Tax Debt & Your Life

Can I Buy a House If I Owe the IRS? What Lenders Require in 2026

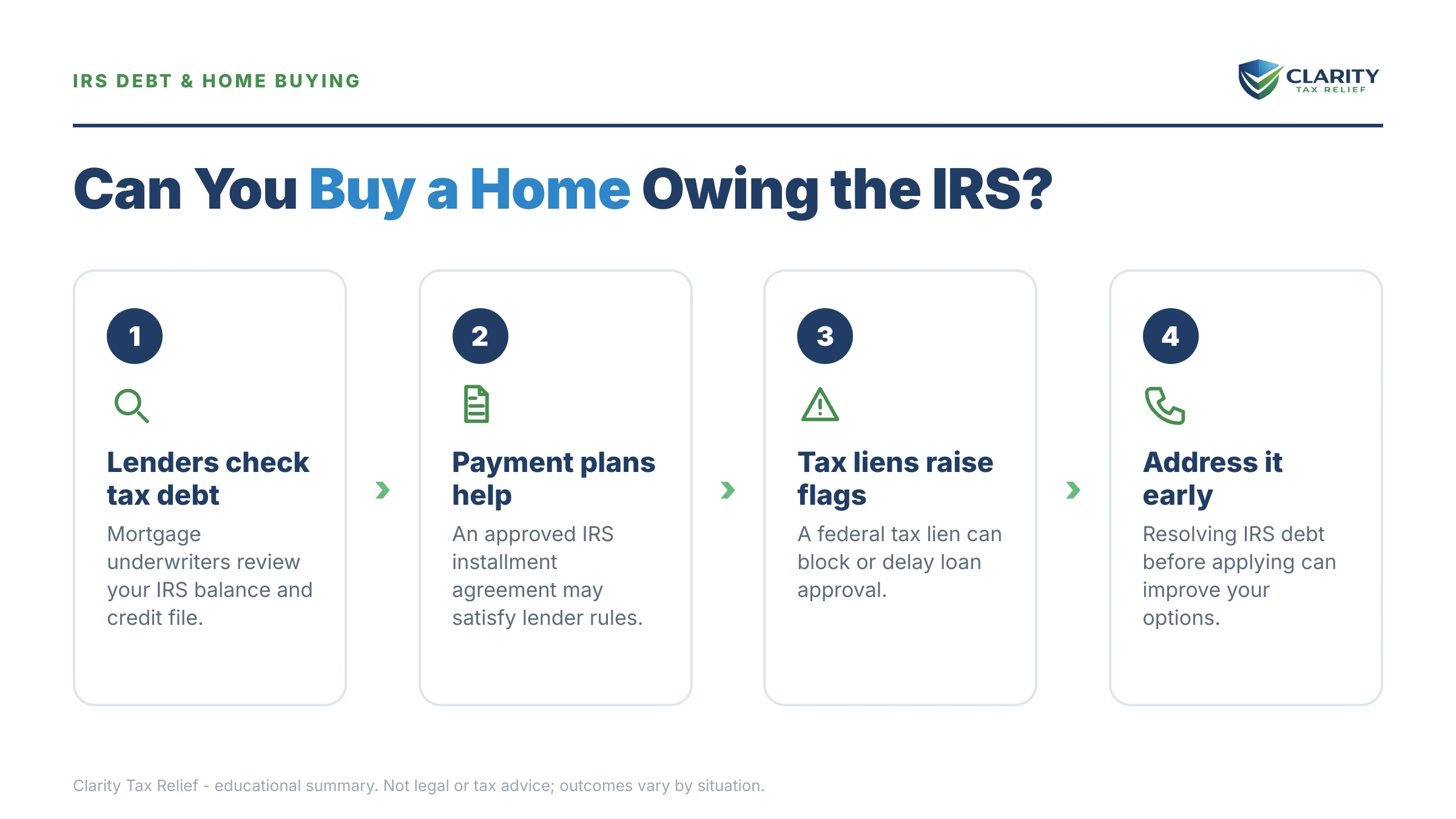

The short answer: yes — you can buy a house if you owe the IRS, as long as no federal tax lien has been filed and you're in a payment arrangement. Lenders routinely approve borrowers with IRS debt on an installment agreement; a filed Notice of Federal Tax Lien is what blocks financing.

You've been pre-qualified, you've found the neighborhood, and then the loan officer asks the question you were hoping to dodge: "Any federal tax debt?" You do — from a couple of strong self-employment years where the quarterlies didn't quite get paid. The good news: this is a sequencing problem, not a disqualification. Set the IRS up correctly before underwriting, and the debt becomes a line item in your debt-to-income ratio instead of a denial letter.

⏱ The real clock: there's no printed deadline on this decision, but interest and a 0.5% monthly failure-to-pay penalty are added to your balance every month you wait — and the longer a balance sits unresolved, the more likely the IRS files the Notice of Federal Tax Lien that turns a workable mortgage file into a denial.

Can I buy a house if I owe the IRS? What lenders actually check

Owing the IRS does not automatically disqualify you from a mortgage — a filed Notice of Federal Tax Lien is what does. That distinction is the entire strategy: keep the debt in "balance due, being repaid" territory and out of "public lien on record" territory.

Since 2018, tax debt doesn't appear on your credit report at all — the three bureaus stopped reporting tax liens entirely (here's how IRS debt affects your credit score). So how does a lender find out? Three ways:

- The application asks. Federal debt is a direct question, and misstating it on a mortgage application is fraud — never worth it.

- Form 4506-C transcripts. Your lender pulls your tax return transcripts directly from the IRS to verify income. Balances and unfiled years surface here whether you mention them or not.

- Public-records search. Title and underwriting search county records, where a filed Notice of Federal Tax Lien lives. No lien filed, nothing to find.

The practical takeaway: disclosure plus a payment plan is a routine mortgage file. Concealment plus a surprise in underwriting is a dead one.

Getting a mortgage with IRS debt: FHA vs. conventional rules

Conventional and FHA loans treat IRS debt differently, and knowing which lane you're in changes your prep timeline. Under current agency guidelines, conventional (Fannie Mae) loans generally accept delinquent federal tax debt when you have an approved IRS installment agreement, no lien has been filed, and the monthly payment is counted in your debt-to-income ratio.

FHA takes a slightly harder line: you need a valid repayment agreement and a history of timely payments under it — lenders typically look for at least three consecutive on-time payments, and you can't prepay three at once to shortcut the clock. VA and USDA lenders generally want the same thing: a documented plan and a clean payment record on it.

Two caveats. First, individual lenders layer their own overlays on top of agency minimums — some want the balance paid entirely, so shop more than one. Second, guidelines get updated; treat this as the map, and let your loan officer confirm the current edition. What no lender waives is the transcript pull, which is where the next section becomes the whole ballgame.

The self-employed complication: your tax returns are your paycheck stub

For a self-employed borrower, filed tax returns aren't just a compliance item — they're the only proof of income the lender will accept. Underwriters typically want two years of filed returns, verified against IRS transcripts, and they qualify you on your net Schedule C profit, not your gross deposits.

That creates three traps that W-2 buyers never face:

- An unfiled year is a hard stop. If last year's return isn't filed, there's no transcript to verify, and the file goes nowhere. File it even if you can't pay the balance it creates — a filed-but-owed year is workable; an unfiled one is not. (Behind by more than one year? Start with what to do when you haven't filed in 3 years.)

- Aggressive write-offs cut both ways. Every deduction that shrank your tax bill also shrank the income your lender can count. The return that created a small balance due may also be the return that limits your loan size.

- Current-year quarterlies matter. A lender seeing old IRS debt will ask whether this year's estimated payments are being made — otherwise you're building next year's problem while borrowing against this one.

What happens if you ignore the IRS debt while house-hunting

An unresolved IRS balance doesn't sit still while you shop for houses — it moves through an automated collection sequence, and each stage makes the mortgage harder:

- CP14 — the first bill. You typically have about 21 days from the notice date (10 business days if the balance is $100,000 or more) before the sequence advances. At this stage nothing touches your mortgage file except the DTI math.

- CP501 / CP503 — reminders. Still just bills, but the balance grows monthly with interest and the failure-to-pay penalty.

- CP504 — intent to levy your state refund. The IRS can now take your state tax refund, and the account is flagged for harder enforcement.

- Notice of Federal Tax Lien. This is the stage that changes everything for a homebuyer. A filed lien is a public record, attaches to property you own or later acquire, and moves you from "approvable with a plan" to fighting for withdrawal or subordination before any closing. (Here's what a federal tax lien on your house actually does.)

- LT11 / Letter 1058 — final notice of intent to levy. A 30-day clock starts on your Collection Due Process rights. After it, the IRS can levy bank accounts — including the savings account holding your down payment, with a 21-day hold before the funds leave.

One 2026 reality worth knowing: per TIGTA reports, the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but these notices, liens, and levies are generated by automated systems that never stopped running. The machine escalates on schedule whether anyone reads your file or not.

Trying to buy a home with an IRS balance hanging over the deal?

Get your balance, transcripts, and lien status reviewed free before you apply — the order you fix things in decides whether underwriting says yes. Interest and penalties are accruing either way.

Your options: matching the IRS fix to the mortgage you want

Every IRS resolution option affects a mortgage application differently, and some that sound appealing (like an Offer in Compromise) actually work against a near-term purchase. The general playbook for each program lives in our guide to how to settle tax debt yourself; here's how each one plays specifically at the closing table:

| Option | Typical eligibility | What it means for your mortgage |

|---|---|---|

| Pay in full | Anyone with the cash | Cleanest file — but weigh it against draining your down payment and reserves, which lenders also scrutinize |

| Short-term plan (up to 180 days) | Can clear the balance within 180 days; $0 setup fee | Works if the payoff lands before closing; some lenders still want the debt fully resolved or in a formal agreement |

| Streamlined installment agreement | $50,000 or less; up to 72 months; set up online | The standard homebuyer path — payment counts in DTI; direct debit is the norm and helps keep a lien off the record |

| Non-streamlined agreement | Over $50,000; full financial disclosure required | Doable but slower to set up, and lien risk is higher — resolve before applying, not during underwriting |

| Offer in Compromise | Means-tested; $205 fee; roughly 1 in 5 accepted in FY2024 | Poor fit for a near-term purchase — review takes many months, and buying a house mid-review changes your asset picture |

| Currently Not Collectible | Documented financial hardship | If your finances qualify for CNC, they rarely qualify for a mortgage — and a lien is often filed in hardship status |

| Lien withdrawal / subordination / discharge | Lien already filed | The repair kit: withdrawal via Form 12277, subordination via Form 14134, or discharge/payoff at closing |

How much you owe changes the path

The size of your IRS balance largely determines which resolution is realistic — and how much friction the mortgage adds:

| You owe | Realistic IRS resolution | Mortgage outlook |

|---|---|---|

| Under $10,000 | Pay in full, or a guaranteed installment agreement (an official IRS program name) with returns current | Minimal friction — small DTI hit, lien unlikely if you act promptly |

| $10,000–$25,000 | Streamlined installment agreement, set up online | Approvable with the agreement in place and payments current |

| $25,000–$50,000 | Streamlined agreement, up to 72 months, direct debit strongly preferred | Approvable — expect roughly a $350–$700/month DTI hit depending on the balance; direct debit helps keep a lien off record |

| $50,000–$100,000 | Non-streamlined agreement with Form 433 financial disclosure | Workable but slow — set it up well before applying; lien risk is materially higher |

| Over $100,000 | Often assigned to a revenue officer; negotiated resolution | A lien is likely already filed or imminent — resolve, withdraw, or subordinate before house-hunting |

A worked example: $36,900 in IRS debt and a mortgage application

Say you're a sole proprietor who owes $36,900 across two years of underpaid self-employment tax. That's under the $50,000 line, so you can set up a streamlined installment agreement online — no financial disclosure, up to 72 months. The floor payment is $36,900 ÷ 72 = $512.50, call it $515/month — and in practice a bit more, because interest and the 0.5% monthly failure-to-pay penalty keep accruing until the balance is gone.

Now the lender's side of the math. Suppose your qualifying income — the two-year average of your net Schedule C profit — is $7,400/month, and your lender caps total monthly debts at 43% of income: $3,182. You carry a $450 truck payment and $180 in card minimums. Without the IRS, $2,552/month is left for housing. With the $515 IRS payment in your DTI, that drops to $2,037/month. You still qualify — just for a smaller payment, which means a smaller loan.

The alternative — writing the IRS a $36,900 check from your down-payment fund — buys back that $515/month of capacity but may leave you short on the down payment and the cash reserves lenders also require. There's no universal right answer; there's a right answer for your income, your savings, and your target price, and it's worth running both versions before you commit either way.

One more lever: if penalties make up a meaningful slice of that $36,900, first-time abatement — or, starting summer 2026, the new Automatic Exemption from Penalty (AEP), which applies without a request — can shrink the balance before you divide it by 72. (Interest itself is harder to remove; see can IRS interest be waived.)

How to buy a house when you owe the IRS, step by step

- Pull your IRS records — log into your IRS online account and confirm the exact balance, that every return is filed, and whether a lien shows on your account.

- File any missing returns — lenders verify income with transcripts; an unfiled year stops the loan cold, even if filing it creates a balance you can't pay yet.

- Set up a direct-debit installment agreement — do this before you apply, not during underwriting; at $50,000 or less you can usually do it online in one sitting (here's the IRS payment plan online setup, step by step).

- Document the agreement and every payment — keep the IRS acceptance letter and proof of each debit; FHA lenders typically want to see months of on-time history.

- Disclose the debt to your loan officer up front — tell them the balance, the plan, and the payment on day one so they can structure the file; surprises in underwriting kill deals.

- If a lien is already filed, resolve it before closing — pursue withdrawal (Form 12277), subordination (Form 14134), or a payoff through escrow at closing, with professional help if the numbers are large.

When you can handle this yourself — and when help changes the outcome

If your returns are all filed, your balance is under $50,000, and no lien has been filed, you genuinely don't need professional help for the IRS side: set up the streamlined direct-debit agreement online, keep the confirmation letter, and hand it to your loan officer. That's a 30-minute task, and paying someone to do it buys you nothing.

Experienced help changes outcomes in four specific situations. A lien is already on record — withdrawal, subordination, and discharge each have different rules, and picking the wrong one before a closing date costs you the house. You have unfiled years — the order you file and resolve them in changes both your tax bill and your qualifying income. You owe well over $50,000 — the negotiated agreement you get shapes your DTI for years. Your Schedule C is the problem — when the same return has to satisfy the IRS and impress an underwriter, an experienced tax professional who understands both audiences earns their fee. The lien's mortgage-priority mechanics — who gets paid first when a lien and a mortgage collide — are covered in tax lien vs. mortgage priority.

Terms your lender and the IRS will use, decoded

- Notice of Federal Tax Lien (NFTL): the public filing that attaches the government's claim to your property — the single biggest obstacle between IRS debt and a mortgage.

- Subordination: the IRS agreeing to let a new mortgage jump ahead of its lien in priority (requested on Form 14134) so a loan can close.

- Withdrawal: removing the lien notice from public record entirely (requested on Form 12277), typically after setting up a qualifying direct-debit agreement.

- DTI (debt-to-income ratio): your total monthly debt payments — including an IRS installment payment — divided by gross monthly income; the number that sets your maximum loan.

- Form 4506-C: the authorization your lender uses to pull your tax transcripts straight from the IRS to verify what you filed.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though certain events pause that clock.

Buying a house with IRS debt: your questions answered

Can I get an FHA loan if I owe the IRS?

Yes — FHA guidelines allow borrowers with delinquent federal tax debt if you have a valid repayment agreement with the IRS and have made the required timely payments under it (lenders typically look for at least three months of history, and you can't prepay three payments at once to shortcut it). A filed federal tax lien makes FHA approval much harder, so set up the agreement before the lien stage.

Does an IRS payment plan stop you from getting a mortgage?

No. An installment agreement is generally acceptable to conventional and government lenders as long as you're current on it and, for conventional loans, no Notice of Federal Tax Lien has been filed. The monthly payment counts in your debt-to-income ratio just like a car loan, so it reduces how much house you qualify for rather than whether you qualify at all.

Can I get a mortgage with a federal tax lien?

It's difficult but not always impossible. Conventional guidelines generally won't approve a loan with an open federal tax lien; FHA may still work if the lien holder (the IRS) subordinates or you're in a documented repayment plan, depending on the lender. The cleaner paths are lien withdrawal after setting up a direct-debit agreement, subordination via Form 14134, or paying the lien off at closing.

Do mortgage lenders know if you owe the IRS?

Usually yes. Tax liens dropped off credit reports in 2018, so the debt itself isn't on your credit — but lenders pull your tax return transcripts with Form 4506-C, ask about federal debt on the application, and search public records for liens. An undisclosed balance that surfaces in underwriting looks far worse than one you disclosed with a payment plan already in place.

Should I pay off the IRS before buying a house?

Not automatically. If paying the IRS in full would drain your down payment and reserves, many lenders would rather see a modest installment-agreement payment in your debt-to-income ratio than an empty savings account. Paying in full makes sense when the balance is small relative to your cash, or when it's the only way to get a filed lien released before closing.

Can I buy a house with cash if I owe the IRS?

Yes — a cash purchase involves no lender, so no one checks your IRS balance at closing. But if the IRS later files a Notice of Federal Tax Lien, it attaches to every property you own, including the new house, which complicates any future sale or refinance. Resolving the debt before or right after a cash purchase protects the asset you just bought.

Can I get a mortgage if I haven't filed my tax returns?

No — this is the hardest stop in the process, especially for self-employed borrowers. Lenders verify income with IRS transcripts, and a missing year means there's nothing to verify. File the missing returns first (even if you can't pay the balance they create), then set up a payment arrangement; a filed-but-owed year is workable, an unfiled year is not.

Your next 24 hours

- Log into your IRS online account and write down three things: your exact balance by year, whether every return shows as filed, and whether any lien activity appears on the account.

- Gather your lender package: your last two years of tax returns, your monthly income and debt figures, and any IRS notices you've received — the same stack answers both the underwriter's and the IRS's questions.

- Get a free case review — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779. We'll map the exact sequence — file, agree, document, apply — for your balance and your closing timeline, while interest and penalties are still the only thing accruing against you.

For the IRS's own rules, see the official IRS payment plans and installment agreements page, the primer on understanding a federal tax lien, and payment options at IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Mortgage lending guidelines vary by lender and change over time; confirm current requirements with your loan officer.