Tax Debt by Amount

I Owe the IRS $5,000 — What Do I Do? Every 2026 Option, Compared

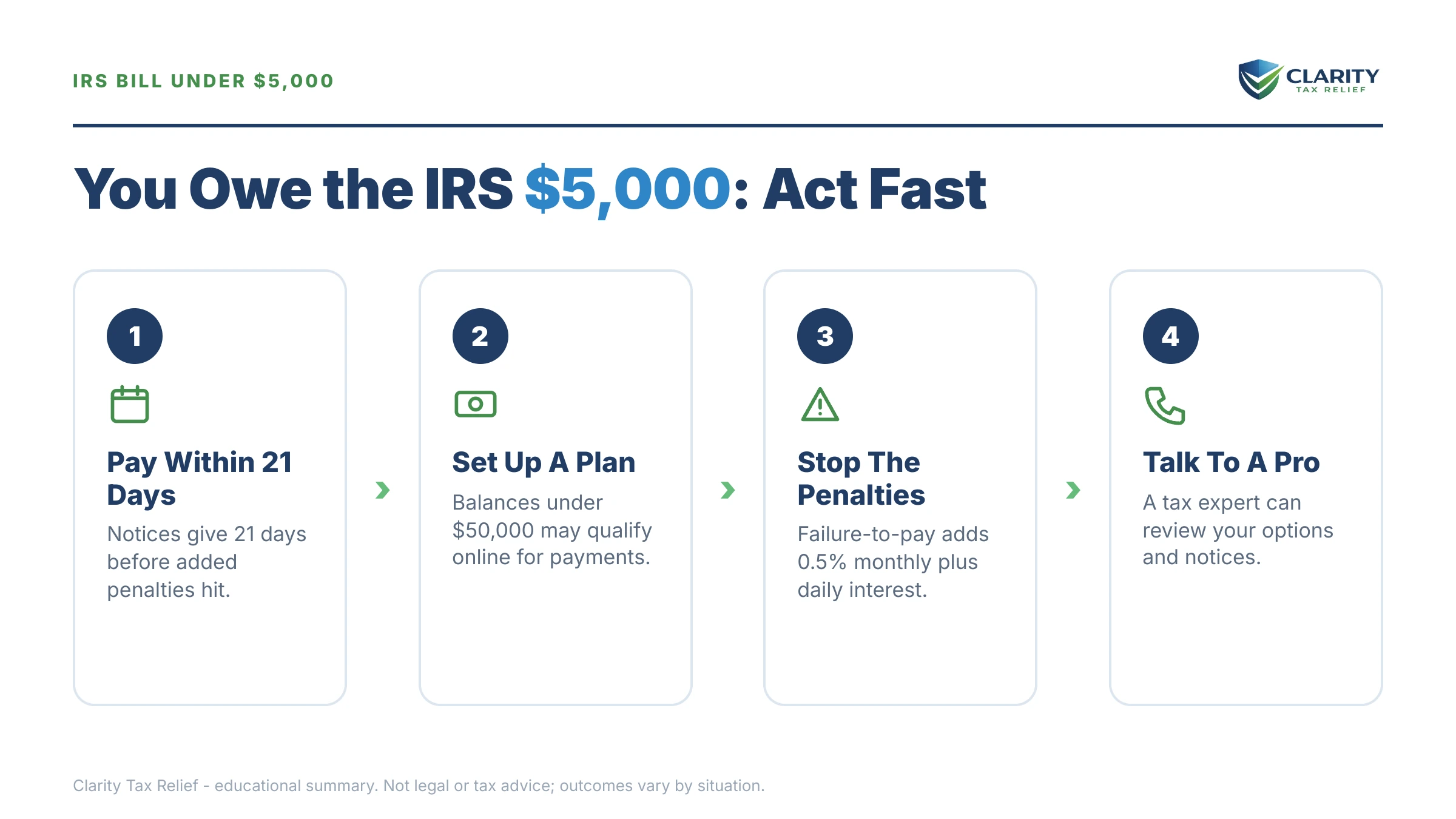

I owe the IRS $5,000 — what do I do? At $5,000 you're under the IRS's $10,000 guaranteed installment agreement threshold: the IRS must accept a monthly plan if you've filed all returns and can pay within three years. Set up that plan — or a free 180-day extension — before the notice cycle escalates and penalties keep compounding.

You've run the numbers twice hoping the software was wrong, and it wasn't: the IRS says you owe $5,000 you don't have sitting in checking. That sinking feeling is real — but at this exact balance, you hold more legal leverage than at almost any other. Under $10,000, the law requires the IRS to accept a reasonable monthly plan from you. You're also nowhere near passport trouble (that starts at $66,000 in 2026), and the IRS rarely files a lien at this level. This guide shows you how to use that leverage.

⏱ The real clock: there's no single deadline printed on a $5,000 balance — the cost is monthly. The failure-to-pay penalty adds 0.5% of the balance every month (about $25 on $5,000), and interest compounds daily on top. Every month you wait makes the fix more expensive than it had to be.

Why you owe the IRS $5,000

A $5,000 IRS balance almost always comes from one of four sources: under-withholding, a retirement-account withdrawal, untaxed side income, or an IRS adjustment to a return you already filed. It is a bill, not an audit — nobody is questioning your honesty.

The most common versions we see at this amount:

- A retirement distribution. You pulled money from an IRA or 401(k), the custodian withheld only 10%, and the withdrawal also made more of your Social Security taxable. The shortfall lands at filing time.

- Withholding that didn't keep up. A pension plus Social Security, two jobs, or a spouse's income pushed you into a higher bracket than any single payer withheld for.

- 1099 or side income with no quarterly payments behind it.

- An IRS recalculation — a CP2000 income match or math-error change that turned a small refund into a balance due.

If the number arrived on a letter rather than your tax software, it's usually a CP14 notice — the first bill in the IRS collection sequence, and the cheapest moment in that sequence to act.

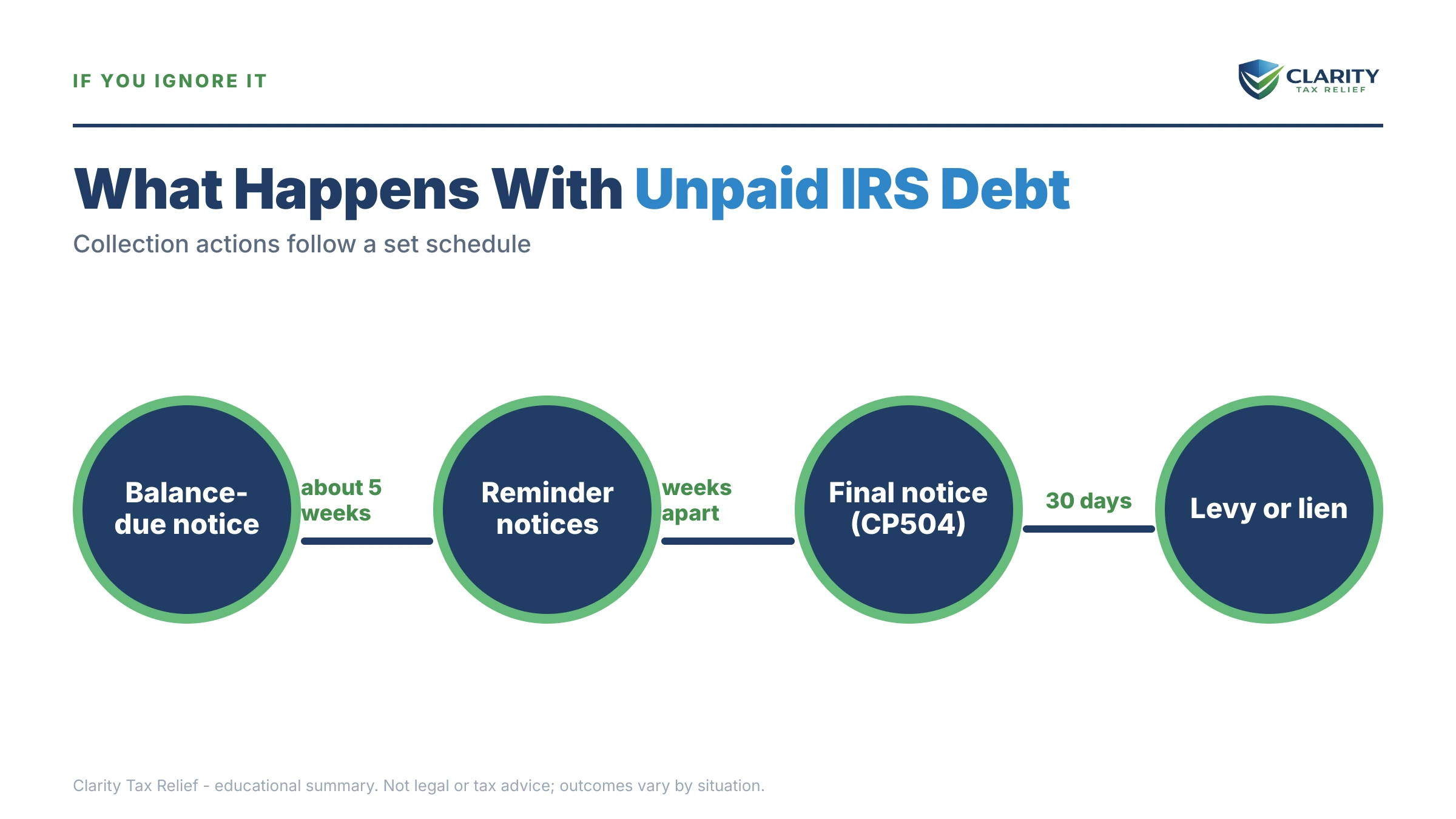

What happens if you ignore a $5,000 tax debt

An unpaid $5,000 balance triggers an automated notice sequence that ends with the legal power to levy bank accounts and take up to 15% of your monthly Social Security check. At this dollar level you'll almost never see a revenue officer at your door — the escalation is entirely machine-driven, which means it never forgets and never takes a month off, even with IRS staffing down sharply in 2026.

The sequence runs in this order:

- CP14 — the first bill. You typically have about 21 days from the notice date before the next stage queues up. No enforcement yet.

- CP501 and CP503 — reminders. Still just bills, arriving weeks apart while the balance grows monthly.

- CP504 — intent to levy your state refund. The IRS can now seize any state tax refund you're owed. This is not yet the final notice, but it's the last cheap exit.

- LT11 or Letter 1058 — the final notice. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After the 30 days, levies become legal.

- Enforcement. A bank levy freezes funds for 21 days before they're sent to the IRS; the Federal Payment Levy Program can attach up to 15% of Social Security benefits and keep taking it monthly. See can the IRS garnish Social Security for how that levy works and what stops it.

Two quieter consequences run in parallel the whole time: the IRS keeps every federal tax refund you're owed until the debt is gone, and penalties plus daily-compounding interest push the balance up each month. A $5,000 debt left alone for three years can grow well past $6,000 before any levy ever happens.

| Stage / notice | What it means | Your window |

|---|---|---|

| CP14 | First bill for the balance due | Typically about 21 days from the notice date |

| CP501 / CP503 | Reminder notices — no enforcement yet | Usually several weeks between each |

| CP504 | Intent to levy your state tax refund | The date printed on the notice controls |

| LT11 / Letter 1058 | Final notice — levies become legal after the window | 30 days, with appeal rights via Form 12153 |

| Levy | Bank levy (21-day hold) or up to 15% of Social Security | Continues until released or the debt is resolved |

Owe the IRS about $5,000 right now?

Before another month of penalties and interest posts, let an experienced tax professional review your balance, your notices, and which plan actually fits your budget — free, confidential, no pressure.

"I owe the IRS $5,000 — what do I do?" Your options, compared

A $5,000 IRS debt qualifies for every resolution program the IRS offers — and one that's essentially automatic at this level. The general playbook for resolving any balance on your own lives in our guide to how to settle tax debt yourself; here's how each option specifically plays at $5,000.

| Option | Do you qualify at $5,000? | Setup cost | The catch |

|---|---|---|---|

| Pay in full | Always | $0 | None — stops all penalties and notices immediately |

| Short-term plan (up to 180 days) | Yes — well under the limit | $0 | Needs roughly $833/month; interest and penalties still accrue |

| Guaranteed installment agreement | Yes, if returns are filed, no plan in prior 5 years, and full pay within 3 years | Setup fee (lowest with direct debit; waived or refunded for qualifying low-income taxpayers) | Interest and a reduced penalty continue until paid |

| Currently Not Collectible | Only if paying anything would prevent basic living expenses | $0 (financial disclosure required) | Debt remains and grows; refunds still offset |

| Offer in Compromise | Rarely worth it at $5,000 unless income and assets are genuinely minimal | $205 fee + 20% down (both waived with low-income certification) | ~1 in 5 offers accepted in FY2024; months of review |

| Penalty abatement | Yes, if the prior 3 years were clean (or via reasonable cause) | $0 | Removes penalties only — the tax itself remains |

The guaranteed installment agreement — your ace under $10,000

This is the fact that changes everything at your balance: under $10,000 in tax, the IRS is required to accept your monthly plan. The conditions are simple — all required returns filed, no installment agreement in the prior five years, a clean payment history over that stretch, and full payment within 36 months. $5,000 over 36 months is about $139 a month before penalties and interest. There's no financial disclosure, no negotiation, no judgment call by an IRS employee. Full details in our guaranteed installment agreement guide, and the setup itself takes about 15 minutes online — walkthrough at how to set up an IRS payment plan online.

A bonus most people miss: while an installment agreement is in effect, the failure-to-pay penalty drops from 0.5% to 0.25% per month. The plan doesn't just stop enforcement — it cuts the bleeding in half.

The 180-day short-term plan — free, if the cash is coming

If money is on the way — a CD maturing, a home sale, a required minimum distribution — the short-term plan gives you up to 180 days with $0 setup fee. Interest and the 0.5% monthly penalty continue, but the notice sequence stops. On $5,000, six months of accrual costs roughly $150 in penalty plus interest — cheap insurance against a levy.

Currently Not Collectible — when there's truly nothing to give

If your income barely covers rent, food, medicine, and utilities, Currently Not Collectible status pauses all collection — no levies, no garnishment — while the debt sits. You'll show income and expenses (often on Form 433-F). The balance keeps accruing interest and your refunds still get taken, but the pressure stops. For many people on fixed incomes, CNC quietly carries the debt toward the 10-year collection expiration.

Offer in Compromise — real, but rarely the answer at $5,000

An OIC settles the debt for what the IRS calculates it could realistically collect from you — not what you'd like to pay. It costs a $205 application fee plus 20% down on lump-sum offers (all waived if your income is at or below 250% of the federal poverty level), takes months, and the IRS accepted only about 1 in 5 offers in FY2024. On a $5,000 balance, the effort-to-savings ratio usually favors a payment plan — unless your finances are so limited that CNC or a low-income-certified offer genuinely fits.

Penalty relief — often the fastest $250+ you'll save

If the prior three tax years were clean — filed on time, paid on time, no penalties — first-time penalty abatement can wipe the failure-to-pay penalty from the balance with a single phone call or letter. And starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) begins applying this relief automatically, with no request needed — so check your account before assuming penalties are permanent. You can estimate what penalties and interest are adding to your balance with our IRS Penalty & Interest Calculator.

One sizing note: penalties and interest post monthly, so the number on your next notice may be higher than $5,000. If your true balance is closer to five figures, the strategy shifts — see our guides for when you owe the IRS $10,000 or owe the IRS $15,000, where the guaranteed-agreement threshold and lien math change.

A worked example: $5,000 owed on Social Security income

Say you're 71, your income is $2,150 a month in Social Security plus a small IRA, and last year you withdrew $25,000 from the IRA for a roof and dental work. The custodian withheld 10% — but the withdrawal also made most of your Social Security taxable, and at filing you owe $5,000. (This is a hypothetical, not a client story.) Here's the math on your three realistic paths:

- 180-day plan: $5,000 ÷ 6 ≈ $833/month. On $2,150 of monthly income, that's not survivable. Skip it.

- Guaranteed installment agreement: $5,000 ÷ 36 ≈ $139/month of principal. Set the payment at $150 to cover the reduced 0.25% monthly penalty and interest, and the debt clears in roughly three years at a total added cost in the ballpark of $600–$750, depending on the quarterly interest rate.

- Doing nothing: $25/month in penalty plus compounding interest, every refund taken, and — once the final notice window closes — a Federal Payment Levy Program levy of 15% of your Social Security: about $322 a month, more than double the payment plan, taken without your consent.

Same debt, three outcomes: $150 on your terms, or $322 on the IRS's. Then fix the cause — Form W-4V lets you add voluntary withholding to Social Security so next April doesn't repeat this one.

What to do if you owe the IRS $5,000 but can't pay anything

If your budget genuinely has no room — not "tight," but nothing left after essentials — the IRS cannot lawfully levy you into hardship. Section 6343 requires releasing levies that prevent basic living expenses, and CNC status exists precisely for this situation. If Social Security is your main or only income, start with our guide to IRS hardship while on Social Security; retirees carrying older balances should also see retired and owe back taxes for how fixed-income cases usually resolve.

Two protective facts worth knowing before you panic: the FPLP levy on Social Security is capped at 15% of the benefit — the IRS cannot take your whole check through that program — and no Social Security levy happens at all before the final-notice stage and its 30-day window. If you're already past that point, the Taxpayer Advocate Service (linked below) can intervene when collection is causing hardship, at no cost.

How to respond to a $5,000 IRS balance, step by step

- Confirm the balance is real and right. Log into your IRS online account and match the balance, tax year, and penalty breakdown against your own return before you pay or agree to anything.

- Ask for penalty relief first. If you've filed and paid on time for the prior three years, request first-time penalty abatement before setting up a plan — a smaller balance means smaller payments.

- Choose your payment path. Pay in full if you can, take the free 180-day short-term plan if you can clear it within six months, or lock in a guaranteed installment agreement of roughly $139–$150 a month if you can't.

- Set it up online. Use the IRS Online Payment Agreement tool — approval is typically immediate at this balance — or mail Form 9465 if you can't verify your identity online. Details on both are at the IRS payment plans page, and one-time payments go through IRS.gov/payments.

- Protect the agreement. File every future return on time and fix your withholding so no new balance appears — a new unpaid year defaults an existing plan.

When you can handle a $5,000 balance yourself — and when help changes the outcome

Honest answer: most $5,000 cases are DIY-friendly, and you should know that before anyone quotes you a fee. If the balance is correct, your returns are filed, and a $139–$150 monthly payment fits your budget, the guaranteed installment agreement plus a first-time abatement request is something you can complete yourself in an afternoon — no professional required.

Experienced help earns its cost in the exceptions:

- A levy is already in motion — your bank account is frozen or Social Security is being reduced, and the release needs to happen inside the 21-day bank-levy window.

- You dispute the amount — the balance came from a CP2000 or an IRS-filed substitute return, and the real fix is correcting the assessment, not paying it.

- Multiple years are unfiled — the order you file and resolve them changes the total, and a payment plan can't start until the returns are in.

- Hardship paperwork — building a CNC or low-income OIC case on a fixed income involves financial disclosure where the allowable-expense math decides everything.

If money is the barrier to getting help at all, the Taxpayer Advocate Service and Low Income Taxpayer Clinics offer free assistance for qualifying taxpayers.

Terms you'll see, decoded

- Installment agreement: the IRS's formal name for a monthly payment plan.

- Guaranteed installment agreement: the plan the IRS must accept on balances of $10,000 or less when the basic conditions are met.

- Failure-to-pay penalty: 0.5% of the unpaid tax per month (reduced to 0.25% while a plan is active), on top of interest.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

- FPLP: the Federal Payment Levy Program, which can take up to 15% of federal payments such as Social Security after the final notice.

- Refund offset: the automatic seizure of your tax refunds each year until the balance is paid.

Owe the IRS $5,000? Your questions, answered

Can I get a payment plan if I owe the IRS $5,000?

Yes — at $5,000 you sit under the $10,000 guaranteed installment agreement threshold, so the IRS must accept a monthly plan if you've filed all required returns, haven't had a plan in the prior five years, and agree to pay within three years. That works out to roughly $139 a month before penalties and interest. You can usually set it up online in about 15 minutes without submitting any financial documents.

Will the IRS garnish my Social Security over $5,000?

It can, but not without warning. The Federal Payment Levy Program lets the IRS take up to 15% of Social Security benefits, and only after the collection notice sequence ends with a final notice of intent to levy and a 30-day window. Setting up any payment arrangement — or qualifying for hardship status — takes you off the levy path entirely.

Will the IRS put a lien on my house for a $5,000 tax debt?

It's unlikely at this balance. The IRS typically reserves federal tax lien filings for larger debts — generally $10,000 and up — and a $5,000 case handled through a payment plan almost never sees one. Ignore the balance long enough for penalties and interest to push it higher, though, and a lien becomes a realistic risk.

Can I settle a $5,000 IRS debt for less with an Offer in Compromise?

Only if your finances genuinely can't cover $5,000 before the 10-year collection statute expires — and at this balance the math rarely works. An OIC costs a $205 application fee plus 20% down on lump-sum offers (both waived with low-income certification), and the IRS accepted roughly 1 in 5 offers in FY2024. Most people with $5,000 debts resolve them faster and cheaper with a payment plan plus penalty relief.

How fast does a $5,000 IRS debt grow?

The failure-to-pay penalty adds 0.5% per month — about $25 on a $5,000 balance — and interest compounds daily on top at the IRS's quarterly rate. If the balance comes from a return you haven't filed yet, the failure-to-file penalty runs 5% per month, ten times higher, which is why filing always comes first even when you can't pay a dime.

Does owing the IRS $5,000 affect my credit score or passport?

No on both counts. The credit bureaus removed tax liens from credit reports years ago, so IRS debt doesn't appear on your credit file at all. Passport certification only applies to seriously delinquent debts above $66,000 in 2026 — more than thirteen times your balance. Where a $5,000 debt does bite is refunds: the IRS keeps yours every year until the balance is gone.

What happens if I never pay the IRS the $5,000?

The IRS has 10 years from assessment to collect, and it uses them: your refunds are offset every year, penalties and interest compound monthly, and after the final notice the IRS can levy bank accounts and up to 15% of Social Security. The 10-year clock also pauses during appeals, offers, and bankruptcy, so waiting it out usually takes longer and costs more than a $139-a-month plan.

Your next 24 hours

- Pin down the exact number. Log into your IRS online account (or find the "Amount due" box on your most recent notice) and write down the balance, the tax year, and how much of it is penalty versus tax.

- Gather three things: your last filed return, any IRS letters you've received, and a rough monthly budget — income against essential expenses. That's everything needed to pick the right plan.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your $5,000 balance to the cheapest resolution before another month of penalties and interest posts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.