IRS Collections

Can the IRS Freeze My Bank Account Without Notice? (2026)

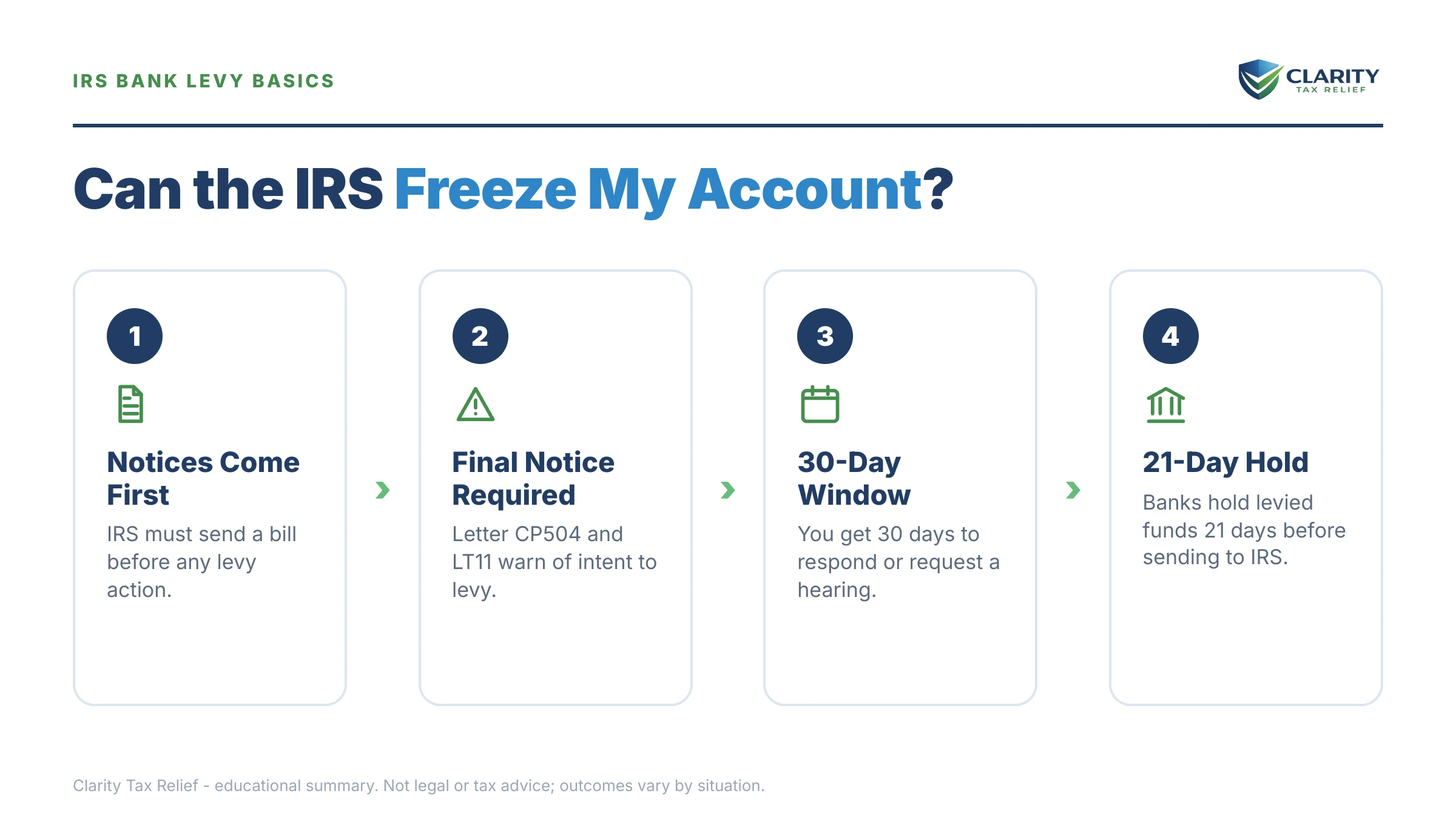

The short answer: no — the IRS generally cannot freeze your bank account without notice. It must mail a Final Notice of Intent to Levy (LT11 or Letter 1058) and wait 30 days first. But that notice only needs to reach your last known address, so a legal levy can still feel like zero warning.

Maybe you're asking "can the IRS freeze my bank account without notice" because payroll runs Friday and you can't afford a surprise. Or maybe the surprise already happened — you logged into your business checking account this morning and part of the balance is on hold. Either way, the answer has a legal side and a practical side, and the gap between them is exactly where people get hurt.

Legally, a bank levy is one of the most heavily fenced-in things the IRS does. Practically, the fences only protect people who see the warnings. The image below shows exactly what the final levy notice looks like and where to find the date that starts your 30-day clock — because that one letter is the difference between a levy you can block and a levy you're cleaning up after.

⏱ Two clocks matter here. If you're holding an LT11 or Letter 1058, you have 30 days from its date to request a hearing that blocks the levy. If your account is already frozen, your bank holds the funds for 21 days before sending them to the IRS — that window is your last realistic chance to get the money released.

Can the IRS freeze my bank account without notice? What the law requires first

Before it can levy your bank account, the IRS must send a Final Notice of Intent to Levy — the LT11 notice or Letter 1058 — and wait 30 days. That final notice also grants you Collection Due Process (CDP) rights: file Form 12153 for a CDP hearing within the 30 days and the bank levy is blocked while an appeals officer reviews your case.

That final notice is never the first letter, either. It sits at the end of a months-long automated sequence of bills and reminders — if you're trying to figure out which letter you're holding, our guide to why you got a letter from the IRS decodes the whole system. Here's the ladder as it applies to your bank account specifically:

| Notice | What it is | Can the IRS touch your bank account yet? |

|---|---|---|

| CP14 | First bill after a balance posts — typically about 21 days to pay (10 business days if the balance is $100,000 or more) | No |

| CP501 / CP503 | Automated reminder bills, usually weeks apart | No |

| CP504 | "Notice of Intent to Levy" under IRC §6331(d) — scarier title than power | No — it authorizes seizing your state tax refund, not your bank account |

| LT11 / Letter 1058 | Final Notice of Intent to Levy, with CDP hearing rights | Yes — 30 days after this notice, if you don't respond |

| Bank levy | Levy order delivered directly to your bank | Funds frozen that day; 21-day hold before the transfer |

Notice the CP504 row — it's the most misunderstood letter in the sequence. Millions of people panic-empty accounts over a CP504 that can't reach their bank, then ignore the LT11 that actually can. The final notice usually arrives by certified mail; if you signed a green card recently, our certified letter from the IRS decoder tells you which letters travel that way and why.

So why do so many people swear they got no notice? Because the IRS only has to mail the final notice to your "last known address" — the one on your most recent return or change-of-address filing. Moved and never told the IRS? Mail going to a closed business location? Someone else opening the mail? The notice is legally delivered even if you never read a word of it, and the resulting levy is valid.

The four real exceptions: when the IRS can levy first and notify you after

There are exactly four situations where the IRS can levy without giving you the 30-day warning first. For everyone else, the pre-levy notice is mandatory:

- Jeopardy levy. An emergency seizure used when the IRS believes collection is in immediate danger — assets moving offshore, a taxpayer preparing to disappear. It requires high-level approval and comes with expedited review rights. If your situation is "I owe money and haven't dealt with it yet," this is not you; see our guide to the jeopardy levy for how rare it truly is.

- State tax refund levy. The IRS can grab your state refund after a CP504 with no further warning — you get your hearing rights after that levy instead of before.

- Federal contractor levy. If you're paid by the federal government as a contractor, those payments can be levied with post-levy hearing rights.

- Disqualified employment tax levy. The one that matters most if you run payroll. If your business already requested a CDP hearing on employment taxes within the prior two years and then racked up new payroll debt, the IRS can levy for the new periods without a fresh pre-levy hearing. Repeat 941 back taxes are the one scenario where a business account genuinely gets frozen with no new warning.

The pattern is worth naming: three of the four exceptions still give you a hearing — just after the levy instead of before. Only the timing of your rights changes, never their existence.

What happens if you ignore the warnings — the freeze sequence, hour by hour

An IRS bank levy is a snapshot, not a permanent lock: it captures the money in your account on the day the bank receives it, up to what you owe. Here is the sequence once the final notice's 30 days run out and no arrangement is in place:

- Day 0 — the levy lands at your bank. The bank freezes the funds in the account at that moment, up to your balance due. You often find out from a declined payment or a balance alert, not from the IRS.

- Days 1–21 — the hold. The frozen money sits at your bank. The account stays open, new deposits are yours, but the held funds are untouchable. This is your release window — details in our guide to the IRS bank levy 21-day rule.

- Day 21 — the transfer. The bank sends the held funds to the IRS. Getting money back after this point is dramatically harder — see the IRS took money out of my bank account for what's still possible.

- After the transfer — the levy repeats and spreads. If a balance remains, the IRS can re-levy the account to capture new deposits, issue a continuous wage levy against your paycheck, and — for a business — levy your accounts receivable so customer payments go to the IRS instead of you. A wage levy doesn't stop until released; you can estimate how much of a paycheck it could reach with our IRS Wage Garnishment Calculator.

For a business owner the second freeze is usually worse than the first, because by then the IRS knows the account is active. If your operating account is exposed, our guide to an IRS levy on a business bank account covers the going-concern rules. And note what 2026 changes about this: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but these levies are issued by automated systems that never got cut. Fewer people answer the phone; the machine still freezes accounts on schedule.

Holding a final notice — or staring at frozen funds?

Both clocks are short: 30 days from the LT11 date to block the levy, 21 days from the freeze to get funds released before they leave your bank. Get your notice reviewed free by an experienced tax professional before either window closes — tell us the date printed on your letter and we'll tell you exactly where you stand.

Your options to stop a bank freeze before it starts

The IRS levies bank accounts to force a conversation — any legitimate resolution takes you out of the levy queue. Which one fits depends mostly on how much you owe and what your finances honestly look like:

| Your balance | Realistic options | Key requirement |

|---|---|---|

| Under $10,000 | Short-term plan (up to 180 days, $0 setup) or a guaranteed installment agreement | Returns filed; full payment within 3 years on the guaranteed plan |

| $10,000–$25,000 | Streamlined installment agreement, set up online | Up to 72 months; no detailed financial disclosure |

| $25,000–$50,000 | Streamlined agreement with direct debit | Direct-debit enrollment; still up to 72 months online |

| Over $50,000 | Non-streamlined agreement with financial disclosure (Form 433 series) | Full income, expense, and asset review |

| Any balance — genuine hardship | Currently Not Collectible status, or an hardship levy release if a levy already hit | Show that allowable living or operating expenses consume your income |

| Any balance — limited assets and income | Offer in Compromise ($205 application fee; waived with low-income certification) | Strict means test — the IRS accepted roughly 1 in 5 offers in FY2024 |

One critical point for every option: an active payment plan takes bank levies off the table while you keep the payments current, even though interest and penalties continue to accrue on the shrinking balance. The levy threat isn't about the size of the debt — it's about whether the account is in an arrangement or in the collection queue.

A worked example: $4,800 owed and a payroll to make

Say you own a small shop with four employees and owe the IRS $4,800 in personal income tax from last year — profit you'd already spent on inventory by the time the return was done. This is a hypothetical, but the math is real. Two paths:

Path one — set up a plan while it's still a CP-series bill. At $4,800 you're under the $10,000 guaranteed-agreement line: full payment within 3 years means $4,800 ÷ 36 = roughly $134 a month, plus the interest and late-payment penalty that keep accruing on the declining balance (so the true payoff runs somewhat higher, or you finish early). No financial disclosure, no levy exposure, ten minutes online.

Path two — ignore the mail for eight months. Penalties and interest push the balance to about $5,150. The LT11 arrives at your old shop address; 30 days pass unanswered. On a Wednesday, the levy hits your business checking account holding $6,100 — the bank freezes $5,150 and leaves you $950. Friday's payroll is $5,200. Now you're choosing between bouncing paychecks and borrowing at card rates — and if missed payroll leads to missed 941 deposits, you've traded a $4,800 problem for trust-fund exposure that follows you personally. The monthly plan costs $134; the levy costs your float, your payroll, and possibly a second, worse tax debt.

How to respond, step by step

- Find the last IRS notice you received. Dig out every IRS envelope from the past year and look for an LT11 or Letter 1058 — the date on that letter started your 30-day clock. No letter? Log into your IRS online account to check your balance and notice history.

- Confirm the IRS has your current address. File Form 8822 (or 8822-B for a business) if you've moved. Notices mailed to your last known address count legally even if you never saw them.

- Request a hearing if your 30-day window is still open. File Form 12153 within 30 days of the date on your LT11 or Letter 1058. A timely Collection Due Process request blocks a bank levy while your case is heard.

- Use the 21-day hold if your account is already frozen. Contact the IRS before the hold expires. A levy can be released for economic hardship, a processing error, or because you've set up a payment arrangement.

- Set up a resolution so the next levy never issues. A payment plan, hardship status, or offer — whichever your finances support — takes your account out of the levy queue. Under $10,000, a guaranteed installment agreement can usually be set up online in minutes.

When you can handle this yourself — and when help changes the outcome

If no levy has hit and no final notice has arrived, you can usually fix this alone. A balance you can clear within 180 days, or a personal debt under $50,000 you can put on a streamlined plan through the IRS payment plans page, needs no professional — set it up, keep the payments current, and the levy machinery never reaches your bank.

Experienced help earns its cost in four situations: a levy is already in motion and the 21-day hold is running; the frozen account funds payroll, because a bounced pay run creates trust-fund liability that attaches to you personally; you have unfiled years, since the IRS generally won't approve any arrangement until returns are in; or the debt is employment tax, where the disqualified-levy rule means the next freeze can come with no fresh warning at all. In those cases, an experienced tax professional isn't buying you comfort — they're buying you days, and days are the whole game inside a 21-day hold. If money was taken that wasn't yours to lose — a joint account, a third party's funds — a wrongful-levy claim may recover it, and the free Taxpayer Advocate Service can intervene when a levy creates immediate hardship the normal channels won't fix fast enough.

Terms on your notice, decoded

- Levy vs. lien: a levy takes property (like bank funds); a lien is a legal claim recorded against property you keep. The freeze is a levy.

- Last known address: the address from your most recent return or address-change filing — where notice is legally "given," whether or not you actually read it.

- Collection Due Process (CDP): your right, triggered by the final notice, to a hearing before the levy — requested on Form 12153 within 30 days.

- 21-day holding period: the time your bank must sit on levied funds before sending them to the IRS — your release window.

- Jeopardy levy: the rare emergency levy issued without the 30-day warning when the IRS believes collection is at immediate risk.

- Disqualified employment tax levy: a no-new-warning levy on repeat payroll-tax debt when a CDP hearing was already requested for employment taxes within the prior two years.

If your goal today is simply to stop the freeze from ever issuing, paying or arranging payment at IRS.gov/payments before the LT11's 30 days expire ends the threat immediately.

IRS bank freeze questions, answered

Can the IRS take money from my bank account without telling me?

Not in the ordinary case — the IRS must first send a Final Notice of Intent to Levy (LT11 or Letter 1058) and give you 30 days to respond before it can levy a bank account. The catch is that the notice only has to go to your last known address, so if you moved and never updated the IRS, a legally valid levy can still feel like it came out of nowhere.

How long does an IRS bank account freeze last?

The freeze itself lasts 21 days: your bank holds the levied funds for 21 days before sending them to the IRS. Your account is not closed, and deposits made after the levy date are not taken by that levy. The 21-day window exists so you can contact the IRS, prove an error or hardship, or set up a resolution and get the levy released before the money leaves.

Does the IRS freeze my whole bank account or just what I owe?

A bank levy attaches only to the funds in your account on the day the bank receives it, up to the balance you owe. Anything above your tax debt stays available, and money you deposit afterward is not covered by that levy. The IRS can, however, issue a new levy later to reach new deposits if the debt remains unresolved.

Can the IRS freeze a business bank account without notice?

Businesses get the same 30-day final-notice protection as individuals, with one major exception: the disqualified employment tax levy. If your business already requested a collection hearing on payroll taxes within the prior two years, the IRS can levy for new payroll debt first and offer the hearing afterward. Repeat 941 balances are the one situation where a genuinely unannounced freeze happens with any regularity.

What if the IRS sent the levy notices to my old address?

The levy is usually still legally valid — the IRS only has to mail the final notice to your last known address, which comes from your most recent tax return or a change-of-address filing. If you never saw the notice, you may still be able to request an equivalent hearing and negotiate a release. Update your address with Form 8822 (or 8822-B for a business) so it never happens again.

Can I get my money back after an IRS bank levy?

Your best chance is during the 21-day hold, before the bank sends the funds: a levy can be released if it causes economic hardship, if you set up a payment arrangement, or if the IRS made a procedural error. Once the money is transferred, recovery is much harder — generally limited to showing the levy was wrongful or that the IRS failed to follow required procedures.

What is a jeopardy levy?

A jeopardy levy is the rare emergency exception that lets the IRS seize assets without the usual 30-day warning — used when it believes collection is in immediate danger, such as a taxpayer moving money offshore or preparing to flee. It requires high-level approval and gives you expedited review rights afterward. For an ordinary unpaid balance, even an ignored one, jeopardy levies essentially never happen.

Your next 24 hours

- Find the controlling date. Pull your most recent IRS letter and locate the notice date in the top corner. LT11 or Letter 1058 date plus 30 days = the day a levy becomes legal. Account already frozen? The day your bank received the levy plus 21 days = the day the money leaves.

- Gather three things: your last filed return, every IRS notice you can find, and — if you run a business — your bank statements and upcoming payroll schedule, so whoever helps you can see exactly what a freeze would break.

- Get a free case review before your window closes. Whether you're inside the 30-day hearing window or the 21-day hold, call (888) 825-7779 or use the 2-minute form — an experienced tax professional will map the fastest route to a release or a plan that keeps your account off the levy list.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.