Liens & Property

IRS Tax Lien on My House: What It Means and How to Remove It (2026)

The short answer: an IRS tax lien on your house is a public legal claim that secures your unpaid tax debt against your property — it is not a seizure, and the IRS almost never takes a primary home. The lien can be released, withdrawn, discharged, or subordinated once you resolve or restructure the debt behind it.

You probably found out the hard way — a certified letter from the IRS, a title officer's call in the middle of a refinance, or a county-records search that made your stomach drop as you typed "IRS tax lien on my house" into a search bar. Here's the reorientation you need: a lien is the IRS staking a claim on your equity, not taking your keys, and there is a defined set of tools for getting it off your title. The document driving all of this is a short recorded filing called Form 668(Y) — the image below shows you exactly what it looks like and where to find the tax years, amounts, and refile deadline that shape every decision that follows.

⏱ Your appeal window: you typically have 30 days from the deadline date printed on Letter 3172 — the letter telling you a Notice of Federal Tax Lien was filed — to request a Collection Due Process hearing on Form 12153. The exact date printed on your letter controls. Miss it, and challenging the lien gets dramatically harder.

Why is there an IRS tax lien on my house?

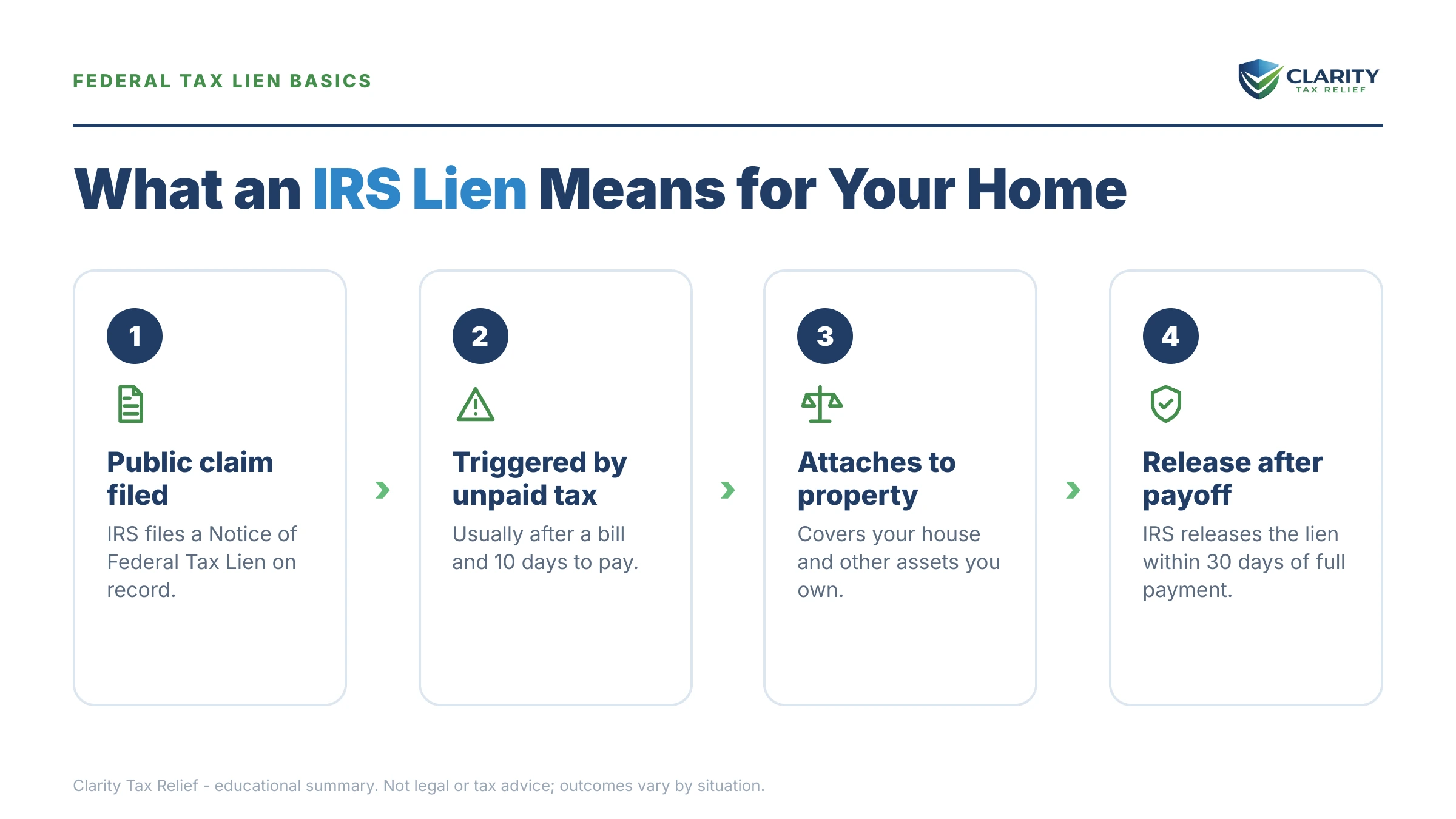

A federal tax lien attaches to your house automatically once the IRS assesses a tax, sends you a bill, and the balance goes unpaid — the county filing you just discovered only makes that claim public. The "silent" lien has likely existed for months. What changed is that the IRS recorded a Notice of Federal Tax Lien (NFTL, Form 668(Y)) with your county recorder, and mailed you Letter 3172 announcing it.

The IRS generally waits until a balance tops $10,000 before filing, though it has the authority to file at any amount. If you owe for multiple years, each assessment is listed as its own line on the 668(Y), with its own amount and its own collection deadline.

One thing worth absorbing early: the lien was never aimed at your house specifically. It attaches to everything you own — vehicles, bank accounts, business assets, even property you acquire later. Real estate is simply where liens bite hardest, because every sale and refinance triggers a title search that surfaces the filing. And a lien is still only a claim; the seizure tool is a levy, which is a separate action with its own separate warning letters. The distinction matters enough that we cover it fully in lien vs. levy: the difference.

What a federal tax lien does to your home — and what it doesn't

An IRS tax lien encumbers your home's equity and clouds its title, but it does not transfer ownership, force a sale, or lower your credit score. Most of the fear around liens comes from confusing them with foreclosure. Here is the honest map:

| The fear | The reality |

|---|---|

| "The IRS will take my home" | A lien is a claim, not a seizure. Taking a primary residence requires a federal court order — a step the IRS takes rarely, and only after other collection fails. See can the IRS take my house. |

| "I can't sell now" | You can sell. The lien is paid from your proceeds at closing — or discharged from the property (Form 14135) when the equity won't cover it. |

| "I can't refinance" | Lenders won't close over an unresolved lien, but subordination (Form 14134) lets the new mortgage take priority so the loan can fund. |

| "My credit score is wrecked" | Tax liens came off all three credit bureaus in 2018. The filing is still a public county record — which is exactly how title companies and underwriters find it. |

| "At least it's only on the house" | The lien attaches to everything you own, including equity you build in the future. The house is just where it surfaces first. |

If only one spouse owes the tax

Whose name is on the debt matters as much as whose name is on the deed. Debt from a joint return attaches to both spouses and the entire property. Debt belonging to one spouse alone — separate filings, or a balance from before the marriage — generally attaches only to that spouse's interest in the home, though community-property states blur that line. If you co-own with a spouse, parent, or ex, the mechanics are covered in our guide to an IRS lien on jointly owned property.

Two related edge cases: bankruptcy can wipe out your personal liability for the tax, but a properly filed lien survives against property you owned when you filed. And if you also owe your state, the state records its own lien under its own rules — California's FTB, for example, can collect for 20 years, twice the federal window.

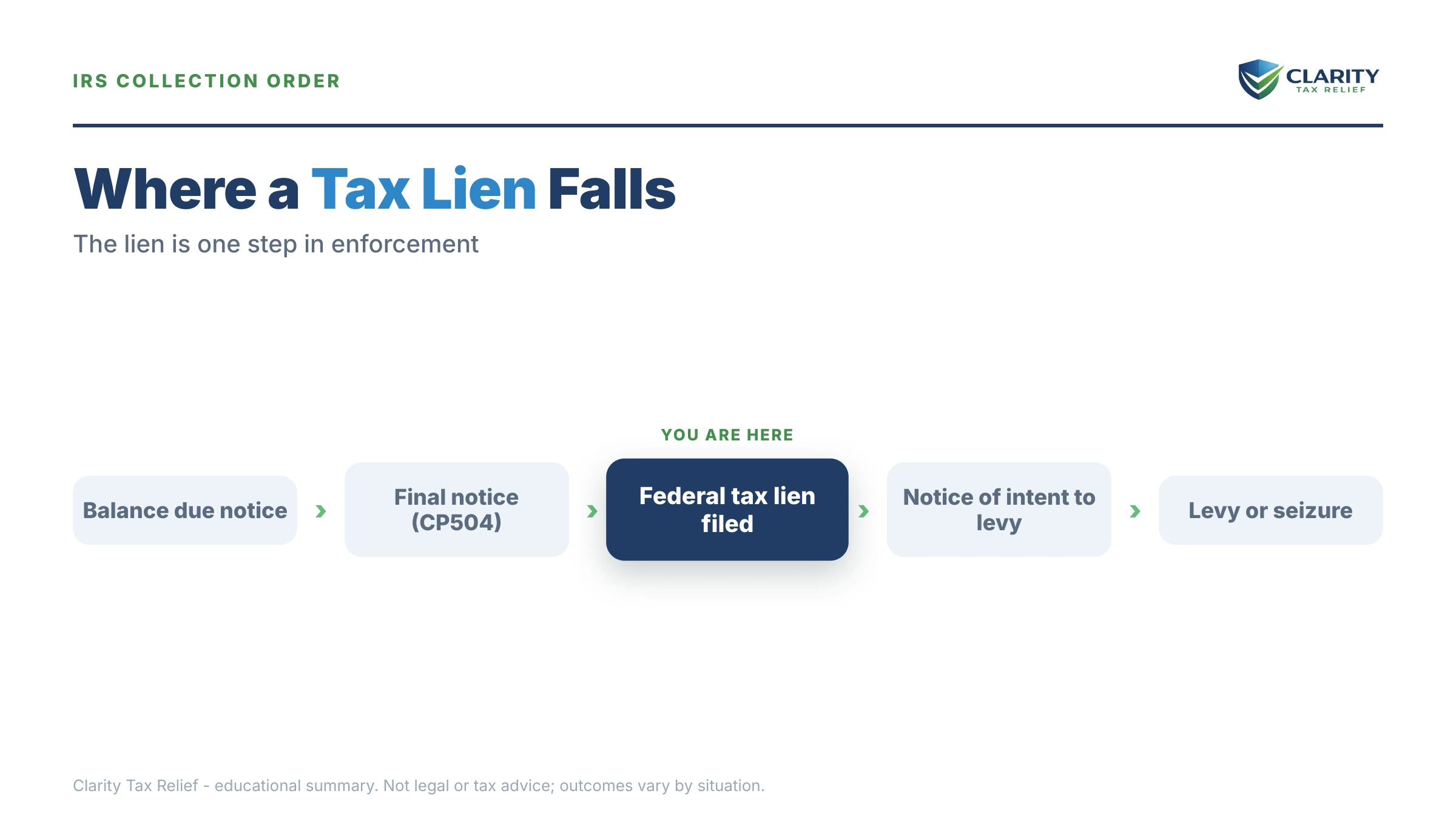

What happens if you ignore an IRS tax lien

An unaddressed tax lien grows with the debt it secures — every month of penalties and interest converts more of your home's equity into the IRS's claim. The lien itself doesn't "escalate," but the collection machine behind it does, in a predictable sequence:

- The claim keeps swelling. Interest compounds daily and the failure-to-pay penalty adds 0.5% of the balance every month until it caps out. The lien automatically secures the growing total — you don't get a new notice each time it grows.

- The final levy notice arrives. An LT11 or Letter 1058 starts a 30-day clock, after which the IRS can levy bank accounts (funds hold for 21 days before leaving) and garnish wages continuously until released.

- Passport certification becomes possible. Once a seriously delinquent balance passes $66,000 (the 2026 threshold), the IRS can certify it to the State Department, which can deny or revoke your passport.

- The lien gets refiled. If anything paused your 10-year collection clock — an offer, an appeal, bankruptcy — the IRS can refile the notice before its refile deadline, keeping the public claim alive.

- The rare endgame. For large, long-ignored balances, the government can sue to foreclose the lien or seek court approval to seize the home. It is genuinely rare — but it is the ceiling of what "do nothing" allows.

If you're wondering how a mailed bill turned into a recorded claim on your title, here is the standard path — and the windows that still matter going forward:

| Stage | Notice | Your window |

|---|---|---|

| First bill | CP14 | Typically 21 days from the notice date before the next notice queues |

| Automated reminders | CP501 / CP503 | No enforcement yet — but the balance compounds monthly |

| Intent to levy state refund | CP504 | 30 days before the IRS can take your state tax refund |

| Lien filed | Letter 3172 + recorded Form 668(Y) | Typically 30 days to request a CDP hearing — the date on the letter controls |

| Final levy notice | LT11 / Letter 1058 | 30 days before wages and bank accounts can be levied |

One 2026-specific note: the IRS workforce shrank roughly 27% in 2025, which makes reaching a human harder than ever — but lien filings, refilings, and levy notices are generated by automated systems that never stopped. Waiting for the IRS to slow down is not a strategy.

The lien is already on your title — the next notices bring levies

Send us your Letter 3172 and the county filing. An experienced tax professional will map which removal tool fits your house and your balance — free, confidential, before the appeal window printed on your letter closes.

How to remove an IRS tax lien from your house: the four tools

Every IRS tax lien on a house comes off through one of four tools — release, withdrawal, discharge, or subordination — and each has its own form, its own eligibility test, and its own use case:

| Tool | Form | Who typically qualifies | What it does for your house |

|---|---|---|---|

| Release | IRS issues Form 668(Z) | Debt paid in full, satisfied through an accepted Offer in Compromise, or expired at the CSED | Ends the lien — the IRS must release within 30 days of full payment |

| Withdrawal | Form 12277 | Generally a balance of $25,000 or less on a direct-debit installment agreement after three consecutive payments — or a notice filed in error | Erases the public filing as if it had never been recorded |

| Discharge | Form 14135 | Homeowners selling a specific property, where the IRS gets its interest from the proceeds or the property carries no lien equity | Removes the lien from that one property so the sale can close |

| Subordination | Form 14134 | Refinances that help collection — cash-out going to the IRS, or a lower payment that funds a plan | Moves the IRS behind the new lender so the loan can fund |

The vocabulary trips people up, so hold onto this: a release says the debt is satisfied; a withdrawal pulls the filing off the record entirely, which matters when a lender or licensing board asks whether a lien was ever filed. The mechanics of getting the release recorded — and chasing it when the IRS is slow — live in our hub guide to getting a lien released after payment, with the paperwork side covered in the certificate of release of tax lien guide. If your goal is a full withdrawal, the application walkthrough is at lien withdrawal (Form 12277).

Resolving the debt behind the lien

Every lien tool runs through the tax debt that created it, so your payment resolution and your lien strategy have to be chosen together:

- Full payment — the only path that forces a release on a fixed clock: 30 days from payoff.

- Short-term plan — up to 180 days to pay in full, no setup fee. The lien stays until the balance hits zero, but enforcement stops.

- Installment agreement — up to 72 months online for balances of $50,000 or less. Above $50,000, expect to document your finances on Form 433-F; the terrain changes enough that we cover it separately in IRS payment plan over $50,000. A plan alone doesn't remove a filed lien — but it opens the withdrawal path once the balance is at $25,000 or below on direct debit.

- Offer in Compromise — real, but honest math matters here: your home equity counts toward what the IRS believes it can collect, and meaningful equity usually pushes that number above your balance. The IRS accepted roughly 1 in 5 offers in FY2024. An accepted, completed offer does end in a lien release.

- Currently Not Collectible — pauses collection during genuine hardship, but the lien typically stays in place, and the IRS often files one when granting hardship status. Details in does CNC stop a tax lien.

- Penalty relief — first-time abatement (and, starting summer 2026, the new Automatic Exemption from Penalty, which applies without a request) shrinks the balance the lien secures, which can be the difference between qualifying for a threshold and missing it.

Worked example: married, filing jointly, $54,600 — and a lien on the house

Say you and your spouse filed jointly, owe $54,600 across two tax years, and just found the 668(Y) recorded against your home. This is hypothetical, but the arithmetic is real:

- The cost of waiting: the failure-to-pay penalty alone runs 0.5% a month — about $273 a month on $54,600 — before daily-compounding interest. Every month of delay is equity quietly reassigned to the lien.

- The streamlined pay-down: at $54,600 you're above the $50,000 online-plan ceiling, which means financial disclosure. Pay $4,601 toward the balance and you're at $49,999 — eligible for a streamlined agreement of up to 72 months. $49,999 ÷ 72 ≈ $695 a month, plus the interest and reduced penalties that keep accruing until payoff.

- The withdrawal play: to pull the filing off your title before a planned refinance, the target is $25,000 or less on direct debit. That means paying the balance down by $29,600, making three consecutive direct-debit payments, then applying on Form 12277. The IRS can withdraw at that point — it isn't required to — but this is the path homeowners use when a clean title search matters more than cash in hand.

- The OIC reality check: if your home holds, say, $150,000 in equity, the IRS counts a discounted share of that equity toward what it could collect — and that figure alone likely exceeds $54,600. A couple in this position may qualify for an offer only if their equity and income picture is genuinely far weaker than it looks on paper.

One more number worth watching: $54,600 sits under the $66,000 passport-certification threshold today. Left alone for a couple of years of penalties and interest, it won't stay under.

Selling or refinancing while the lien is recorded

A recorded tax lien does not legally prevent you from selling your house — it guarantees the IRS gets paid out of your equity when you do. In a straightforward sale, the title company treats the lien like a second mortgage: it's paid from proceeds at closing and the release follows. When the numbers don't cover both your mortgage and the lien, a discharge application keeps the deal alive; the full playbook, including timing traps that kill closings, is in selling a house with an IRS lien and the companion guide to a tax lien discharge.

Refinancing works differently: no proceeds change hands to pay the IRS unless you take cash out, so the lender needs the IRS to voluntarily step behind the new loan. That's subordination, and the IRS generally agrees when the refinance improves collection. Start with refinancing with a tax lien for the lender-side view, and tax lien subordination for the application itself. Either application should be filed at least 45 days before your closing date — these packages move at IRS speed, not escrow speed.

Will the lien just expire? The 10-year rule

A federal tax lien generally dies with the 10-year collection statute, releasing itself by its own terms unless the IRS refiles. Look at your recorded Form 668(Y): each tax year listed has a "Last Day for Refiling" column, and if that date passes with no refiling, the notice operates as its own release. The catch is tolling — a pending Offer in Compromise, bankruptcy, or a CDP appeal pauses the clock, so the real deadline is often later than assessment-plus-ten-years. You can estimate your own collection deadline with our CSED Calculator, and the refiling mechanics are covered in does an IRS tax lien expire.

Honest framing: for a homeowner, "wait out the clock" is usually the worst plan on the menu. The lien sits on your title the entire time, the balance compounds, and any sale or refinance during the wait forces the issue anyway.

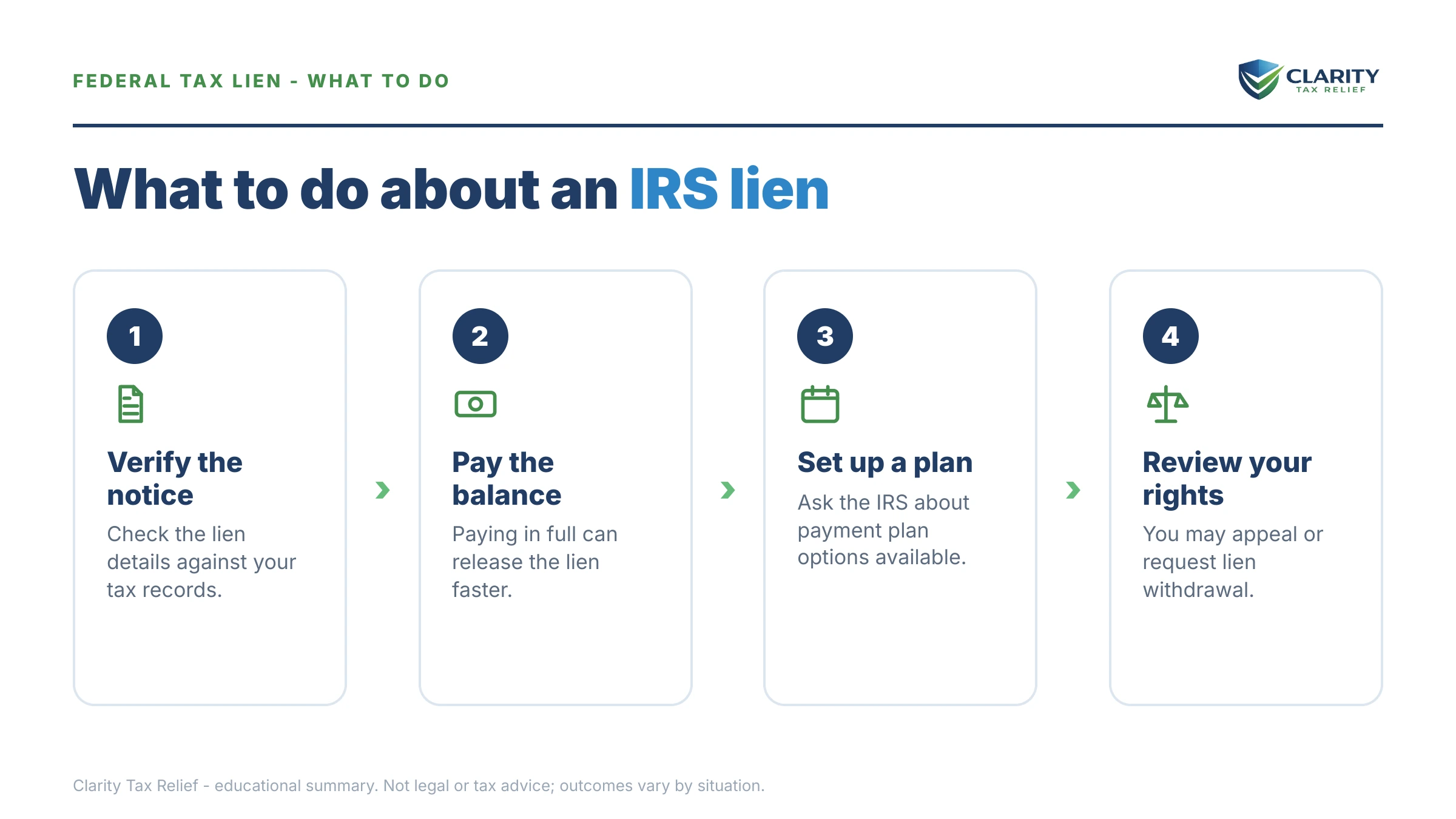

How to respond to an IRS tax lien on your house, step by step

- Pull the actual filing. Get your Letter 3172 and the recorded Form 668(Y) from your county recorder, then match the tax years and amounts against your IRS online account.

- Protect your appeal rights. If you are inside the window printed on Letter 3172, file Form 12153 to request a Collection Due Process hearing — it preserves your right to propose alternatives before enforcement escalates.

- Resolve the debt behind the lien. Choose the payment path that fits your balance — full payment, an installment agreement, an Offer in Compromise, or hardship status — because every lien remedy runs through the debt that created it.

- File the matching lien tool. Request withdrawal (Form 12277), discharge (Form 14135), or subordination (Form 14134) based on what you need the house to do — stay, sell, or refinance.

- Verify the public record. Confirm the IRS issued the release or withdrawal certificate, then check that your county records actually show it — recording errors linger for years when nobody checks.

When you can handle this yourself

Plenty of lien situations don't need professional help, and it would be dishonest to pretend otherwise. You can likely handle this on your own if: your balance is $25,000 or less and you can set up a direct-debit plan online, then file Form 12277 yourself; you've already paid in full and just need to chase the release through the IRS Centralized Lien Operation; or you can pay the whole balance within 180 days and simply want the lien gone on the standard 30-day release clock. The IRS's own overview at Understanding a federal tax lien and its payment portal at IRS.gov/payments are all you need for those paths.

Experienced help tends to change outcomes in four situations: a sale or refinance closing on a deadline, where a discharge or subordination package has to be underwriting-grade and right the first time; a balance over $50,000, where the financial statement you submit shapes both your monthly payment and your lien options; multiple years with unfiled returns, where filing order affects the assessments the lien secures; and any Offer in Compromise involving home equity, where the valuation math decides everything. If a levy notice has already followed the lien, timing matters more than anything else on this page.

Terms on your notice, decoded

- Notice of Federal Tax Lien (NFTL): the public version of the lien — Form 668(Y), recorded with your county so the world (and every lender) can see the IRS's claim.

- Self-releasing lien: the 668(Y) contains built-in release language tied to its "Last Day for Refiling" date — if the IRS doesn't refile by then, the notice releases itself.

- CSED: the Collection Statute Expiration Date — the IRS's 10-year deadline to collect each assessed year, pausable by offers, bankruptcy, and appeals.

- CDP hearing: a Collection Due Process hearing — your formal chance to challenge the lien filing or propose an alternative, requested on Form 12153 within the window on Letter 3172.

- Discharge: removal of the lien from one specific property (usually so a sale can close) while the lien survives against everything else.

- Subordination: the IRS agreeing to stand in line behind another lender — the lien stays, but a refinance can fund.

If your balance, the lien, and a pending closing are tangled together, a free case review can map which form — 12277, 14134, or 14135 — actually gets your deal done: call (888) 825-7779 or use the 2-minute form.

IRS tax lien on your house: questions answered

Can the IRS take my house because of a tax lien?

Almost never. A lien is a claim, not a seizure - and seizing a primary residence requires the IRS to get a federal court order, a step it takes rarely and only after other collection fails. The realistic risks are different: the lien absorbs your equity as the balance grows, and it complicates any sale or refinance until you deal with it.

How do I remove an IRS tax lien from my house?

There are four main paths: release (pay or resolve the debt in full), withdrawal (Form 12277 - generally available once you owe $25,000 or less on a direct-debit payment plan), discharge (Form 14135 - removes the lien from one property so a sale can close), and subordination (Form 14134 - lets a refinance lender take priority). Which one fits depends on your balance and what you need the house to do.

Does an IRS tax lien show up on my credit report?

Not anymore - the three major credit bureaus stopped reporting tax liens in 2018, so the lien will not lower your credit score directly. But it remains a public record at your county recorder, which means title companies and mortgage underwriters find it every time they search. That is why liens surface during home sales and refinances even when your credit looks clean.

Can I sell my house with an IRS tax lien on it?

Yes. The most common route is paying the lien out of your sale proceeds at closing - the title company sends the IRS its share and you keep the rest. If the sale price will not cover both your mortgage and the lien, you can apply for a discharge on Form 14135, which removes the lien from that property so the deal can close. Start the paperwork early; discharge applications take time to process.

Can I refinance my house with an IRS lien?

Often, yes - through subordination. Form 14134 asks the IRS to let your new lender take priority over the lien, which the IRS generally agrees to when the refinance helps collection - for example, a cash-out where the proceeds go to the IRS, or a lower payment that frees up money for an installment agreement. Without subordination, most lenders will not close.

Does an IRS tax lien on my house expire?

Yes - the lien is tied to the 10-year collection statute (the CSED). When the CSED expires, the recorded notice releases itself by its own terms unless the IRS refiles it. But the clock pauses for things like a pending Offer in Compromise, bankruptcy, and appeals, so your real expiration date can land later than assessment plus ten years.

My spouse owes the taxes, not me - is our house still covered?

If the debt comes from a joint return, yes - both of you are liable and the lien reaches the whole property. If only one spouse owes (separate returns, or debt from before the marriage), the lien generally attaches only to that spouse's interest in the home. Community-property states can complicate that split, and title companies often demand a resolution either way before closing anything.

How long does the IRS take to release the lien after I pay?

The IRS is required to issue a Certificate of Release (Form 668(Z)) within 30 days of full payment or of the debt becoming legally unenforceable. In practice, follow up: confirm the certificate was issued and check that your county records actually show the release. If 30 days pass with nothing recorded, contact the IRS Centralized Lien Operation to push it through.

Will the IRS file a lien if I set up a payment plan?

It depends on your balance and plan type. The IRS generally does not file a lien on balances under $10,000, and setting up a direct-debit streamlined agreement before a lien is filed often keeps one off the record entirely. Above $50,000 - or after a defaulted plan - a filing becomes much more likely. If the lien already exists, a payment plan alone does not remove it; the withdrawal path opens once your balance is $25,000 or less on direct debit.

Your next 24 hours

- Find three things on your paperwork: the request-a-hearing deadline printed on Letter 3172, and the tax years and "Last Day for Refiling" dates on the recorded Form 668(Y). Those three items determine every option you have.

- Gather your file: the letter, your last filed returns for the listed years, a current mortgage statement (so you know your real equity), and a rough picture of monthly income — everything a resolution decision depends on. If a levy has already started and it's creating hardship, the Taxpayer Advocate Service is a free escalation path.

- Get the lien reviewed free before the hearing window on your letter closes: use the 2-minute form or call (888) 825-7779, and an experienced tax professional will match your balance and your house plans to the right removal tool.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.