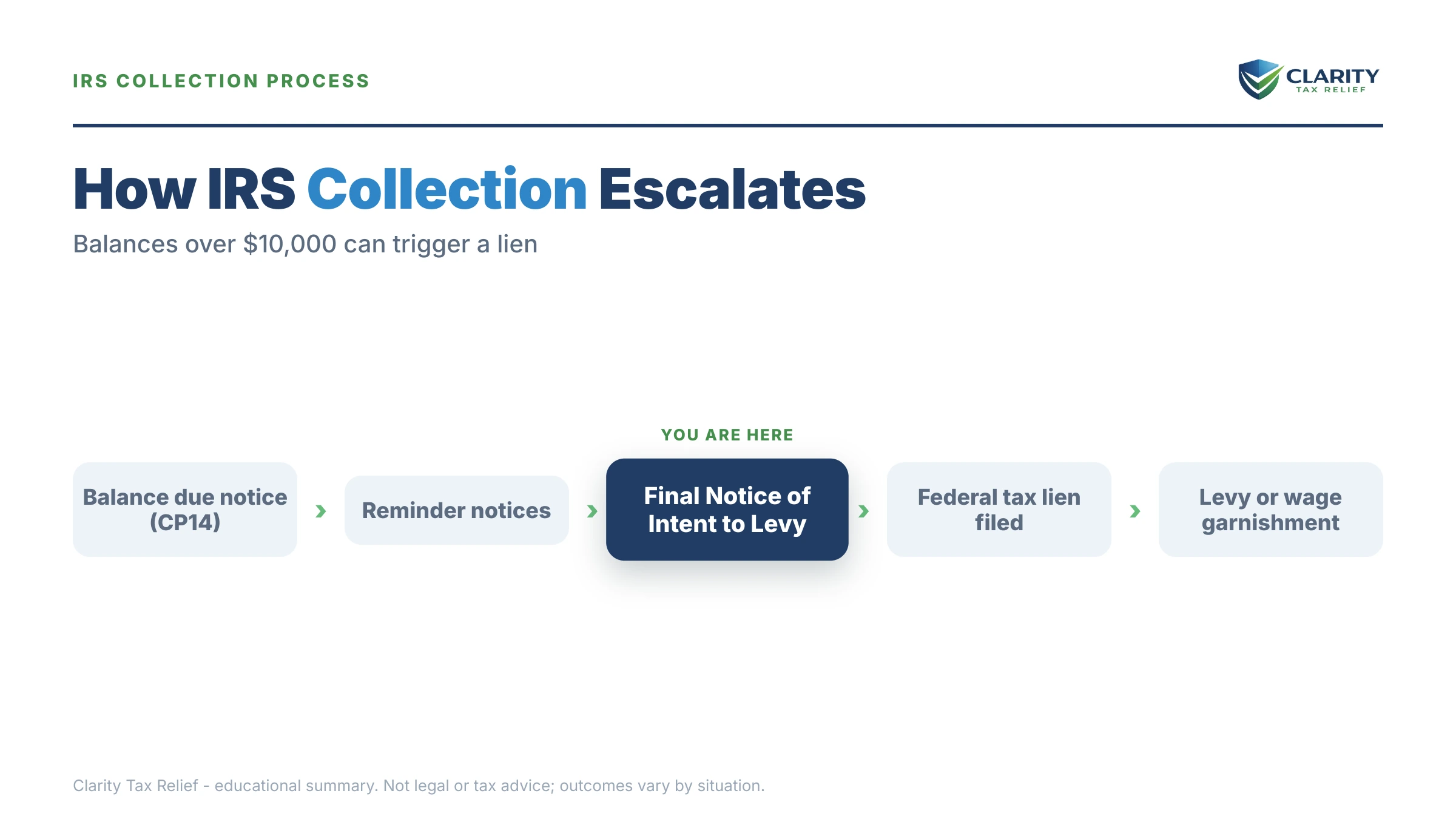

What happens if you ignore a $100,000 tax debt

An unanswered six-figure balance moves through the IRS collection sequence automatically, and each stage removes an option you have today. In 2026 the IRS workforce is down roughly 27% from the 2025 cuts — which makes humans harder to reach but changes nothing about the automated notices, liens, and levies. The sequence runs whether or not anyone at the IRS ever reads your file:

- CP14 — first bill. The cheapest moment to act. Penalties and interest are already accruing, but no enforcement exists yet.

- CP501 / CP503 — reminders. Typically weeks apart. Still just bills, but at this balance each cycle adds four figures in penalties and interest.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and a Notice of Federal Tax Lien becomes likely — a public record that attaches to everything you own, including a jointly owned home.

- LT11 / Letter 1058 — final notice of intent to levy. This starts a hard 30-day clock. Inside it, you can demand a Collection Due Process hearing with Form 12153, which pauses levy action. Miss it and the IRS can levy without further warning.

- Enforcement. A bank levy freezes funds with a 21-day hold before the bank sends them to the IRS. A wage levy is continuous — it repeats every paycheck until released. In parallel, a CP508C can certify your debt to the State Department for passport denial, and at this dollar level a local revenue officer may take the case for in-person collection and asset review.

Notice what happens along that path: at the top, you choose the resolution. At the bottom, the IRS chooses it for you.

Facing a six-figure IRS balance right now?

Above $100,000, the order you do things in — returns, penalty relief, then the balance — changes what you ultimately pay, and you're already past the passport-certification threshold. Get a free, confidential review of exactly where your account stands before the next notice escalates it.

Your options when you owe the IRS $100,000

Every IRS resolution program is still available at $100,000 — what changes is that each one now requires proof, in the form of a Collection Information Statement. Here is the full menu, with what each costs and what disqualifies you:

| Option | What it takes at $100,000 | Cost / catch |

|---|---|---|

| Pay in full (or borrow to) | Liquidity or credit — HELOC, retirement loan, asset sale | Stops penalties immediately; compare loan cost vs. IRS accrual |

| Pay down below $50,000, then online plan | A lump sum big enough to cross under the streamlined line | Unlocks a 72-month online plan with no Form 433 |

| Non-streamlined installment agreement | Form 433-F or 433-A; all returns filed; often Form 9465 to request | Setup fee (lower with direct debit); interest and penalties continue |

| Partial-payment installment agreement (PPIA) | Financials showing you can't full-pay before the CSED | IRS periodically re-reviews your finances; lien likely stays |

| Offer in Compromise | Reasonable Collection Potential below the balance; Forms 656 + 433-A(OIC) | $205 fee, 20% down on lump-sum offers (waived with low-income certification); ~1 in 5 accepted in FY2024 |

| Currently Not Collectible | Proof that any payment creates genuine hardship | Pauses collection, not the debt; refunds offset; lien likely |

| Penalty relief (FTA / AEP / reasonable cause) | Clean prior 3 years, or documented cause | Free to request; can cut a five-figure slice off a $100k balance |

The installment routes

A non-streamlined installment agreement is the workhorse at this level. You document income, expenses, and assets — our Form 433-A walkthrough shows exactly what the IRS counts — and the payment is negotiated from what the numbers support, measured against IRS allowable living expense standards, not your actual lifestyle. Expect the IRS to ask whether home equity or retirement funds could pay some of the debt first.

If the honest math shows you can't full-pay before the collection statute expires, a partial payment installment agreement lets you pay what you can afford, with whatever remains at the CSED expiring. The trade: the IRS re-examines your finances periodically and raises the payment if your income grows.

The settlement route

An Offer in Compromise turns on one number: your Reasonable Collection Potential — asset equity plus a multiple of your monthly ability to pay. If your reasonable collection potential is genuinely below $100,000, an offer near that RCP figure is viable; if you have substantial equity or surplus income, it isn't, no matter what late-night ads suggest. You can estimate your own numbers with our Offer in Compromise Calculator before spending anything. Two honest data points: the IRS accepted roughly 1 in 5 offers in FY2024, and an offer the IRS doesn't decide within 2 years is accepted by default.

The pause and the discount

Currently Not Collectible status stops levies when your financials show that paying anything would leave you unable to cover basic living expenses — the balance stays and grows, but collection sleeps. And regardless of which route you take, penalty relief belongs in the plan: first-time penalty abatement can wipe the failure-to-pay penalty for a clean-compliance year, and starting summer 2026 the new Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. On a balance this size, penalties are often a five-figure component — the single cheapest dollar reduction available.

A worked example: married couple, $113,600 balance

Say you and your spouse, filing jointly, owe $113,600 across two tax years — one big self-employment year with no estimated payments, plus underwithholding the following year. Here's how the three main routes actually price out (hypothetical numbers, shown so you can run your own):

- Straight installment agreement: $113,600 ÷ 72 months ≈ $1,578/month before ongoing interest and penalties, which keep accruing until paid. Because you're over $50,000, this requires Form 433 financials — and the IRS may set a different number than the simple division.

- Pay-down route: if you can raise $63,600 from savings or borrowing, the remaining $50,000 qualifies for a streamlined online plan — roughly $695/month over 72 months, no financial disclosure. Dropping under $66,000 also takes you back below the passport-certification threshold.

- Offer route: suppose your reachable asset equity totals $30,000 and your monthly income exceeds IRS allowable expenses by $200. Lump-sum RCP ≈ $30,000 + ($200 × 12) = $32,400. Because $32,400 is far below $113,600, an offer near that figure is mathematically possible — but only if those numbers survive IRS verification of every account, vehicle, and pay stub.

Same debt, three very different monthly realities. Which one is right depends entirely on the financial statement — which is why running the 433 math first, before calling the IRS, is the highest-leverage hour you'll spend.

Deadlines and rights: the notices a $100,000 balance generates

Each notice in the sequence carries its own response window, and each window protects a specific right. This is the reference card:

| Notice / event | Response window | The right at stake |

|---|---|---|

| CP14 (first bill) | Pay-by date printed — typically 21 days, often 10 business days at $100,000+ | Resolving before the escalation queue starts |

| CP504 (intent to levy state refund) | The date printed on the notice | Your state refund; lien filing becomes likely after |

| LT11 / Letter 1058 (final notice) | 30 days | Collection Due Process hearing via Form 12153 — miss it and levies can begin |

| CP508C (passport certification) | Certification has already happened when it arrives | Passport issuance/renewal — reversed by entering a qualifying resolution |

| Bank levy served | 21-day hold before the bank remits funds | Your window to prove hardship or error and get the levy released |

The pattern to notice: every stage still has a lever — but each lever is smaller than the one before it. More on the passport mechanics specifically in our guide to passport revoked tax debt.

Married, self-employed, or multiple years: what changes the answer

On a joint return, both spouses are each fully liable for the entire $100,000 — the IRS can collect all of it from either of you, regardless of who earned the income. If the debt traces to income or errors you knew nothing about, innocent spouse relief can separate your liability — but it's a specific application with deadlines, not something the IRS offers on its own.

If part of the balance is self-employment tax, one requirement surprises almost everyone: every agreement requires current-year compliance. You must be making this year's quarterly estimated payments, or the installment agreement or offer defaults — the IRS won't formalize a plan for old debt while new debt is forming.

And when the $100,000 spans multiple years, each year has its own assessment date and its own 10-year expiration. That matters strategically: a payment plan can sometimes be structured so the oldest, closest-to-expiring years aren't inadvertently kept alive. The mechanics are in our guide to how long the IRS can collect back taxes.

How to Respond When You Owe the IRS $100,000, Step by Step

- Pull your full IRS balance. Log in to your IRS online account or request account transcripts to confirm the exact total — tax, penalties, and interest — for every year, not just the year on the latest notice.

- File every missing return. The IRS will not approve any agreement while returns are unfiled, and substitute returns the IRS files for you usually overstate what you owe.

- Run the Form 433 math before the IRS does. Draft a Form 433-A using the IRS allowable living expense standards so you know what monthly payment the numbers support — and whether an offer or hardship status is realistic.

- Open one resolution before the next notice lands. Set up the installment agreement, partial-pay plan, offer, or Currently Not Collectible request the math supports; a pending agreement or offer generally pauses levy action while it is reviewed.

- Protect your rights at every printed deadline. If a CP504, LT11, or CP508C arrives while you work, respond inside its window — an LT11 gives you 30 days to request a Collection Due Process hearing with Form 12153.

When you can handle this yourself — and when help changes the outcome

Some $100,000 cases are genuinely self-serviceable. If the debt is one or two agreed-upon years, your income is W-2, and you can either full-pay soon or pay down below $50,000 and set up the streamlined plan online, you don't need to hire anyone — the IRS's own payment plans page and Offer in Compromise page are the primary sources, and if you hit a wall inside the IRS itself, the independent Taxpayer Advocate Service exists for exactly that.

Experienced help earns its cost in the harder versions of this case: a levy already in motion, multiple unfiled years, business or payroll debt mixed in, a revenue officer assigned, a passport already certified, or an Offer in Compromise where the 433 presentation — which assets count, which expenses the IRS allows — swings the result by tens of thousands. At $100,000, the gap between a well-presented financial statement and a careless one is not a rounding error. It is the difference between a payment you can live with and one you can't.

Terms you'll see on your notices, decoded

- CSED — Collection Statute Expiration Date: the day, 10 years after assessment, when the IRS's legal right to collect a tax year ends (pausable by appeals, offers, and bankruptcy).

- RCP — Reasonable Collection Potential: the IRS's calculation of the most it could ever collect from you; the number every offer is measured against.

- Notice of Federal Tax Lien — a public filing that attaches the government's claim to everything you own; it secures the debt but takes nothing by itself.

- Revenue officer — a local IRS collection employee assigned to larger cases for in-person contact, financial review, and enforcement.

- PPIA — partial-payment installment agreement: a plan sized to your ability to pay rather than the full balance, with the remainder expiring at the CSED.

- CDP rights — Collection Due Process: your statutory right, triggered by a final notice, to a hearing that pauses levies while alternatives are considered.

Owe the IRS $100,000? Your questions, answered

Can I get a payment plan if I owe the IRS $100,000?

Yes, but not online. Above $50,000 the IRS requires a Collection Information Statement — Form 433-F or 433-A — documenting your income, expenses, and assets before approving an agreement. Your monthly payment is set by what those financials support rather than a fixed formula, and the IRS may first ask whether you can borrow against or liquidate assets.

Will the IRS settle a $100,000 tax debt for less than I owe?

Sometimes, through an Offer in Compromise — but only when your assets and future income genuinely cannot cover the balance before the collection statute runs out. The IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns entirely on the Reasonable Collection Potential math, not on how much you owe. Significant home equity or strong income usually sinks an offer.

Will I lose my passport if I owe the IRS $100,000?

You are over the line where it becomes possible. The IRS certifies seriously delinquent tax debt — $66,000 or more in 2026 — to the State Department, which can then deny a passport application or renewal and in some cases revoke one. Entering an installment agreement, an accepted offer, or a timely Collection Due Process hearing generally prevents or reverses certification.

Can the IRS take my house for a $100,000 tax debt?

A federal tax lien attaching to your home is likely at this balance, but an actual seizure of a primary residence is rare and requires court approval. The lien's practical effect is blocking a clean sale or refinance until it is addressed. The IRS's everyday enforcement tools are wage levies and bank levies, which need no court order.

Does a $100,000 IRS debt go away after 10 years?

The IRS generally has 10 years from assessment to collect, and unpaid balances do expire at the CSED — but appeals, offers, and bankruptcy pause that clock, and each tax year has its own expiration date. Waiting out six figures is rarely realistic because collection activity intensifies, not fades, as the deadline approaches.

Will a revenue officer be assigned if I owe the IRS over $100,000?

It is more likely at $100,000 than at smaller balances, though not automatic. Business or payroll debt, repeat non-filing, and growing balances raise the odds of a local revenue officer taking the case. Even with the IRS workforce down roughly 27% after the 2025 cuts, the automated system keeps issuing notices and levies while cases wait for assignment.

Can I go to jail for owing the IRS $100,000?

No — owing money to the IRS, even six figures, is a civil matter, not a crime. Criminal exposure comes from willful evasion, hiding assets or income, or filing fraudulent returns, not from an honest debt you cannot pay. Filing accurate returns on time and engaging with collection notices keeps a large balance firmly on the civil side.

Does owing the IRS $100,000 affect my credit score?

Not directly — the credit bureaus removed tax liens from credit reports in 2018, so the balance itself never appears there. A filed Notice of Federal Tax Lien is still a public record, though, and mortgage and business lenders search for it. Most underwriters will require a payment arrangement or lien resolution before approving new financing.

Your next 24 hours

- Pull the real number. Log in to your IRS online account and write down the exact balance for each tax year — tax, penalties, and interest separately. Decisions built on the notice you happen to be holding, instead of the full account, go wrong.

- Gather the Form 433 inputs. Your last filed return, recent pay stubs or a profit-and-loss if self-employed, bank and retirement balances, and your real monthly household expenses. This is the raw material for every option on this page.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will run your numbers against the installment, partial-pay, and offer math before another month of penalties and interest (roughly $500-plus at this balance) stacks on, and before passport certification narrows your options further.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.