Tax Debt by Amount

I Owe the IRS $15,000 — What to Do in 2026

The short answer: if you owe the IRS $15,000, you can typically set up a long-term payment plan online — up to 72 months, roughly $209 a month minimum — with no financial disclosure, as long as all your returns are filed. Do it before the notice stream reaches the levy stage.

You finished the return, hit calculate, and the software showed a five-figure balance you don't have sitting in the business account. If you're self-employed or run a small company, you already know how it got there — and you're now trying to figure out whether $15,000 is "payment plan" territory or "the IRS comes after my accounts" territory. It's the first one, if you act while the choice is still yours. Here's the full map.

⏱ The clock that's actually running: there's no single deadline attached to owing $15,000 — but the meter never stops. The failure-to-pay penalty adds 0.5% of your balance every month — $75 a month on $15,000 — and interest compounds daily on top. If you're holding a notice, the date printed on it controls your response window.

Why a $15,000 tax bill happens

A $15,000 IRS balance is most often one year of untaxed income, not years of neglect. Roughly $100,000 of self-employment profit with no quarterly payments can produce a bill in this range once you stack 15.3% self-employment tax on top of income tax.

The common paths here: a first strong year on Schedule C with no estimated payments, a 1099 contract alongside a W-2 job that under-withheld, a CP2000 that added unreported income to an old year, or an early retirement withdrawal that came with tax and a penalty. For a business owner, it can also be the personal side of a payroll problem — more on that below, because it changes the rules.

Whatever the cause, the balance itself now behaves the same way: it grows monthly, and the IRS's automated collection system works it on a schedule that doesn't care why you owe.

Where $15,000 sits on the IRS's own scale

The IRS treats tax debt in bands, and $15,000 lands in the most flexible one: above the $10,000 guaranteed-agreement ceiling but well under the $25,000 and $50,000 streamlined thresholds. That means you get the easy online plan, but you're past the point where approval is automatic by statute.

| Balance band | Payment plan access | What else changes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement — the IRS must accept if you meet the conditions | Lien filing is uncommon at this level |

| $10,000–$25,000 (you are here) | Streamlined installment agreement — up to 72 months online, no financial statement | Lien generally avoidable with a direct-debit plan |

| $25,001–$50,000 | Streamlined available, but direct debit is required to skip financials | Lien determinations get more likely |

| Over $50,000 | Full financial disclosure (Form 433 series); possible revenue officer | Passport certification at $66,000+ (2026 threshold) |

Two takeaways from that table. First, at $15,000 you are not in passport-revocation or revenue-officer territory. Second, the closer your balance drifts toward $25,000 through penalties and interest, the more paperwork and lien exposure you inherit — a reason to lock in an agreement while you're comfortably inside the band. (If your balance is actually closer to a neighboring figure, see the guides for people who owe the IRS $10,000 or owe the IRS $20,000.)

What happens if you ignore a $15,000 IRS balance

An unresolved $15,000 balance moves through an automated notice sequence that ends in levy authority — no human decides to escalate you. The stages run in a fixed order:

- CP14 — the first bill, with roughly 21 days to pay before the sequence continues (10 business days if the balance is $100,000 or more). No enforcement power yet.

- CP501 / CP503 — reminder notices. Still just bills, but the $75-a-month penalty and daily interest are compounding the whole time.

- CP504 — intent to levy your state tax refund under IRC §6331(d). This is also where a federal tax lien becomes a realistic next move — serious for anyone with business assets or plans to borrow. See the full CP504 guide.

- LT11 / Letter 1058 — the final notice. A 30-day clock starts, along with your Collection Due Process appeal rights (Form 12153). After day 30, the IRS can levy.

- Levy — a bank levy freezes funds for 21 days before they're sent to the Treasury; a wage levy is continuous until released. For a business owner, receivables and business accounts are reachable too.

| Notice | What it lets the IRS do | Your window |

|---|---|---|

| CP14 | Nothing yet — it's a bill | ~21 days from the notice date (10 business days if the balance is $100,000 or more) |

| CP501 / CP503 | Nothing new — pressure notices | The date printed on each notice |

| CP504 | Seize your state tax refund; lien filing likely on the table | The date printed on the notice |

| LT11 / Letter 1058 | Levy wages and bank accounts after the window closes | 30 days — also your CDP appeal deadline |

One 2026 reality worth naming: the IRS workforce shrank about 27% in 2025, so reaching a human is harder than ever — but the notices, liens, and levies come from systems that never got cut. Silence from the IRS is not the same as the case going quiet.

Staring at a $15,000 balance right now?

Every month you wait adds roughly $75 in penalty plus daily interest — and moves you one notice closer to levy authority. An experienced tax professional will map your fastest, cheapest way out in one free call: (888) 825-7779 or the 2-minute form.

Your options when you owe the IRS $15,000

Five real programs apply at $15,000, and which one fits comes down to your monthly cash flow — not to marketing promises. The general playbook for working these programs on your own lives in our guide to how to settle tax debt yourself; here's how each option looks at exactly this balance.

| Option | Fit at $15,000 | Upfront cost | What it does |

|---|---|---|---|

| Pay in full | Best if you can raise the cash — cheapest total outcome | $0 | Stops all penalty and interest accrual immediately |

| Short-term plan (up to 180 days) | Money is coming — a contract payout, a sale, a refund | $0 setup fee | Buys time; accrual continues but enforcement pauses |

| 72-month installment agreement | The default answer at this balance — ~$209/mo minimum | Setup fee (lowest online with direct debit) | Stops the notice stream; penalty rate is reduced while it's active |

| Currently Not Collectible | Only if paying anything creates genuine hardship (Form 433-F required) | $0 | Pauses collection; the debt and accrual remain |

| Offer in Compromise | Rare at $15,000 — only when income and assets can't cover the debt | $205 fee + 20% down on lump-sum (waived if AGI ≤ 250% of poverty) | Settles for less — the IRS accepted roughly 1 in 5 offers in FY2024 |

Two honest notes on that table. An OIC at $15,000 is genuinely uncommon: if you can afford about $209 a month, the IRS's collectibility math says you can pay in full over 72 months, and it will reject the offer. And "Currently Not Collectible" isn't a discount — the balance keeps growing while collection is paused, and the IRS reviews your finances periodically.

The sixth lever isn't a payment program at all: penalty relief can cut a meaningful slice off the balance itself. If your prior three years were clean, first-time penalty abatement can erase the failure-to-pay penalties that have accrued — and starting summer 2026, the IRS's Automatic Exemption from Penalty (AEP) begins applying that relief automatically, with no request needed. Reasonable-cause relief may apply for illness, disaster, or other events outside your control.

The $15,000 math, worked out

A hypothetical makes the choice concrete. Say you owe $15,000 from last year's Schedule C profit and set up nothing:

- Failure-to-pay penalty: 0.5% × $15,000 = $75 added every month, up to the statutory cap.

- Interest: compounds daily on the growing total, at the federal short-term rate plus 3 percentage points.

- After one year of drift, you've added roughly $900 in penalty alone before counting a dollar of interest — and you've moved several notices down the escalation ladder.

Now say you set up a direct-debit installment agreement instead:

- Minimum payment: $15,000 ÷ 72 months ≈ $209 a month.

- Penalty rate: the failure-to-pay penalty drops by half — to 0.25% a month — while an approved agreement is in effect ($37.50 a month at the starting balance, shrinking as you pay down).

- Enforcement: the notice sequence stops. No CP504, no LT11, no levy — as long as you don't miss payments or fall behind on new taxes.

- Paying $350–$400 a month instead of the minimum cuts years off the term and most of the accrual with it. You can estimate your own accrual with our Penalty & Interest Calculator.

The gap between those two paths — hundreds of dollars a year plus levy exposure versus a fixed, protected payment — is why the installment agreement is the default answer at this balance.

If your $15,000 is business payroll tax, the rules change

Payroll tax debt is the one kind of $15,000 the IRS refuses to treat casually, because the withheld portion is your employees' money held in trust. If your balance comes from unpaid Form 941 deposits rather than your personal 1040, three things are different:

- Personal exposure: the IRS can assess the trust-fund portion against you — and anyone else who controlled the money — personally through the Trust Fund Recovery Penalty. Closing or dissolving the business does not erase it.

- Different plan rules: the individual 72-month online plan doesn't apply to an operating business with payroll debt. Business agreements exist, but with their own thresholds and compliance conditions — starting with staying current on every new deposit from today forward.

- Faster escalation: payroll cases get assigned to revenue officers at lower balances than personal debt does, and repeated missed deposits draw the harshest scrutiny the IRS has.

If any part of your $15,000 traces to payroll, read the guide to 941 back taxes before you do anything else — the sequencing (deposits current first, then the back balance) matters more than the dollar amount.

When you can handle a $15,000 balance yourself

Most people with a clean, single-year $15,000 balance can resolve it without paying anyone. If all your returns are filed, you agree with the amount, and ~$209+ a month fits your budget, the online agreement takes about 20 minutes — our walkthrough on setting up an IRS payment plan online covers every screen. Add a first-time abatement request and you've likely done everything a pro would do.

Experienced help changes the outcome in specific situations: a levy or final notice already in motion, multiple unfiled years (the plan can't be approved until they're in), payroll or business debt with personal-liability exposure, a balance you dispute, or finances tight enough that CNC or an offer is genuinely on the table and the Form 433 presentation decides the result. In those cases the order of operations — returns, penalties, then the balance — is where money gets saved or lost.

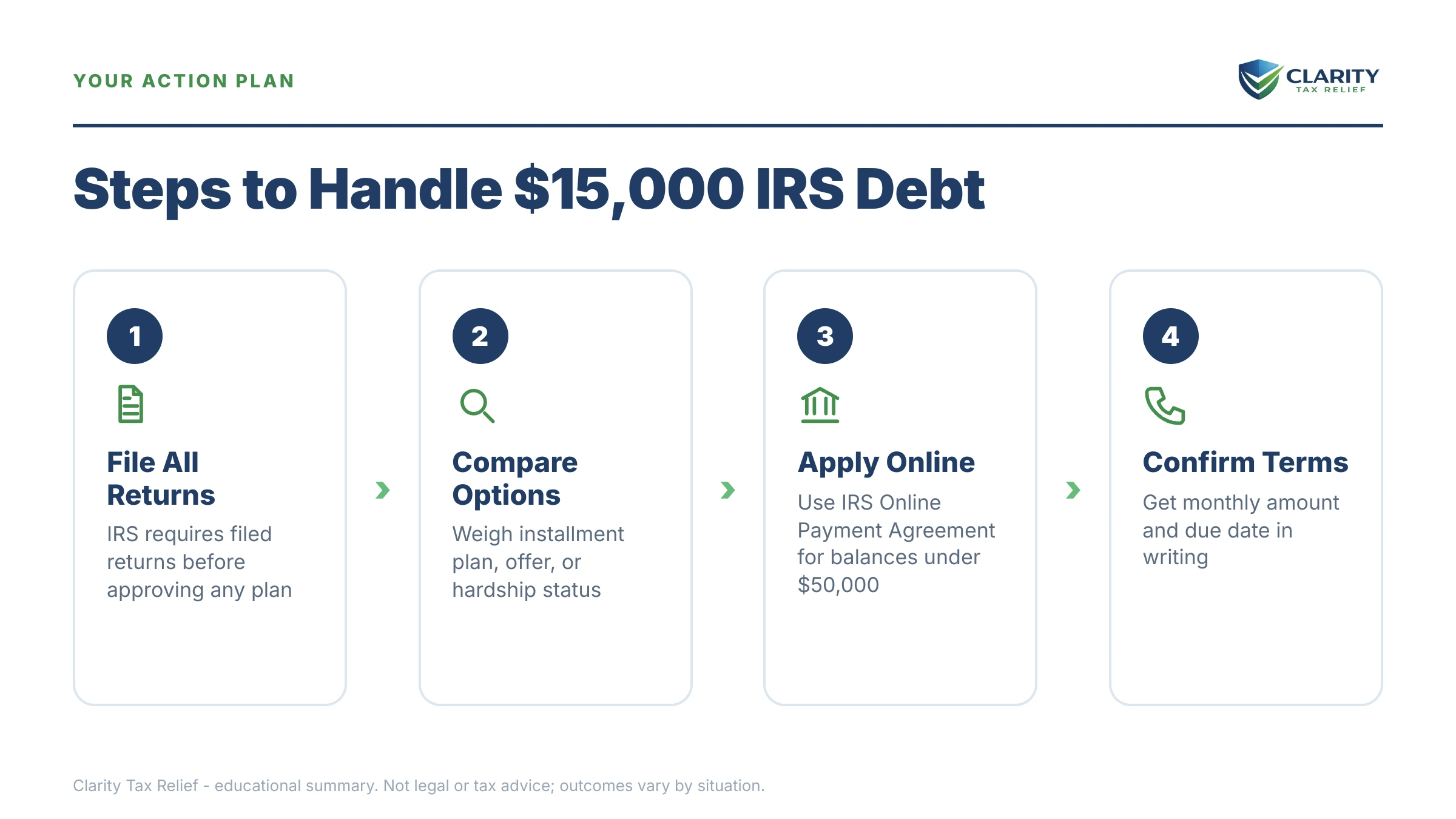

How to respond when you owe the IRS $15,000, step by step

- Confirm the real balance. Log into your IRS online account and compare the current total — with accrued penalties and interest — against the figure on your last notice.

- File any unfiled returns. The IRS won't approve a payment plan until every required return is in — and the failure-to-file penalty runs ten times the failure-to-pay penalty.

- Pick the option that fits your cash flow. Use the 180-day full-pay window if the money is coming, a 72-month plan if it isn't, and CNC or an Offer in Compromise only if your numbers genuinely support hardship.

- Set it up online before the next notice lands. Apply through the IRS Online Payment Agreement and choose direct debit — it carries the lowest setup fee and the lowest lien risk.

- Request penalty relief. If your prior three years are clean, ask for first-time abatement — and starting summer 2026, the Automatic Exemption from Penalty (AEP) may apply relief with no request at all.

If you'd rather pay in full or make a partial payment while you decide, every IRS payment channel is listed at IRS.gov/payments. And if the IRS's own process stalls your case — a levy despite a pending agreement, for instance — the independent Taxpayer Advocate Service exists for exactly that. If you're tempted to simply outlast the debt, understand how long the IRS can collect back taxes first — the 10-year clock pauses more often than people think.

Owe the IRS $15,000? Your questions, answered

How much is the monthly payment on $15,000 of IRS debt?

The minimum on a 72-month plan is about $209 a month ($15,000 ÷ 72), though interest and a reduced late-payment penalty keep accruing on the unpaid balance, so the total you repay is higher. The IRS will always accept more than the minimum, and every extra dollar shortens the accrual period. If your budget only supports less than roughly $209, you'll need to discuss a partial-payment plan or hardship status with the IRS instead.

Can I set up a payment plan for $15,000 online?

Yes — the IRS Online Payment Agreement covers individual balances up to $50,000 for terms up to 72 months, so $15,000 qualifies comfortably. The catch is compliance: every required return must be filed before the system will approve you. Choose direct debit when you apply; it carries the lowest setup fee and the lowest risk of a federal tax lien being filed.

Will the IRS file a tax lien if I owe $15,000?

It can, but at $15,000 a lien is usually avoidable. On streamlined direct-debit agreements for balances of $25,000 or less, the IRS generally does not file a Notice of Federal Tax Lien. The risk rises sharply if you ignore the notice stream — by the CP504 stage, a lien filing becomes a realistic next move, and it attaches to everything you own, including business assets.

Can I settle $15,000 with an Offer in Compromise?

Only if the IRS's own math shows it could never collect the full $15,000 from your income and assets before the collection statute runs out. The application costs $205 plus 20% down on a lump-sum offer (both waived if your AGI is at or below 250% of the poverty line), and the IRS accepted roughly 1 in 5 offers in FY2024. Most people who can afford around $209 a month will not qualify at this balance.

Will owing the IRS $15,000 affect my passport?

No — passport certification requires a seriously delinquent balance of $66,000 or more in 2026, and $15,000 is far below that line. Be aware the threshold applies to your combined assessed balances, so multiple unresolved years plus years of penalties and interest can eventually stack toward it. Levies, liens, and refund offsets still apply at $15,000; only the passport consequence is off the table.

Can the IRS garnish my wages or bank account over $15,000?

Yes — once the IRS issues a final notice (LT11 or Letter 1058) and 30 days pass, it can levy bank accounts and garnish wages at any balance, including $15,000. A wage levy is continuous until released; a bank levy freezes funds for 21 days before they're sent to the IRS. Getting into any payment arrangement before that final notice window closes is what prevents it.

What if my $15,000 is payroll (941) tax from my business?

Payroll tax debt is treated much more aggressively than personal income tax debt, because the withheld portion is your employees' money held in trust. The IRS can assess the trust-fund portion against you personally through the Trust Fund Recovery Penalty, even if the business closes. Business payment plans exist, but the thresholds and rules differ from the individual ones — don't assume the 72-month individual plan applies.

Does $15,000 of IRS debt go away after 10 years?

The IRS generally has 10 years from the date of assessment to collect, but the clock pauses during an Offer in Compromise, bankruptcy, and certain appeals — so the real deadline is often later than year ten. Waiting it out on a $15,000 balance means a decade of exposure to liens, levies, and refund offsets while penalties and interest grow. It is almost never cheaper than a payment plan.

Your next 24 hours

- Pull your exact balance. Log into your IRS online account (or grab the total from your most recent notice, including the date printed on it) so you're working from the real number, not the one on your return.

- Gather three things: your last filed return, any IRS notices you've received, and a rough monthly income-and-expenses figure — that's everything needed to pick between the 180-day window, the 72-month plan, and hardship options.

- Get a free case review. Bring those numbers to (888) 825-7779 or the 2-minute form and an experienced tax professional will map the cheapest resolution for your $15,000 — before another month of penalties and interest lands on it.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.