IRS Levies

Joint Account With a Parent and an IRS Levy: Whose Money Is at Risk (2026)

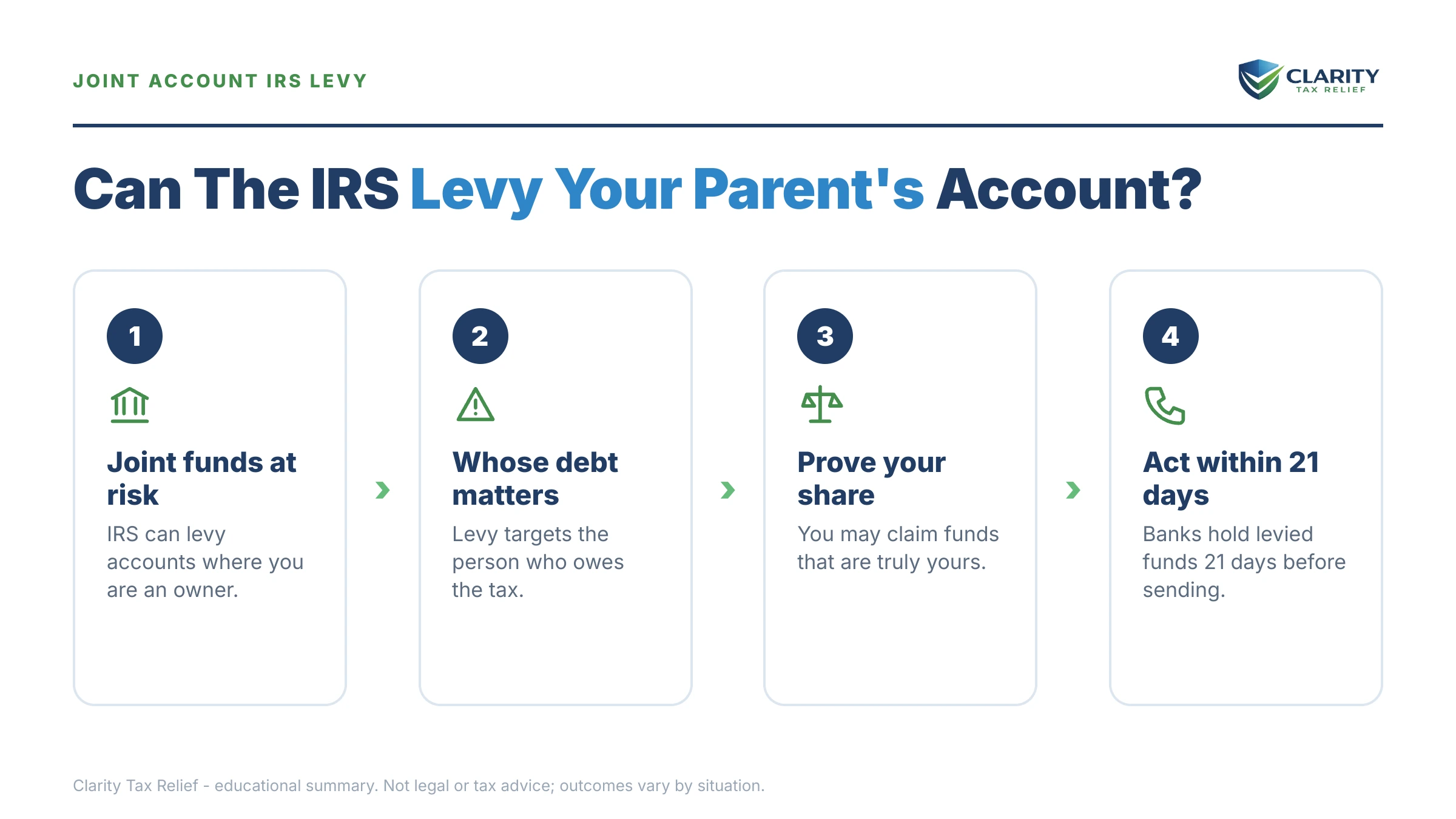

The short answer: if you hold a joint account with a parent, an IRS levy against either owner can freeze the entire balance — even money the tax debtor never contributed. The bank holds the funds for 21 days before sending them, and the non-liable owner can recover their share through a wrongful levy claim.

You added your name to Mom's checking account years ago so you could pay her utilities from your phone — and now, because your own gig-work tax debt caught up with you, her account is frozen with her Social Security savings inside. That sinking guilt is exactly why this page exists. The rules here are harsh but knowable, and there are three separate ways to get the money back — the fastest ones only work inside a 21-day window.

A joint account with a parent is the single most common way one person's IRS levy lands on another person's money. The image below shows you exactly what the levy paperwork looks like and where the amounts and dates that control your options appear.

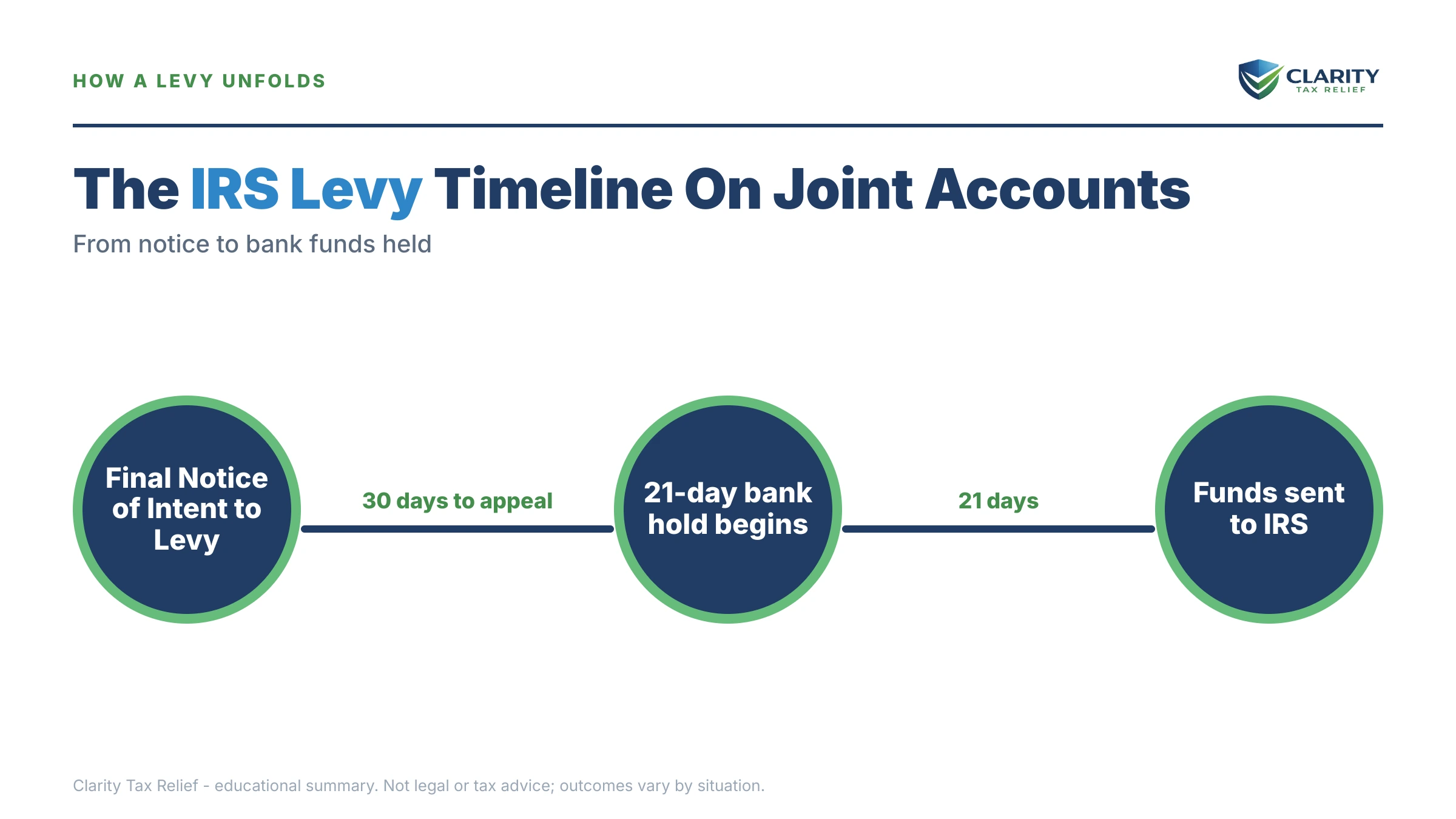

⏱ Your real clock: the bank holds levied funds for 21 days before sending them to the IRS. During those 21 days the money is frozen but still at your bank — a hardship release, a payment arrangement, or proof that the funds belong to the non-liable owner can stop it from ever leaving. After day 21, recovery is still possible but far slower.

Joint account with a parent: why an IRS levy reaches the whole balance

An IRS levy attaches to every dollar in any account the tax debtor has an unrestricted legal right to withdraw from — regardless of who actually deposited the money. That is the brutal mechanics of joint ownership. If your name is on the account and you owe, the levy reaches your parent's deposits. If your parent owes, it reaches yours.

This isn't an IRS overreach the bank can push back on. The Supreme Court settled it in 1985 in United States v. National Bank of Commerce: under the levy authority in IRC §6331, the bank must surrender whatever is in the account, up to the debt, and true ownership gets sorted out afterward. The bank has no discretion to protect the innocent co-owner's share — that protection comes later, through a wrongful levy claim, or earlier, through how you structure the account.

The paperwork that triggers all of this is Form 668-A, the Notice of Levy the IRS serves on the bank. Neither owner gets advance warning of the freeze itself; the warning came weeks earlier in the notice sequence covered below.

What the levy can reach depends heavily on your exact role on the account:

| Your role on the parent's account | What a levy for YOUR debt reaches | Best defense |

|---|---|---|

| Full joint owner (both names, either can withdraw) | The entire balance, up to the amount you owe — including your parent's deposits | Parent files a wrongful levy claim tracing their deposits; act inside the 21-day hold |

| Authorized signer only (you can sign checks but don't own the funds) | Generally nothing — the account isn't your property. Banks sometimes freeze anyway in confusion | Send the bank the signature-card/account agreement showing you are a signer, not an owner |

| Payable-on-death (POD) beneficiary only | Nothing while your parent is alive — you have no present ownership | None needed; this is the safest "inheritance" structure for a debtor child |

| Joint owner where the PARENT is the one who owes | Reversed exposure: the parent's levy reaches your gig deposits sitting in the account | You file the wrongful levy claim; keep your own income in a separate account going forward |

One nuance worth flagging: some states treat "convenience accounts" — a child added purely to help with bills — as belonging entirely to the parent under state law. That characterization can strengthen a wrongful levy claim, but it does not stop the bank from freezing the money first. The freeze always comes before the argument.

What happens if you ignore the notices behind the levy

A bank levy on a joint account is never the first step — it is the last step of an automated notice sequence that ran for months. If you're a gig worker with unfiled years, the sequence often started with the IRS filing a substitute return for you and assessing a balance you never agreed to. From assessment forward, the letters escalate in a fixed order:

- CP14 — the first bill after assessment. About three weeks to respond before reminders begin.

- CP501 / CP503 — reminder bills, arriving roughly five weeks apart while penalties and interest compound.

- CP504 — Notice of Intent to Levy under IRC §6331(d). The IRS can now take your state tax refund. Not yet the final notice.

- LT11 / Letter 1058 — the final notice. This starts a 30-day clock and your Collection Due Process rights. It is the last exit before the bank gets served.

- Form 668-A served on your bank — the joint account freezes that day, for the full balance up to the debt. The 21-day hold begins.

- Day 22 — the bank transmits the funds to the IRS. If the debt remains unresolved, a fresh levy can be issued against whatever lands in the account next.

Here is the part that makes joint accounts uniquely dangerous: the warning letters go to the debtor's last known address. If you owe and the notices went to an old apartment, your parent's first hint that anything was wrong is a frozen account. And in 2026, with IRS staffing down roughly 27%, no human reviews the file before the levy fires — the automated system escalates on schedule whether or not anyone ever answers the phone. Our guide to the IRS bank levy 21 days rule covers the mechanics of the hold itself in more depth.

| Stage | Typical timing | What it means for the joint account |

|---|---|---|

| CP14 first bill | ~21 days to respond | No enforcement yet — cheapest moment to fix everything |

| CP501 / CP503 reminders | Roughly 5 weeks apart | Balance growing; still no reach into the account |

| CP504 intent to levy | 30-day response window | State refund seizable; joint account not yet touchable |

| LT11 / Letter 1058 final notice | 30 days + CDP rights | Last stage before the bank can be served |

| Form 668-A hits the bank | Freeze is same-day | Entire joint balance frozen, up to the debt |

| 21-day hold expires | Day 22 | Funds go to the IRS; re-levy possible until resolved |

Account frozen with a parent's money inside?

The 21-day hold is the window where the right move gets every dollar released before it ever leaves the bank. Send us the levy notice — an experienced tax professional will map your fastest release path free, whether the debt is yours or your parent's.

Your options: releasing the levy and protecting the non-liable owner

There are three separate paths to getting money out of a frozen joint account, and they can run at the same time. Which one leads depends on whose debt it is and whose money is in the account.

If YOU owe and your parent's money is frozen: your parent — the non-liable owner — can pursue a wrongful levy claim by showing the IRS the funds trace to their deposits: Social Security, pension, their paychecks. Filed during the 21-day hold, the claim can get the parent's share released before it leaves the bank. Filed after, it generally must be made within two years of the levy date, and recovery takes months instead of days. Meanwhile, you resolve your side of the debt so the IRS has a reason to release the rest and no reason to levy again.

If your PARENT owes and your money is frozen: the roles flip. You file the wrongful levy claim with your own deposit records — gig platform payouts are easy to trace, which works in your favor. If your parent's income is mostly Social Security, note that the IRS can separately take up to 15% of the benefit itself through the Federal Payment Levy Program, so fixing the underlying debt matters even after the account is sorted. The same rules apply to spouses, covered in can the IRS take my spouse's bank account.

For the debtor's own share, the release paths are the standard ones:

- Economic hardship release — if the levy leaves the debtor unable to cover basic living expenses, the IRS must release it under §6343. See levy causing hardship for the proof the IRS looks for. This releases the levy, not the debt.

- Payment arrangement — setting up an installment agreement is the most common lever for a release. Balances under $50,000 generally qualify for a streamlined installment agreement of up to 72 months, but the IRS requires all past-due returns filed first. Interest and penalties continue accruing on a plan.

- CDP hearing — if you are still inside the LT11's 30-day window (or within one year for an "equivalent hearing"), a Form 12153 CDP hearing request puts a person, not a machine, between you and further levies.

- Bankruptcy's automatic stay — a filing stops active levies, though it is rarely the right tool for tax debt alone; see does bankruptcy stop IRS levy before considering it.

Every deadline in this fight is short, and each one protects a different right:

| Trigger | Window | Right it protects | If it passes |

|---|---|---|---|

| LT11 / Letter 1058 date | 30 days | CDP hearing (Form 12153) with Tax Court review — levy paused | Equivalent hearing still available for 1 year, but without the same court review or levy pause |

| Bank receives Form 668-A | 21 days | Release before funds ever leave the bank | Money goes to the IRS; recovery shifts to slower claim channels |

| Funds sent to the IRS | Generally 2 years | Non-liable owner's wrongful levy claim | The innocent co-owner's money is generally unrecoverable |

| Debt still unresolved | Ongoing until the CSED (10 years from assessment) | N/A — this is the IRS's clock, not yours | Re-levy of the account can happen at any time |

A worked example: $19,700 owed, a parent's account frozen

Say you're a gig worker who owes $19,700 across three unfiled years the IRS assessed for you, and you're a joint owner on your mother's checking account, which holds $6,200 — $4,900 of her Social Security savings and $1,300 of transfers you made to cover her bills. The levy freezes all $6,200, because $6,200 is less than $19,700.

Inside the 21 days: her bank statements show every Social Security deposit, so a wrongful levy claim with those statements targets the $4,900 for release. Your $1,300 is genuinely yours, so it stays levied — unless you move on the debt. Filing the three missing returns (which often lowers a substitute-return balance, since the IRS's version skipped your mileage and expense deductions — see haven't filed taxes in 3 years) makes you eligible for a streamlined plan: $19,700 over 72 months is roughly $274/month ($19,700 ÷ 72 ≈ $273.61), with interest and penalties continuing to accrue until paid. With a plan pending or in place, the IRS can release the levy and has no reason to serve a new one. This is a hypothetical illustration — real numbers depend on your assessments and finances.

How to respond, step by step

- Locate the final notice. Pull every IRS letter and find the LT11 or Letter 1058 date — if you are still inside its 30-day window, filing Form 12153 for a Collection Due Process hearing generally pauses levy action while your case is heard.

- Confirm the freeze date with the bank. Ask the bank the exact day it received the levy — the 21-day hold runs from that date, and every release option has to move inside it.

- Trace whose money is in the account. Pull 12 months of statements and match each deposit to its source — Social Security, gig deposits, transfers — because ownership proof drives both a wrongful levy claim and any partial release.

- Call the IRS at the number on the levy. Request a release based on economic hardship, a payment arrangement you set up now, or proof that the funds belong to the non-liable owner.

- Fix the root cause. File any unfiled returns and get a resolution in place — a released levy can be reissued at any time until the debt itself is resolved.

When you can handle this yourself — and when help changes the outcome

You can usually handle this alone when the picture is simple: the debt is clearly yours, all your returns are filed, the balance is under $25,000, and the account's ownership is easy to prove. In that case, calling the levy number, setting up a plan online, and faxing the bank statements is genuinely doable without paying anyone.

Experienced help tends to change the outcome in three situations. First, unfiled years plus a live levy — the returns must be prepared fast and correctly, because the plan that releases the levy can't start until they're in, and a rushed return can lock in an inflated substitute-return balance. Second, a wrongful levy claim on a parent's money, where the tracing evidence and the filing route determine whether the claim succeeds inside the 21 days or drags for months. Third, anything involving a IRS levy business bank account — mixed business and personal funds multiply both the exposure and the proof problems. Elderly parents helping from the other side of this can act through a power of attorney; see power of attorney for parent IRS. And if the underlying problem is the IRS reaching your pay rather than the account, start with our hub on how to stop IRS wage garnishment.

Terms on your levy paperwork, decoded

- Levy vs. lien: a levy takes property (like the account balance); a lien is a legal claim recorded against everything you own.

- Form 668-A: the Notice of Levy the IRS serves on your bank — it captures only what's in the account that day.

- 21-day hold: the period the bank must keep levied funds frozen before sending them to the IRS — your fastest release window.

- CDP rights: your right, after an LT11/Letter 1058, to a Collection Due Process hearing before levy action — requested on Form 12153 within 30 days.

- Wrongful levy claim: the process a non-liable person (like your parent) uses to recover their own money taken by a levy on someone else's debt.

- CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though certain actions pause that clock.

Joint account levy questions, answered

Can the IRS levy a joint bank account I share with my parent?

Yes. Under federal law, a levy reaches every dollar in any account the tax debtor can legally withdraw from — including a joint account where the other owner contributed most or all of the money. The bank must comply and freeze the full balance up to the amount owed. Ownership disputes get sorted out afterward, through a wrongful levy claim, not before the freeze.

Can the IRS take my parent's Social Security money out of our joint account?

Once Social Security is deposited into a joint account, it generally loses its protected character for IRS levy purposes, and the automatic bank protection that shields two months of federal benefits from most garnishments does not apply to IRS levies. Your parent can still recover the funds by proving to the IRS that the money was theirs, but prevention — a separate account — is far easier than recovery.

How does the non-liable owner get their money back after a joint account levy?

By filing a wrongful levy claim with the IRS showing the seized funds belonged to them — bank statements tracing each deposit to its source are the core evidence. The claim generally must be filed within two years of the levy. If the claim is made before the bank sends the money, during the 21-day hold, the IRS can release those funds without them ever leaving the bank.

Will the IRS levy the account again after releasing it?

It can. A bank levy is a one-time snapshot: it only captures funds in the account on the day it is served. If the underlying debt is still unresolved, the IRS can issue a new levy weeks or months later and capture whatever is in the account that day. The only durable fix is a resolution — a payment plan, hardship status, or an offer the IRS accepts.

Should I take my name off my parent's account to protect them?

If the money in the account is genuinely your parent's and you were added only for convenience, removing your name before a levy is served is a legitimate protective step — you cannot transfer away money that was never yours. Timing matters: once a levy hits the bank, it attaches to that day's balance and a name change won't undo it. If the funds are partly yours, moving them after IRS notices arrive can raise separate problems, so get advice first.

Does the bank warn you before an IRS levy freezes a joint account?

No. The bank freezes the balance the day it receives the levy and typically mails both account owners a notice afterward. Your advance warning came earlier, in the IRS notice sequence — especially the LT11 or Letter 1058 final notice, which by law must arrive at least 30 days before a levy. That is why unopened IRS mail is so dangerous with a joint account.

Is there a safer way to help a parent with their banking than a joint account?

Usually, yes. An authorized-signer arrangement or a financial power of attorney lets you pay a parent's bills without becoming a legal owner of the funds, and a payable-on-death designation handles inheritance without joint ownership. Those structures keep your tax problems off their money and their tax problems off yours. If either of you owes the IRS, restructuring before enforcement starts is the cleanest protection.

Your next 24 hours

- Find the levy date. Call or visit the bank and get the exact day it received Form 668-A — write it down and count 21 days forward. That is your release deadline.

- Gather the proof. Pull the levy notice, every IRS letter you can find (especially any LT11 or Letter 1058), 12 months of account statements, and — if you have unfiled years — whatever income records you have, even just app payout summaries.

- Get the levy reviewed free before the 21-day hold runs out. Use the 2-minute form or call (888) 825-7779 — whether the debt is yours or your parent's, the review maps which release path moves fastest for your exact facts.

For primary-source detail, see the IRS's own pages on payment plans and installment agreements and paying the IRS. If the levy is causing hardship the IRS won't address, the independent Taxpayer Advocate Service can intervene.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.